When I last reviewed Paychex (PAYX) in this April 3, 2024 post, the most current financial information was for Q3 and YTD2024. In that post, I disclosed the purchase of additional shares @ ~$117.55.

Fast forward to October 1. We now have Q1 2025 results and shares are trading @ ~$140.80 as I compose this post.

Nothing has materially changed between the release of Q3 2024 results on February 29, 2024 and the release of Q1 2025 results on August 31, 2024. What could possibly justify a ~20% share price increase in 6 months!? In several recent posts I express my concern that valuations, in general, are too high. PAYX appears to be such a company.

Business Overview

Please review the company’s website and Part 1 in the company’s Form 10-K.

Financial Review

Q1 2025 Results

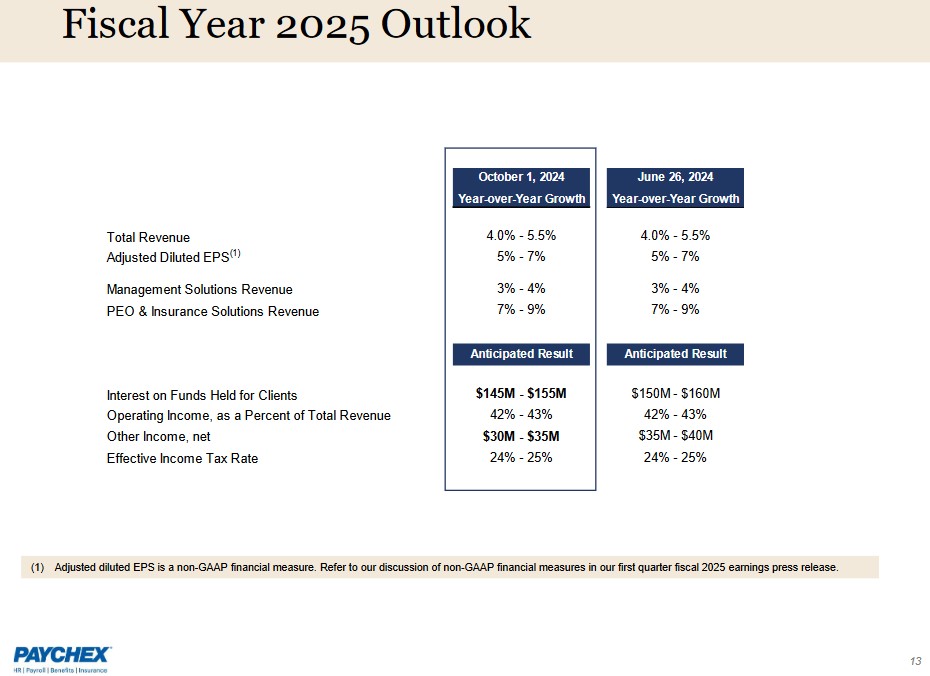

PAYX’s Q1 2025 results and FY2025 outlook are accessible here.

PAYX has recently launched new products that offer ‘digital and artificial intelligence (AI) driven solutions’ aimed at helping clients attract, retain, and engage their workforce. This is contributing to growth in PAYX’s customer base. The following are links to press releases about recent product launches:

- Paychex Introduces AI-Assisted Recruiting to Help Small Businesses Instantly Find Top Talent

- Paychex Launches Digital Employee Benefits Marketplace

- Paychex Announces Employee Engagement Solution

Revenue increased 3% to ~$1.3B in Q1. This reflects headwinds from the expiration of the Employee Retention Tax Credit (ERTC) program* and 1 less processing day as compared to Q1 2024. These two items impacted growth by ~400bps. Excluding these headwinds, total revenue grew ~7% in Q1.

* The ERTC is a refundable tax credit for certain eligible businesses.

Strong expense discipline enabled PAYX to generate $0.546B of cash flow from operations in Q1.

The 12-month rolling return on equity was ~46%.

FY2025 Outlook

The following reflects PAYX’s prior and current FY2025 outlook.

PAYX’s total revenue outlook is unchanged and continues to include ~200bps of headwind from the expiration of the ERTC program.

The two changes to guidance relate to interest rates.

Expectations are for interest rates in the US to drop over the next several months.

PAYX’s new outlook assumes a total of 125 bps of cuts to the short-term rate on a full year basis. Given that PAYX has billions of client funds from which it can generate interest, a declining interest rate environment has a negative impact.

Risk Assessment

No rating agency rates PAYX’s debt but PAYX’s risk is low.

At the end of Q1 2025, PAYX had current assets before funds held for clients of ~$3.598B. Of this total, ~$1.553B was cash, cash equivalents, and corporate investments and ~$1.68B was Accounts Receivable, net of allowance for credit losses and professional employer organization (PEO) unbilled receivables, net of advance collections.

At the end of Q1 2025, PAYX’s Current Assets before funds held for clients were ~2.4x more than Current Liabilities before client fund obligations; this was 2.16x when I last reviewed PAYX.

Total short-term and long-term borrowings of ~$0.818B are similar to prior recent quarters.

The following reflects the details of PAYX’s long-term debt. On March 13, 2019, PAYX completed the private placement of Senior Notes, Series A in an aggregate principal amount of $0.4B due on March 13, 2026, and Senior Notes, Series B in an aggregate principal amount of $0.4B due on March 13, 2029.

Full repayment of these Notes will further improve the company’s financial strength.

Dividends and Dividend Yield

PAYX currently does not reflect its dividend history on its website; the dividend history is accessible here.

Looking at PAYX’s historical capital allocation priorities, we see that steadily increasing the dividend ranks ahead of share repurchases.

In 2020, PAYX froze its quarterly dividend at $0.62/share given the uncertainty the COVID pandemic would have on its business. Other than this brief period, PAYX has consistently rewarded its shareholders with attractive dividend increases (post 2013).

Within days, PAYX will declare its 3rd consecutive $0.98/share quarterly dividend for distribution at the end of November.

In July 2021, PAYX’S Board approved a program to repurchase up to $0.4B of common stock with authorization expiring on January 31, 2024, at which time $157.9 million of unused repurchase authorization expired. In January 2024, PAYX’s Board approved a program to repurchase up to an additional $0.4B of common stock, with authorization expiring on May 31, 2027.

Share repurchases are not a capital allocation priority; repurchases are made to manage common stock dilution. This is borne out from the relatively stable weighted average number of outstanding diluted shares (in millions rounded) of 363, 365, 366, 365, 363, 363, 362, 362, 361, 362, 363, 362.3, and 362.1 in FY2012 – FY2024. The weighted-average diluted common shares outstanding in Q1 2025 was 361.9.

In FY2024, PAYX repurchased 1.5 million shares at a weighted-average price of $115.37. These shares were retired immediately upon purchase and were partially offset by $61.1 million stock-based compensation costs.

In Q1 2025, PAYX repurchased 828,855 shares for ~$0.104B (an average cost of ~$125.47). This was partially offset by $16.5 million stock-based compensation costs.

In my September 28, 2024 post, I provide a couple of examples of how the aggressive use of stock compensation can meaningfully distort a company’s FCF. Looking at PAYX’s Consolidated Statement of Cash Flows and weighted-average diluted common shares outstanding over the past several years, PAYX does not fall in this camp.

Valuation

PAYX’s FY2012 – FY2024 diluted PE levels are 20.19, 28.28, 26.08, 26.31, 28.32, 29.34, 23.44, 28.54, 31.80, 38.78, 28.53, 28.97, 26.47, and 28.48.

On April 2, 2024, I acquired shares at ~$117.55. I estimated PAYX would generate adjusted diluted EPS of $4.72 in FY2024 thus giving me a forward adjusted diluted PE of ~25; it ended up generating $4.72.

At the time, PAYX’s valuation based on adjusted diluted earnings broker estimates and my ~$117.55 share price were:

- FY2024 – 19 brokers – mean of $4.71 and low/high of $4.65- $4.74. Using the mean estimate, the forward adjusted diluted PE was ~25.

- FY2025 – 19 brokers – mean of $4.99 and low/high of $4.85 – $5.15. Using the mean estimate, the forward adjusted diluted PE was ~23.6.

- FY2026 – 12 brokers – mean of $5.30 and low/high of $5.20 – $5.47. Using the mean estimate, the forward adjusted diluted PE was ~22.

Management’s FY2025 outlook calls for a ~5% – ~7% increase from the FY2024 adjusted diluted EPS meaning a range of ~$4.96 – ~$5.05; in Q1 2025 it generated $1.16.

With the current share price being ~$140.80 and management’s ~$4.96 – ~$5.05 FY2025 adjusted diluted EPS outlook, we get a forward adjusted diluted PE range of ~27.9 – ~28.4.

Revisions to broker adjusted diluted earnings estimates are likely over the coming days but at the moment, we get the following using current estimates:

- FY2025 – 17 brokers – mean of $4.98 and low/high of $4.90 – $5.03. Using the mean estimate, the forward adjusted diluted PE was ~28.3.

- FY2026 – 17 brokers – mean of $5.29 and low/high of $5.18 – $5.37. Using the mean estimate, the forward adjusted diluted PE was ~26.6.

- FY2027 – 9 brokers – mean of $5.61 and low/high of $5.45 – $5.77. Using the mean estimate, the forward adjusted diluted PE was ~25.1.

PAYX typically generates FCF that slightly exceeds net earnings and I expect the same in FY2025.

In Q1 2015, it generated ~$0.510B of FCF. We can expect ~$2.042B of FCF in FY2025 if PAYX generates a similar amount of FCF in each of the next 4 quarters.

Erring on the side of caution, I estimate PAYX will generate ~$1.95B of FCF in FY2025 and the weighted average diluted shares outstanding should be ~361.9 million. Using these estimates, PAYX’s estimated FCF/share is ~$5.39. Divided the current ~$140.80 share price by ~$5.39 and the forward P/FCF is ~26.1. This is slightly higher than most levels during FY2014 – FY2024.

Final Thoughts

My final thoughts are unchanged from my April 3, 204 post.

My exposure currently consists of 839 shares (390 and 449 shares in a ‘Core’ and a ‘Side’ account, respectively) and it was my 27th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review.

I have been a PAYX shareholder since July 2, 2009. During this time, PAYX’s annual total investment return has been ~13.25% – ~15.53%; the return differs if the dividends were reinvested or not. The annual total investment return, however, drops to ~12.50% – ~13.33% if we change the time frame to September 30, 2019 – September 30, 2024 (5 years). This is not terrible considering a PAYX investment is low risk.

PAYX makes periodic bolt-on acquisitions but I expect annual revenue growth will remain in the 4% – 6% range unless is makes another major acquisition; PAYX completed its largest acquisition (Oasis) for $1.2B in December 2018.

It is also quite possible it will eliminate half its long-term debt in March 2026 and fully eliminate it in March 2029. Eliminating this debt would reduce annual interest costs by ~$33.74 million. In addition, PAYX’s capital allocation could change with the elimination of this $0.8B of debt. Hopefully, the valuation of PAYX’s shares might be sufficiently compelling to prompt the Board to ramp up share repurchases.

There are other investment opportunities that have the potential to generate superior long-term total annual investment returns. PAYX’s business, however, is predictable. Furthermore, it has the potential to become another holding in the FFJ Portfolio with billions of cash, cash equivalents, and corporate investments and NO long-term debt.

Having said this, I think low-risk PAYX is too richly valued. In my opinion, the annual total investment return over the next 5 years might be closer to ~9.5% – ~10.5% if we acquire shares at the current valuation. Applying the Rule of 72 to determine how long it will take for the value of an investment to double, it could take 7.2 years ( 72/10% = ~7.2 years).

This annual rate of return is likely to exceed the rate of inflation over the next several years. If your risk tolerance is low and you consider a doubling of your investment over 7.2 years to be suitable, then PAYX might be a company worth holding in your portfolio.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long PAYX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.