West Pharmaceutical’s (WST) recent share price behavior has given rise to concern by some shareholders. After reviewing the recently released Q2 and YTD2024 results and the transcript of the Q2 earnings call with analysts, my opinion about WST’s long term outlook is unchanged. WST remains a good long-term investment despite weaker than expected results and lowered FY2024 guidance.

Warren Buffett has often quoted his mentor, Ben Graham, as saying:

In the short run, the market is a voting machine – reflecting a voter-registration test that requires only money, not intelligence or emotional stability – but in the long run, the market is a weighing machine.

Here are my thoughts on WST.

Business Overview

I highly recommend referring to the company’s website and the FY2023 Form 10-K.

Financials

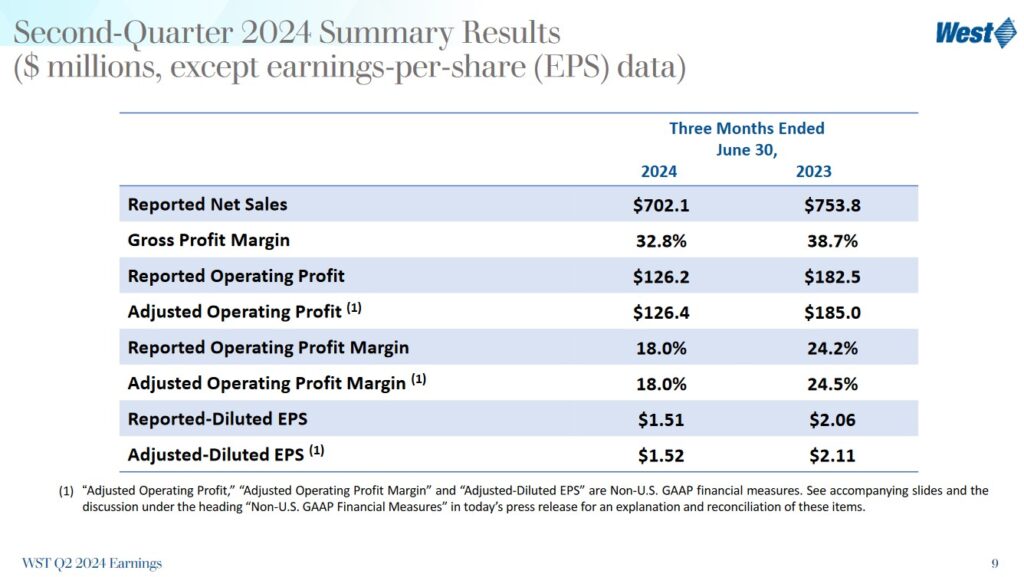

Q2 and YTD2024 Results

The Q2 Earnings Presentation and the Form 8-K and Form 10-Q are accessible at SEC Filings section of WST’s website.

Looking at the following summary results without understanding the recent weakness is likely to raise concerns. This is why it is so important to delve into the company’s financial statements. Making investment decisions merely based on share price behavior is foolish.

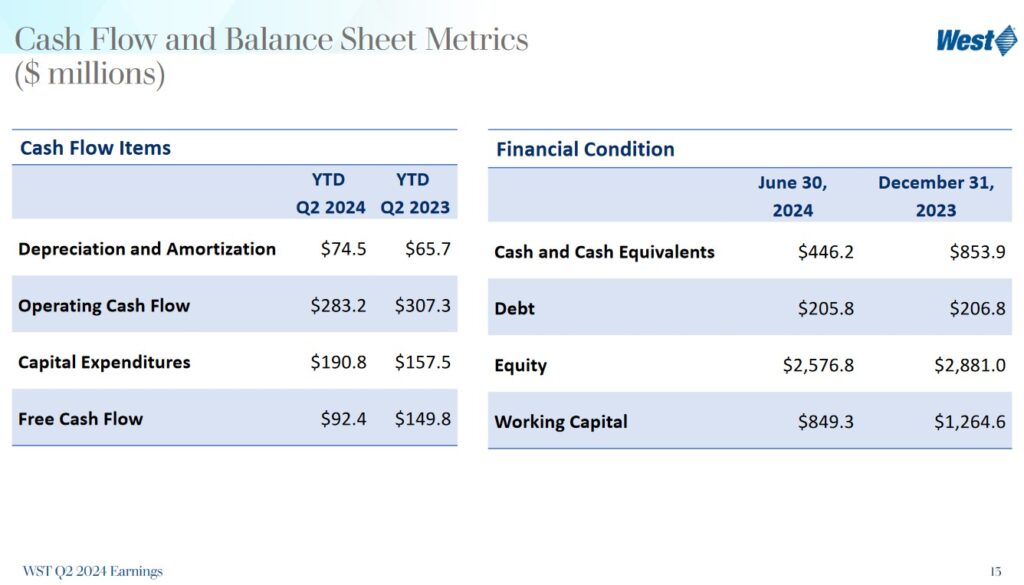

WST’s strong Balance Sheet enables it to weather short-term headwinds.

At the end of Q2 2024, WST’s cash balance of $446.2 million was $407.7 million lower than at FYE2023. This cash reduction and cash from operations was used to repurchase $454.1 million of shares and to fund CAPEX.

WST continues to invest in CAPEX to increase both high-value product and/or contract manufacturing capacity. YTD CAPEX is $190.8 million which is $33.3 million higher than the same period in FY2023. The major driver for this increase is that customers who have awarded business at WST’s Dublin facility have specifically asked that WST put additional capacity in place sooner than originally anticipated. Some of the CAPEX earmarked for FY2025, therefore, has been pulled forward to FY2024 to meet these requests.

Once the facilities currently under construction become operational in FY2025, annual CAPEX should return to pre-COVID levels; management is targeting CAPEX of 6%- 8% of revenues versus ~9%, ~10%, and ~12.3% of annual revenue in FY2021 – FY2023.

On the Q2 earnings call, management states:

We had a lower-than-expected second quarter impacted by continued customer destocking. That being said, we are seeing promising signs from our customers that give us confidence of a turning point in this trend.

Looking ahead, we expect the second half of the year to be stronger than the first half with a return to year-over-year organic growth in the fourth quarter, led by our Proprietary Products segment specifically Biologics.

WST’s confidence in its medium- to long-term outlook is underscored by its ongoing capital expansion projects. While these projects were originally undertaken to address COVID, these investments are now being repurposed to drive increased capacity to address new opportunities.

WST’s expansion plans are now focused on high-value products that provide a combination of increased manufacturing capacity and higher level of global standardization through WST’s network.

In Biologics, WST is witnessing increased customer interest for higher quality, lower particulate, and more standardized solutions given the changing global regulatory requirements. This favorably positions leading products such as Westar Select and NovaPure.

WST’s expansion projects remain on target to go into production by the end of Q3 2025. Unfortunately, WST’s major expansion is coinciding with ongoing customer destocking; customers had elevated elevated inventory levels because they wanted to ensure they did not run out of inventory during COVID.

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

In the FY2014 – FY2023 time frame, WST’s:

- OCF was (in B$) 0.18, 0.21, 0.22, 0.26, 0.29, 0.37, 0.47, 0.58, 0.72, and 0.78.

- CAPEX was (in B$) 0.11, 0.13, 0.17, 0.13, 0.10, 0.13, 0.17, 0.25, 0.28, and 0.36 .

- FCF was (in B$) 0.10, 0.09, 0.11, 0.17, 0.21, 0.26, 0.31, 0.52, 0.45, and 0.43.

YTD2024 cash from operations is ~$0.283B, YTD FCF is ~$0.191B, and YTD CAPEX is ~$0.092B.

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

WST’s FY2014 – FY2023 ROIC (%) was 10.61, 8.05, 11.14, 10.98, 13.82, 14.05, 17.23, 27.60, 20.77, and 18.6.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. WST’s has exceeded this level in the last few years.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

FY2024 Guidance

WST’s current FY2024 guidance is:

- Consolidated Net Sales: $2.87B – $2.9B

- Adjusted-Diluted EPS: $6.35 – $6.65

Prior FY2024 guidance was:

- Consolidated Net Sales: $3B – $3.025B

- Adjusted-Diluted EPS: $7.63 – $7.88

and before that, it was:

- Consolidated Net Sales: $3B – $3.025B

- Adjusted-Diluted EPS: $7.50 – $7.75

Risk Assessment

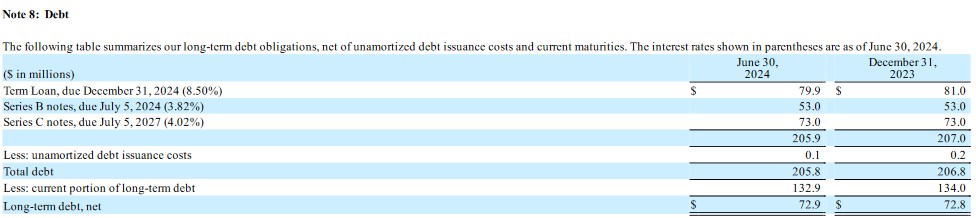

No rating agency rates WST’s debt. WST’s cash flow and balance sheet metrics, however, reflect a prudent use of debt.

The following reflects WST’s debt at the end of Q2 2024 and FYE2023.

On July 2, 2024, just after the end of Q2, WST amended its existing credit facility agreement that established an incremental term loan of $130.0 million that matures on July 2, 2027; the entire stated principal amount of the new Term Loan is due at maturity and there is no scheduled amortization prior to such date.

This facility was fully drawn at closing and together with cash on hand, proceeds from the new Term Loan were used to repay the Series B notes due July 5, 2024 and the Term Loan due December 31, 2024. Now, WST has no debt that matures prior to early July 2027!

Various financial covenants in WST’s debt agreements include the need to maintain established interest coverage ratios and to not exceed established leverage ratios. The agreements also contain other customary covenants, none of which are restrictive to WST’s operations. At the end of Q2 2024, WST complied with all debt covenants.

Dividends, Share Repurchases, and Stock Splits

Dividend and Dividend Yield

WST does have a dividend history. A WST investment, however, is typically not made for dividend income. This is a low dividend yielding company and the bulk of WST’s total long-term investment return is likely to continue to be derived from capital appreciation.

Share Repurchases

WST’s weighted average shares outstanding in FY2012 – FY2023 are (in millions of shares) 71.8, 71.4, 72.8, 73.8, 75, 75.8, 75.4, 75.4, 75.8, 76.3, 75.8, and 75.3. The diluted weighted average shares outstanding in Q2 2024 was ~73.7.

During the 3 months ended June 30, 2024 and 2023, there were 0.3 million and 0.1 million shares, respectively, from stock-based compensation plans not included in the computation of diluted net income per share because their impact was antidilutive.

In February 2023, WST’s Board approved a share repurchase program under which WST may repurchase up to $1.0B in shares of common stock. The share repurchase program does not

have an expiration date under which the company may repurchase common stock on the open market or in privately-negotiated transactions. The number of shares to be repurchased and the timing of such transactions will depend on a variety of factors, including market conditions.

- During the 3 months ended June 30, 2024, WST purchased 509,336 shares of common stock under the program at a cost of $187.1 million, or an average price of $367.48/share.

- In the 3 months ended June 30, 2023, WST purchased 492,710 shares of common stock under the program at a cost of $173.4 million, or an average price of $351.82/share.

- During the 6 months ended June 30, 2024, WST purchased 1,239,015 shares of common stock under the program at a cost of $454.1 million, or an average price of $366.53/share.

- In the 6 months ended June 30, 2023, WST purchased 676,070 shares of common stock under the program at a cost of $233.5 million, or an average price of $345.33/share.

Stock Splits

WST initiated a 2-for-1 stock split in September 2013.

Valuation

WST’s FY2012 – FY2023 diluted PE levels are 23.80, 31.65, 32.46, 47.05, 45.85, 39.47, 47.82, 49.29, 68.60, 58.12, 28.53, and 47.46.

In prior posts I calculated WST’s valuation at different points in time. These posts are accessible through the Archives section of this site.

Analysts’ forward-adjusted diluted EPS estimates may change slightly over the next several days. The following, however, is based on the ~$284.76 share price at the July 26 market close and current estimates.

- FY2024 – 9 brokers – mean of $6.60 and low/high of $6.35 – $8.13. Using the mean estimate, the forward-adjusted diluted PE is ~43.1.

- FY2025 – 10 brokers – mean of $7.97 and low/high of $6.81 – $9.48. Using the mean estimate, the forward-adjusted diluted PE is ~35.7.

- FY2026 – 8 brokers – mean of $9.27 and low/high of $7.65 – $10.75. Using the mean estimate, the forward-adjusted diluted PE is ~30.7.

Using management’s $6.35 – $6.65 FY2024 adjusted-diluted EPS outlook and the $284.76 share price, the forward adjusted diluted PE range is ~42.8 – ~44.8.

FCF in in the first half of FY2023 and FY2023 was $149.8 million and ~$430 million, respectively. YTD FCF, however, is only $92.4 million. I think WST may only generate ~$200 million of FCF in FY2024.

If it does reach ~$200 million and we use ~74 million diluted weighted average shares outstanding for FY2024, we are looking at ~$2.70 of FCF/share. Divide the current $284.76 share price by ~$2.70 and we get a P/FCF of ~105.5.

Final Thoughts

As noted in several previous posts, I am looking to increase my exposure in great companies that appear to have fallen out of favor. WST certainly falls in this group!

I hold 400 shares in a ‘Core’ account within the FFJ Portfolio. When I completed my 2024 Mid Year FFJ Portfolio Review, WST was my 20th largest holding; I had negligible exposure when I completed my 2023 Year End FFJ Portfolio Review.

I have no change in WST’s long term outlook despite its short term challenges. The increasing biologics sales, GLP-1 obesity drug sales, and regulatory pressures are forcing its customers toward higher-quality packaging solutions and WST is spending heavily to handle its customers’ growing needs. As noted earlier, however, this expansion is coinciding with a period in which customers are destocking.

Once WST’s capital expansion projects have been completed and revenue is being generated from the expanded and new facilities, we should expect stronger earnings and FCF. Furthermore, no debt repayment is due until mid-2027. If all goes according to plan, WST’s numbers should improve from current levels. In the short term, however, investors should not panic. This is a perfect illustration of why investors need to think long term like good business owners do.

WST’s business remains fundamentally sound and it is still the industry leader. Despite my very recent purchases (300 Visa (V) on July 24 and 300 Mastercard (MA) on July 25), I will dip into my liquidity to add to my WST exposure within the next few days.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long WST.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.