In my September 13, 2024 How To Think About Risk post, I include a link to Howard Marks’ – co-founder and co-chairman of Oaktree Capital Management (the largest investor in distressed securities worldwide) – explanation about the character of risk, the relationship between risk and return, the misconceptions about risk, and how to think about risk.

I followed up that post with my September 15 You Don’t Need 10 Bagger Stocks To Create Financial Freedom post. This topic came to mind following a number of posts on various social media platforms in which there is a fixation on finding the next ‘home run’ investment.

My September 23 Avoid Permanent Capital Impairment post touches upon the importance of mitigating the possibility of a permanent impairment to our capital. Not every investment pans out. It is, therefore, imperative that we do not place ourselves in the predicament of permanently wiping out our capital.

Sure, a company’s share price can languish (how long is unknown) below our average cost. If the underlying thesis for making the investment is intact, however, there should be no reason to exit at a loss. Never be FORCED to sell. In fact, a lower share price (and having excess capital) provides the opportunity to add to our exposure.

When writing that post, I though back to my childhood when we played the Snakes and Ladders board game.

Landing at the base of a ladder would propel a player ahead several board spaces. This is akin to holding a multi bagger investment.

On the flip side, landing on a snake’s head is like a capital impairment; you slide down the snake to the board space that has the end of the snake’s tail.

Imagine that in the game of life you are on space #96 and your goal (space #100) is in sight. You roll, get a 3, and slide all the way down to space #41.

Perhaps your goal is to step off the hamster wheel at a specific age. You diligently saved and invested and debt was a non-issue. Now, you are in the predicament where you have to work longer. That blows!

Did we fixate on the prize with little consideration to the risks? What if:

- that investment has a majority shareholder with a criminal record? (ie. Carvana)

- the company’s product is all ‘smoke and mirrors’?

- the investment turns out to be an elaborate Ponzi scheme?

- there are financial shenanigans being played? (Fooling Some of the People All of the Time, A Long Short (and Now Complete) Story, Updated with New Epilogue – David Einhorn)

…and the list goes on and on.

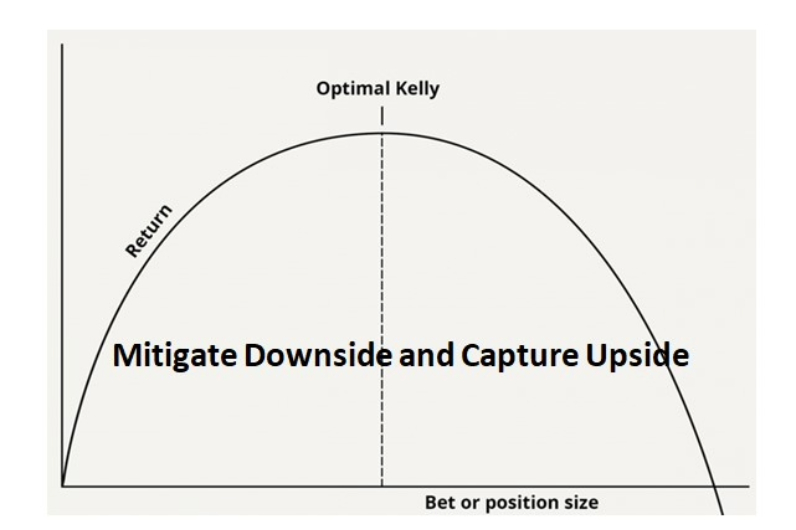

The Kelly Criterion

In my September 23 post, I reference the Kelly Criterion described in William Poundstone’s Fortune’s Formula The Untold Story of the Scientific Betting System That Beat the Casinos and Wall Street.

The Kelly Criterion was introduced by John L. Kelly Jr. in a 1956 paper on optimal betting strategies. This criterion was originally developed to maximize the growth of capital in gambling scenarios. It gained wider recognition through the work of Edward Oakley Thorp, an American mathematics professor, author, hedge fund manager, and blackjack researcher.

Thorp pioneered the modern applications of probability theory, including the harnessing of very small correlations for reliable financial gain and adapted the Kelly Criterion for use in financial markets. Now, the Kelly Criterion is predominantly used by professional traders and institutional investors to determine the optimal investment ‘sizing’ based on their edge and risk tolerance; the aim is to achieve the highest possible growth while managing the risk of significant losses.

‘The Kelly Criterion, Under the Hood’ chapter that commences on page 130 of 454 in William Poundstone’s book explains how this money management system works and why it is superior to other methods.

Michael J. Mauboussin states on page 157 of 242 in Think Twice – Harnessing the Power of Counterintuition that:

One common and conspicuous error in dealing with complex systems is betting too much on a particular outcome. The Kelly formula tells you how much to bet, given your edge. One of the Kelly formula’s central lessons is that betting too much in a system with extreme outcomes leads to ruin.

Mitigate Downside – Capture Upside

I have neither the desire nor the time to employ a sophisticated process that professional investors employ. Perhaps I am being foolish but I like to think I am employing a rudimentary form of the Kelly Criterion.

Twice a year, I analyze the holdings in ~19 investment accounts to gauge my exposure to each holding; the results of my most recent analysis are reflected in my 2024 Mid Year FFJ Portfolio Review post. Since this is merely a snapshot of my exposure at the end of a specific trading day, the total value of each holding is naturally subject to change daily.

For the most part, the top 10 holdings do not change much. There are, however, several changes over time in the top 11 – 20 and top 21 – 30.

One very noticeable change is Intuitive Surgical (ISRG). It was not within the top 30 when I completed my January 6, 2022 analysis. When I completed my June 28, 2024 analysis, it was my 7th largest holding.

Comparing the rankings at December 31, 2023 and June 28, 2024, we see several changes. Some of these changes are because I increased my exposure to companies in which I have a strong conviction.

Earlier this year, however, the Canadian Federal Government introduced changes to tax treatment of capital gains. In order to minimize our tax liability several changes were made based on advice from our tax accountants; I disclose the changes in my June 11, 2024 FFJ Portfolio Adjustments Before Capital Gains Tax Changes Arrive post.

Regrettably, in June I had to sell shares in a few holdings I never intended to sell. Fortunately, I was able to subsequently purchase a greater number of CME Group (CME), Mastercard (MA), and Brookfield Asset Management (BAM.to) shares at a lower price. In hindsight, I should have repurchased a greater number of shares in Apple (AAPL), S&P Global (SPGI), Moody’s (MCO), and Goldman Sachs (GS) but I deemed their respective valuation to be too rich. Now, I have to wait for their valuation to retrace to a level I consider reasonable.

On the bright side, this entire exercise prompted me to revisit my entire portfolio.

Using a rudimentary form of the Kelly Criterion reaffirmed my decision to have a more concentrated portfolio – optimal investment ‘sizing’.

I have very little interest in Canadian company exposure and have whittled my exposure to 7 (Brookfield Asset Management and Brookfield Corporation are separate and distinct).

I had exposure to 53 US companies (now 49). This is still too many and I will further reduce this when I sell smaller positions in early 2025 as part of my Registered Retirement Savings Plan (RRSP) meltdown strategy.

I also have a meaningful amount of cash sitting on the sidelines awaiting deployment.

Never be FORCED to sell. Since we have no control over share price behavior, the share price of several of my holdings could very well fall below my average cost. I may land on a ‘snake’s head’ thereby setting me back. This is of little concern to me since I intend to weather whatever storm may arise. If I have to wait a few years for a company’s share price to recover, so be it. I am happy to remain a shareholder as long as the company does not fall off the rails.

Realistically, what are the chances of a large-cap or mega-cap company becoming a ’10 bagger’? Were I chasing ’10 baggers’, I would likely have exposure to micro-, small-, and mid-cap companies.

When times get tough, my holdings have far more ‘fire power’ than much smaller companies. If my exposure was to smaller companies, would I have the intestinal fortitude to ‘hold’ or would I be inclined to ‘throw in the towel’ if things turn ugly?

I don’t mind ‘sliding down the snake’s tail’ if I know a company and I can ‘weather the storm’.

Judging from what I see on social media, some investors either:

- have a much higher risk tolerance than me; OR

- fixate on the potential return and ignore the risks.

From an optimal investment ‘sizing’ perspective, I think I have exposure to too many companies. I suspect John L. Kelly Jr. and Michael J. Mauboussin would agree.

Having said this, at least I do not have a low 6 figure investment portfolio (~$300,000) with exposure to ~150 companies like one particular investor who regularly dispensed investment advice on various social media platforms.

Final Thoughts

During a talk at Georgetown University on Sept. 19, 2013, Warren Buffett described his 20 slot punch card approach to investing.

You only have an opinion on a few things. In fact, I’ve told students if when they got out of school, they got a punch card with 20 punches on it, and that’s all the investment decisions they got to make in their entire life, they would get very rich because they would think very hard about each one.

In essence, Buffett recommends investors concentrate their investments on a limited number of well-known, high-quality businesses. According to him, you do not need 20 right decisions to get very rich. Four or five will probably do it over time.

As we build our portfolio, it would be wise not to throw mud at the wall. Employ a rudimentary version of The Kelly Criterion. Invest in a few high quality companies at attractive valuations and build meaningful positions.

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ISRG, CME, MA, MCO, SPGI, AAPL, BRK-b, BAM.to, BN.to.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.