Lately, I have been giving more thought to how stock-based compensation (SBC) distorts Free Cash Flow (FCF).

What If Employee Compensation Was 100% SBC?

I have no objection to the use of SBC to reward employees. My concern is when it goes overboard. As a shareholder, I want the weighted average number of diluted outstanding shares to decline…especially if the company does not distribute a dividend.

Let’s suppose a company decides to compensate its employees 100% via SBC. Under current GAAP rules, a company adds back 100% of its SBC in the Consolidated Statement of Cash Flows!

How does this impact our FCF calculations? Let’s look at a couple of companies.

The Impact of SBC on Free Cash Flow (FCF)

Amazon (AMZN)

In my August 5, 2024 I Am Not Initiating An Amazon Position post, I share the following:

The weighted average diluted shares outstanding in FY2014 was ~9.3B. In the 3 months ending on June 30, 2024, this has grown to ~10.708B. This increase is because AMZN’s stock based compensation far exceeds share repurchases.

AMZN repurchased ~$0.960B in FY2012, $0 in FY2013 – FY2021, $6B in FY2022, and $0 in FY2023 – YTD2024.

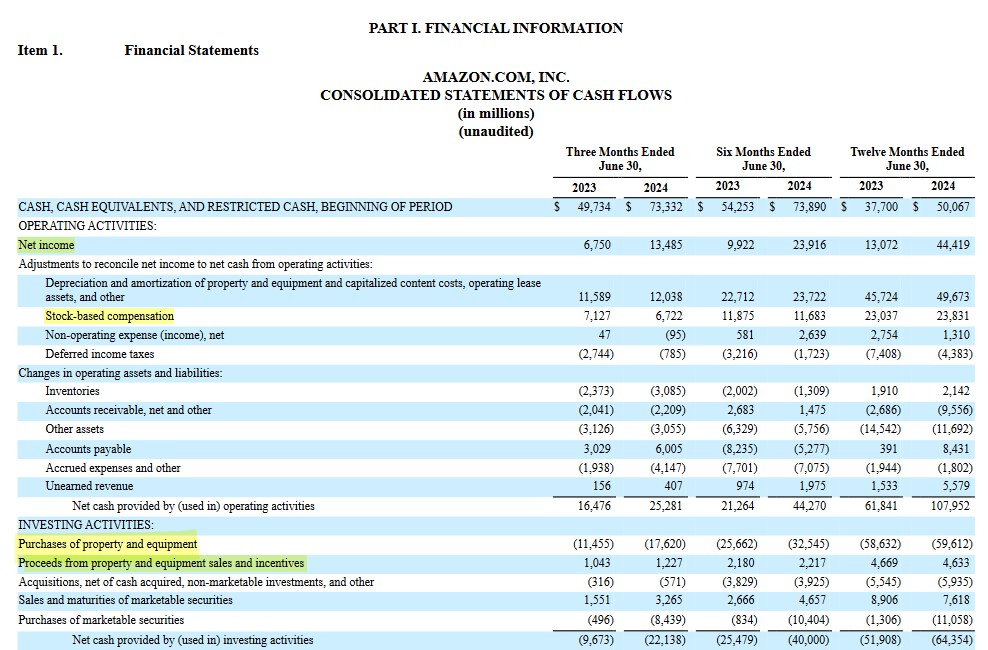

Looking at AMZN’s Consolidated Statements of Cash Flows, stock based compensation in FY2012 – FY2023 was (in $B): $0.833, $1.134, $1.497, $2.119, $2.975, $4.215, $5.418, $6.864, $9.208, $12.757, $19.621, and $24.023. In the first half of FY2024, stock-based compensation was $11.683B and no shares were repurchased.

I conclude with the following in my Final Thoughts:

We then need to consider AMZN’s capital allocation history and question whether anything will change. How can we make a decent investment return if no cash flow or earnings are being returned to shareholders? This company continues to issue a ‘boatload’ of shares annually under its various stock based compensation programs. How does this help the average investor?

In the 12 months ending June 30, 2024, AMZN generated ~$44.42B of Net Income. Adding back ~$23.83B of SBC and various other line items, we arrive at ~$108B of net cash provided by operating activities.

To determine FCF, we deduct ~$55B of Net CAPEX from ~$108B giving us ~$53B of FCF.

Were we to exclude SBC in our FCF calculation, net cash provided by operating activities would be ~$84.2B. Deduct ~$55B of Net CAPEX and FCF drops to ~$29.2B.

Zoom Video Communications (ZM)

I have a 900-share ZM position in one of the Core accounts within the FFJ Portfolio. Despite being a relatively insignificant holding, I question the extent to which ZM has been employing the use of SBC.

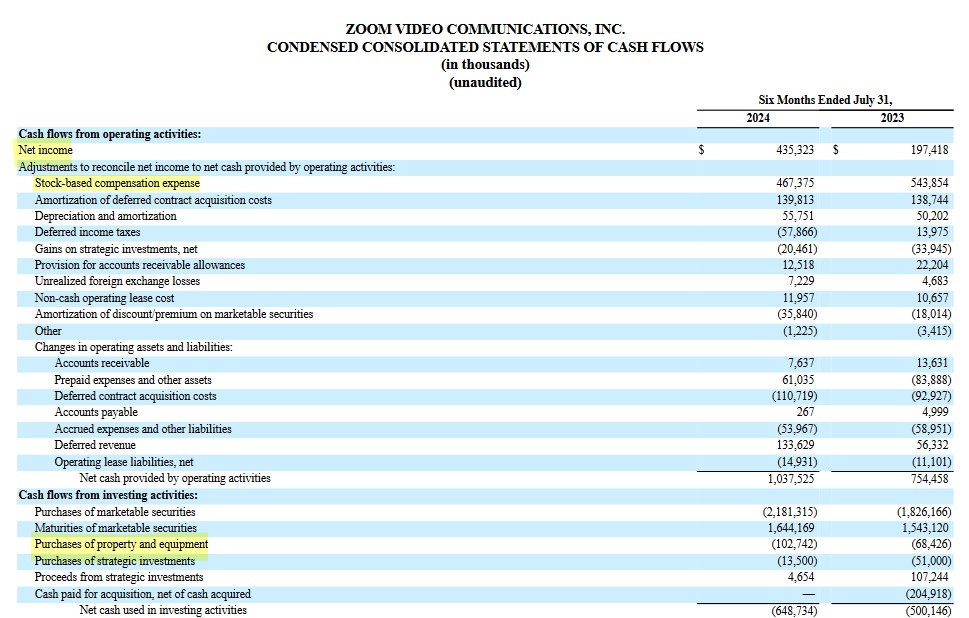

In the 6 months ending July 31, 2024, ZM generated ~$0.435B of Net Income. Adding back ~$0.467B of SBC and various other line items, we arrive at ~$1.038B of net cash provided by operating activities.

To determine FCF, we deduct ~$0.103B of CAPEX from ~$1.038B giving us ~$0.935B of FCF.

Were we to exclude SBC in our FCF calculation, net cash provided by operating activities would be ~$0.571B. Deduct ~$0.103B of CAPEX and FCF drops to ~$0.468B.

ZM’s Decision To Scale Back SBC

In FY2019, the weighted average number of diluted outstanding ZM shares was ~276.4 million. In Q2 2024, this had increased to ~314 million.

Growth of this magnitude is not sustainable. Fortunately, ZM’s senior management recognizes this.

ZM’s existing equity plans were instituted to balance a volatile pandemic stock price and now, changes are coming about.

Very recently, CEO Eric Yuan wrote a note to employees in which he stated that equity in ZM has been issued to workers at a rate that is ‘not sustainable’. Yuan goes on to say:

We grant a significant amount of shares each year which has led to very high dilution. Put simply, we are granting too much equity and must proactively reduce it.

ZM’s ‘annual performance equity plan’ is to be phased out over the next 2 fiscal years beginning in February 2025. Furthermore, the amount of equity granted to new hires is to be reduced. To partially compensate for these changes, some employees will receive higher cash bonuses.

It will be important to keep this in mind when comparing ZM’s future FCF relative to historical FCF levels.

Note: Salesforce Inc. (CRM) and Workday Inc. (WDAY) have already disclosed plans to limit their reliance on this common compensation technique in the tech industry.

Final Thoughts

Although SBC is a non-cash expense, it is a real expense. Its GAAP treatment, however, distorts the FCF calculation (a non-GAAP metric) thus impacting our valuation analysis.

In my opinion, SBC should be moved to the cash flow from financing activities section. My reasoning is that how a company decides to pay its employees (cash or equity) is a financing decision. By making this change, SBC would no longer come into play in determining a company’s FCF.

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ZM.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.