With all the changes brought on by artificial intelligence, I have no idea which companies are likely to be long-term winners. Microsoft (MSFT) has a proven track record to navigate the tech sector safely. As a result, it suits my relatively conservative investor profile.

Despite not having written about MSFT since my November 11, 2021 guest post, it is not my intent to analyze this company in any great depth. The primary reason for this post is merely to disclose the purchase of an additional 100 shares @ $415.04 on January 31 in one of the ‘Core’ accounts in the FFJ Portfolio.

Business Overview

The best way to learn about MSFT is to read the company’s website and the Form 10-Qs and Form 10-Ks accessible through the SEC Filings section of the company’s website.

Financials

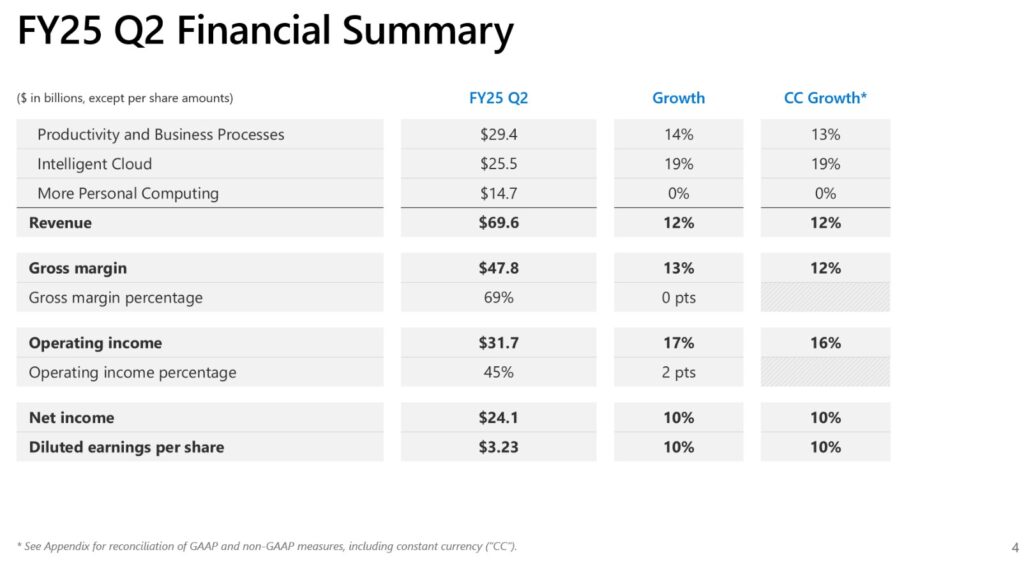

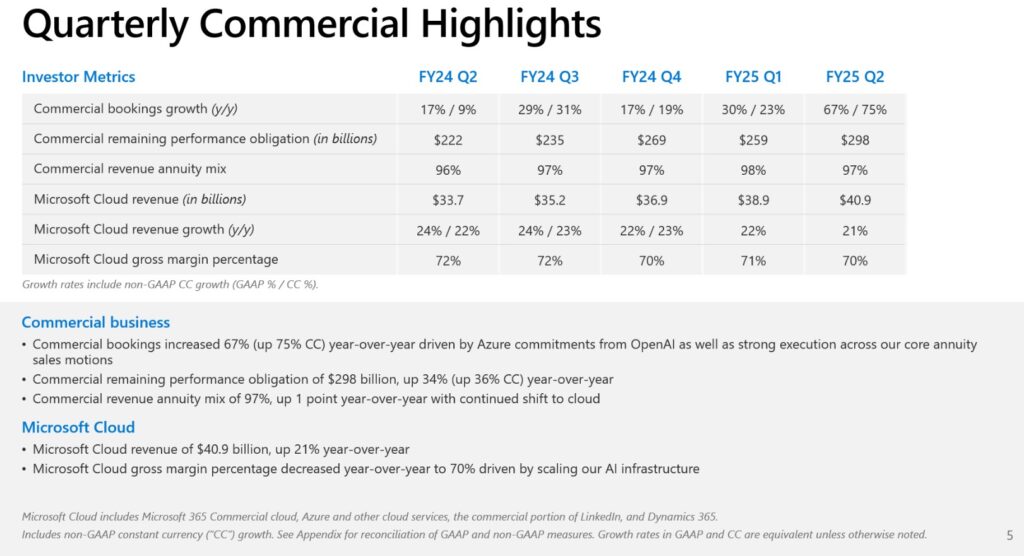

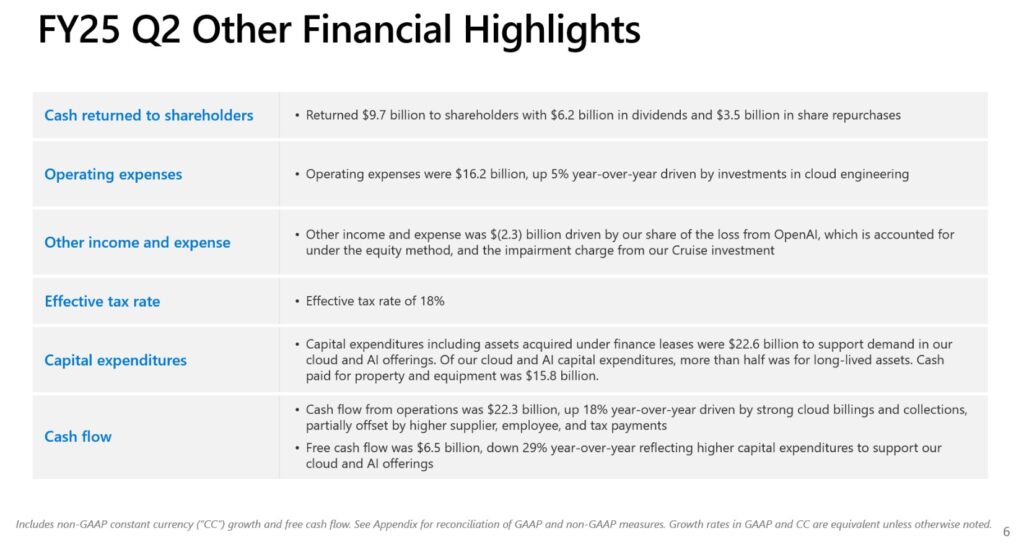

Q2 and YTD2025 Results

Refer to the material available in the Form 8-K and Form 10-Q filed on January 28, 2025.

The following are extracted from the Q2 2025 earnings presentation.

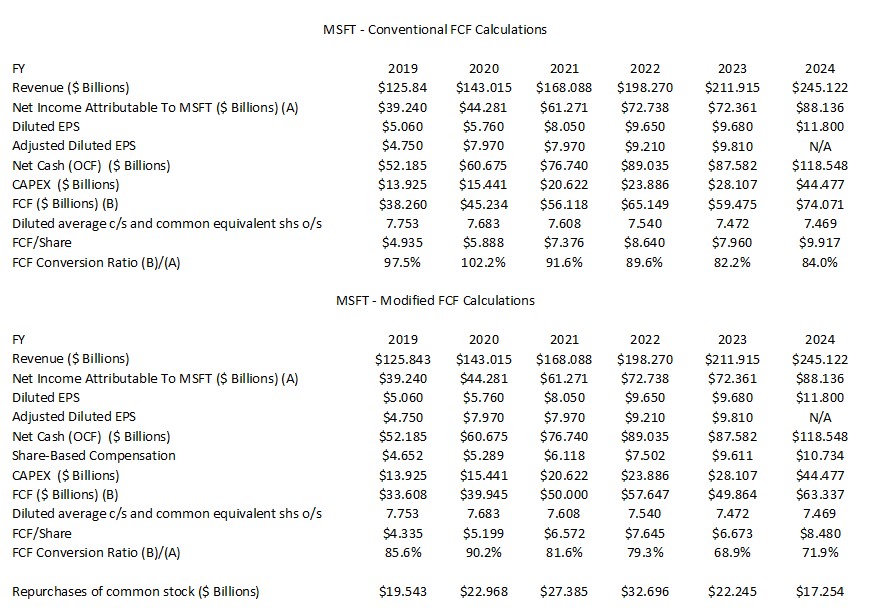

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2020 – FY2024)

In several recent posts I express my thoughts about the way many companies calculate Free Cash Flow (FCF). Since FCF is a non-GAAP metric, there is no standardization in its calculation.

In most cases, companies merely deduct net CAPEX from net cash flows from operating activities. I think it is also necessary to deduct share based compensation (SBC).

Many companies employ SBC as part of their employee compensation plans and reflect this cost within the Income Statement. Because SBC involves no cash outlay, however, companies add back SBC to determine net cash flows from operating activities in the Condensed Consolidated Statement of Cash Flows.

Suppose, however, that MSFT were to compensate employees 100% by way of SBC. Since there is no cash outlay, the full amount of its employee compensation would be added back in the Condensed Consolidated Statement of Cash Flows to determine net cash flows from operating activities.

If, on the other hand, MSFT were to have no SBC and were to actually disburse funds to pay its employees, nothing would be added back in the Condensed Consolidated Statement of Cash Flows.

By merely changing the manner in which it compensates its employees we get very different net cash flows from operating activities! How does this make any sense? Is the use of SBC not a form of ‘financing’? Would it be more proper to reflect SBC within the Cash Flows From Financing Activities section of the Condensed Consolidated Statement of Cash Flows? This way, we would arrive at similar FCF results no matter how a company chooses to compensate its employees.

The following table reflects data extracted from the FY2019 – FY2024 earnings related material.

MSFT merely deducts CAPEX from OCF to arrive at FCF. It, however, has sizable SBC every year. When we deduct SBC, we see a significant reduction in its annual FCF.

In the first half of FY2025, MSFT generated $56.471 of OCF and incurred $30.727B of CAPEX. Using MSFT’s method of calculation FCF, we get YTD2025 FCF of $25.744B. If we deduct YTD SBC of $5.921B, however, YTD2025 FCF drops to $19.823B.

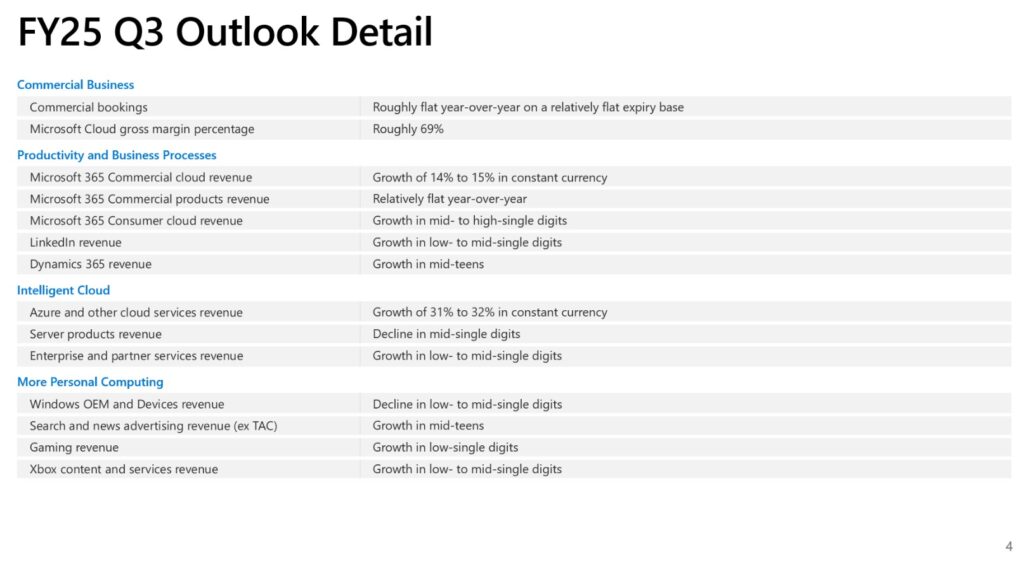

Q3 and FY2025 Outlook

The following reflect MSFT’s Q3 and FY2025 outlook.

Risk Assessment

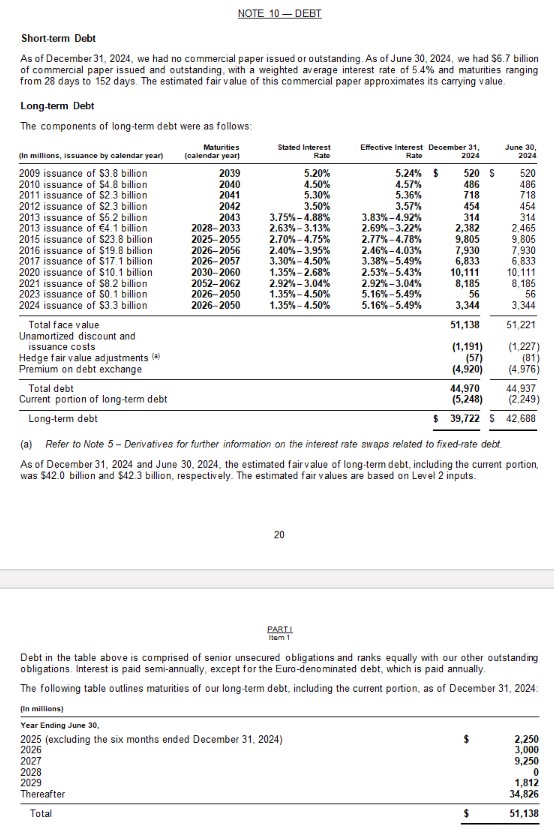

The following schedule reflects MSFT’s debt at the end of Q2 2025.

MSFT’s credit ratings are the best awarded by the major credit rating agencies.

- Moody’s: Aaa. This rating was last reviewed on January 18, 2022 at which time the outlook was stable.

- S&P Global: AAA. This rating was last reviewed on July 17, 2024 at which time the outlook was stable.

Both ratings define MSFT as having an extremely STRONG capacity to meet its financial commitments. I want exposure to the technology sector. At this stage of my life, however, I am not prepared to speculate.

Dividend and Dividend Yield

MSFT’s dividend history is accessible here. The next $0.83 quarterly dividend is payable on March 13 to shareholders of record on February 20.

Following my recent purchase, I only own 406 shares which will generate $336.98 of dividend income. With shares being held in taxable accounts, however, I incur a 15% dividend withholding tax; Canadian residents incur this tax when US shares are held in a taxable account. This means I will receive $286.43 of dividend income…a YEAR! It is tough to get excited about this which always makes me wonder why some investors fixate on dividend metrics.

I much prefer that a company not distribute dividends if it can generate superior returns by 1) retaining money in the company to grow organically / make strategic acquisitions OR 2) repurchase shares at attractive valuations.

Looking at MSFT’s share repurchase history, we see that it aggressively repurchases shares. The diluted weighted average shares outstanding in Q4 2018 was 7.775B. By Q2 2025, it had been reduced to 7.468B.

In Q1 and Q2 2024 and 2025, MSFT repurchased the following.

Since the beginning of FY2019 until the end of Q2 2025, MSFT has repurchased ~$151.184B of its shares. It has, however, issued a substantial number of shares as part of its various SBC programs. These shares are typically issued at prices well below the price at which investors acquire shares in the open market.

On September 14, 2021, MSFT’s Board approved a share repurchase program authorizing up to $60.0B in share repurchases. As of December 31, 2024, $4.0B remained of this $60.0B share repurchase program.

On September 16, 2024, MSFT’s Board approved a share repurchase program authorizing up to $60.0B in share repurchases. This share repurchase program will commence following completion of the program approved on September 14, 2021. It has no expiration date, and may be terminated at any time.

Valuation

In the first half of FY2025, MSFT generated $6.53 of diluted EPS. When I recently added to my exposure with the purchase of shares @ $415.04, I estimated that FY2025 diluted EPS would be ~$13.00 – ~$13.10. Using a $13.05 mid-point, I arrived at a ~31.8 PE. MSFT’s share price has pulled back to ~$410.90 as I compose this post after the February 3 market close; this slight price decline has no material impact on my estimate of MSFT’s valuation.

MSFT’s valuation using the current broker guidance and my $415.04 purchase price is:

- FY2025 – 39 brokers – mean of $13.10 and low/high of $12.93 – $13.44. Using the mean, the forward adjusted diluted PE is ~31.7.

- FY2026 – 40 brokers – mean of $14.95 and low/high of $14.30 – $16.69. Using the mean, the forward adjusted diluted PE was ~27.8.

- FY2027 – 24 brokers – mean of $17.51 and low/high of $16.00 – $21.38. Using the mean, the forward adjusted diluted PE was ~23.7.

- FY2028 – 3 brokers – mean of $19.47 and low/high of $18.53 – $21.16. Using the mean, the forward adjusted diluted PE was ~21.3.

These estimates will change over the coming days given that MSFT has very recently released its results.

I place virtually no reliance on broker estimates beyond FY2026.

MSFT’s FCF conversion ratio is well below 100% (see conventional and modified FCF calculations tables). Its valuation based on FCF is, therefore, inferior to its valuation based on earnings.

Final Thoughts

When I completed my 2024 Year End FFJ Portfolio Review, MSFT was my 24th largest holding…down from my 18th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review.

In the FFJ Portfolio, I own 206 shares in 1 account at an average cost of ~$74.26 and 200 shares in another account at an average cost of $321.14.

The Canadian Federal government indicates that the current inflation rate in Canada is ~1.8%. I think most Canadians living in the real world would strongly agree the rate is much higher. If we also consider the possibility that the US will follow through with its decision to impose a 25% tariff effective the beginning of March 2025, the rate of inflation will undoubtedly be much higher than ~1.8%. This is why I want our investments to generate at least a low double digit total investment return over the very long-term.

I am not quite sure how investors who fixate on dividend metrics think an $0.83/share quarterly dividend is going to achieve this rate of return! If I can acquire undervalued shares, hold them for the very long-term so as to not incur any tax obligations…now THIS makes much more sense to me.

If we apply the Rule of 72 and MSFT can generate at least a 10% rate of return, the value of this investment should double in ~7.2 years. Using a baseball analogy, this is not a ‘home run’. At this stage of my life, I want a high OBP (on base percentage) and if that means consistently hitting’ singles’ and ‘doubles’, then I am fine with this.

I am a relatively conservative investor wishing to navigate the tech sector safely. I have no idea which companies investing heavily in artificial intelligence are going to be long-term winners. Given this, MSFT’s proven track record and very strong financial position give me confidence that it will be one of the winners.

Although MSFT is not immune to macroeconomic challenges, it is one of a few companies with a complete, integrated product set aimed at:

- enterprise efficiency;

- cloud transformation;

- collaboration; and

- business intelligence.

MSFT has a large and loyal customer base and its financial position is extremely strong. There may be some young and upcoming tech companies that will generate far superior investment returns than MSFT. However, such firms typically expose investors to higher risk. As an investor with very limited knowledge about the technology sector, I view MSFT as a ‘safe haven’.

Investors will use different metrics and various formulas to try and determine MSFT’s fair value which explains why there are many different ‘fair values’ out there. I don’t know how anyone can accurately determine what a company’s earnings will be 10 years from now….let alone 3 years from now.

I do not use such formulas to try and determine what is a ‘fair value’. Using MSFT’s FY2025 outlook, I try to extrapolate its results 1 – 2 years, at most, in the future. In addition, I also take into consideration that MSFT has a massive share repurchase program and that senior management and the Board will wisely repurchase shares so as to maximize their investment returns; they own far more shares than me.

The current share price as I finish composing this post is ~$411. If you think $455 is a fair price, then you stand to generate just under an 11% rate of return if the share price rises to this $455 value. This seems like an acceptable return for a company that is accorded the best credit ratings by rating agencies.

If MSFT’s share price remains under pressure, I will increase my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long MFST.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.