Johnson & Johnson (JNJ) is virtually irrelevant to my investment strategy, and therefore, I rarely look at this investment. With the release of the Q4 and FY2024 financial results on January 22, 2025, I figure this is the opportunity to look at it more closely.

Twice a year I disclose which companies are my top holdings; this includes exposure to accounts for which I do not divulge details. At the time of my 2024 Year End FFJ Portfolio Review, JNJ was my 21st largest holding constituting a mere 1.8% of our total holdings. At the time of my April 2021 review, it was ~2.95% of our overall holdings.

Some investors may disagree with my rationale for reducing my JNJ exposure. How could I think of reducing my exposure in a ‘Dividend King’ that has increased its dividend for 62 consecutive years?

Well….I have ~$25.8B litigation related expense reasons that JNJ incurred in FY2017 – FY2024; these expenses are ongoing.

Although JNJ generated ~$14B in after-tax net earnings from continuing operations in FY2024, let us not lose sight that ~$25.8B could have been used to enrich JNJ shareholders instead of law firms. Current JNJ shareholders are ‘holding the bag’.

Business Overview

JNJ is engaged in the research and development, manufacture and sale of a broad range of products in the healthcare field.

Following the completion of the separation of the Consumer Health business (Kenvue – (KVUE)) in August 2023, JNJ consists of the Innovative Medicine and MedTech business segments that focus on drugs and devices.

NOTE: KVUE now owns formerly JNJ’s highly recognizable brands.

A high level overview of JNJ and each segment is found on the company’s website and Part 1 Item 1 within the 2023 Form 10-K found within the SEC Filings section of the company’s website; the FY2024 Form 10-K is currently unavailable.

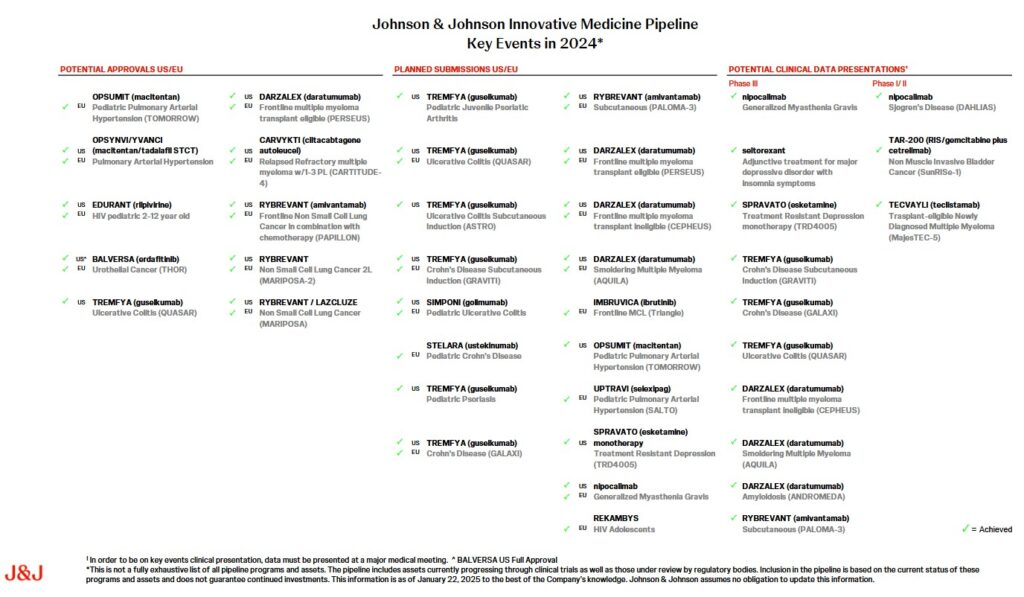

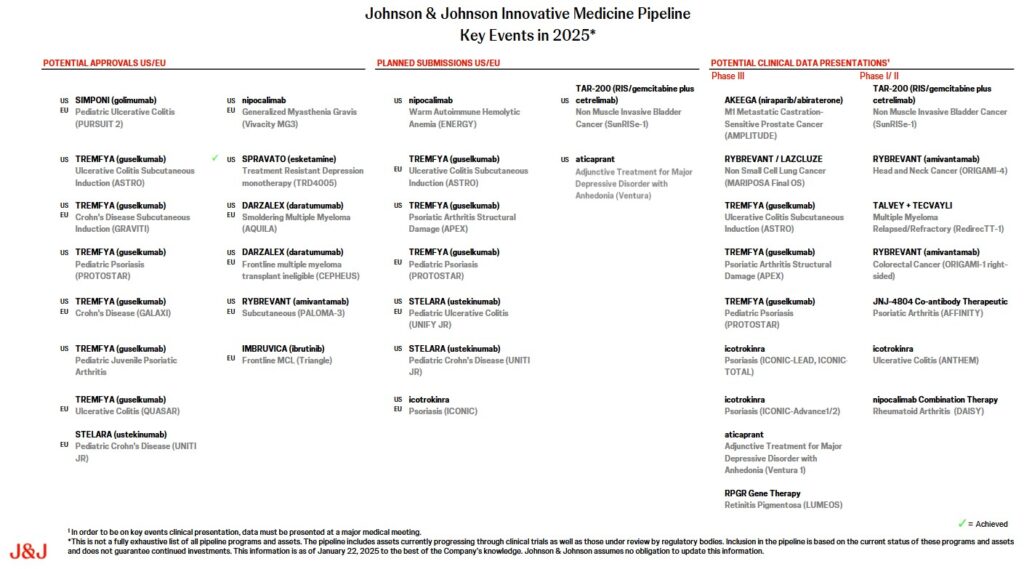

Pipeline

A robust pipeline is critically important for pharmaceutical companies. Extensive information on JNJ’s pipeline, key events, and patent expiration are accessible here.

The January 22, 2025 Earnings Release includes tables that reflect JNJ’s US, International, and Worldwide drug sales in Q4 and FY2024 within its Innovative Medicine segment. Despite a diverse pipeline, we see from these tables that JNJ generates a significant percentage of its revenue from a few drugs.

FY2024 revenue:

- Darzalex: $11.67B

- Stelara: $10.361B

- Invega Sustenna / Xeplion / Invega Trinza / Trevicta: $4.222B.

The FY2024 revenue from these 3 drugs was $26.253B or ~46% of JNJ’s FY2024 ~$56.964B worldwide revenue within its Innovative Medicine segment.

Drug development is extremely expensive. JNJ’s research and development expense in FY2023 and FY2024 was ~$15.1B and ~$17.23B, respectively.

Drug development goes through various phases before being eligible to apply for registration; the US Food and Drug Administration website (USFDA) has a good explanation of the various phases of the drug development process.

Pharmaceutical companies spend a considerable amount developing drugs with no assurance they will generate revenue. This is why major pharmaceutical companies acquire smaller pharmaceutical companies that have promising new drugs in later stages of the development process.

In addition to the cost of development, pharmaceutical companies have to contend with the time required to develop new drugs. Existing drugs within a company’s pipeline face patent expiry at which time generic drug producers can start producing competing drugs. For example, the patents for Stelara, one of JNJ’s top selling drugs, expired in the United States in September 2023 and in Europe in January 2024. Biosimilars of Stelara are likely to be available within the first half of 2025!

Pharmaceutical companies are also susceptible to competitors producing a superior product using a different formulation.

In addition to acquisitions made to enhance the Innovative Medicine segment, JNJ also acquires companies to expand its MedTech segment.

On May 31 2024, for example, JNJ completed the ~$13.1B acquisition of Shockwave Medical. Despite only generating ~$0.49B of revenue in FY2023, JNJ acquired Shockwave Medical to accelerate its position in the high-growth cardiovascular segments.

Intra-Cellular Therapies, Inc. Acquisition

On January 13, 2025, JNJ announced that it had entered into a definitive agreement to acquire all outstanding shares of Intra-Cellular Therapies (ICT), a biopharmaceutical company focusing on the development and commercialization of therapeutics for central nervous system (CNS) disorders, for $132.00/share in cash for a total equity value of ~$14.6B. ICT’s principal drug is Caplyta which is used to treat schizophrenia and depression.

The expectation is for the acquisition to close in the second half of 2025.

JNJ anticipates it will recognize ~$5B in annual Caplyta sales by the end of 10 years. It is also possible the drug’s approval could expand into new indications like major depressive disorder; ICT filed this new indication with the USFDA in late 2024.

Financials

Q4 and FY2024 Results

JNJ’s most recent financial results are accessible here.

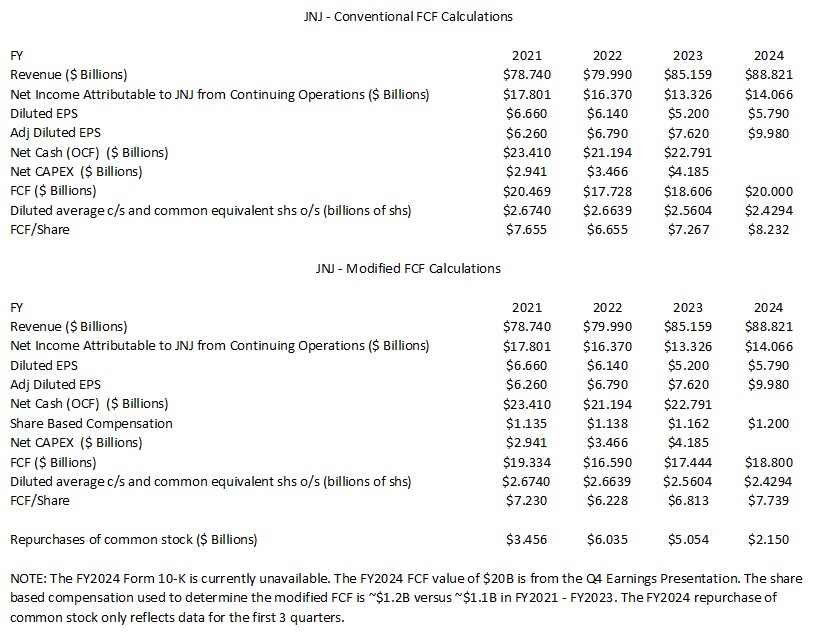

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2021 – YTD2024)

In several previous posts I touch upon why I am now taking a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. As explained in prior recent posts, I think we need to look at FCF using the conventional method AND a modified method; the modified method also deducts share-based compensation.

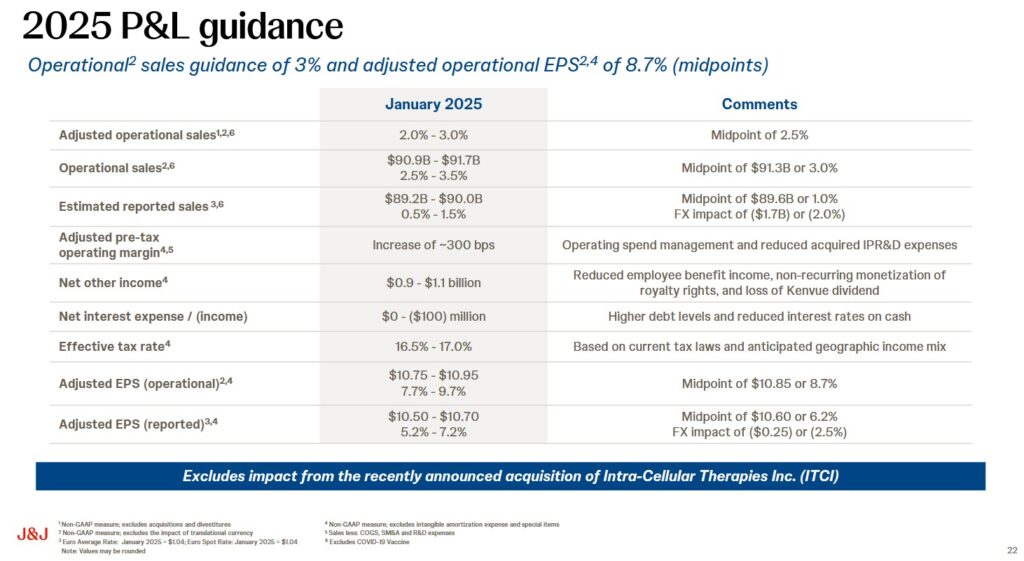

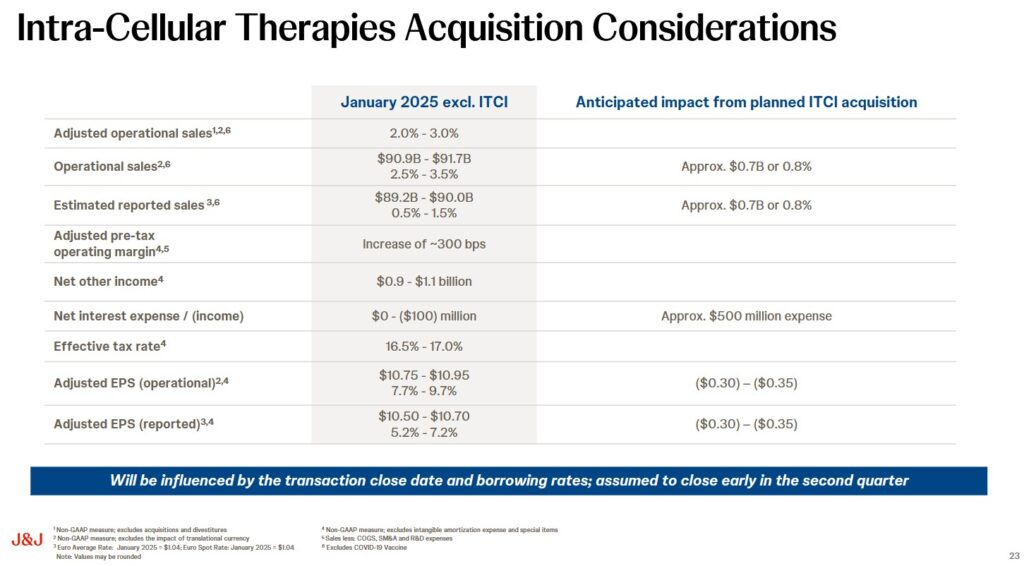

FY2025 Guidance

The following reflects JNJ’s 2025 guidance excluding the impact of the recently announced Intra-Cellular Therapies acquisition.

The anticipated impact from the recently announced acquisition is reflected below. We see that this acquisition will have a dilutive effect on earnings in the near term.

Credit Ratings

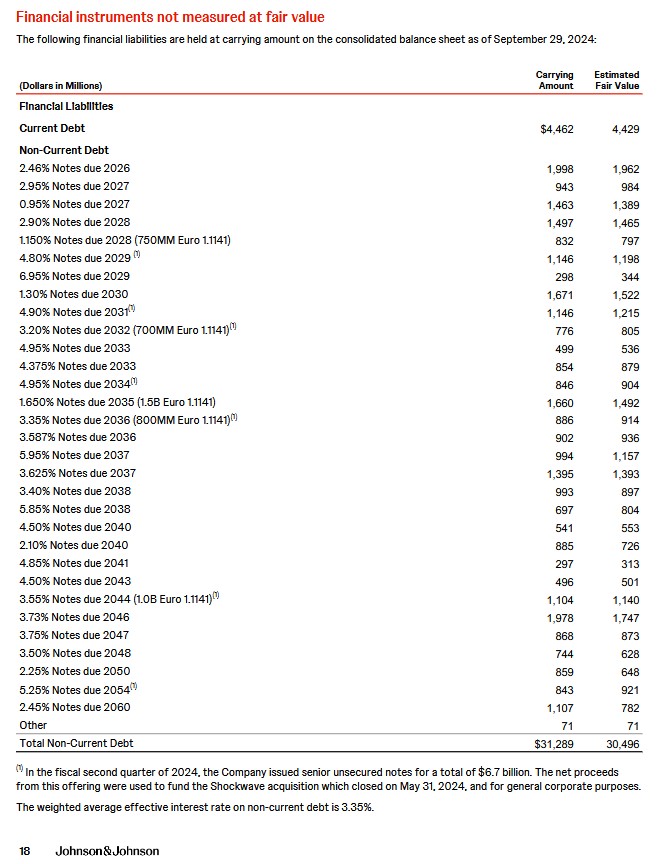

Since the Form 10-K is currently unavailable, I provide the schedule of debt at the end of Q3 2024. This schedule does not reflect any debt JNJ will incur to assist in the $14.6B acquisition of Intra-Cellular Therapies.

Moody’s continues to assign a AAA rating to JNJ’s senior unsecured domestic debt. This rating was affirmed January 14, 2025.

On January 22, 2025, S&P Global placed JNJ’s AAA local currency long-term debt rating under review with a negative outlook.

These ratings are the best and define JNJ as having an extremely strong capacity to meet its financial commitments.

Both ratings are investment grade and are acceptable for my purposes.

Dividend and Dividend Yield

JNJ’s dividend history is accessible here.

Although many investors gravitate to companies with attractive dividend metrics, I point out why dividends have drawbacks in this December 5, 2024 post.

JNJ’s capital allocation priorities were set well before the divestiture of KVUE and the significant litigation issues. The capital allocation priorities are to retain funds to grow the business, M&A, dividend distributions, and then share repurchases.

Once a company’s investor base expects to receive an ever increasing dividend, a decision to re-prioritize the dividend will undoubtedly negatively impact the company’s share price.

In FY2021 – FY2024, JNJ distributed ~$11B, ~$11.7B, ~$11.8B, and ~$11.8B in dividends for a total of ~$46.3B. If JNJ had distributed perhaps 50% of this amount in the form of dividends and had not incurred ~$25.8B (and counting) in litigation related expenses in FY2017 – FY2024, we would be looking at an even MORE formidable JNJ.

In FY2007, the weighted average diluted shares outstanding was 2910.7 million. In FY2021, the weighted average diluted shares outstanding was 2674.0 million. This is a reduction of 236.7 million shares in ~1.5 decades. By Q4 2024, this had been reduced to 2427.1 million or ~247 million fewer shares than in FY2021.

Since early FY2022, JNJ’s shares have been predominantly undervalued. If JNJ had not been hamstrung by its dividend policy, it could have repurchased an even greater number of shares in the last couple of years.

Valuation

It is pointless to compare JNJ’s historical, current and projected valuations because JNJ is morphing into a VERY different company following the KVUE spin-off.

Interestingly, however, the significant disparity between JNJ’s GAAP and non-GAAP EPS is ongoing.

- FY2020: $5.51 vs $8.03

- FY2021: $7.81 vs $9.80

- FY2022: $6.73 vs $10.15

- FY2023: $5.20 vs $9.92

- FY2024: $5.79 vs $9.98

Given the significant variance every year, I am hesitant to value JNJ on a PE basis. Nevertheless, for investors who like to value a company this way, I provide the following:

The closing share price on January 22, 2025 was $145.27. Using JNJ’s FY2024 results, the diluted PE and adjusted diluted PE are ~25.1 and ~14.6.

On a FCF basis, JNJ’s P/FCF is ~17.65 ($145.27/$8.232) and on an adjusted FCF basis it is ~18.8 ($145.27/$7.739).

The valuation using broker forward adjusted diluted EPS estimates and ~$145.27 is:

- FY2025: 20 brokers, mean estimate $10.52, low/high range $10.11 – $11.04. The valuation using the mean estimate is ~13.8.

- FY2026: 15 brokers, mean estimate $11.08, low/high range $10.30 – $11.63. The valuation using the mean estimate is ~13.1.

- FY2027: 6 brokers, mean estimate $11.57 low/high range $10.15 – $12.61. The valuation using the mean estimate is ~12.6.

- FY2028: 6 brokers, mean estimate $12.12 low/high range $10.57 – $13.08. The valuation using the mean estimate is ~12.

JNJ’s FY2025 guidance is for $10.50 – $10.70 in adjusted (reported) EPS. I, therefore, expect changes in the current range of the FY2025 broker estimates over the coming days.

NOTE: Take the FY2026 – FY2028 broker estimates with a ‘grain of salt’.

Final Thoughts

We hold the majority of our JNJ shares in a retirement account at an average cost of ~$68.37. When we converted Canadian dollars to acquire these shares, the foreign exchange rate was superior to the current (~$1.4364 CDN = $1 USD) foreign exchange conversion rate.

The shares held in a tax deferred account do not incur the 15% non-refundable dividend withholding tax. Those held in a taxable account do incur the tax.

Under the terms of Canada’s retirement accounts. will will eventually have to dispose of the JNJ shares and withdraw funds from the account; retirement account withdrawals incur tax at the tax holder’s personal marginal tax rate.

We will not be mandated to sell the JNJ shares held in the taxable account. This means we could potentially hold these shares well beyond those held in a retirement account. The return on our JNJ shares held in the two accounts could, therefore, be significantly different.

The time frame over which you are a JNJ shareholder will impact your rate of return. Use the Compound Annual Growth Rate Calculator on JNJ’s website to approximate your rate of return.

JNJ has undergone a significant transformation in recent years and its transformation in ongoing. It has exited the slower growth but more stable Consumer Health business. The focus is now on higher growth markets. With this higher growth, however, comes more uncertainty.

Within the past year, JNJ has completed the acquisition of Shockwave Medical for ~$13.1B and it has announced the proposed acquisition of Intra-Cellular Therapies for $14.6B with a target completion in the second half of FY2025….a total of $27.7B!

JNJ also faces patent expiration and/or the development of superior drugs by its competitors. It must, therefore, hope that some of the drugs within its pipeline receive FDA approval and that they become immensely profitable. Just because they receive FDA approval does not mean they will become blockbuster drugs.

I am not yet prepared to give up on JNJ despite it becoming virtually irrelevant to my investment strategy. Much like JNJ’s senior executives, I hope the strategic repositioning to become a higher growth and higher margin company pans out.

I do not intend to increase my JNJ exposure other than through the automatic reinvestment of dividends. In all likelihood JNJ will constitute even less than 1.8% of our total holdings by the time I complete my mid 2025 investment holdings review.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long JNJ.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.