The world of equities consists of fuel generators and fuel suckers. I use this terminology to describe the types of companies that either fuel or hamper wealth creation.

Both categories include companies that:

- distribute no dividend, or that have unimpressive dividend metrics; and

- have alluring dividend metrics.

This is why it is so important to analyze a company when making investment decisions as opposed to merely investing in a company based on share price behavior or dividend metrics.

Quite often, the companies with alluring dividend metrics may appear to be attractive investments because of the dividend income periodically credited to an investor’s account. Upon closer examination, however, the underlying fundamentals of the company are less than impressive. Furthermore, such companies can generate a long-term total investment return well below that of companies that retain earnings and free cash flow to compound at attractive rates.

In this post I contrast the historical long-term total investment return of BCE Inc. (BCE), a widely held Canadian fuel sucker, and 9 companies held within the FFJ Portfolio and/or retirement accounts (for which I do not disclose details) that either issue no dividend or that have less than impressive dividend metrics.

Mea Culpa

I confess that I have fallen into the trap of using some dividend metrics to influence my investment decisions. I never, however, thought companies with very attractive dividend yields were wise investments. Furthermore, I stayed away from Real Estate Investment Trusts (REIT) like the plague although I did have negligible exposure to one which I eventually ‘punted’ because it was a terrible investment.

I have also had my fair share of other ‘fuel suckers’. Looking back, my exposure to almost every single one of them came about because I paid too much attention to their dividend metrics.

At one time, terms such as Dividend Achievers, Contenders, Aristocrats, Champions, and Kings factored into my decision on what companies to analyze. Fortunately, I eventually came to the realization that many such companies were actually ‘handcuffed’ because the dividend ranked high on the list of capital allocation priorities.

In some cases, the dividend is a capital allocation priority because reinvesting in the business will generate sub-par returns. These are typically companies operating in an industry where the total addressable market is not growing or is shrinking (eg. tobacco). If reinvesting in the business will generate sub-par returns, why invest in the company to begin with!?

At the other end of the spectrum are profitable companies that generate strong free cash flow (FCF) and that prioritize their capital allocation as follows:

- Reinvest in the business – debt repayment, funding organic growth, and/or mergers and acquisitions;

- Share repurchases;

- Dividend distributions.

These companies essentially have 3 different levers to pull so as to generate attractive total long-term shareholder returns.

When a company:

- generates strong FCF but has little growth potential; and/or

- establishes dividend distributions as a primary capital allocation method

it attracts shareholders that desire and prioritize income. Once investor expectations are set, a company can not easily alter its capital allocation priorities without upsetting its investor base.

Imagine a company that experiences a share price plunge.

If it is a great company, an improvement in the valuation might present an opportunity to repurchase undervalued shares.

If the company prioritizes dividend distributions from a capital allocation perspective, it may not have the financial wherewithal to aggressively repurchase attractively valued shares; a decision to repurchase undervalued shares would be approached from an unenviable position. On the other hand, had funds been retained to create a fortress Balance Sheet, any decision to repurchase shares would be approached from a position of strength. The company could, for example, potentially borrow to repurchase a significant number of undervalued shares without the risk of credit rating downgrades.

Fuel Suckers

Avoid such companies.

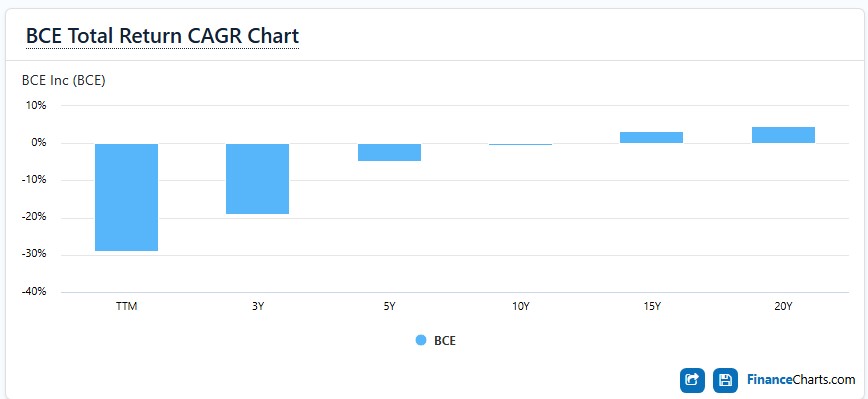

Fuel sucker BCE was founded in 1880. It is a Canadian communications company that provides wireless, wireline, internet, streaming services, and television (TV) services to residential, business, and wholesale customers in Canada. It operates in two segments: Bell Communication and Technology Services, and Bell Media.

At one time, BCE essentially was a monopoly. Over time, the Canadian telecommunications industry evolved into an oligopoly. In the past decade and a half, new entrants have been permitted to enter and BCE is no longer a cash generating machine.

Its capital allocation priorities are such that it was once known as a ‘widows and orphans’ stock. Being handcuffed to investor expectations of a steadily increasing dividend, however, has contributed to BCE burning through cash.

FCF? Non-existent for a few years.

Some investors may like BCE for its dividend (see dividend history). BCE’s business, however, has deteriorated dramatically and it now generates insufficient cash flow to fund its normal business operations, repay its debt, AND service its dividend.

Looking at BCE’s credit ratings, we immediately see a ‘red flag’. The lowest investment grade is assigned to the subordinated debentures. Equity investors are exposed to even greater risk than the debenture holders, and therefore, have ‘junk’ risk exposure.

The company may not necessarily be about to go out of business. In the universe of possible companies in which to invest, however, why assume this risk given the abysmal investment returns?

As evidence of the dire nature of BCE’s situation, the company announced in September 2024 of its decision to sell its 37.5% stake in Maple Leaf Sports & Entertainment (MLSE) for CDN$4.7B to Rogers Communication; MLSE owns the Toronto Maple Leafs and Toronto Raptors. The sale, expected to close in mid-2025, will provide BCE with much needed cash. This cash, however, will help BCE finance its ~CDN $5B acquisition of Ziply in the US.

Another ‘red flag’ is BCE’s current dividend yield which is just shy of 12% (a $0.9975 quarterly dividend and a ~CDN$34 share price). A dividend yield of this magnitude is such that it is inevitable a dividend cut is forthcoming; a 50% reduction is a very reasonable probability.

Some investors might consider that all the bad news is baked into BCE’s share price. In essence, they are hoping things can’t get any worse. Given this, some investors might lull themselves into investing in BCE based on what will likely still be a ~5% – ~6% dividend yield. This line of thinking strikes me as crazy but some pundits think this is an opportune time to invest in the company. They make the case that money previously used for dividend distribution purposes will now be able to be redirected toward debt repayment.

Let’s, however, put things in perspective!

In FY2024, BCE reported:

- Interest Expense: $1.713B

- Dividends on Preferred Shares: $0.187B

- Dividend on Common Shares: $3.613B

- Current Portion of Long-Term Debt: $7.669B

- Long-term Debt: $32.835B

Suppose BCE reduces the annual common share dividend outflow to $1.8065B (50% reduction from $3.613B). The company has $40.504B of debt. To what extent is $1.8065B/year going to make a dent in the company’s indebtedness? It might be a step in the right direction but equity investors will still have ‘junk’ exposure.

BCE’s total investment return over the long-term is horrible and there is little reason to think BCE’s future is likely to materially improve. This is a highly capital intensive business operating in a highly regulated industry!

I recognize past performance is not indicative of future performance. Realistically, however, what is the probability that BCE will generate returns comparable to the following ‘fuel generators’?

Fuel Generators

Long-term fuel generators instill a greater degree of confidence than fuel suckers that future returns are likely to be attractive.

Fuel generators produce attractive total long-term investment returns (ie. solid top line growth, attractive margins, earnings, and FCF). Although they may not necessarily have the strongest credit ratings, their risk profile often improves over time. In addition, they have the ability to aggressively repurchase shares if/when the valuations suggest share repurchases are a wise method of allocating capital.

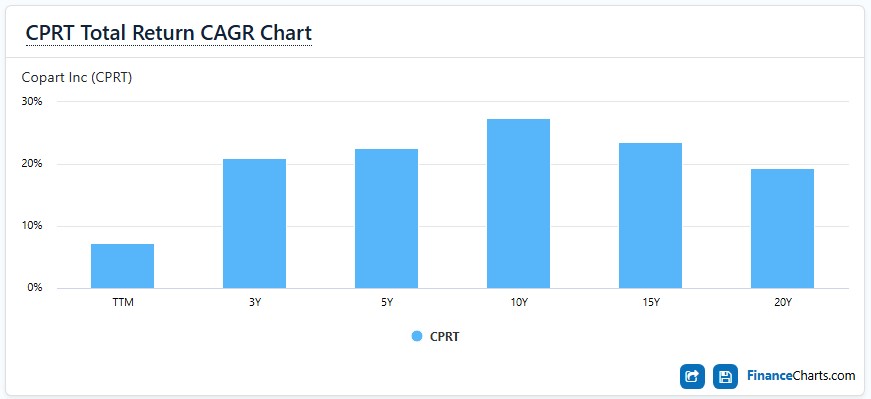

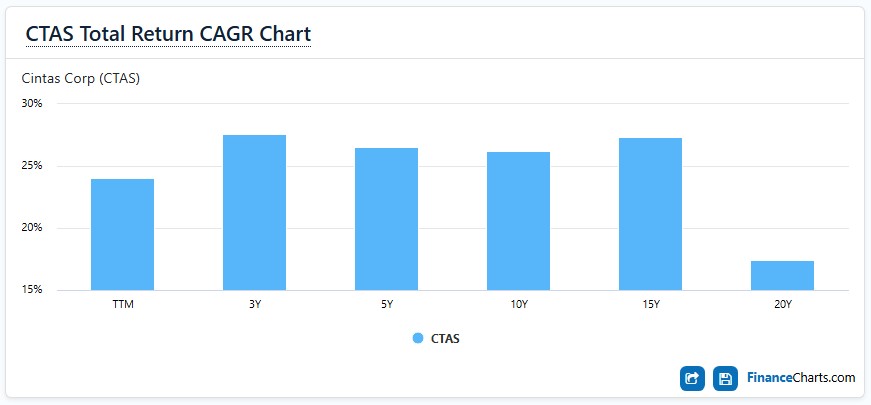

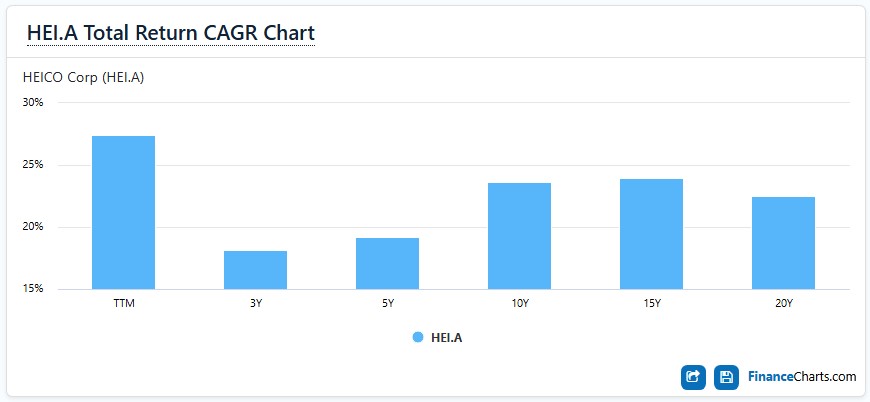

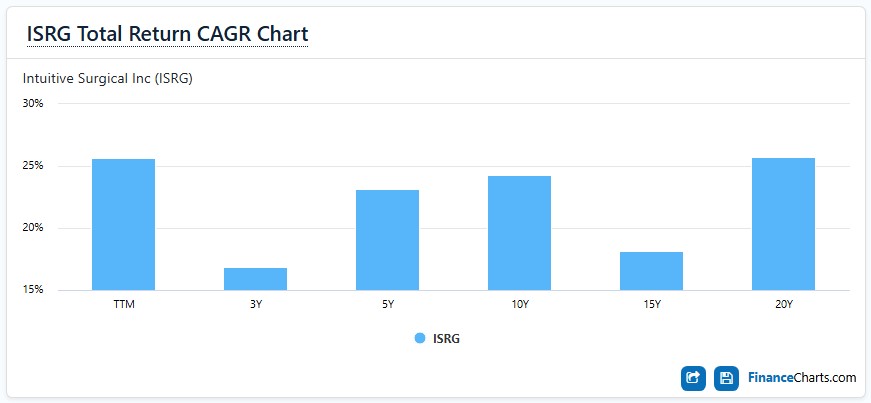

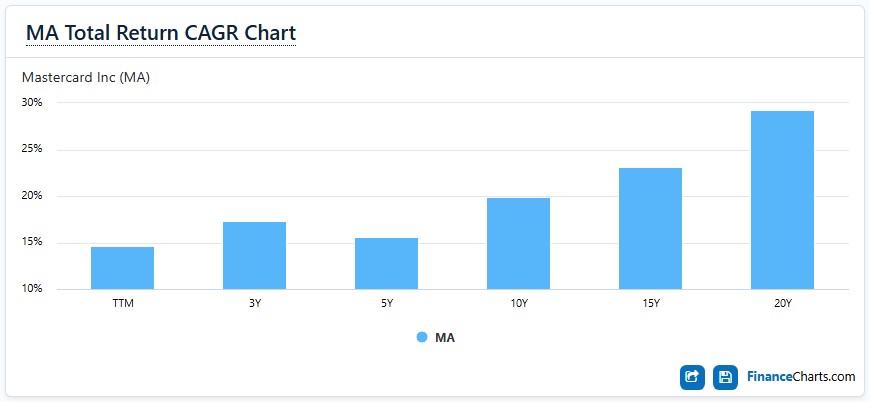

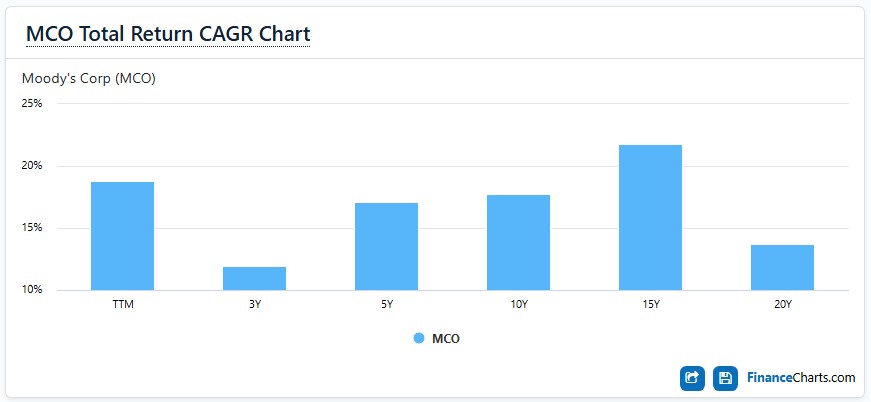

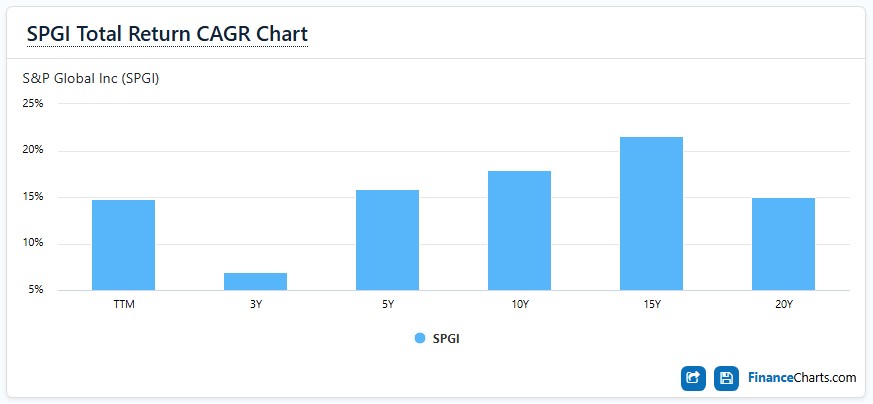

Compare the long-term total investment returns of the following fuel generators to that of BCE, the fuel sucker.

Copart

Cintas

HEICO Class A

Intuitive Surgical

Mastercard

Moody’s

S&P Global

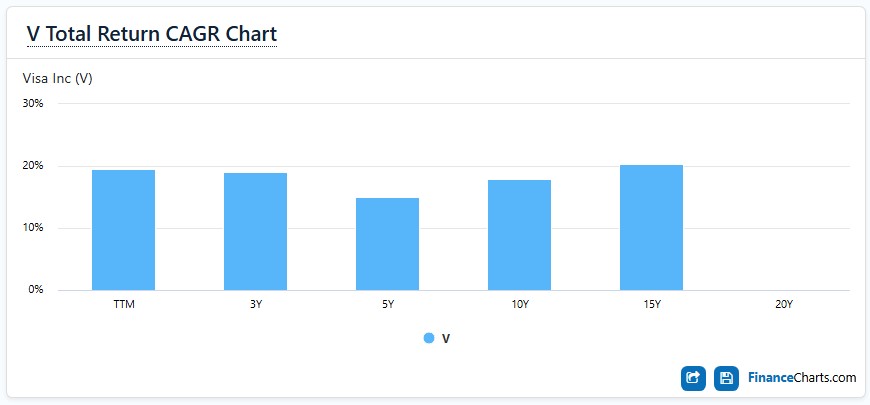

Visa

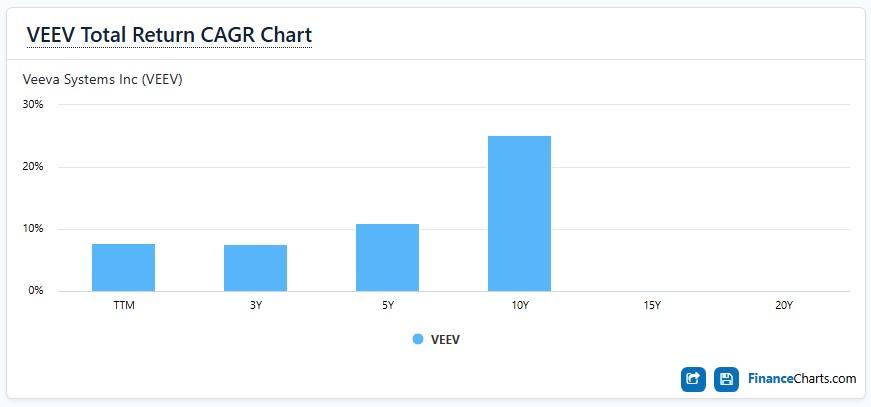

Veeva

NOTE: Visa (V) has not been a publicly listed company for 20 years and Veeva (VEEV) has not been a publicly listed company for 15 years.

Final Thoughts

Naturally, past performance is not indicative of future performance. Furthermore, attractive returns from fuel generators is heavily dependent on the acquisition of shares at attractive or reasonable valuations.

This is why investing in fuel generators when the investing world is in turmoil can lead to impressive long-term returns. The companies might end up experiencing short-term headwinds but their long-term outlook might not materially change. When investing in them, we must have what it takes to withstand challenging times since the duration of challenging times is unknown.

If you are a long-term investor, gravitate toward fuel generators. While they may not have attractive dividend metrics, of far greater importance are the company’s capital allocation priorities, profitability, growth, risk, and valuation. The competitive landscape (eg. to what extent is the company’s competitive position likely to be disrupted?) and the extent to which management has ‘skin in the game’ are also key considerations.

In addition, limit your investments to companies with excellent and ethical management. Let them manage the business during a period in which someone ‘certifiable’ is creating turmoil. Short-term business results may deteriorate but this should be expected. Business conditions are not always ‘rosy’.

Remember that corrections are healthy. Master your mindset and think like an owner when investing. Invest from the perspective of what your investment holdings can do for you over the long-term.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.