I last reviewed Mastercard (MA) in my June 8, 2023 guest post at Dividend Power. At the time, the most recently available financial results were for Q1 2023. Now, based on my analysis of Q4 and FY2023 results and FY2024 outlook that were released on January 31, I conclude that Mastercard is unreasonably valued.

In this brief post, I focus on MA’s valuation based on estimated earnings.

Business Overview

Most investors are familiar with MA to some extent. I, therefore, dispense with a business overview. I do, however, encourage a review of ‘Item 1. Business’ and ‘Item 1A. Risk Factors’ found at the beginning of MA’s FY2023 Form 10-K.

Financials

Q4 and FY2024 Results

Please refer to MA’s Q4 Earnings Release, Earnings Presentation, and Supplemental Materials that are accessible from the company’s website.

MA continues to grow through healthy consumer spending, new and renewed customer agreements, and a continued secular shift from cash to card.

FY2024 Outlook

MA’s base case scenario for 2024 reflects healthy consumer spending. It is, however, closely monitoring the macro environment as well as geopolitical events.

The base case is for FY2024 net revenues is to grow at the high end of a low double-digit rate on a currency-neutral basis, excluding acquisitions. Acquisitions and foreign exchange are forecast to have a minimal impact for the year.

Full year growth in operating expenses is expected to be at the low end of a low double-digit rate on a currency-neutral basis, excluding acquisitions and special items.

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

In FY2014 – FY2023, MA generated OCF of (in $B approx): 3.41, 4.10, 4.64, 5.66, 6.22, 8.18, 7.22, 9.46, 11.20, and 11.98.

In FY2014 – FY2023, MA generated FCF of (in $B approx): 3.07, 3.76, 4.26, 5.24, 5.72, 7.46, 6.52, 8.65, 10.10, and 10.89.

FY2023 CAPEX of ~$1.09B consisted of purchases of property and equipment and capitalized software. In FY2021 and FY2022, CAPEX amounted to ~$0.814B and ~$1.097B.

Credit Ratings

Moody’s currently assigns an Aa3 rating to MA’s senior unsecured long-term domestic debt; this rating was upgraded on November 16, 2022 from A1.

This rating is the lowest tier of the high-grade investment grade category. It defines MA as having a very strong capacity to meet its financial commitments; the rating differs from the highest-rated obligors only to a small degree.

S&P Global currently assigns an A+ rating to MA’s senior unsecured long-term domestic debt; this rating has been in effect since November 2018 and is one level below that assigned by Moody’s.

This rating is the highest tier of the upper-medium-grade investment grade category. It defines MA as having a strong capacity to meet its financial commitments. However, MA is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

MA’s credit risk suits my conservative investor profile.

Dividends, Share Repurchases, and Stock Splits

Dividend and Dividend Yield

MA distributes a quarterly dividend as evidenced by the dividend history. MA’s annual dividend yield has historically been under 1% and is likely to remain under 1% going forward.

The bulk of MA’s historical total investment return has been generated from capital appreciation. This is unlikely to change, and therefore, it is exceedingly important to acquire shares when they are reasonably/attractively valued.

Share Repurchases

The weighted average number of Class A diluted common stock outstanding in FY2013 – FY2023 (in millions of shares) is 1,215, 1,169, 1,137, 1,101, 1,072, 1,047, 1,022, 1,006, 992, 971, and 946.

In Q4, MA repurchased $1.8B worth of stock. It repurchased an additional $0.586B between FYE2023 and January 26, 2024.

The following table summarizes MA’s share repurchase authorizations of its Class A common stock for the years ended December 31.

Source: MA – FY2023 Form 10-K

In December 2023, December 2022, and November 2021, MA’s Board approved share repurchase programs of its Class A common stock authorizing the repurchase up to $11.0B, $9B, and $8B, respectively. The program approved in 2023 becomes effective after the completion of the share repurchase program approved in 2022. The timing and actual number of additional shares repurchased will depend on a variety of factors, including cash requirements to meet the operating needs, legal requirements, as well as the share price and economic and market

conditions.

The following table summarizes MA’s share repurchase authorizations and repurchase activity of its Class A common stock through December 31, 2023:

Source: MA – FY2023 Form 10-K

Valuation

MA’s FY2013 – FY2022 diluted P/E ratio is 32.98, 29.61, 29.87, 28.52, 35.28, 38.11, 44.30, 53.59, 44.20, 34.74, and 37.18.

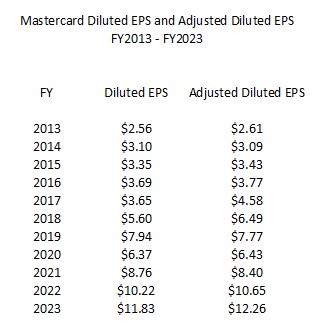

MA’s diluted EPS and adjusted diluted EPS in FY2013 – FY2023 are:

When I reviewed MA in my June 8, 2023 guest post at Dividend Power, shares were trading at ~$374. Using brokers’ adjusted diluted earnings estimates, MA’s forward adjusted diluted PE levels were:

- FY2023 – 35 brokers – mean of $12.28 and low/high of $11.94 – $12.70. Using the mean estimate, the forward adjusted diluted PE is ~30.5.

- FY2024 – 36 brokers – mean of $14.58 and low/high of $13.68 – $15.32. Using the mean estimate, the forward adjusted diluted PE is ~25.7.

- FY2025 – 15 brokers – mean of $17.32 and low/high of $16.74 – $18.31. Using the mean estimate, the forward adjusted diluted PE is ~21.6.

We now know that MA generated FY2023 diluted EPS and adjusted diluted EPS of $11.83 and $12.26, respectively. With shares currently trading at ~$454, the diluted PE and adjusted diluted PE levels are ~38.4 and ~37.

MA generated ~$10.89B of FCF and the weighted average diluted shares outstanding was 946 million giving us a FCF/share value of ~$11.51. With shares trading at ~$454, the P/FCF is ~39.4.

MA’s valuation using the ~$454 share price and brokers’ adjusted diluted earnings estimates are:

- FY2024 – 34 brokers – mean of $14.41 and low/high of $13.62 – $14.81. Using the mean estimate, the forward adjusted diluted PE is ~31.5.

- FY2025 – 34 brokers – mean of $16.79 and low/high of $15.21 – $17.43. Using the mean estimate, the forward adjusted diluted PE is ~27.

- FY2026 – 9 brokers – mean of $19.47 and low/high of $19.08 – $19.89. Using the mean estimate, the forward adjusted diluted PE is ~23.3.

If we compare broker estimates when I wrote my June 8, 2023 post with current broker estimates, we see that the FY2024 and FY2025 estimates are lower now. However, MA’s share price is $80 higher than in June 2023!

Final Thoughts

I currently hold 664 shares in ‘Core’ accounts and 300 shares in a ‘Side’ account in the FFJ Portfolio. A young investor I am helping on their journey to financial freedom also owns MA shares. I do not, however, disclose details regarding this investor’s holdings.

MA was my second largest holding when I completed my 2023 Year End FFJ Portfolio Review; it was a distant second after Visa (V).

Lately, I have begun to question some of my decisions to place companies on my ‘Watch List’ as opposed to making outright purchases. Whenever I encounter this train of thought, I turn to Howard Marks’ memos; he is the co-founder and co-chairman of Oaktree Capital Management, the largest investor in distressed securities worldwide.

In his ‘Everyone Knows’ memo of April 26, 2077, he states:

There’s no such thing as a good idea. Only a good idea at a price. Something can be a very good idea at one price and a very bad idea at another.

In this current environment, I think there are a lot of very bad ideas and just because some investors pay little or no regard to valuation doesn’t mean I have to.

Markets are cyclical and companies can be undervalued, overvalued, or fairly valued. As companies become overvalued, the odds of generating an attractive investment return are lowered. I think Mastercard is unreasonably valued and will only add to my exposure once I am satisfied with its valuation AND if other more attractive investment opportunities do not exist.

If I were to buy shares at ~$454, I think I would be hard pressed to generate a double digit total investment return over the next few years. MA’s share price would need to rise to ~$500 within the year to generate a ~10% return. With a FY2024 adjusted diluted earnings estimate of $14.41, at ~$500, the forward adjusted diluted PE would be ~34.7.

Could the share price rise to $500? Yes. Does it make sense? No.

In one of the ‘Core’ accounts within the FFJ Portfolio, the average cost of my MA shares is ~$155. I certainly don’t expect MA’s share price to retrace to that level. However, MA’s share price can be volatile so it is not unreasonable that, for whatever reason, it could drop to ~$400 or lower. Were it to drop to ~$400, the forward adjusted diluted PE level would be ~27.8 using the mean of the FY2024 broker estimates.

For now….MA is on my ‘Watch List’.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long MA and V.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.