I currently have insignificant PepsiCo, Inc. (PEP) exposure within a retirement account for which I do not disclose details.

As evidence of how little interest I have in this company, I have not reviewed this holding since this July 12, 2022 post.

I strongly suspect that world-class athletes rarely consume PEP products. People who lead a sedentary lifestyle, however, are apt to be PEP product consumers.

You don’t have to be a Mensa member (the High IQ society that includes people who score in the top 2% where the IQ is usually 132+) to realize that PEP products should be avoided. Let’s be perfectly honest. Almost every PEP product is not fit for human consumption despite having received FDA approval (US Food and Drug Administration).

If you are inclined to invest in PEP, approach it this way. Invest in:

- PEP if you want to benefit from the addictive and unhealthy nature of its products; and

- healthcare-related companies such as Intuitive Surgical (ISRG), Thermo Fisher (TMO), Danaher (DHR), and Becton Dickinson (BDX). In all probability, the regular consumption of PEP products is very likely to lead to PEP consumers requiring the products/services from these healthcare companies.

Let’s move on to why I have negligible exposure and why I might even exit PEP when I have to withdraw funds from our retirement accounts in 2025 as part of our Registered Retirement Savings Plan (RRSP) meltdown strategy.

Business Overview

I strongly suspect you are familiar with PEP to some extent. If you want to delve into the company a bit further, I suggest reviewing the company’s website and Part 1 of the most recent Form 10-K.

Financial Review

Q3 and YTD2024 Results

PEP released its Q3 and YTD2024 results on October 8, 2024 for the 36 weeks ending on September 7, 2024. You can access the information here.

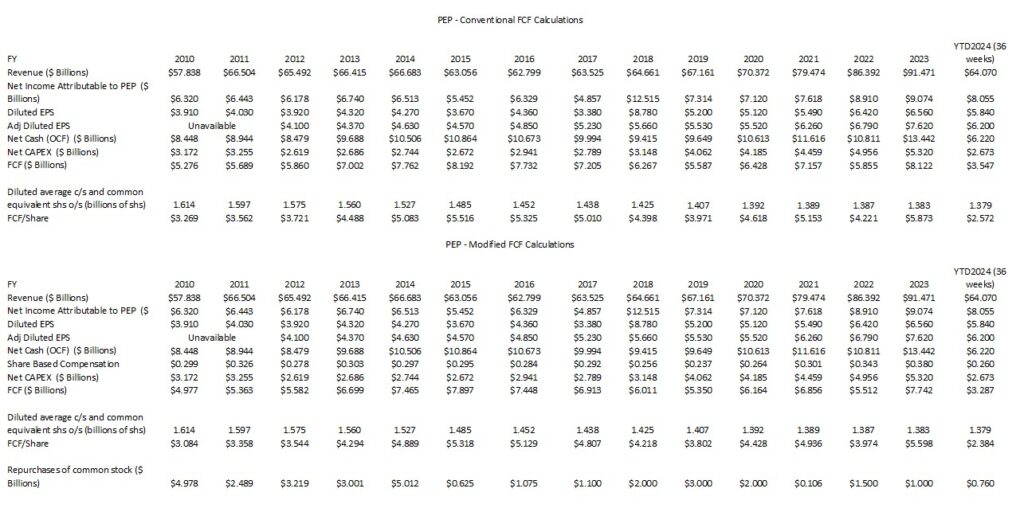

If you look at PEP’s results over the past several years, you may notice the following line items often crop up in the Condensed Consolidated Statement of Cash Flows:

- Impairment and other charges ($3.618B and $1.23B in FY2022 and FY2023);

- Restructuring and impairment charge ($0.411B and $0.445B in FY2022 and FY2023);

- Cash payments for restructuring charges ($0.224B and $0.434B in FY2022 and FY2023);

- Product recall-related impact ($0.184B YTD2024); and

- Cash payments for product recall-related impact ($0.138B YTD2024).

These are but a few examples. If you look at the financial statements going back to 2010, for example, these types of charges are a regular occurrence.

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2010 – YTD2024)

In several recent posts including my most recent Adobe – Conventional Free Cash Flow Calculation Is Misleading, I touch upon why I am now taking a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. As explained in prior recent posts, I think we need to look at FCF using the conventional method AND a modified method; the modified method also deducts share-based compensation.

PEP’s SBC is not that significant in the grand scheme of things so the FCF results calculated using both methods does not reflect that much of a variance. Tech companies!? That is a whole different story. Look at my Adobe post to see the extent to which SBC impacts FCF.

FY2024 Outlook

With the release of Q3 and YTD2024 results, PEP provide the following outlook.

- A low-single-digit increase in organic revenue (previously ~4% organic revenue growth).

There was no change in the following provided in prior guidance:

- At least an 8% increase in core constant currency EPS;

- A core annual effective tax rate of 20%;

- Total cash returns to shareholders of ~$8.2, comprised of dividends of $7.2B and share repurchases of $1.0B;

- A ~1% FX translation headwind to impact reported net revenue and core EPS growth based on current market consensus rates; and

- FY2024 core EPS of at least $8.15, a 7% increase compared to FY2023 core EPS of $7.62.

Risk Assessment

I look at a company’s senior unsecured long-term debt and rating outlook to gauge the degree of risk I am assuming as a shareholder.

The current unsecured long-term debt ratings assigned to PEP are:

- Moody’s: A1 rating with a stable outlook affirmed on June 20, 2024.

- S&P Global: A+ rating with a stable outlook affirmed on October 21, 2024.

- DBRS Morningstar: A (high)

All 3 ratings are the top tier of the upper medium-grade investment-grade category. They define PEP as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

These ratings are satisfactory for my purposes.

Dividends and Share Repurchases

Dividend and Dividend Yield

PEP’s dividend history is accessible here.

PEP has paid consecutive quarterly cash dividends since 1965, and the recently declared dividend marks the 52nd consecutive year in which it has increased its dividend thereby making it a ‘Dividend King’. A Dividend King is a company that has increased its dividend for at least 50 consecutive years.

Another Dividend King I recently reviewed is Emerson Electric (EMR). Unlike EMR, which is struggling to maintain its Dividend King status, PEP is not facing the same issue and its annual dividend increases are more meaningful.

If we compare PEP’s dividend distributions to the amount expended toward share repurchases, it is readily apparent that dividend distributions are a higher priority.

In FY2018 – YTD2024 it distributed dividends of just under $40B. On the other hand, it repurchased shares in the amount of ~$10.366B during the same period.

I think investing based on dividend metrics is fundamentally flawed. Instead, the focus should be on a company’s capital allocation that produces attractive total investment returns. In some cases, reinvesting in the company is preferable and in other cases, repurchasing undervalued shares is optimal.

Once investors become accustomed to a consistent increase in the dividend, this is the type of investor base a company will attract. Should a company’s Board eventually deem it more appropriate to allocate more capital toward share repurchases by perhaps lowering/freezing or approving a negligible dividend increase, the company’s investor base would likely react negatively leading to a share price correction.

Share Repurchases

We see from the table reflected earlier that the extent to which PEP repurchases shares has been all over the map since FY2010.

You would like to think that a company would ramp up its share repurchases when the company considers its shares to be undervalued. This, however, does not always happen.

PEP shares were undervalued in 2016, 2023, and 2024. Did PEP ramp up its share repurchases? No. Perhaps this is because PEP prioritizes the dividend.

Valuation

In the first 36 weeks of FY2024, PEP generated $5.84 of diluted EPS and $6.20 of adjusted diluted EPS. If it were to generate ~$7.80 in diluted EPS for FY2024, the current PE, using a ~$158 share price, is ~20.3.

NOTE: PEP intends to repurchase $1.0B of its shares in FY2024 and it has only repurchased $0.76B YTD. The diluted average common stock outstanding in FY2024 should, therefore, be slightly lower than the YTD figure reflected in the table above. In addition, the YTD adjusted diluted EPS is $6.20 yet PEP’s FY2024 outlook is for at least $8.15. I do not, expect a variance between FY2024 GAAP and non-GAAP EPS to be greater than $1/share. If I am correct, PEP’s GAAP EPS should be at least ~$7.15 and the current forward diluted PE should be ~22.

Using the current adjusted diluted EPS estimates from the brokers which cover PEP, we get the following adjusted diluted PE levels.

- FY2024: 20 brokers, mean estimate $8.15, low/high range $8.14 – $8.18. Valuation using the mean estimate is ~19.4.

- FY2025: 20 brokers, mean estimate $8.62, low/high range $8.35 – $8.72. Valuation using the mean estimate is ~18.3.

- FY2026: 13 brokers, mean estimate $9.26, low/high range $8.96 – $9.45. Valuation using the mean estimate is ~17.1.

Looking at PEP’s valuation based on FCF, it has generated YTD FCF of ~$2.572/share and ~$2.384/share calculated using the conventional and modified methods. Suppose PEP generates ~$5.87 and ~$5.60 of FCF calculated using both methods; this is comparable to the prior fiscal year. With shares trading at ~$158, the P/FCF is ~27 and ~28.

Final Thoughts

PEP has not been one of my top 30 holding for over a year. I anticipate it will form a negligible percentage of my entire holdings when I complete my next Portfolio Review at the end of 2024.

Despite shares being slightly undervalued (a fair value appears to be in the mid-high $160s), I resign myself to capitalizing on PEP consumers once they require the use of products and services from my healthcare-related holdings.

I prefer to conserve liquidity to deploy toward increasing my exposure in superior companies when their valuations are attractive.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long PEP.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.