In my August 2, 2024 Mastercard (MA) post, I disclosed the purchase of an additional 300 shares @ ~$432.05 in one of the ‘Side’ accounts within the FFJ Portfolio.

On October 31, MA released its Q3 and YTD2024 results and Q4 outlook. I, therefore, revisit MA to determine if I should increase my exposure.

Business Overview

Most investors are familiar with MA to some extent. I, therefore, dispense with a business overview. I do, however, encourage a review of ‘Item 1. Business’ and ‘Item 1A. Risk Factors’ found at the beginning of MA’s FY2023 Form 10-K.

Financials

Q3 and YTD2024 Results

Refer to MA’s Earnings Release, Earnings Presentation, and Supplemental Materials that are accessible from the company’s website.

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

In the FY2014 – FY2023 time frame, MA’s:

- OCF was (in B$) 3.41, 4.10, 4.64, 5.66, 6.22, 8.18, 7.22, 9.46, 11.20, and 11.98.

- CAPEX was (in B$) 0.33, 0.34, 0.38, 0.42, 0.50, 0.73, 0.71, 0.81, 1.10, and 1.09.

- FCF was (in B$) 4.24, 4.52, 4.97, 5.42, 7.03, 9.15, 7.67, 9.57, 11.00, and 12.84.

YTD2024 net cash provided by operating activities is ~$9.946BB, YTD CAPEX (Purchases of property and equipment and Capitalized software) is ~$0.944B, and YTD FCF is ~$9.002B.

Share based compensation has been added back to determine Net cash provided by operating activities in the Consolidated Statements of cash Flows. In my How Stock Based Compensation Distorts Free Cash Flow, I explain why we need to be wary about the extent to which stock based compensation (SBC) can distort FCF.

In the first 9 months of FY2024, MA’s SBC amounted to ~$0.418B. If we deduct this amount from ~$9.002B, FCF drops to ~$8.584B.

As a conservative investor, I will use YTD2024 FCF of ~$8.584B in estimating MA’s valuation later in this post.

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level.

MA’s FY2014 – FY2023 ROIC (%) was 42.09, 43.81, 40.96, 36.89, 51.99, 64.76, 39.41, 44.94, 49.74, and 54.35.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

FY2024 Outlook

MA’s base case scenario for 2024 reflects healthy consumer spending. It is, however, closely monitoring the macro environment as well as geopolitical events.

Risk Assessment

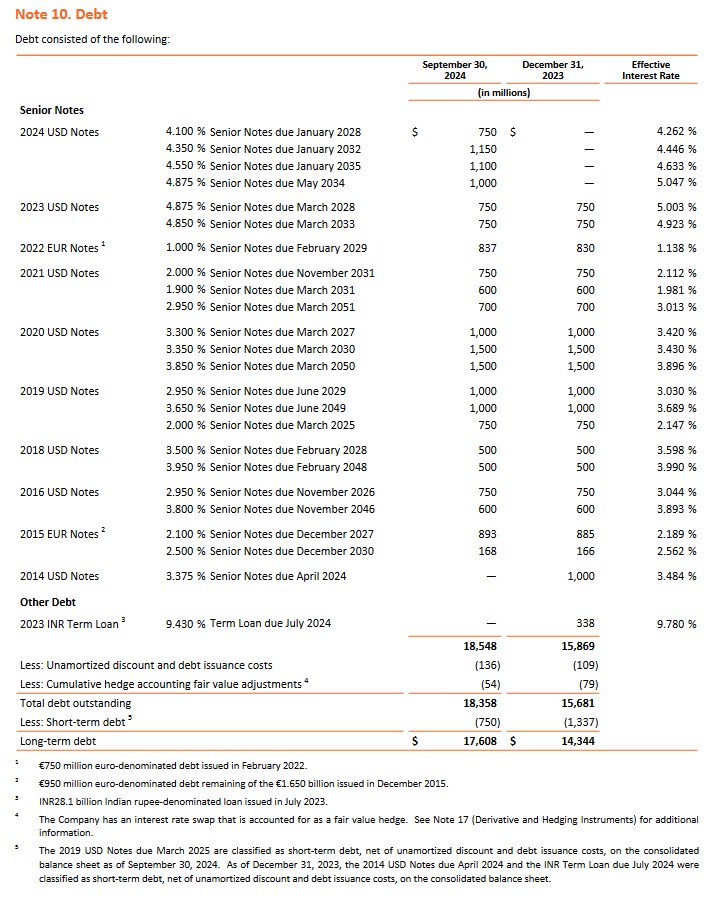

The following debt schedule is found on page 19 of 53 in MA’s Q3 Form 10-Q. During the quarter, MA raised an additional $3.25B of long-term debt.

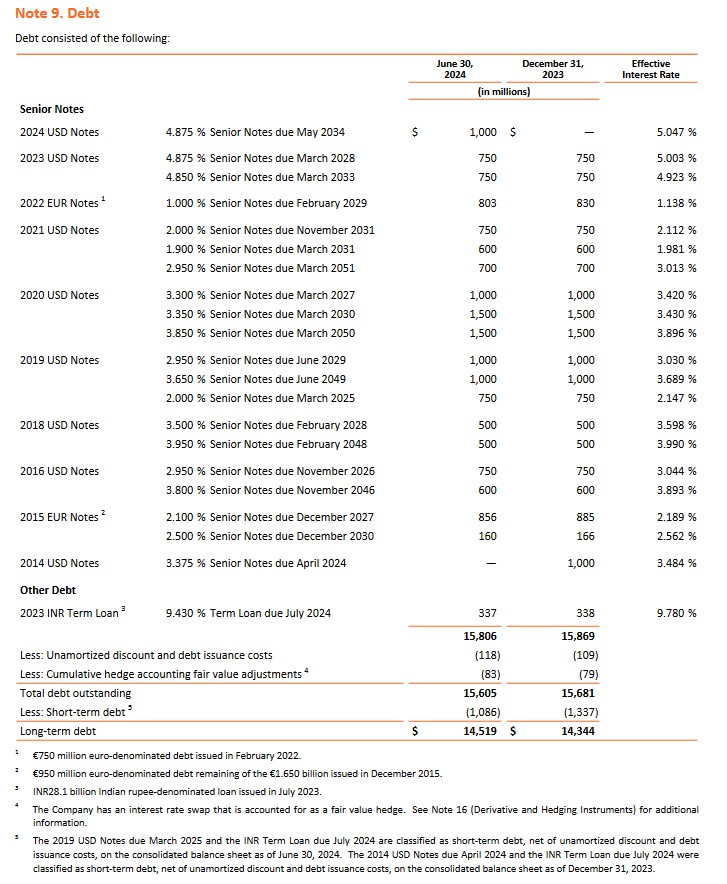

The following debt schedule is extracted from MA’s Q2 Form 10-Q and is provided for comparison.

Moody’s currently assigns an Aa3 rating to MA’s senior unsecured long-term domestic debt; this rating was upgraded on November 16, 2022 from A1.

This rating is the lowest tier of the high-grade investment grade category. It defines MA as having a very strong capacity to meet its financial commitments; the rating differs from the highest-rated obligors only to a small degree.

S&P Global currently assigns an A+ rating to MA’s senior unsecured long-term domestic debt; this rating has been in effect since November 2018 and is one level below that assigned by Moody’s.

This rating is the highest tier of the upper-medium-grade investment grade category. It defines MA as having a strong capacity to meet its financial commitments. However, MA is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

MA’s credit risk suits my conservative investor profile.

Dividends and Share Repurchases

Dividend and Dividend Yield

MA distributes a quarterly dividend as evidenced by the dividend history. MA’s annual dividend yield has historically been under 1% and is likely to remain under 1% going forward.

The bulk of MA’s historical total investment return has been generated from capital appreciation. This is unlikely to change, and therefore, it is exceedingly important to acquire shares when they are reasonably/attractively valued.

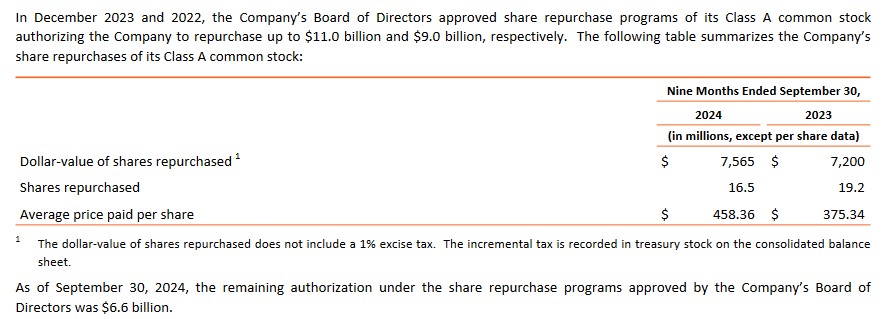

Share Repurchases

The weighted average number of Class A diluted common stock outstanding in FY2013 – FY2023 (in millions of shares) is 1,215, 1,169, 1,137, 1,101, 1,072, 1,047, 1,022, 1,006, 992, 971, and 946.

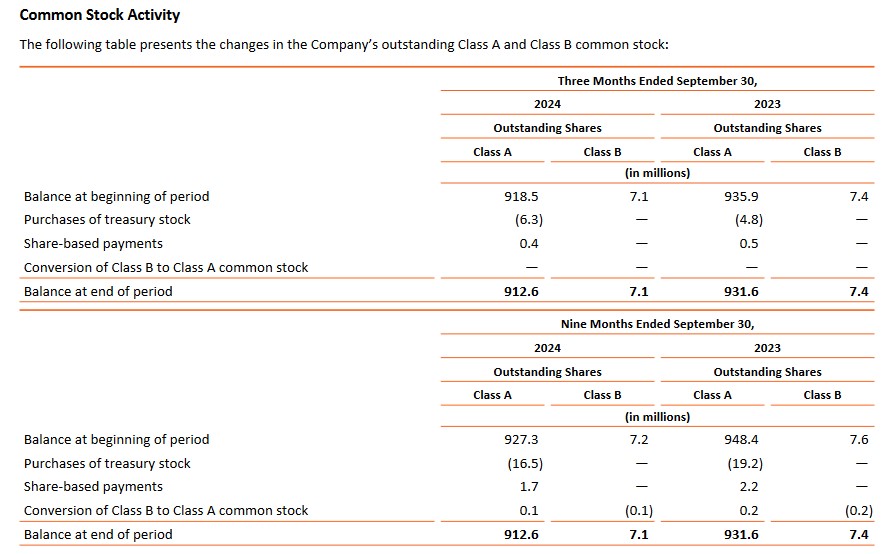

In Q3, MA repurchased $2.9B worth of stock and the weighted average number of shares outstanding in Q3 2024 was 925. Between September 30 – October 28, it repurchased an additional $0.983B.

The following, extracted from MA’s Q3 2024 Form 10-Q, reflects the Q3 and YTD2024 share repurchase activity.

The following, provided for comparison, summarizes MA’s share repurchase authorizations of its Class A common stock for the years ended December 31.

Source: MA – FY2023 Form 10-K

Valuation

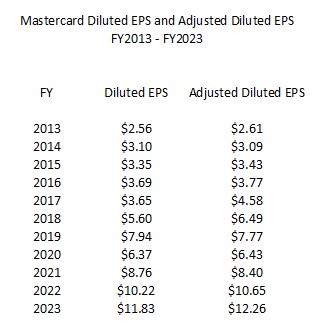

MA’s FY2013 – FY2023 diluted P/E ratio is 32.98, 29.61, 29.87, 28.52, 35.28, 38.11, 44.30, 53.59, 44.20, 34.74, and 37.18.

MA’s diluted EPS and adjusted diluted EPS in FY2013 – FY2023 are:

On July 25, I acquired shares @ ~$432.05. Using this purchase price and brokers’ adjusted diluted earnings estimates, the forward adjusted diluted PE levels are:

- FY2024 – 36 brokers – mean of $14.30 and low/high of $13.98 – $14.65. Using the mean estimate, the forward adjusted diluted PE is ~30.2.

- FY2025 – 36 brokers – mean of $16.62 and low/high of $15.94 – $17.23. Using the mean estimate, the forward adjusted diluted PE is ~26.

- FY2026 – 21 brokers – mean of $19.34 and low/high of $18.54 – $20.31. Using the mean estimate, the forward adjusted diluted PE is ~22.3.

By the time I composed my prior post on August 1, however, the share price had risen to ~$462. Using this price and brokers’ adjusted diluted earnings estimates, the forward adjusted diluted PE levels were:

- FY2024 – 36 brokers – mean of $14.30 and low/high of $13.98 – $14.65. Using the mean estimate, the forward adjusted diluted PE is ~32.3.

- FY2025 – 36 brokers – mean of $16.62 and low/high of $15.94 – $17.23. Using the mean estimate, the forward adjusted diluted PE is ~27.8.

- FY2026 – 21 brokers – mean of $19.34 and low/high of $18.54 – $20.31. Using the mean estimate, the forward adjusted diluted PE is ~23.9.

In the first half of FY2024, MA generated FCF of ~$3.873B after deducting SBC and ~$4.136B before deducting SBC. If it were to generate ~$8B for the year (or $9B before deducting SBC) and we use a weighted average number of shares outstanding of 930 million for FY2024, we arrive at ~$8.60 of FCF/share or ~$9.68 of FCF/share before deducting SBC. Using my ~$432.05 purchase price, the forward adjusted P/FCF was ~50.2 or ~44.6 before deducting SBC. Were we to use the ~$462 share price at the time I composed my post, the forward P/FCF was ~53.7 or ~47.7 before deducting SBC.

In the first 9 months of FY2024, MA generated $10.25 and $10.78 of diluted EPS and adjusted diluted EPS. If it were to generate ~$13.67 and ~$14.37 of diluted EPS and adjusted diluted EPS for FY2024, the forward diluted PE and forward adjusted diluted PE using a $508 share price would be ~37.2 and ~35.4.

Using the brokers’ adjusted diluted earnings estimates, the forward adjusted diluted PE levels are:

- FY2024 – 35 brokers – mean of $14.44 and low/high of $14.18 – $14.65. Using the mean estimate, the forward adjusted diluted PE is ~35.2.

- FY2025 – 35 brokers – mean of $16.42 and low/high of $15.91 – $17.37. Using the mean estimate, the forward adjusted diluted PE is ~31.

- FY2026 – 28 brokers – mean of $19.09 and low/high of $18.29 – $20.42. Using the mean estimate, the forward adjusted diluted PE is ~26.6.

The FCF used when I composed my prior post appear to have been somewhat off the mark. Unless MA has a horrendous Q4, FCF after deducting SBC should be somewhat higher than my prior estimate.

In the 9 months of FY2024, MA generated FCF of ~$8.584B after deducting SBC. If it generates just over $2.7B of FCF in Q4 (slightly less than in each of the prior 3 quarters), it should generate $11.3B for the year.

The diluted weighted-average shares outstanding for the fiscal year ending December 31, 2023 was 946 million. At the end of Q3, this had been reduced to 925 million. In Q4, it has already repurchased additional shares and further shares will likely be repurchased between now and FYE2024. Given this, let’s stick with a weighted average of 930 million for FYE2024.

Divide ~$11.3B of FCF by 930 million shares and we arrive at ~$12.15 of FCF/share. Using the current ~$508 share price, the forward P/FCF is ~41.8.

Final Thoughts

I currently hold 664 shares in ‘Core’ accounts and 300 shares in a ‘Side’ account in the FFJ Portfolio. A young investor I am helping on their journey to financial freedom also owns MA shares. I do not, however, disclose details regarding this investor’s holdings.

It continues to be my 2nd or 3rd largest holding and I intend to opportunistically increase my exposure. Based on my assessment, however, I think a fair valuation is closer to ~$465. At this price, MA’s forward adjusted diluted PE would be ~32.2 (~$465/$14.44) and the forward P/FCF would be ~38.3 (~$465/$12.15).

Some investors will undoubtedly view these levels to still be elevated. MA, however, has significant long term upside potential. I am, therefore, prepared to ‘pay up’ (to an extent) given that the plan is to hold shares for the VERY long term (as in well beyond my lifespan).

MA’s dividend yield is razor thin, and therefore, the lion’s share of any return on a MA investment is likely to be from capital gains. If I grossly overpay, there is a very real risk that even an investment in a great company such as MA will lead to a sub-standard total return.

Determining a fair price for an investment is not an exact science, and therefore, the irrational exuberance we are currently witnessing is a factor as to why I am not currently adding to my exposure.

Investors should keep in mind that the low/high variance in MA’s share price within a calendar year can be significant; it is currently ~$384 and ~$528 as I compose this post. It might be prudent to sit on the sidelines in the hope of a much lower share price.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long MA.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.