I will not touch TransDigm Group (TDG) despite it having been an immensely rewarding investment since going public in 2006. Not only is its lofty valuation an area of concern, its liberal use of debt is well beyond my risk tolerance.

On occasion, I will invest in a company whose leverage is elevated because it has recently made a major acquisition (eg. Nasdaq (NDAQ) and S&P Global (SPGI)). I do so, however, when management is committed to deleveraging within a reasonable time frame. TDG makes no such commitment and its modus operandi entails the liberal use of debt.

Business Overview

I see many similarities between TDG and HEICO Corporation (HEI and HEI-a) – I currently have HEI-a exposure.

Much like HEI, TDG is highly decentralized and has numerous business units. Both companies encourage business unit leaders to think like business owners (set aggressive targets for managers and allow them to achieve these goals however they choose).

Their respective strategy entails the acquisition of businesses that supply proprietary and highly engineered aircraft components with high aftermarket content; the businesses under the TDG umbrella manufacture and sell replacement parts for aircraft (eg. actuators, flight controls, ignition systems, pumps, cabin equipment, etc.).

Management estimates that ~90% of its FY2023 net sales were generated by proprietary products for which it has significant pricing power because it is the only provider of many such products.

TDG’s strategy has worked to date because of high barriers to entry. Any potential competitor must be licensed by the Federal Aviation Administration (FAA) and their products must be identical to the original product. This poses a challenge since TDG’s designs are proprietary and because the parts it produces generally cost very little relative to the value of the overall aircraft. Given this, competitors do not bother trying to replicate them.

The company follows a consistent long-term strategy in which it:

- owns and operates proprietary aerospace businesses with significant aftermarket content;

- utilizes a simple, well-proven, value-based operating methodology;

- has a decentralized organizational structure and a unique compensation system closely aligned with shareholders; and

- acquires businesses that fit this strategy and where there is a clear path to private equity-like returns.

Part 1 Item 1 – Business in the FY2023 Form 10-K/Annual Report provides a good overview of the company.

Financials

Q2 and YTD2025 Results

The Q2 2024 Form 10-Q is accessible through the SEC Filings section of TDG’s website.

TDG’s Q2 results exceeded expectations thus leading to an upwards revision to the FY2024 guidance.

Commercial aerospace market trends remain favorable as the industry continues to recover and progress towards normalization. Global air traffic has surpassed pre-pandemic levels and demand for travel remains robust.

Airline demand for new aircraft also remains high, and the OEMs are working to increase aircraft production. OEM aircraft production rates, however, remain well below pre-pandemic levels which continue to adversely impact TDG’s results relative to pre-pandemic production levels.

During the quarter, TDG saw a healthy growth in revenues and bookings for all 3 of its major market channels: commercial OEM, commercial aftermarket and defense. Revenues and bookings also sequentially improved in all 3 of these market channels.

It ended the quarter with ~$4.3B of cash; this includes $2B of cash from new debt issued during Q1 2024 of which ~$1.4B is reserved for the anticipated closing of the acquisition of CPI’s electron device business.

Management expects significant additional cash generation throughout the remainder of FY2024.

Capital Allocation and Priorities

Management states that the capital structure and capital allocation are a key part of the value-creation methodology. If TDG has excess cash, it generally prioritizes allocating the excess cash in the following manner:

- capital spending at existing businesses;

- acquisitions of businesses;

- payment of a special dividend and/or repurchases of common stock; and

- prepayment of indebtedness or repurchase of debt.

On the Q2 earnings call, management stated that ‘the option of paying down debt seems unlikely at this time’.

TDG continues to actively seek small and midsize M&A opportunities that fit its model and is expanding its pipeline of potential M&A targets; it is expanding its M&A team to address these opportunities.

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

In FY2014 – FY2023, TDG generated OCF of (in millions of $) 541, 521, 683, 789, 1,022, 1,015, 1,213, 913, 948, and 1,375. TDG generated ~$230 million of operating cash flow in Q2 and by the end of Q2 2024, it generated ~865 versus ~507 at the end of Q2 2023.

In FY2014 – FY2023, TDG generated FCF of (in millions of $) 507, 466, 639, 718, 949, 913, 1,108, 808, 829, and 1,236. At the end of Q2 2024, it generated ~781 versus ~441 at the end of Q2 2023.

In FY2014 – FY2023, TDG’s annual CAPEX was (in millions of $) 34, 55, 44, 71, 73, 102, 105, 105, 119 and 139. At the end of Q2 2024, CAPEX amounted to ~84 versus ~66 at the end of Q2 2023.

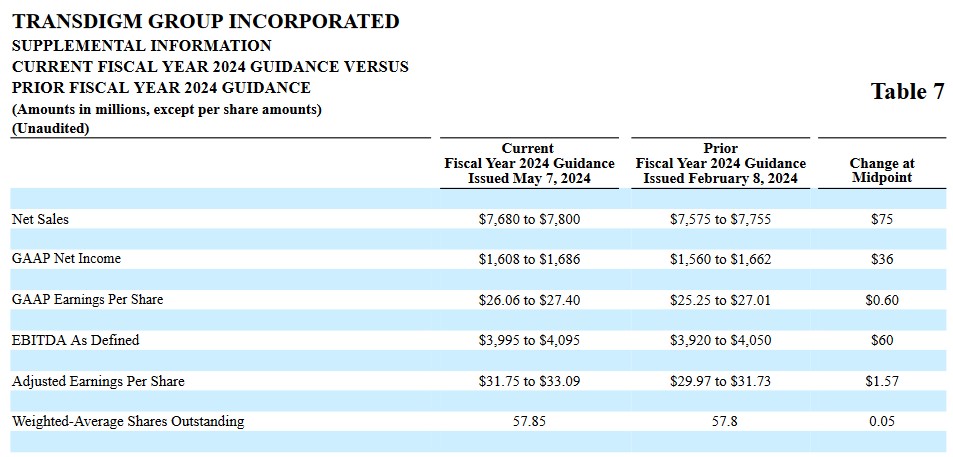

FY2024 Outlook

The following reflects TDG’s current and prior outlook.

This guidance uses the following assumptions and assumes no additional acquisitions or divestitures. In addition, it is based on current expectations for continued performance in TDG’s primary commercial end markets throughout FY2024.

Management excludes CPI’s Electronic Device business from current guidance until the acquisition closes.

Management continues to expect to generate free cash flow of ~$2B in FY2024 which is a considerable increase from $1.236B in FY2023.

Risk Assessment

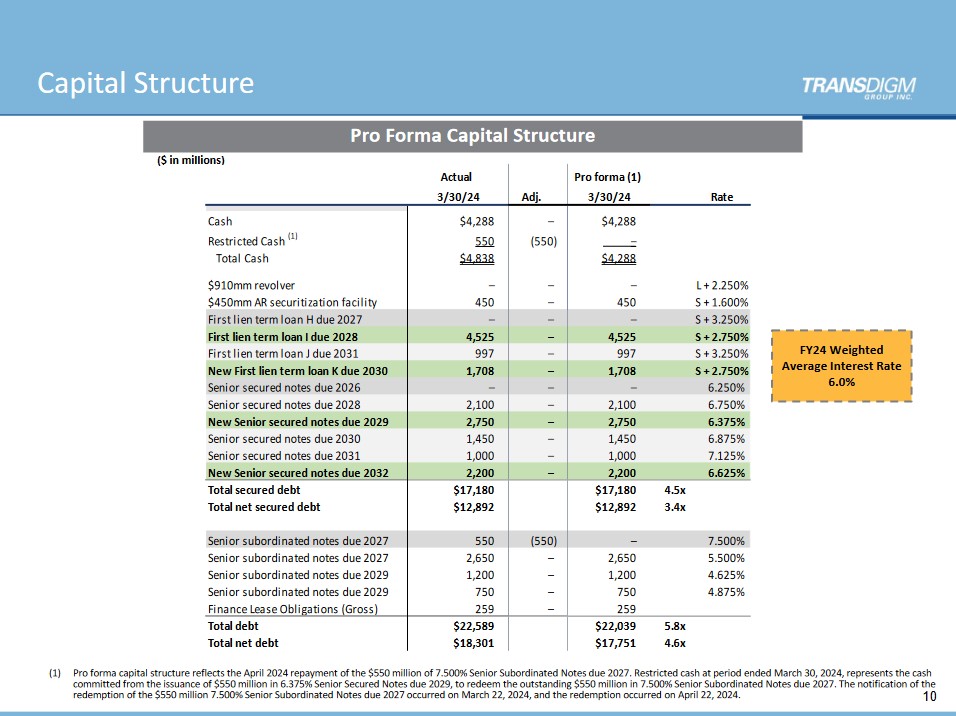

On the Q2 earnings call, management stated that it continues to be comfortable operating in the 5 – 7 net debt-EBITDA ratio range.

In addition, the EBITDA to interest expense coverage ratio at the end of Q2 was 3.4x versus a 2 – 3x target range.

In Q2, TDG completed a few financing objectives of which one was to push out the nearest term maturity date by 2 fiscal years to FY2028.

We see that TDG operates with a high degree of financial leverage to amplify its operating results. This high degree of leverage is reflected in its less than stellar credit ratings.

On February 12, 2024, Moody’s issued the following:

Moody’s Investors Service (“Moody’s”) assigned Ba3 ratings to TransDigm, Inc.’s (“TransDigm”) new backed senior secured first lien revolving credit facility due 2029. Moody’s also assigned Ba3 ratings to TransDigm’s new backed senior secured notes due 2029 and 2032. All other ratings, including the B1 Corporate Family Rating (“CFR”), B1-PD Probability of Default Rating (“PDR”), SGL-1 Speculative Grade Liquidity Rating (“SGL”), Ba3 backed senior secured bank credit facility ratings, Ba3 backed senior secured notes ratings and B3 backed senior subordinate notes ratings are unchanged. The outlook remains unchanged.

Proceeds from the new notes will be used to refinance TransDigm’s existing senior secured notes due 2026. The new $810 million revolving credit facility will replace the existing revolving credit facility of the same size that expires in 2026.

On February 12, 2024, S&P Global issued the following:

S&P Global Ratings today assigned its ‘B+’ issue level rating and ‘3’ recovery rating to TransDigm Inc.’s proposed new $2.2 billion senior secured notes due 2029, $2.2 billion senior secured notes due 2032, and new $810 million revolving credit facility due 2029. The ‘3’ recovery rating indicates our expectation of meaningful (50%-70%; rounded estimate: 50%) recovery in the event of a hypothetical default situation.

The company will use proceeds from the transaction to refinancing the existing $4,400 million of 6.25% senior secured notes and its existing $810 million revolver both due 2026. The issuer credit rating remains ‘B+’. We note that the transaction is largely leverage-neutral. However, the refinance plan will address TransDigm’ s nearest maturities. We expect the company’s S&P Global adjusted debt to EBITDA to measure between 6.0x and 6.3x for fiscal 2024. Following the transaction, the closest material maturity is not until 2027, when its $1.708 billion first lien term loan H and $3.2 billion in subordinated notes come due.

The B1 and B+ Corporate Family Rating is the top tier of the highly speculative non-investment grade category. These ratings define TDG as being more vulnerable than the obligors rated ‘BB’, however, the obligor currently has the capacity to meet its financial commitments. Adverse business, financial, or economic conditions will likely impair the obligor’s capacity or willingness to meet its financial commitments.

At this stage of my life, I deem this level of risk to be unacceptable.

Dividends and Share Repurchases

Dividend and Dividend Yield

TDG does not distribute a dividend.

Share Repurchases

TDG’s weighted average shares outstanding in FY2014 – FY2023 are (in millions of shares) 57, 57, 56, 56, 56, 56, 57, 58, 58, and 57. A similar number were outstanding in Q1 2024.

On January 27, 2022, TDG’s Board authorized a new stock repurchase program with no expiration date to permit repurchases of its outstanding common stock not to exceed $2.2B. This new repruchase program replaced the $0.65B stock repurchase program previously authorized by the Board on November 8, 2017.

No repurchases were made under the program in FY2023 and in the twenty-six week period ended March 30, 2024. As of March 30, 2024, $1.288B remained available for repurchase under the $2.2B stock repurchase program.

Valuation

We can not determine TDG’s valuation on a PE basis since it has a shareholder’s deficit.

Should TDG be of interest to you, you will need to perform a discounted cash flow analysis using metrics you think would be acceptable to compensate you for the level of risk TDG presents.

The current share price is ~$1339 and the midpoint of management’s FY2024 adjusted diluted EPS guidance is $32.42. On this basis, the forward adjusted diluted PE is ~41.3.

The PE levels using the current adjusted diluted EPS broker estimates are:

- FY2024 – 23 brokers – ~40.6 using a mean of $32.97 and low/high of $31.86 – $34.50.

- FY2025 – 23 brokers – ~34.71 using a mean of $38.58 and low/high of $35.78 – $41.50.

- FY2026 – 13 brokers – ~30.2 using a mean of $44.33 and low/high of $37.24 – $48.06.

Earnings can easily be distorted, and therefore, I like to gauge a company’s valuation based on FCF.

Management’s FY2024 outlook calls for ~57.85 million weighted average diluted shares outstanding and ~$2B of FCF. This works out to ~$34.6/share. Divide $1339 by 34.6 and we get a P/FCF value of ~39.

While TDG might be a wide moat company, I am not prepared to acquire shares at this valuation considering the credit risk is so high.

Final Thoughts

I do not dispute that TDG has rewarded shareholders. I will not touch TransDigm Group, however, and view HEI to be a more prudent long-term investment given my risk tolerance.

TDG’s and HEI’s total rate of return was very similar over the past decade. Recently, however, TDG’s share price appreciation has considerably outpaced that of HEI. I attribute this surge in TDG’s share price to ‘irrational exuberance’.

The valuation of both companies appear to be at least 20% above fair valuation. Although I will ‘pay up’ for a high quality business with a wide moat that is experiencing steady growth, I can not fathom investing in a company whose debt is deep in ‘junk’ territory.

I am not implying that TDG will be unable to meet its obligations. When a company is so highly leveraged, however, it becomes vulnerable.

HEI, on the other hand, is far more prudent when it comes to the use of leverage. This gives it greater flexibility.

At least with HEI, its Baa2 long-term issuer credit rating assigned by Moody’s is investment grade.

TDG’s B1 Corporate Family Credit Rating is 5 tiers below that of HEI and is 4 tiers below the lowest investment grade ratings. In essence, TDG’s rating is ‘junk’.

I am at the stage of my life where I am unwilling to assume this degree of risk; there are several high quality companies in which I can invest that are likely to provide double digit total investment returns without taking on this level of risk.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I have no exposure to TDG and have no intention of initiating a position. I am long HEI-a.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.