In my May 2 2024 post, I disclosed that Paycom’s (PAYC) attractive valuation prompted me to acquire additional shares @ ~$163 thus bringing my exposure to 700 shares in a ‘Core’ account within the FFJ Portfolio. At the time of that post, the most currently available financial information was for Q1 2024 and the Q2 and FY2024 outlook. After the October 30, 2024 market close, PAYC released its Q3 and YTD2024 results and FY2024 outlook thus prompting me to revisit this existing holding.

Unfortunately, PAYC’s share price of ~$167 at the October 30 market open has risen to $210.65 at the November 1 market close.

Many PAYC shareholders might welcome this higher share price. I, however, am somewhat disappointed even though my average cost is ~$236.34. In this brief post I explain why.

Business Overview

I have provided a brief business overview in prior posts. The best sources of information to learn about the company, however, are PAYC’s website and the FY2023 Annual Report/Form 10-K.

Financials

Q3 2024 Results

Details of PAYC’s Q3 results are accessible here and in the Q3 2024 Form 10-Q.

Q4 and FY2024 Outlook

PAYC’s Q4 outlook is:

- Total Revenues of $0.477B – $0.484B or ~9% growth at the midpoint which is comparable to Q2 2023.

- Adjusted EBITDA of $0.1845B – $0.1915B or a ~35% margin at the midpoint of the range.

Its FY2024 outlook is unchanged from the previously provided outlook:

- Total Revenues of $1.866B – $1.873B or ~11% YoY growth at the midpoint.

- Adjusted EBITDA of $0.745B – $0.752B or a ~39% margin at the midpoint of the range.

On the Q3 earnings call, management stated:

On the float revenue, for every 25 basis point cut, it could impact us as much as $6 million on an annualized basis. And we’ve already seen 50 basis point cut, maybe a couple more this year.

So as we’re looking into next year, that’s going to be something that’s going to impact us but we’re starting to also look at layering in some more longer term on that float balances.

This is something Automatic Data Processing (ADP) does. It has a core component of funds held for clients which can be invested for a longer term thus allowing it to capture additional yield.

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

Historically, I have not deducted the stock based compensation (SBC) reflected in the Consolidated Statements of Cash Flows to determine OCF and FCF; the figures reflected below do not deduct PAYC’s annual SBC.

- OCF was (in millions of $) 22.34, 42.97, 98.95, 130.60, 184.82, 224.26, 227.21, 319.36, 365.10, and 485.04. YTD OCF is 373.513.

- CAPEX was (in millions of $) 14.27, 16.55, 43.81, 59.39, 59.91, 92.93, 94.10, 126.19, 136.80, and 196.83. YTD CAPEX is 141.536.

- FCF was (in millions of $) 8.07, 26.42, 55.01, 70.76, 124.91, 131.33, 133.11, 193.17, 228.31, and 292. YTD FCF is 231.977.

After giving the matter much consideration, I am going to start adjusting a company’s OCF so that SBC is NOT added back. My reasoning for doing so is covered in my How Stock Based Compensation Distorts Free Cash Flow post. By making this adjustment, my OCF and FCF will differ from many other online sources going forward; my figures will be more conservative.

Typically, the SBC line item is a positive number so by removing it from my calculation, the OCF drops.

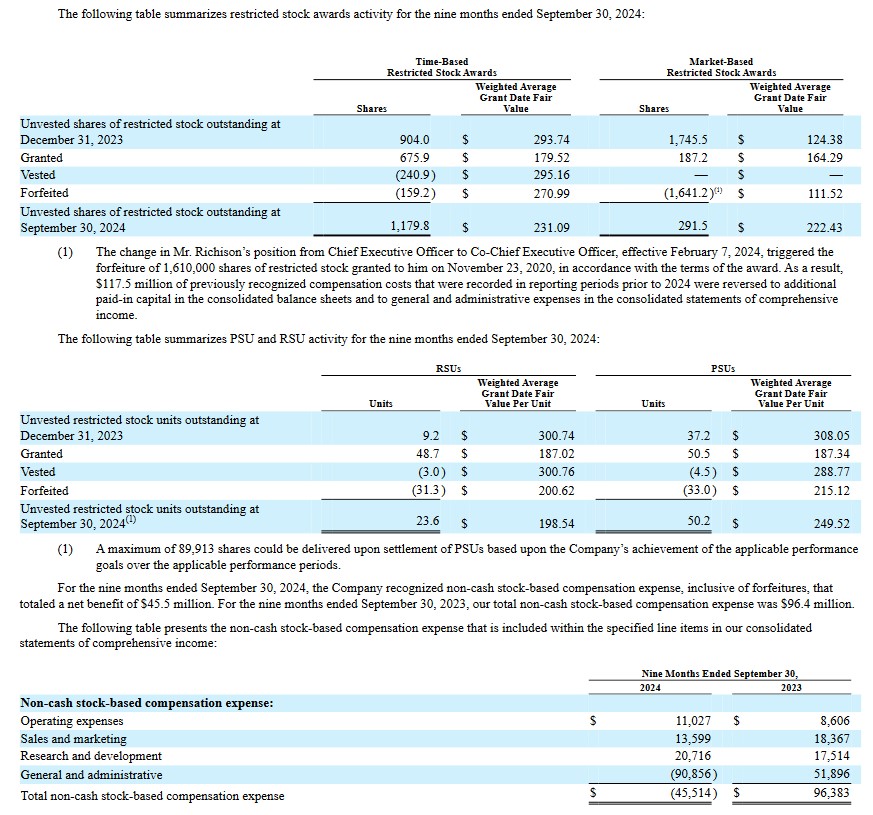

In the first 9 months of Fy2024, however, PAYC’s SBC is ($45.514)…a negative number!

The following, extracted from the Q3 2024 Form 10-Q, explains why this figure is negative.

If I exclude this negative YTD2024 SBC line item, the YTD OCF increases to $419.027 million. Subtract the YTD CAPEX of $141.536 million and YTD FCF increases to $277.491 million from $231.977 million reflected earlier.

Were it not for the forfeiture of 1,610,000 shares of restricted stock, I would deduct $45.342 million ($11.027 + $13.599 + $20.716) to arrive at PAYC’s YTD OCF.

In Q4, management expects SBC of ~$27 million. The FY2024 total non-cash SBC expense will likely be (~$18.514 million).

A major component of PAYC’s YTD2024 CAPEX was the construction of its 5th building in Oklahoma City. This building is now in service.

Total FY2024 CAPEX as a percent of revenues in FY2024 will be ~12% versus 11.3% in FY2023. This is expected to drop slightly below 10% in FY2025.

Return On Invested Capital (ROIC)

In FY2014 – FY2023, PAYC’s ROIC (%) was 8.53, 19.14, 32.75, 42.53, 50.94, 39.04, 23.03, 24.35, 26.56, and 27.53.

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. In the past 7 fiscal years, PAYC’s ROIC has exceeded 20%!

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

Risk Assessment

PAYC has no debt.

At the end of Q3, PAYC had ~$0.326B in cash and cash equivalents. Current liabilities before client funds obligation (excluding deferred revenue of $27.6 million) was ~$0.191B.

At FYE2023, it had ~$0.294B of cash and cash equivalents. Current liabilities before client funds obligation (excluding deferred revenue of ~$29 million) was ~$0.184B.

The short-term and long-term deferred revenue represents funds received from clients in advance of providing services.

Dividends and Share Repurchases

Dividend and Dividend Yield

PAYC has a brief dividend history having distributed its first quarterly dividend on June 12, 2023.

On October 28, PAYC announced that its Board declared a cash dividend in the amount of $0.375/share to be paid on December 9, 2024 to all stockholders of record as of the close of business on November 25, 2024.

Dividend metrics are of little relevance in my investment decision making process. I would much rather a company retain funds to grow the business if this is the most beneficial means by which to allocate capital.

Share Repurchases

The weighted average diluted shares outstanding in FY2021 – FY2023 is 57.974, 58.175, and 58.191 million and 55.964 million in Q3 2024.

In May 2016, PAYC’s Board authorized a stock repurchase plan allowing for the repurchase of shares of common stock in open market transactions at prevailing market prices, in privately negotiated transactions or by other means in accordance with federal securities laws.

In July 2024, PAYC’s Board authorized the repurchase of up to $1.5B of common stock. As of September 30, 2024, there was $1.49B available for repurchases under the stock repurchase plan. This current stock repurchase plan will expire on August 15, 2026.

In the first 9 months of FY2024, PAYC repurchased an aggregate of 892,669 shares at an average cost of $153.70/share. This includes 80,464 shares withheld to satisfy tax withholding obligations for certain employees upon the vesting of equity incentive awards.

In comparison, PAYC repurchased an aggregate of:

- 1,495,752 shares at an average cost of $200.93/share, including 51,119 shares withheld to satisfy tax withholding obligations for certain employees upon the vesting of equity incentive awards in FY2023.

- 364,667 shares at an average cost of $273.74/share, including 17,355 shares withheld to satisfy tax withholding obligations for certain employees upon the vesting of the restricted stock in FY2022.

Because the investor community was short sighted thus resulting in a depressed stock price, PAYC was able to acquire a significant number of undervalued shares!

Now that the share price has bounced back, the ‘window of opportunity’ has closed.

Valuation

On May 2, I acquired an additional 100 shares @ ~$163. Using this purchase price and PAYC’s current forward-adjusted diluted EPS broker estimates, PAYC’s forward adjusted diluted PE levels were:

- FY2024 – 20 brokers – ~21 using the mean of $7.72 and low/high of $6.82 – $8.02.

- FY2025 – 20 brokers – ~18.6 using the mean of $8.78 and low/high of $7.81 – $9.53.

- FY2026 – 6 brokers – ~15.6 using the mean of $10.48 and low/high of $9.79 – $10.87.

In Q1 alone, PAYC generated ~$101 million of FCF. I estimated that PAYC might generate ~$75 million of FCF in each of the next 3 quarters thus leading to FY2024 FCF of ~$326 million.

The weighted average diluted shares outstanding in Q1 was 56.552 million. PAYC expected its quarterly stock-based compensation expense to be ~$33 million for the remainder of FY2024. If it repurchased shares at an average price of $185, this amounts to ~178 thousand shares quarterly or ~534 thousand for the remainder of FY2024. If we conservatively estimate the weighted average diluted shares outstanding in FY2024 drops to 56.3 million and use ~$326 million of FY2024 FCF, we arrive at a FCF/share of ~$5.80. Divide the ~$163 share price by ~$5.80 and we get a forward P/FCF of ~28.

PAYC’s depressed valuation allowed the company to aggressively repurchase shares. The recent share price increase to ~$210.65 completely changes PAYC valuation!

YTD, PAYC has generated $6.89 of diluted EPS and $5.89 of adjusted diluted EPS. If it were to generate ~$9.20 of diluted EPS and ~$7.85 of adjusted diluted EPS in FY2024, the current forward P/E would be (using a ~$210.65 share price) ~23 and the current forward adjusted diluted PE would be ~27.

Using PAYC’s current forward-adjusted diluted EPS broker estimates, its forward adjusted diluted PE levels are:

- FY2024 – 20 brokers – ~26.6 using the mean of $7.92 and low/high of $7.73 – $9.18.

- FY2025 – 20 brokers – ~23.9 using the mean of $8.83 and low/high of $8.18 – $10.68.

- FY2026 – 11 brokers – ~21.2 using the mean of $9.94 and low/high of $8.85 – $12.36.

PAYC has no debt, its FY2025 CAPEX as a percentage of revenue is expected to be lower in FY2025, and it generates strong FCF. If its share price were to stay depressed, it could continue to make a significant dent to the weighted average diluted shares outstanding. Compare how many shares it was able to repurchase in FY2022, FY2023, and YTD2024 (see Share Repurchases section above).

If PAYC’s share price does not retrace to much lower levels, $1 of share repurchases will not go as far as it did when the share price was depressed. This is why I am disappointed.

Final Thoughts

As noted in several previous posts, the time to acquire shares in great companies is when they experience temporary challenges and the investment community sours on the company.

I currently hold 700 shares in a ‘Core’ account within the FFJ Portfolio. Unless I complete another portfolio review, I can only surmise that PAYC is a top 20 holding; I intend to complete such a review at the end of 2024.

I was premature in my decision to invest in the company. My average cost of ~$236.34 means I am still currently ‘under water’. While I could lower my average cost by acquiring additional shares, I am not adding to my exposure because I think shares are almost fairly valued following the share price surge.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long PAYC and ADP.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.