Investors have witnessed a recent surge in Raytheon Technologies’ share price and may wonder ‘Is Raytheon Technologies a worthwhile investment?’

I last reviewed Raytheon Technologies (RTX) in mid-2021 in a guest post at Dividend Power at which time I drew the following conclusion…

‘As much as I think RTX is currently fairly valued and will reward shareholders over the long term, it is not my intent to acquire additional shares. I am satisfied with my current exposure but fully intend to increase my exposure to the aerospace and defence industry.’

…and elected to continue adding to my Lockheed Martin (LMT) position.

Since RTX and LMT released Q4 and FY2021 results on January 25, 2022, I now revisit RTX.

I encourage you to read my January 25, 2022 LMT post. In that post, I touch upon the Federal Trade Commission’s January 25, 2002 announcement stating it declines to approve LMT’s $4.4B acquisition of Aerojet Rocketdyne; this decision benefits RTX.

Business Overview

Since I have covered RTX in previous posts, I dispense with a brief Business Overview. However, I encourage investors unfamiliar with RTX to review the company’s website and to read Part 1 Item 1 within the 2020 10-K.

The Risk Factors section immediately follows the Business Overview section within the 10-K. In this section, various risks are described that could impact RTX’s business, financial condition, operating results and cash flows.

Financials

Q4 and FY2021 Results

On January 25, 2022, RTX released its Q4 and FY2021 results and an accompanying Earnings Presentation.

FCF of ~$5B was $0.5B better than expectations at the beginning of FY2021 primarily because of higher net income and lower CAPEX.

Merger Synergies

RTX continues to execute well on its synergy programs as it continues to drive structural cost reduction and productivity in its operations.

In FY2021, RTX achieved about $0.76B in incremental cost synergies from the RTX merger. This brings the total to over $1B since the completion of the April 2020 merger. This meets RTX’s original merger cost synergy target 2 years ahead of schedule; management expects further cost synergies.

In addition to these cost synergies, the Collins Aerospace team has achieved over $0.6B in total Rockwell Collins synergies since the November 2018 acquisition. This cost reduction means it has met its commitment a year ahead of schedule despite the significant downturn in RTX’s commercial aerospace business.

Acquisitions and Divestitures

RTX also continues to fine-tune its portfolio.

In FY2021, RTX completed the acquisition of SEAKR Engineering and FlightAware. This acquisition expands and enhances RTX’s capabilities in key growth areas.

RTX also completed the divestitures of:

- Forcepoint (completed in January 2021) for proceeds of ~$1.1B, net of cash transferred;

- Raytheon Intelligence and Space’s Global Training and Services business to Vertex Aerospace (completed in December 2021).

Outlook

RTX’s FY2022 Sales outlook is $68.5B – $69.5B; FY2021 Sales were $64.388B. Projections call for 7% – 9% to be organic sales growth.

Segment Outlook

Backlog at the end of Q4 2021 was $156B, of which $93B was from commercial aerospace and $63B was from defence. At the end of Q4 2020, RTX’s backlog was $150.1B, of which $82.8B was from commercial aerospace and $67.3B was from defence.

The Collins Aerospace and Pratt & Whitney segments are expected to witness the most significant increase in adjusted operating profit.

Source: RTX – Q4 and FY2021 Earnings Presentation – January 25, 2022

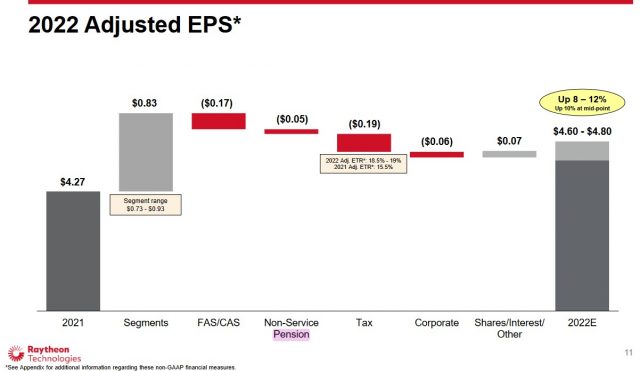

Adjusted EPS Outlook

Projections call for an 8% – 12% increase in adjusted EPS from FY2021.

Source: RTX – Q4 and FY2021 Earnings Presentation – January 25, 2022

RTX’s 4 segments are forecast to generate ~$0.83 of EPS growth at the midpoint of the outlook range. From there, non-service pension will be a headwind, primarily due to lower CAS recovery and higher discount rates.

NOTE: The FAS/CAS pension adjustment is the difference between SFAS No. 87 (FAS) pension expense or income and the Cost Accounting Standards (CAS) (the standards that prescribe the allocation to and recovery of pension costs on U.S. government contracts) pension expenses.

A 18.5% – 19% FY2022 tax rate is forecast versus 15.5% in FY2021. This is primarily due to one-time tax benefits from the FY2021 optimization of RTX’s legal entity and operating structure. This Q3 2021 benefit will not repeat. This will result in a $0.19 headwind.

A $0.06 corporate expenses YoY headwind projection is due to higher investment in synergy projects and digital transformation initiatives.

Lower share count, interest and other items will be a $0.07 tailwind.

These items result in an FY2022 $4.60 – $4.80 EPS earnings estimate.

Free Cash Flow (FCF) Outlook

FY2022 $6B FCF guidance is an increase from the ~$2.5B and ~$5B levels in FY2020 and FY2021.

RTX’s strong FCF provides it with flexibility when it comes to:

- reinvesting in the business;

- debt repayment;

- share buybacks; and

- dividend increases.

Source: RTX – Q4 and FY2021 Earnings Presentation – January 25, 2022

FY2022 Priorities

RTX has repeatedly indicated that dividend increases and share repurchases are two means by which it intends to increase shareholder returns. It is committed to returning at least $18B – $20B to shareholders in the first 4 years following the merger. However, RTX’s CFO stated at the May 18, 2021 Investor Day that the plan is to return more than $20B to shareowners in the 4 years post-merger; this was reiterated by RTX’s Chairman & Chief Executive Officer on the Q4 earnings call.

Source: RTX – Q4 and FY2021 Earnings Presentation – January 25, 2022

Credit Ratings

Moody’s currently rates RTX’s senior unsecured domestic currency debt Baa1. This is the top tier of the lower medium grade category.

This rating defines RTX as having an ADEQUATE capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to meet its financial commitments.

S&P Global rates it A- with a negative outlook. This rating is one notch higher than that assigned by Moody’s and is the lowest tier of the upper-medium grade category.

S&P’s rating defines RTX as having a STRONG capacity to meet its financial commitments. However, it is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Both ratings are investment grade and are acceptable for my purposes.

Dividend and Dividend Yield

RTX’s dividend history is relatively brief as the merger of United Technologies and Raytheon only occurred in 2020; the dividend history for each company before the merger is provided on its website.

With shares currently trading at ~$90, the $0.51 quarterly dividend yields ~2.3%.

Investors can expect a 4th consecutive $0.51 quarterly dividend announcement within the next 2 weeks. I envision a ~$0.04 – $0.055 dividend increase announcement in early April. This would result in a ~$2.24 annual dividend for a dividend yield of ~2.5% based on the current share price.

RTX distributed $2.732B and $2.957B of dividends in FY2020 and FY2021.

RTX’s weighted average number of issued and outstanding shares in FY2011 – FY2021 (in millions rounded) is 907, 915, 912, 883, 826, 799, 810, 864, 1,358, and 1,509. The significant increase in RTX’s share count is attributed primarily to the merger of United Technologies and Raytheon (refer to the 9 Months Ended September 30, 2020 column on the Condensed Consolidated Statement of Changes in Equity found on page 8 of 78 in RTX’s Q3 2021 Form 10-Q).

This merger closed on April 3, 2020. This distorts the weighted average number of diluted outstanding shares in FY2020. We, therefore, can not merely compare the FY2020 and FY2021 share count and say that the $2.327B of share repurchases in FY2021, of which $0.327B was in Q4, was not effective in adding shareholder value.

In the first 9 months alone of FY2021, RTX repurchased ~24,177 of shares for ~$2B of shares for an average purchase price of ~$82.7/share. With shares currently trading at ~$90, the share repurchases added shareholder value.

On September 30, 2021, management had the remaining authority to repurchase approximately $3.0B of common stock under its December 7, 2020 share repurchase program. Under this program, shares may be purchased on the open market, in privately negotiated transactions, under accelerated share repurchase programs.

Included in RTX’s FY2022 outlook are share repurchases of at least $2.5B.

Investors can expect RTX’s Board to set the appropriate share repurchase program limits to enable management to continue with ongoing share repurchases.

Valuation

In my October 1st, 2020 post, I indicated that using Earnings per Share (EPS), which takes into account the significant non-cash related goodwill impairment charges incurred in Q2 2020, would render us unable to calculate RTX’s P/E since there were no earnings.

Using forward-adjusted diluted EPS estimates reflected on the two discount brokerage platforms I use and the current $57.45 share price, I arrived at the following valuations:

- FY2020: 18 brokers, mean estimate $2.87, low/high range $2.12 – $3.62. Valuation using mean estimate is ~20 and ~16 using the upper end of the range.

- FY2021: 17 brokers, mean estimate $3.85, low/high range $3.34 – $4.85. Valuation using mean estimate is ~15 and ~12 using the upper end of the range.

When I reviewed RTX in my May 18, 2021 post, management’s FY2021 forward-adjusted diluted EPS guidance was $3.50 – $3.70 and the current share price was ~$85.40. On this basis, the forward adjusted diluted PE range was ~23.1 – ~24.4.

In my July 30, 2021 Guest Post at Dividend Power, RTX was trading at ~$88 and management’s FY2021 forward-adjusted diluted EPS guidance had been revised upwards to $3.85 – $4 giving us a forward-adjusted diluted PE range of ~22 – ~23.

I expected broker estimates to be adjusted over the coming days following the July 27 Q2 earnings release. Using the guidance currently available from the 2 trading platforms I use, I arrived at the following forward-adjusted diluted PE valuations.

- FY2021: 23 brokers, mean estimate $3.98, low/high range $3.68 – $4.35. Valuation using mean estimate is ~22 and ~20 using the upper end of the range.

- FY2022: 23 brokers, mean estimate $4.99, low/high range $4.30 – $5.70. Valuation using mean estimate is ~17.6 and ~15.43 using the upper end of the range.

- FY2023: 17 brokers, mean estimate $6.09, low/high range $5.44 – $6.89. Valuation using mean estimate is ~14.4 and ~12.78 using the upper end of the range.

RTX is now trading at ~$90 and management’s FY2022 adjusted EPS outlook is $4.60 – $4.80. On this basis, the forward adjusted diluted PE range is ~19 – ~20.

Using the guidance currently available from the 2 trading platforms I use, however, I arrive at the following forward-adjusted diluted PE valuations.

- FY2022: 19 brokers, mean estimate $4.87, low/high range $4.68 – $5.33. Valuation using mean estimate is ~18.5 and ~17 using the upper end of the range.

- FY2023: 17 brokers, mean estimate $5.86, low/high range $5.31 – $6.60. Valuation using mean estimate is ~15.4 and ~13.6 using the upper end of the range.

- FY2024: 11 brokers, mean estimate $6.75, low/high range $6.10 – $7.46. Valuation using mean estimate is ~13 and ~12 using the upper end of the range.

I expect broker adjustments over the coming days and the above estimates may come in lower than current levels; estimates have been declining over the last 3 months.

I view RTX to be fairly valued based on current forward earnings estimates.

Final Thoughts

I recommend investors hold shares in both LMT and RTX to benefit from the signing of the US government’s $0.74B bipartisan Defense Authorization bill; this is ~$25B higher than the original Presidential request.

Furthermore, the global threat environment should continue to drive strong demand internationally for RTX’s products and services.

I initiated a position in United Technologies on April 18, 2008 in an account for which I do not disclose details. Subsequently, I acquired UTX shares on October 22, 2018 and on June 11, 2019 for one of the ‘Side’ accounts within the FFJ Portfolio; all these shares subsequently became RTX shares upon completion of the merger. I also received Otis Worldwide Corporation (OTIS) and Carrier Global Corporation (CARR) shares when these entities were spun off from UTX.

I acquired an additional 300 RTX shares at $57.45/share for one of the ‘Core’ accounts within the FFJ Portfolio and disclosed this purchase in my October 1, 2020 post.

In my mid-April 2021 review, RTX was my 24th largest holding; it was not a top 30 holding at the time of my mid-August 2020 review. RTX is now my 22nd largest holding as per my January 7, 2022 holdings review.

RTX investors have come to expect dividend increases. I, however, favour share repurchase over dividends as a means by which companies can reward shareholders. The drawbacks with dividend income are:

- as a Canadian resident I incur an immediate 15% withholding tax when shares in US companies are held in a taxable account; and

- I have to claim dividend income on my annual tax return.

Share repurchases, however, attract no tax liability until I sell shares. I can delay any tax liability for decades if I never sell.

While I recommend shares in both companies, I favour LMT over RTX. LMT’s credit risk and Free Cash Flow generating abilities are superior to those of RTX. I also like that LMT is making a far more meaningful reduction in its share count than RTX.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long LMT and RTX.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.