On December 5, 1996, Federal Reserve Chairman Alan Greenspan made his famous speech wherein he asked if “Irrational Exuberance” had begun to play a role in the increase of certain asset prices. Looking at Netflix’s current stock valuation I spell Irrational Exuberance: NETFLIX.

Here is a the key quote from Greenspan:

“Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?”

A little more than three years after his famous speech, the NASDAQ topped out.

NASDAQ Chart

While Greenspan mentioned the phrase in 1996, it was Yale professor Robert Shiller, who published the book “Irrational Exuberance” in 2000, who made the phrase infamous when he predicted the collapse of the dot-com bubble.

In the July 2014 Board of Governors of the Federal Reserve System Monetary Policy Report, Federal Reserve chair Janet Yellen mentioned twice that “Equity valuations of smaller firms as well as social media and biotechnology firms appear to be stretched, with ratios of prices to forward earnings remaining high relative to historical norms.” This sounds very much like what Alan Greenspan said three years before the bursting of the dot-com bubble. It would certainly be ironic if in the second half of 2017 we witnessed a similar implosion.

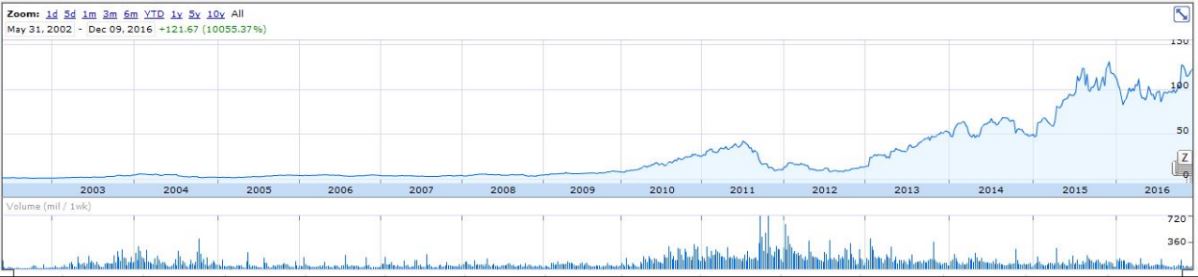

I bring this to your attention because I was just reviewing the daily average trading activity for Netflix, Inc. (NASDAQ: NFLX). I certainly was not reviewing it as a potential investment but rather to ascertain to what extent speculators are exchanging shares of this company.

Netflix Stock Chart

Here is a company that had revenue of $3.205 Billion in 2011, net income available to common shareholders of $226 Million, and Diluted EPS of $0.59/share. As per the December 31, 201510-K, NFLX had revenue of $6.78 Billion, net income available to common shareholders of $123 Million, and Diluted EPS of $0.28/share. For the 9 months ended September 30, 2016, Netflix generated had revenue of $6.353 Billion, net income available to common shareholders of $119.9 Million, and EPS of $0.27/share on a diluted basis.

As I compose this, NFLX has a stock price of $122.88. Let’s say they hit their projected annual EPS of $0.37/share, you get a P/E ratio in excess of 330:1. I call this “irrational exuberance”! Despite this ridiculous valuation level, 7.4 Million NFLX shares on average exchange hands every trading day.

There is just no fathomable way that a speculator buying NFLX shares today could conceivably expect to earn a reasonable rate of return on this investment unless the “greater fool theory” continues.

The space in which NFLX competes is becoming increasingly competitive. Just recently it announced that it will permit subscribers to download some content onto their phones and tablets. This is a reversal of NFLX’s policy, which just last year said it would not join Amazon (NASDAQ: AMZN) in providing this feature. While there may be various reasons for this change of heart, I am certain one of them is that NFLX knows its stock must somehow maintain its lofty heights. It has essentially been forced to act because domestic subscriber growth is slowing and it cannot risk continuing to lose viewers to another service.

NFLX, however, is restricted with its download offerings because only Netflix originals can be downloaded. The reason for this is that NFLX owns this content while owners of the content that is licensed do not want anyone downloading content.

Despite this additional potential avenue of growth, NFLX speculators should be worried because NFLX will need to offer this feature for free just to keep pace with the competition. In essence, investors should not expect any new revenue to be generated.

Given my concerns with valuation levels and the increasingly competitive landscape, I would suggest that you get out while you can if you are currently a NFLX shareholder. If you are not currently a NFLX shareholder, count yourself as fortunate.