I last reviewed Intuitive Surgical (ISRG) in this June 10, 2025 post at which time the most currently available financial information was for Q1 2025. With the recent release of Q2 and YTD2025 results, I revisit this existing holding.

Business Overview

The Overview section commencing on page 26 of 58 in the Q2 2025 Form 10-Q provides a good overview of the company, a trade and tariffs update, an overview of the macroeconomic environment, and an explanation of the company’s business model. The company’s website and the FY2024 Form 10-K are also very good sources of information.

ISRG used to be ‘the only game in town’ but competition is increasing. With an increase in competition, the expectation is for price reductions and an increase in innovation. Nevertheless, ISRG is investing heavily in research and development to remain the industry leader. While this bulletin from the American College of Surgeons is from May 2023, it provides an indication of how the overall use of robotic surgery is likely to continue to grow significantly over the coming years.

Recent Press Releases

ISRG has 3 very interesting News Releases so far in the month of July 2025.

The July 16 Press Release touches upon how ISRG demonstrated its telesurgery capabilities by remotely connecting two surgeons to perform a transatlantic demonstration at the Society of Robotic Surgery (SRS) conference in Strasbourg, France.

ISRG’s Press Release states:

This landmark event involved Doug Stoddard, MD, located in Peachtree Corners, GA, and Andrea Pakula, MD, located remotely in Strasbourg, France. Together, using a dual console da Vinci 5 system, they performed a telesurgery procedure on an advanced tissue model developed by Intuitive to replicate the behavior of live tissue.

During the demonstration, Stoddard, whose console was alongside the da Vinci 5 patient cart and tissue model, was able to pass control of surgical instruments back and forth remotely to Pakula, located at the remote surgeon console. This included Force Feedback, enabling both surgeons to feel the forces exerted on the advanced tissue model by the instruments, despite being more than 4,000 miles apart.

It should be noted that ‘the telesurgery software on the da Vinci 5 system that was shown during this demonstration was used for demonstration purposes only. The technology is still in development, is not 510(k) cleared or CE marked, and the safety and effectiveness of the product has not been established’. Nevertheless, this recent demonstration shows how ISRG is building the infrastructure to support safety, reliability, and consistent use of its technology with the goal of:

- improving patient outcomes;

- improving patient and care team experience;

- increasing access to minimally invasive care; and

- lowering the total treatment cost.

Interestingly, The Baylor College of Medicine reported in June 2025 that its surgeons at Baylor St. Luke’s Medical Center successfully performed a fully robotic heart transplant on an adult patient. This is the first such procedure reported in the United States.

Surgeons generally note several clear advantages for surgeons and patients with the use of ISRG’s equipment (specifically the da Vinci robotic systems) with the following being key:

-

Surgeons highlight the system’s capability to deliver extraordinary precision, particularly with its latest haptic “Force Feedback” technology which allows for more careful manipulation of tissues using the robotic arms. More information about ‘Force Feedback’ is accessible here.

-

The console setup improves surgeon ergonomics by allowing them to operate while seated and reduces fatigue over long surgeries. This ergonomic benefit is absent from traditional or laparoscopic surgery.

-

The 3D, high-definition imaging provides magnified and immersive views of the surgical field, improving surgical accuracy and the ability to operate in confined spaces.

-

The robotic “wristed” instruments move with a superior range of motion compared to conventional laparoscopic tools, enabling more intricate and delicate procedures. Many surgeons have noted improved comfort and performance, especially during lengthy or complex cases.

Research and Development

ISRG’s success has not gone unnoticed thus attracting an increase in competition. The company, however, is continually improving upon its technology (the cumulative research and development (R&D) amounts to $3.023B in FY2022 – FY2024 and another $0.630B in the first half of FY2025). This heavy R&D investment is an indication that ISRG is not resting on its laurels.

ISRG continues to expand its manufacturing operations and supply chain capabilities to support the mid-2025 broad launch of da Vinci 5. In the broad launch, ISRG will incorporate the latest fully integrated hardware and software.

As robotic-assisted surgery advances, integrating force feedback into retained practice could enhance precision and improved recovery across disciplines. This technology is a breakthrough feature in the da Vinci 5 robotic surgical system. It allows surgeons to feel the push and pull forces exerted on tissue during surgery, enhancing precision and control.

The force feedback instruments are currently in limited supply but the company expects broad availability at the end of 2025.

Information about this technology is accessible on the company’s website.

Financials

Q2 and YTD2025 Results

The Q2 2025 Form 10-Q is accessible through the SEC Filings section of the company’s website.

ISRG ended Q2 2025 with ~$9.5B in cash and investments, up from $9.1B in Q1 2025. The sequential increase was driven by operating cash flow, partially offset by ~$0.181B of stock repurchases and ~$0.155B in CAPEX.

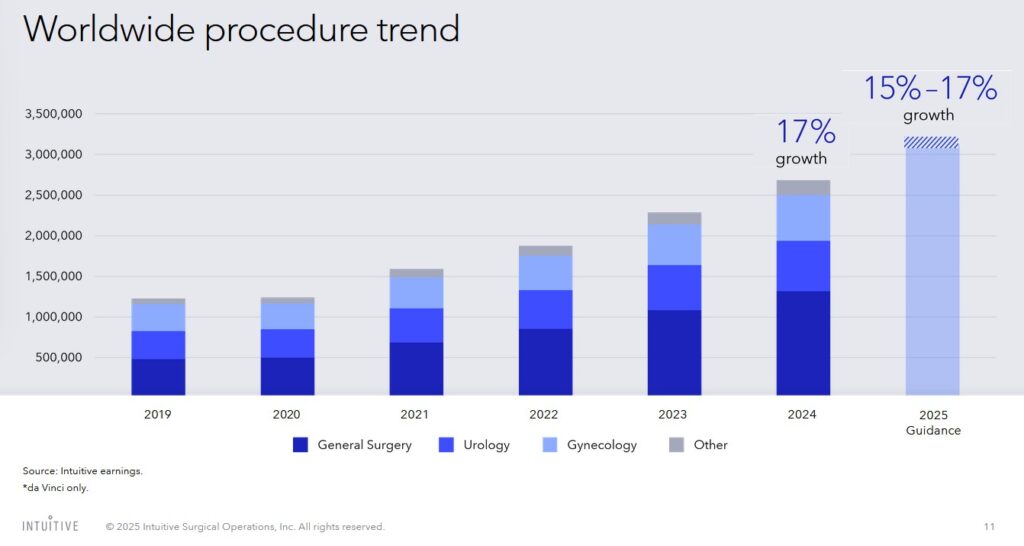

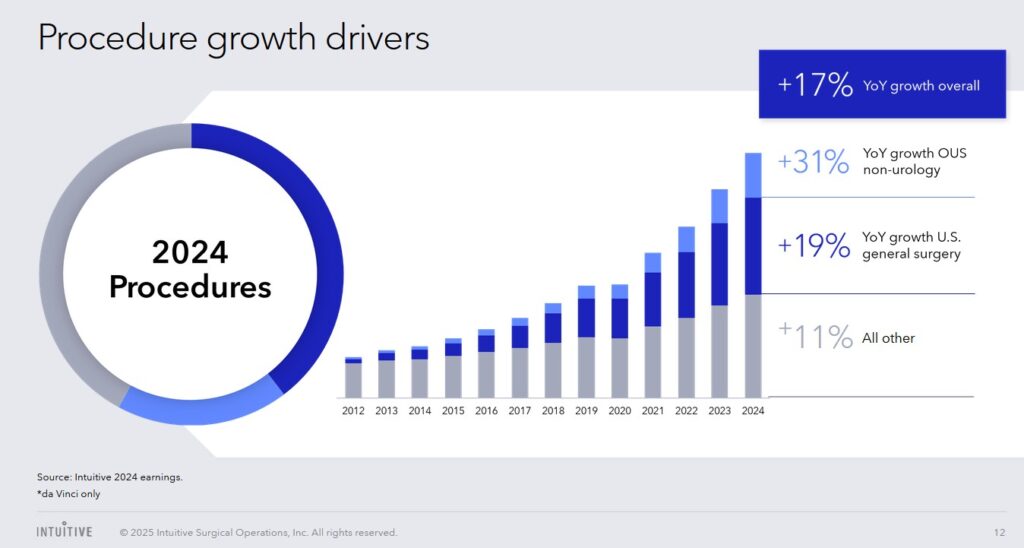

Important metrics to monitor the extent to which ISRG is growing are the installed base and procedures performed by the various da Vinci and and Ion platforms. Several pages are devoted to these important metrics in the Q2 2025 Form 10-Q commencing on page 39 of 58 beginning with the Second Quarter 2025 Operational and Financial Highlights.

The following FY2024 data and procedure growth trend and drivers were provided at ISRG’s May 1, 2025 Annual General Meeting.

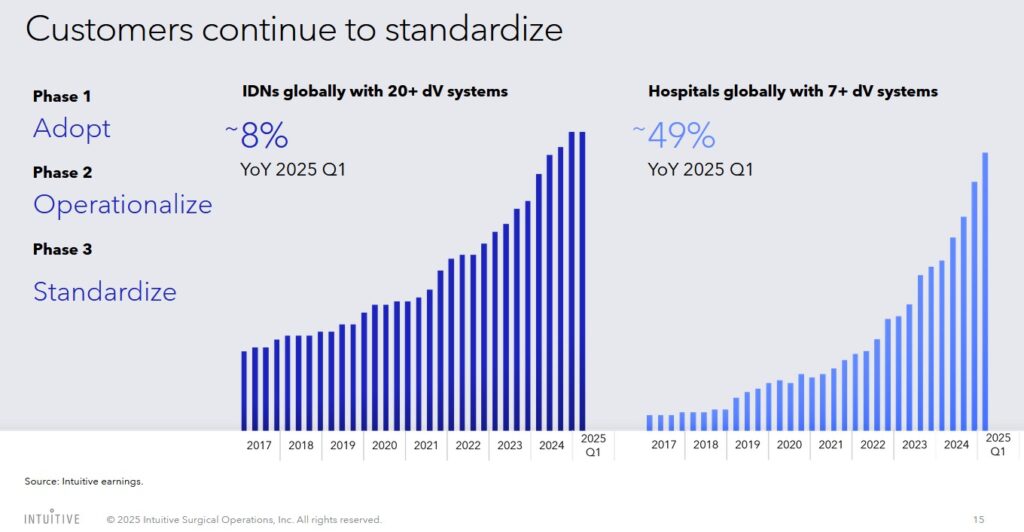

Typically, a phase 1 customer will install 1 ISRG system to ‘test’ whether robotic surgery improves patient care. If the results are positive, hospitals will add one or two more systems. Once a hospital expands its installed base to 3+ ISRG platforms, ISRG has a ‘locked in’ customer. This is because it is extremely disruptive and difficult to displace a system with which operating room staff have become extremely adept at using.

NOTE: IDNs are integrated delivery networks. This is corporate ownership groups of hospitals that own 20 or more hospitals within their group. These are highly sophisticated businesses that can analyze the performance of robotic surgery.

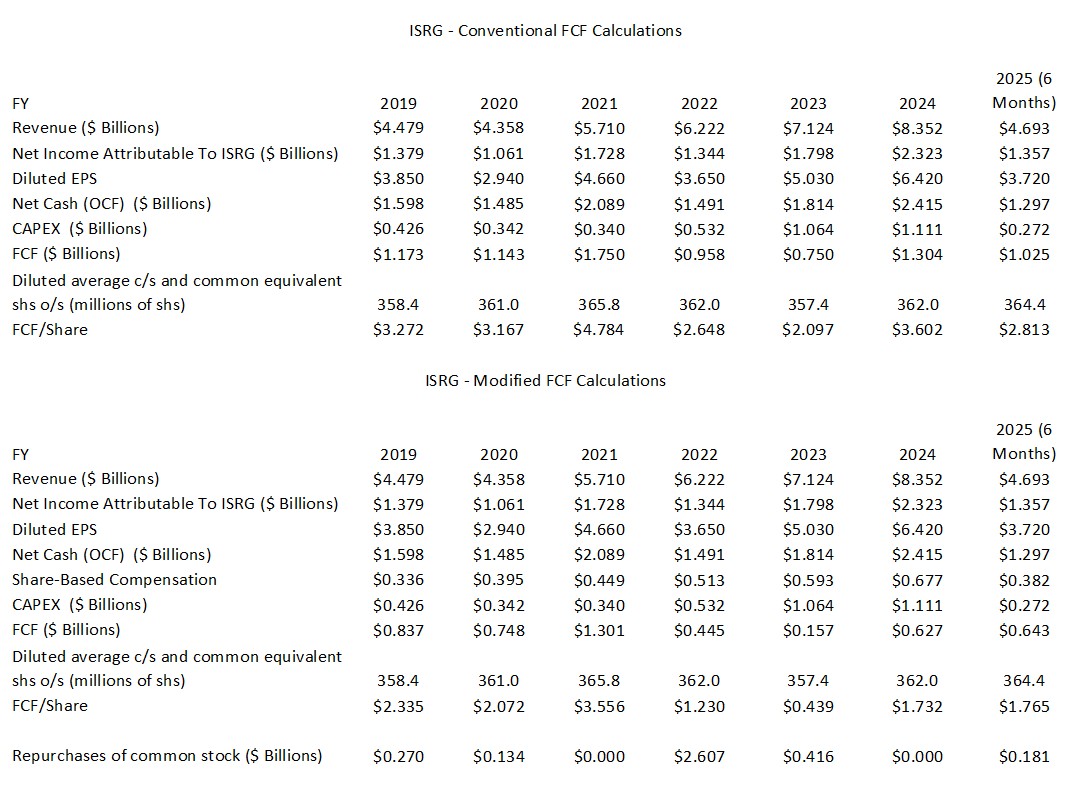

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2024 and YTD2025)

In my September 28, 2024 How Stock Based Compensation Distorts Free Cash Flow post, I touch upon how a company’s FCF can be distorted. In several subsequent posts, I take a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. They do not, however, deduct share-based compensation (SBC). Given the magnitude of ISRG’s SBC, I think it is prudent to deduct it.

FY2025 Outlook

On the Q1 2025 earnings call, management forecast FY2025 da Vinci procedure growth of 15% – 17%. This procedure growth guidance is now revised to 15.5% – 17%. The low end of the range assumes growth in China is impacted by trade, environmental and competitive dynamics.

Governments in key Outside the US markets continue to constrain hospital CAPEX budgets, which limits the expansion of capacity in the field. Bariatric procedures also continue to decline at rates similar to recent trends. The high end of the range assumes China procedure growth improves relative to 2024, the CAPEX environment improves in key Outside the US markets and bariatric procedure declines moderate.

The high end of the range also assumes that da Vinci procedures are not impacted by the current trade environment.

On the Q1 2025 earnings call, ISRG forecast FY2025 pro forma gross profit margin of 65% – 66.5% of revenue. This reflected significant incremental depreciation as ISRG brings on new facilities and the contribution from growth in newer products and the expected impact of tariffs. The current expectation is that the recently implemented tariffs will increase ISRG’s 2025 cost of sales by ~1% of revenue, plus or minus 20 bps. Given this, the estimate for pro forma gross margin is revised to 66% – 67% of revenue.

The expectation is for pro forma operating expense growth to be 10% – 14%, which includes increased depreciation from new facilities and investments to drive growth objectives.

There is no change to management’s $0.77B – $0.79B noncash stock compensation expense guidance.

Other income, comprised mostly of interest income, is likely to be ~$0.37B – $0.39B.

The CAPEX estimate is $0.65B – $0.725B. The prior estimate was ~$0.65B – $0.75B and the estimate before that was ~$0.65B – ~$0.8B. CAPEX is primarily for planned facility construction activities.

The 2025 pro forma income tax rate estimate remains at 22% – 23% of pretax income.

Risk Assessment

No rating agency rates ISRG because it has no debt.

The following commentary is provided on page 48 of 58 in the Q2 2025 Form 10-Q.

Our principal source of liquidity is cash provided by our operations, as well as the issuance of common stock through the exercise of stock options and our employee stock purchase plan. Cash and cash equivalents plus short- and long-term investments increased by $0.70 billion to $9.53 billion as of June 30, 2025, from $8.83 billion as of December 31, 2024, primarily as a result of cash provided by operating activities and proceeds from stock option exercises and employee stock purchases, partially offset by cash used for taxes paid related to net share settlements of equity awards, capital expenditures, and repurchases of common stock.

Our cash requirements depend on numerous factors, including market acceptance of our products, the resources we devote to developing and supporting our products, and other factors. We expect to continue to devote substantial resources to expand procedure adoption and acceptance of our products. We have made substantial investments in our commercial operations, product development activities, facilities, and intellectual property. Based on our business model, we anticipate that we will continue to be able to fund future growth through cash provided by our operations. We believe that our current cash, cash equivalents, and investment balances, together with income to be derived from our business, will be sufficient to meet our liquidity requirements for the foreseeable future. However, we may experience reduced cash flow from operations as a result of macroeconomic and geopolitical headwinds.

Dividends

ISRG does not distribute a dividend.

Share Repurchases

In FY2019, there were 358.4 million outstanding diluted shares. By Q2 2025, this had increased to 364.1 million.

ISRG’s Board has authorized an aggregate of $13.0B of funding for the common stock repurchase program since its establishment in March 2009. The most recent authorization occurred in May 2025, when the Board increased the authorized amount available under the Repurchase Program to $4.0B, including amounts remaining under previous authorization. As of June 30, 2025, the remaining amount of share repurchases authorized by the Board under the Repurchase Program was approximately $3.8B.

Valuation

As a growing business (Total Revenue of ~$2.385B in FY2015 versus ~$8.352B in FY2024 and ~$4.693B YTD2025) with no reliance on debt to fuel this growth, it is not surprising many investors view ISRG is an attractive investment. ISRG’s valuation, therefore, is never at ‘bargain basement’ levels.

Trying to value ISRG using GAAP and non-GAAP earnings or conventional and modified FCF leads to valuation levels in the stratosphere. Investors, therefore, need to assess the probability of ISRG being able to grow into the lofty valuations.

In my June 10, 2025 post, I disclose the purchase of additional shares @ ~$519.22. Using the current broker adjusted diluted EPS estimates at the time, ISRG’s forward-adjusted diluted PE levels were:

- FY2025 – 27 brokers – ~66.2 based on a mean of $7.84 and low/high of $7.59 – $8.23.

- FY2026 – 26 brokers – ~57.3 based on a mean of $9.06 and low/high of $8.49 – $9.80.

- FY2027 – 20 brokers – ~48.8 based on a mean of $10.63 and low/high of $9.46- $11.87.

- FY2028 – 7 brokers – ~43.1 based on a mean of $12.05 and low/high of $11.12 – $13.96.

In my July 17, 2025 post, I disclose the following purchases:

- 50 Intuitive Surgical (ISRG) shares purchased @ ~$511.18 on July 11

- 50 Intuitive Surgical (ISRG) shares purchased @ ~$508.98 on July 16

On July 23, I acquired another 50 shares @ $499.935.

ISRG has generated YTD2025 diluted EPS of $3.72 and $4.00 of adjusted diluted EPS. Despite the headwinds management presented on the Q2 2025 earnings call, there is a good probability that FY2025 diluted EPS and adjusted diluted EPS could be ~$7.45 and ~$8.00. The diluted PE and adjusted diluted PE using my recent purchase price are ~67.1 and ~62.5.

Using my recent $499.935 purchase price and the current broker estimates, ISRG’s forward-adjusted diluted PE levels are:

- FY2025 – 28 brokers – ~61.7 based on a mean of $8.10 and low/high of $7.75 – $8.31.

- FY2026 – 28 brokers – ~54.2 based on a mean of $9.23 and low/high of $8.70 – $9.80.

- FY2027 – 20 brokers – ~46.5 based on a mean of $10.75 and low/high of $10.00 – $11.87.

- FY2028 – 7 brokers – ~41.1 based on a mean of $12.16 and low/high of $11.31 – $13.96.

Although I look at brokers’ earnings estimates, I am extremely reluctant to place any reliance on them. My reasoning for excluding estimates beyond the current fiscal year is that I have no idea how anybody, especially in the current environment, can determine how a company will perform over the next few years. The variance in the brokers’ earnings estimates clearly indicates there is no consensus on how ISRG is likely to perform going forward.

Looking at ISRG’s valuation from a P/FCF perspective, there is a considerable variance in FCF when we use the conventional and modified methods (see table above). This is because ISRG issues significant SBC.

If we assume that ISRG can generate a similar amount of FCF/share in the second half of FY2025 as in the first half, we arrive at ~$5.626 and ~$3.53 of FCF/share. Both are well below my estimates of ~$7.45 in diluted EPS and ~$8.00 adjusted diluted EPS. ISRG’s valuation from a FCF perspective is ~88.9 and ~141.6.

Final Thoughts

I do not dispute that ISRG is richly valued. Sometimes, however, we have to pay up for quality.

Competition is increasing and hospitals are becoming increasingly financially constrained. I, however, expect ISRG will remain at the forefront of a large and growing addressable market. Fortunately, ISRG has the financial wherewithal to assist its customers in the financing their purchases.

ISRG has a dominant industry position and continues to grow. Its annual revenue in FY2015 was $2.38B. I envision FY2025 revenue of ~$9.5B. Even if the top line ‘only’ increases revenue to ~$15.5B by 2035, the company should be considerably more valuable. If my assumption is correct, acquiring ISRG shares @ ~$500 will no longer seem ridiculous.

Typically, we would expect an aggressively expanding company to rely on debt to some extent. ISRG, however, has no debt and it has ~$9.5B in cash and investments.

In my June 10, 2025 post, I disclose my June 9 purchase of an additional 50 shares @ $519.22 thus increasing my average cost from $279.49 to $303.48. Following that purchase, my exposure, excluding shares held by a young investor I am helping on their journey to financial freedom, stood at 500 shares in one of the ‘Core’ accounts within the FFJ Portfolio. ISRG was still my 7th largest holding when I completed my 2025 Mid-Year Portfolio Review.

As noted earlier, I have acquired an additional 150 shares in July bringing my exposure to 650 shares at an average cost of ~$350.42. For the moment, I am satisfied with my ISRG exposure. Unless the company suddenly implodes, I am not averse to increasing my exposure if the company’s valuation improves.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ISRG.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.