Summary

Summary

- Praxair reported strong Q3 2017 results on October 26, 2017 and provided an update on its proposed merger with Linde.

- The successful completion of the Praxair Linde merger in the 2nd half of 2018 will make the combined entity the largest player in the industry.

- Air Products reported strong Q4 and FY2017 results from continuing operations. With its strong balance sheet management expects to invest over $8B over the next three years.

- In FY2017, Air Products divested non-core assets through the spin-off of Versum Materials and the sale of Performance Materials.

- Both companies are expensive at current levels. I will monitor both companies with the intent of eventually acquiring shares in both companies when they are more attractively valued.

Introduction

In the early 1990s, when I was in the Commercial Banking division of a major Canadian financial institution, I had a client who owned a small industrial gases company. One day he came to my office to inform me his major supplier (Messer Griesheim GmbH) had presented him with an offer that was beyond his, and my, wildest dreams.

This was long before the advent of the internet and discount brokers. In addition, my wife and I had just bought a house and paying off the mortgage was our primary focus. As a result, I had no surplus money to invest and researching companies back then was not easy. Had I had money to invest and easy access to material for investment analysis purposes I suspect I might have looked into investing in companies in the industrial gases industry.

Fast forward about 2.5 decades and you think that with the number of times I have seen the Praxair (NYSE: PX), Air Products (NYSE: APD), Linde (OTCMKTS: LNAGF), Air Liquide (OTCMKTS:AIQUY), and Airgas (acquired by Air Liquide) names I might have taken a moment or two to investigate the possibility of acquiring shares in some of these companies. Alas, I never did. Instead, I ended up investing in these highly recognizable names over the course of time.

Recently I was skimming through Fortune’s list of companies and PX (#275) and APD (#294) caught my attention. Their annual revenue is currently very similar but this could change in the second half of 2018 if PX’s proposed acquisition of LNAGF receives regulatory approval.

In today’s post I take a quick look at both companies to determine whether they are priced appropriately to warrant adding them to the Financial Freedom is a Journey portfolio.

PRAXAIR

Business Overview

PX’s Vision, Mission, and Core Values can be found here.

PX, founded in 1907 and headquartered in Danbury, Connecticut, has operations in North and South America, Asia and Europe. Its primary products are atmospheric gases (oxygen, nitrogen, argon and rare gases) and process gases (carbon dioxide, helium, hydrogen, electronic gases, specialty gases and acetylene). It serves customers in approximately 25 industries as diverse as health care and petroleum refining, computer-chip manufacturing and beverage carbonation, fiber-optics and steel making, and aerospace, chemicals, and water treatment.

Approximately 56% of PX’s 2016 sales were outside the US. It is concentrating on emerging markets, including Asia, Mexico, Middle East and Russia, and several less capital-intensive, faster-growing global markets, such as health care, electronics and energy, in addition to core industrial gases.

Source: PX Investor Presentation Q3 2017 October 26, 2017

Source: PX Investor Presentation Q3 2017 October 26, 2017

On December 20, 2016 PX and LNAGF announced their intent to merge. The merger of these companies would result in a global company with ~$29B in annual revenue and a more balanced portfolio.

Source: PX August 31, 2017 Proposed Merger Investor Presentation

Source: PX August 31, 2017 Proposed Merger Investor Presentation

Risk Factors

A comprehensive explanation of the company’s risk factors can be found on pages 15 – 19 in PX’s 2016 Annual Report.

Q3 2017 Results

On October 26, 2017, PX released its Q3 results for the quarter ending September 30, 2017. PX reported record free cash flow in Q3 which allowed it to reduce debt by $0.202B and to reward shareholders with $0.225B in dividends. PX has reduced share count from 302 million in 2012 to 288 million in 2016 but share buybacks have been placed on hold pending the outcome of the proposed merger.

A comparison of PX’s historical sales growth, diluted EPS growth, diluted EPS and free cash flow per share is likely going to be of little benefit in your investment decision making process because if the PX and LNAGF transaction is consummated in the second half of 2018, future results will be dramatically different from historical results. I am, therefore, restricting the level of data provided to 2016 and 2017.

Source: PX Q3 2017 Investor Presentation October 26, 2017

Source: PX Q3 2017 Investor Presentation October 26, 2017

Dividend and Dividend Yield

PX has raised its dividend for 24 consecutive years. Its dividend and stock split history can be found here. Investors have certainly been rewarded with a CAGR dividend growth rate well in excess of inflation for the last several years.

Source: Morningstar

Source: Morningstar

PX’s current ~2.1% dividend yield can be found here.

Valuation

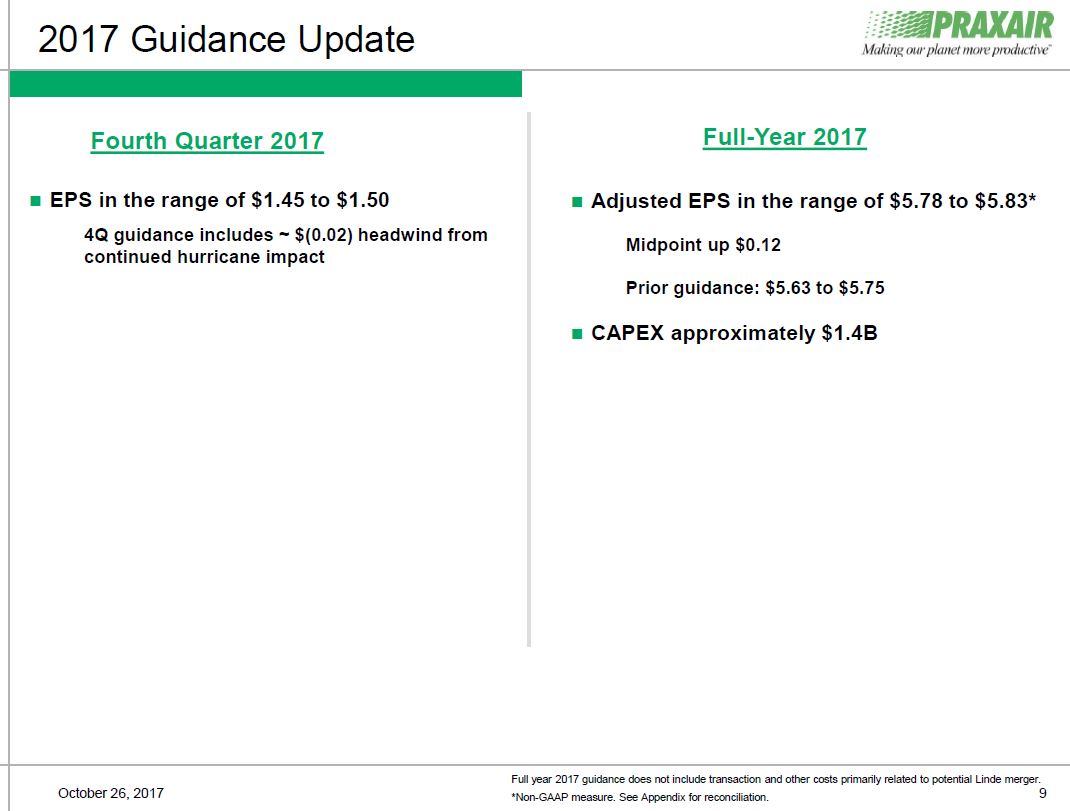

PX’s 2017 EPS guidance is as follows

Source: PX Q3 2017 Investor Presentation October 26, 2017

Source: PX Q3 2017 Investor Presentation October 26, 2017

and the current mean FY2017 adjusted EPS projections from various brokers is $5.78.

Source: TD WebBroker

Source: TD WebBroker

On November 10, 2017, PX closed at $148.28. Using the $5.78 estimate from above, the forward PE is ~25.7. I view this as beyond a prudent level and am prepared to patiently wait for a pullback to the ~21 – 22 PE range; here’s hoping for a market correction. A price at or below ~$125 would really spark my interest.

Source: Morningstar

Source: Morningstar

AIR PRODUCTS

AIR PRODUCTS

Business Overview

APD’s Goal and Roadmap can be found here.

APD, founded in 1940 in Allentown, Pennsylvania, is a leading producer of industrial gases. It provides atmospheric and process gases and related equipment to refining and petrochemical, metals, electronics, and food and beverage companies. In addition, it is a leading supplier of liquefied natural gas process technology and equipment.

Source: APD September 12, 2017 Credit Suisse 30th Annual Basic Materials Conference Presentation

Source: APD September 12, 2017 Credit Suisse 30th Annual Basic Materials Conference Presentation

APD’s company history can be found here. In operates in various regions of the world and is engaged in profitable joint ventures with leadership positions in emerging markets.

Source: APD September 12, 2017 Credit Suisse 30th Annual Basic Materials Conference Presentation

Source: APD September 12, 2017 Credit Suisse 30th Annual Basic Materials Conference Presentation

Risk Factors

A comprehensive explanation of the company’s risk factors can be found on pages 20 – 25 in the full PDF version of APD’s 2016 Annual Report.

FY2017 Results and FY2018 EPS Outlook

On October 26, 2017, APD released its Q4 and FY2017 results as at September 30, 2017.

Source: APD Q4 and FY2017 October 26, 2017 Earnings Conference Call Presentation

Source: APD Q4 and FY2017 October 26, 2017 Earnings Conference Call Presentation

As previously indicated in this post, comparing PX’s Q3 2017 results with historical results is likely of little value in the current exercise since the company is going to change dramatically in the second half of 2018 if the necessary approvals are granted re: PX and LNAGF merger.

In the case of APD, it has executed its strategic plan to restructure the Company to focus on its core Industrial Gases business. Significant cost reduction and asset actions were undertaken as part of this reorganization, and therefore, the results presented below are GAAP financial measures which have been adjusted to exclude certain disclosed items APD deem to be not representative of the underlying business performance. As a result, the numbers presented make it difficult to directly compare APD and PX results.

The FY2018 outlook is provided on a non-GAAP continuing operations basis. Certain items APD deems to not be representative of its underlying business performance have been excluded. Management has specifically stated that for various reasons it is unable to reconcile, without unreasonable effort, the forecasted range of adjusted EPS on a continuing operations basis to a comparable GAAP range.

Source: APD Q4 and FY2017 October 26, 2017 Earnings Conference Call Presentation

Source: APD Q4 and FY2017 October 26, 2017 Earnings Conference Call Presentation

In addition, APD’s guidance excludes the Lu’An Clean Energy Project expansion and any other significant acquisitions.

Source: APD September 12, 2017 Credit Suisse 30th Annual Basic Materials Conference Presentation

Source: APD September 12, 2017 Credit Suisse 30th Annual Basic Materials Conference Presentation

Dividend and Dividend Yield

You can access APD’s dividend history here and stock split history here. Investors have certainly been rewarded with a CAGR dividend growth rate well in excess of inflation for the last several years. This growth, however, is ~330 bps short of that experienced with an investment in PX over the same time frame.

Source: Morningstar

Source: Morningstar

APD’s current ~2.37% dividend yield can be found here.

Valuation

APD’s 2017 EPS guidance is as follows:

Source: APD Q4 and FY2017 October 26, 2017 Earnings Conference Call Presentation

The mid-point of APD’s forecast is $6.95 and the current mean FY2017 adjusted EPS projections from various brokers is $7.04.

Source: TD WebBroker

Source: TD WebBroker

On November 10, 2017, APD closed at $160.30. If I am conservative and use APD’s $6.95 mid-point of its guidance I arrive at a ~23 forward PE. While slightly more reasonable than PX’s valuation, I will exercise patience and will wait for a pullback to ~$150. This would result in a ~21.6 forward PE which appears to be reasonable relative to recent historical levels.

Source: Morningstar

Source: Morningstar

Praxair and Air Products Stock Analysis – Final Thoughts

Both companies appeal to me. My concern is they are trading at levels slightly in excess of what I am prepared to pay.

Should my long awaited market correction ever occur I will need to reassess the attractiveness of these two companies relative to other companies which will likely also get caught in any downdraft. If I deem these companies to be worthwhile additions to our overall holdings I would, in all likelihood, invest in both companies after which time I will no longer be embarrassed to state that “I’ve got gas”.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this post. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I currently do not hold a position in PX or APD and do not intend to initiate a position within the next 72 hours unless the price drops to my target levels.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.