I last reviewed Genuine Parts Company (GPC) in my guest post at Dividend Power. At the time, GPC had recently released FY2020 results and FY2021 guidance. In that post, I concluded GPC was a slightly overvalued Dividend King.

We now have Q3 and YTD2022 results. With just under a month before FYE2022, I revisit GPC to gauge its valuation.

Please visit the company’s website and read Part 1 in the FY2021 Form 10-K if you are unfamiliar with GPC.

Financials

Q3 and YTD2022 Results

Please refer to GPC’s Q3 Earnings Release, Form 10-Q, and Earnings Presentation.

Q3 highlights include:

- Total sales of $5.7B, up 18% from Q3 2021;

- Adjusted EPS of $2.23, up 19% from Q3 2021;

- Record quarterly sales for the automotive and industrial segments and GPC’s 6th consecutive quarter of double-digit sales growth;

- Operating margin expansion in both segments; and

- Record quarterly earnings and the 9th consecutive quarter of double-digit earnings growth.

The ongoing integration of KDG (acquisition closed on January 4, 2022) continues to create significant value.

GPC’s automotive and industrial businesses continue to take advantage of several industry tailwinds.

- Automotive: the increase in year-to-date miles driven, increase in the average age of vehicles, limited new car inventory and elevated used car prices are all supportive of healthy demand in the aftermarket.

- Industrial: manufacturing and the economy remain expansionary with the Purchasing Managers’ Index (PMI) holding at greater than 50%. Industrial production just had its 9th straight quarter of growth, up 2.9% YoY.

NOTE: The PMI is an index of the prevailing direction of economic trends in the manufacturing and service sectors.

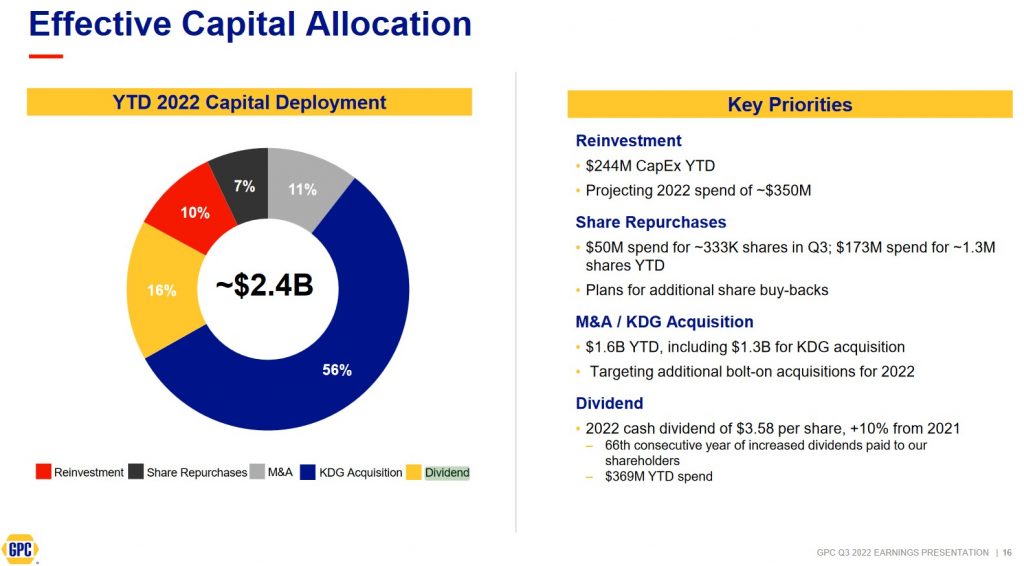

In Q3, GPC invested $91 million in CAPEX. This investment was primarily in technology and other projects to further automate and consolidate the company’s distribution networks and improve productivity.

GPC also completed several bolt-on acquisitions in the quarter consisting primarily of small automotive store groups that increased local market density in key geographies.

Recent acquisitions in Germany, Spain and Portugal are tracking well and internal expectations are being exceeded.

The M&A pipeline continues to be active and the plan is to continue to make bolt-on acquisitions to create value and add to local market coverage.

Important information regarding GPC’s Financial Condition and Liquidity and Capital Resources is found on pages 21 and 22 of 28 in the Q3 2022 Form 10-Q.

FY2022 Outlook

The outlook for Cash from Operations and Free Cash Flow (FCF) has not changed since the beginning of the current fiscal year. The other metrics, however, have been revised upwards each quarter in FY2022. The following reflect the changes.

Credit Ratings

In October 2020, Moody’s and S&P Global initiated coverage. GPC’s unsecured long-term debt ratings remain unchanged from when first introduced.

- Moody’s: Baa1 (stable outlook)

- S&P Global: BBB (stable outlook)

Moody’s rating is the top tier of the lower medium grade. S&P Global’s rating is the middle tier of the lower medium grade. Both ratings are investment grade and are defined as an obligor having ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Both ratings are satisfactory for my purposes.

GPC closed Q3 2022 with $2.1B in available liquidity. Its debt to adjusted EBITDA is 1.7x which compares favourably to the company’s targeted range of 2 – 2.5x.

The following reflects the changes in GPC’s Balance Sheet, liquidity, and debt maturity schedule over time.

Source: GPC – Q3 2022 Earnings Presentation

Source: GPC – Q4 2021 Earnings Presentation

Source: GPC – Q4 2020 Earnings Presentation

Dividends and Share Repurchases

Dividend and Dividend Yield

GPC prides itself on:

- having distributed a cash dividend to shareholders every year since going public in 1948; and

- its 66 consecutive years of dividend increases.

We see that the dividend makes up a sizable percentage of GPC’s capital allocation.

GPC’s dividend history on its website is currently outdated. This dividend history is more accurate.

On January 4, 2023, GPC is scheduled to distribute its 4th quarterly $0.895/share dividend. In early March, I anticipate GPC will announce a $0.03 – $0.04 increase in the quarterly dividend to ~$0.93/share. On this basis, and using GPC’s current ~$187.30 share price, the forward dividend yield is ~2%.

When I initiated a GPC position in July 2017, the dividend yield was 3.26%.

The dividend yield was ~3% when I wrote my March 9, 2021 guest post.

In GPC’s Q3 2022 earnings presentation, page 2 of 27 reflects a 2.4% trailing 12-month dividend yield.

Share Repurchases

GPC’s weighted average shares outstanding in FY2012 -FY2021 and the first 9 months of FY2022 are (in millions of shares) 156, 156, 154, 152, 150, 148, 147, 146, 145, 144 and 142.4.

The company expects to remain active in its share repurchase program. However, the amount and value of shares repurchased will vary and is at the discretion of the Board.

Valuation

When I last reviewed GPC, its FY2021 adjusted diluted EPS guidance was $5.55 – $5.75. Using the current $109.20 share price, the forward adjusted diluted PE range was ~19 – ~19.7.

The FY2021 mean, low, and high adjusted diluted EPS guidance from 12 brokers was $5.72, $5.49, and $5.90 thus giving us a mean adjusted diluted PE of ~19 and a ~18.51 – ~19.9 range.

Although GPC had narrowed its focus on sustainable, value-driving initiatives associated with the faster-growing and higher-margin automotive and industrial businesses, I was of the opinion that an adjusted diluted PE of ~16 and below was a more appropriate valuation at which to acquire shares. On this basis and using the mean $5.72 guidance from analysts and the $5.65 mid-point of GPC’s guidance, a price in the low $90s was a level at which I would consider adding to my GPC exposure.

Prior to the release of Q3 and YTD2022 results on October 20, GPC’s share price was in the range of ~$155. Management’s adjusted diluted EPS guidance was $7.80 – $7.95 ($7.875 mid-point) thus giving us a forward adjusted diluted PE of ~19.7.

In just 1.5 months following the latest earnings release, GPC’s share price has risen to the current ~$187.30 level. We now have management’s revised guidance for FY2022 of $8.29 – $8.39 of diluted EPS and $8.05 – $8.15 of adjusted diluted EPS. On this basis, GPC’s valuation on a GAAP basis (using the $8.34 mid-point) is ~22.46 and ~23.1 (using the $8.10 mid-point) on an adjusted basis.

GPC’s forward-adjusted diluted PE levels using current broker estimates is:

- FY2022 – 13 brokers – mean of $8.17 and low/high of $8.10 – $8.28. Using the mean estimate, the forward-adjusted diluted PE is ~23.

- FY2023 – 13 brokers – mean of $8.60 and low/high of $8.30 – $9.13. Using the mean estimate, the forward-adjusted diluted PE is ~21.8.

- FY2024 – 6 brokers – mean of $9.22 and low/high of $9.00 – $9.68. Using the mean estimate, the forward-adjusted diluted PE is ~20.3.

The valuation based on current forward-adjusted diluted earnings estimates is currently greater than at the time of my prior reviews.

Final Thoughts

I like GPC’s long-term outlook and initiated a 300-share position @ $82.22 in one of the ‘Core’ accounts within the FFJ Portfolio which I disclosed in my July 24, 2017 post.

The quarterly upwards revision of various FY2022 Outlook line items is encouraging and I would like to increase my current 349 share exposure. However, I do not recommend the purchase of GPC shares because of its current valuation; I think the current valuation leaves little margin for error.

If we give GPC the benefit of the doubt that it will generate adjusted diluted EPS of $8.15 in FY2022 (the top of management’s guidance) and assign a generous ~19 PE, then a price in the mid $150s seems more appropriate.

As noted in prior posts, a common theme in most earnings call transcripts I read is the expression of concern by senior executives about a challenging economic environment and a potentially difficult 2023. If 2023 turns out to be difficult, I do not know how GPC can not be affected. I prefer to selectively acquire shares in great companies that are currently experiencing headwinds and which have fallen out of favour with investors.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long GPC.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.