![]()

Intact Financial Corporation (IFC), a high quality Canadian based P&C insurance company, released Q3 2020 results on November 4th.

On November 9th it disclosed that it and Tryg A/S had formed a consortium for the purpose of making an offer to acquire RSA Insurance Group plc.

I view IFC shares as being reasonably valued based on its long-term growth and profitability prospects and have just acquired additional shares.

Summary

- IFC, one of Canada’s largest P&C insurance companies with a ~17% market share, together with Tryg A/S has just recently approached RSA Insurance Group plc with a possible cash offer which values RSA at US$9.3B.

- Growth opportunities in Canada are limited and the current proposal to acquire RSA provides IFC with an opportunity to creates a leading global specialty lines platform and provides an attractive entry into UK & Ireland at scale.

- IFC’s debt to total capital ratio currently sits at 21.2%. This level will rise following the acquisition of RSA but senior management expects to meet its self imposed 20% target debt-to-total capital ratio within 36 months.

- I currently view IFC as being reasonably valued and have acquired additional shares in one of the Core Accounts within the FFJ Portfolio.

Introduction

I initiated a position in Intact Financial Corporation (IFC) in mid-January 2007. Over the years I have reinvested the quarterly dividends and have periodically acquired additional shares.

Having been an investor in IFC for just under a decade and a half, I have benefited from several previously successful acquisitions.

Source: IFC – Strengthening Our Position as a World-Class P&C Insurer – November 9, 2020 Presentation

I am impressed with the company’s growth strategy and its ability to generate reasonable investor returns. I have, therefore, helped our daughter and her boyfriend accumulate shares in IFC and have disclosed same in this article and this article.

Following the November 4th release of Q3 results it was announced on November 5th that IFC and Tryg A/S had approached RSA Insurance Group plc (RSA) about a possible offer; RSA offers a range of general and specialty insurance products and has long been viewed as a possible takeover target.

While there are no assurances this transaction will be completed, I think the probability is likely that it will. I like the opportunities this acquisition brings to IFC and acquired 200 additional shares for one of the Core accounts within the FFJ Portfolio.

Let’s have a quick look at Q3 2020 results and the details of the proposed acquisition.

Financial Results

IFC’s recently released Q3 2020 results can be accessed here.

Comparing Q3’s overall combined ratio of 87.1% relative to historical levels, we see an improvement across both personal lines and commercial lines.

NOTE: The combined ratio is calculated by summing the incurred losses and expenses and dividing the sum by the total earned premiums. It measures the money flowing out of an insurance company in the form of dividends, expenses, and losses. Losses indicate the insurer’s discipline in underwriting policies.

Operating income in Q3 has also shown a steady improvement over the last few years.

Source: IFC – Q3 2020 Review of Performance – November 4, 2020

We can also see from page 14 of the Q3 2020 Review of Performance that IFC has been slowly improving its debt to total capital ratio and at 21.2% it is within striking distance of its self imposed 20% target debt-to-total capital ratio.

Proposed Acquisition of RSA Insurance Group plc

Details of the US$9.3B takeover proposal from IFC and and Danish insurer Tryg A/S can be accessed through the Possible Offer for RSA Insurance Group plc portal. While IFC has completed several acquisitions over the years, the RSA acquisition would its largest.

The proposed offer represents a 49% premium to RSA’s November 4th closing price.

Following the disclosure of this proposed offer, RSA indicated it is in talks with the consortium and has indicated it would likely recommend the potential offer.

The proposal is subject to due diligence, and there is no certainty it will lead to a formal bid. If the deal closes, however, IFC would keep RSA’s Canadian business as well as its U.K. and international division. Tryg plans to keep RSA’s operations in Sweden and Norway, while RSA’s Denmark business would be jointly owned by IFC and Tryg.

IFC’s debt to total capital ratio is expected to rise from the 21.2% level as at the end of Q3 but senior management expects to meet its self imposed 20% target debt-to-total capital ratio within 36 months.

Credit Ratings

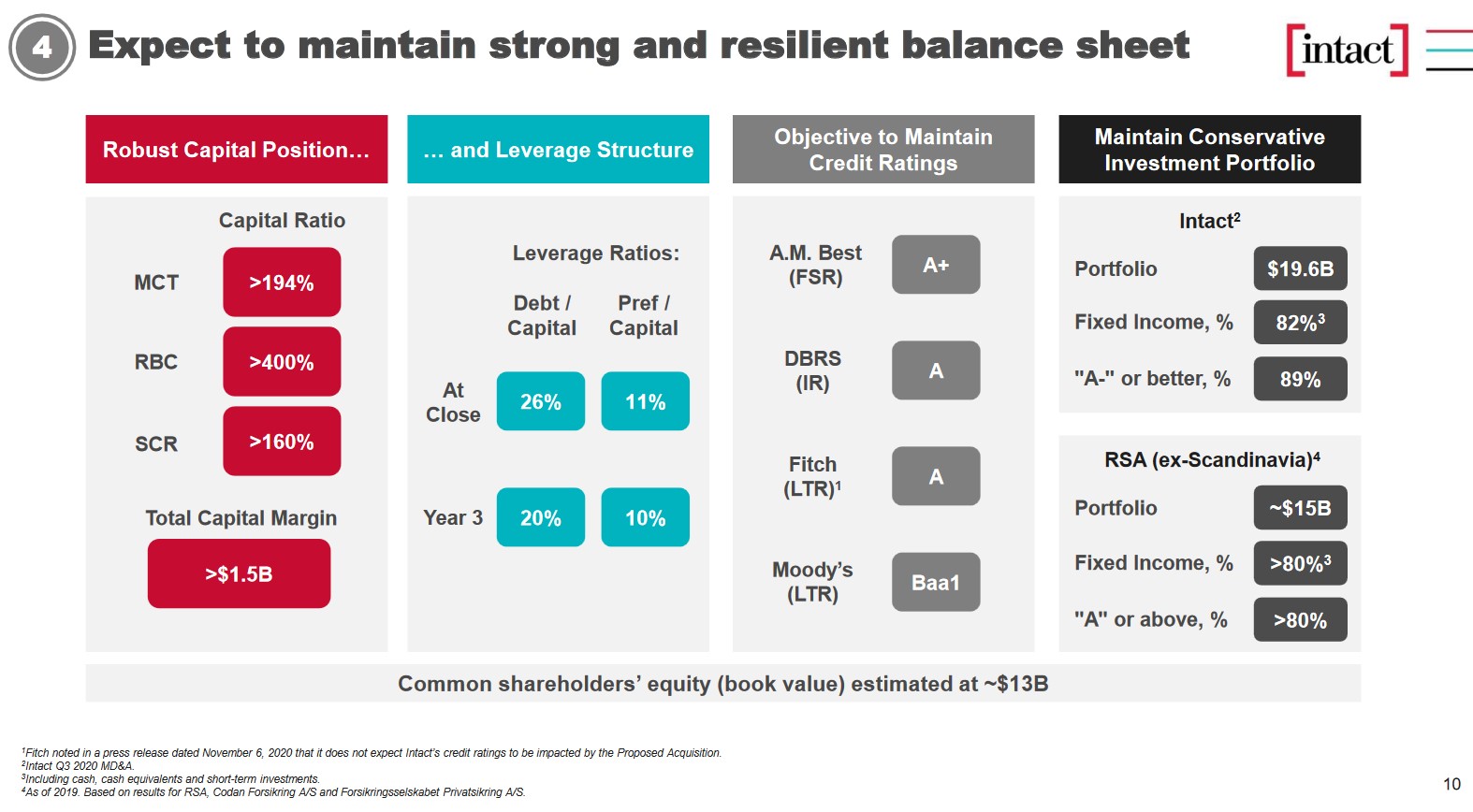

When I see a sizable potential acquisition, what immediately comes to mind is the impact this will have on the acquirer’s credit risk. Looking at the investor presentation which accompanies the proposed acquisition announcement I see that IFC expects to continue to maintain a strong and resilient balance sheet.

Source: IFC – Strengthening Our Position as a World-Class P&C Insurer – November 9, 2020 Presentation

Source: IFC – Strengthening Our Position as a World-Class P&C Insurer – November 9, 2020 Presentation

IFC’s current credit ratings can be found here. Looking at the Senior Unsecured Debt Ratings found on the company’s website and the ratings reflected in the November 9th presentation, we see the following (variances are in bold):

A.M. Best: Website: A- Presentation: A+

DBRS: Website: A Presentation: A

Fitch: Website: A- Presentation: A

Moody’s: Website: Baa1 Presentation: Baa1

Despite the variations reflected above, I continue to be satisfied with IFC’s credit quality. I am also encourage that IFC expects to return its debt-to-capital ratio to 20% within 36 months.

Dividend and Dividend Yield

IFC’s dividend history can be found here.

On December 31st, IFC will distribute its 4th consecutive $0.83 quarterly dividend; the company’s dividend history page is currently incorrect as it has neglected to reflect the $0.83 dividend issued at the end of September 2020.

Looking at IFC’s historical dividend track record it is not unreasonable to expect a $0.06/share/quarter dividend increase to be announced in early 2021 and to take effect with the March 2021 dividend payment. I view this dividend increase as realistic in that it represents a ~7.2% increase from the current $0.83/share/quarter. If you look at page 16 of IFC’s Q3 – Building A Resilient Future – November 5, 2020 presentation and page 14 of IFC’s – Q3 2020 Review of Performance – November 4, 2020 presentation we see a 15 year compound annual growth rate of 11%. On this basis, I think a $0.89/share/quarter projected dividend in 2021 is conservative.

On the basis of $0.89/share/quarter I can expect a dividend yield of ~2.60% calculated as follows: (($0.83 + (3 x $0.89))/$135.62) with $135.62 being my November 11th purchase price.

Valuation

As at the end of Q3 2020 IFC has generated $4.65 in YTD EPS. Based on my analysis I think it is reasonable to expect IFC to generate another ~$1.50 – ~$1.55 in EPS in Q4. Using the lower end of this range I get a FY2020 EPS projection of ~$6.15.

Using my $135.62 purchase price I end up with a PE of ~22. From my perspective, shares appear to be reasonably valued. Should Mr. Market decide that IFC’s share price needs to drop further (shares were trading at ~$148 in early November) I would be consider acquiring additional shares…assuming no catastrophic event permanently negatively impacts the financial strength of the company.

Final Thoughts

I continue to view IFC as a high quality insurance company with attractive long-term prospects and am optimistic the RSA acquisition will be approved by the majority of RSA’s shareholders and the various authorities which must provide approvals.

In the unlikely event the RSA acquisition falls through I remain confident that IFC can continue to add shareholder value over the long-term.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long IFC.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.