Home Depot (HD) is perennially overvalued. If you, therefore, decide to invest in the company the decision typically comes down to how much are you willing to ‘overpay’.

I last reviewed HD in this February 22, 2023 post. My conclusion was that shares were still overvalued despite the recent share price pullback.

At the time of that review, the most current financial information was for Q4 and FY2022. We now have Q2 and YTD2024 results thus prompting me to revisit this holding; HD’s fiscal year end is either the end of January or the beginning of February.

Overview

If you want a good overview of the company that includes the Risk Factors, Part 1 in the FY2023 Form 10-K is a good source of information.

SRS Acquisition

Visit SRS Distribution’s website to learn about the company.

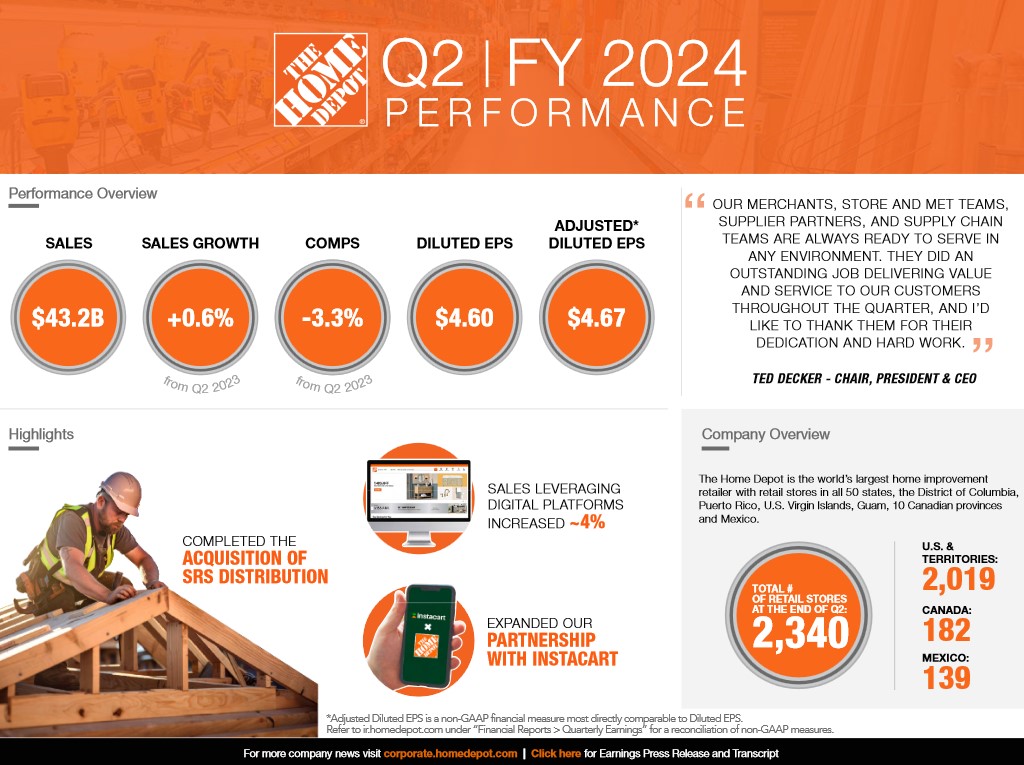

On March 28, 2024, HD announced its intent to acquire SRS Distribution, a leading residential specialty trade distribution company across several verticals serving the professional roofer, landscaper and pool contractor.

HD stated that the acquisition would increase its total addressable market to ~$1T, an increase of ~$50B.

On June 18, HD announced the completion of this acquisition.

In May 2024, HD increased its commercial paper program from $5.0B to $19.5B to aid in the financing of the ~$18.25B SRS acquisition. In connection with the increase in the commercial paper program, HD also entered into additional back-up credit facilities that consist of a 364-day $3.5B credit facility scheduled to expire in May 2025, a 3-year $1.0B credit facility scheduled to expire in May 2027, and a 364-day $10.0B credit facility scheduled to expire in May 2025.

The $10.0B credit facility also provides that the commitments and any borrowings under this facility will be reduced by the amount of net cash proceeds received from any future debt issuance. In the aggregate, HD’s commercial paper program allows for borrowings up to $19.5B.

Financials

Q2 and YTD2024 Results

Earnings-related material is accessible here.

HD’s Goodwill and Intangible Assets ballooned to ~$19.4B and ~$9.2B on July 28, 2024 from ~$8.5B and ~$3.6B at FYE2023 (January 28, 2024). This is primarily attributed to the SRS acquisition. Short-term debt and long-term debt increased ~$11.8B from January 28, 2024 levels.

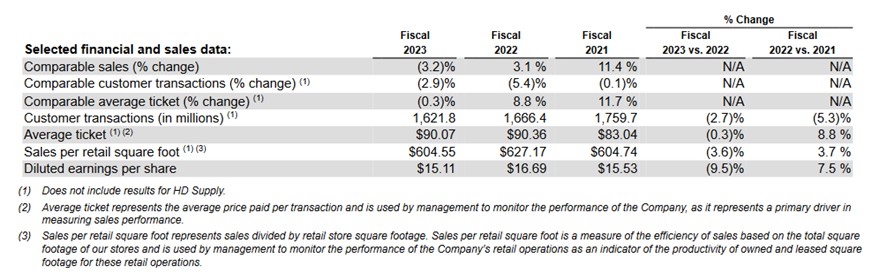

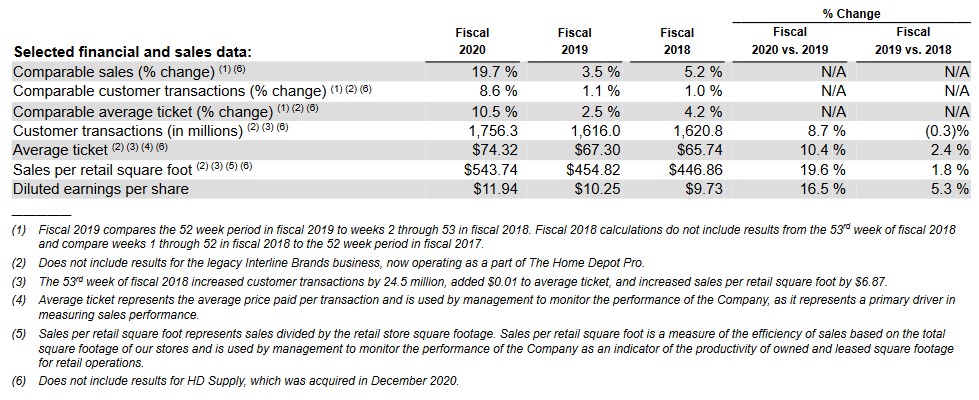

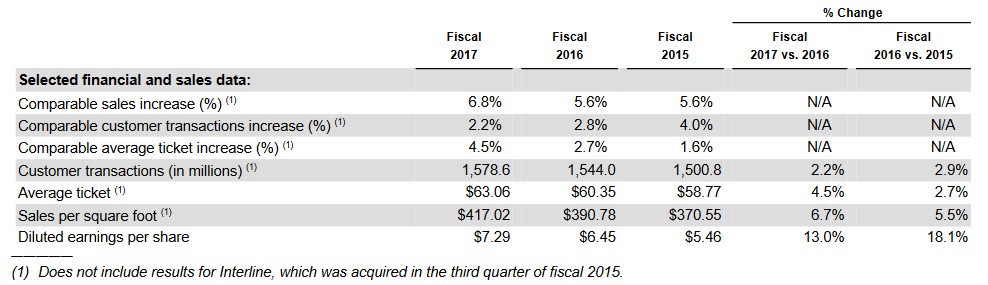

Looking at HD’s selected financial and sales data over the past few years and the first half of FY2023 and FY2024, we notice that the number of customer transactions is relatively stagnant between FY2018 and YTD2024. The average ticket size, however, surged after FY2019 which is not surprising given how the cost of just about everything has increased so much in recent years.

The sales per retail square foot has also been reasonably stagnant although there is a noticeable increase in this metric in Q2 2024 versus Q1 2024. We need to be cognizant, however, that HD’s customer base (DIY and contractors) is likely to be much more active with home renovations during May – July than in February – April.

On the Q2 earnings call, management stated:

During the quarter, higher interest rates and greater macroeconomic uncertainty pressured consumer demand more broadly, resulting in weaker spend across home improvement projects.

Additionally, we saw continued softness in spring projects, which were also impacted by the extreme weather changes throughout the quarter. When we look at the performance in the first 6 months of the year, as well as continued uncertainty around underlying consumer demand, we believe a more cautious sales outlook is warranted for the year.

In response to an analyst’s question about increased pressure on project-oriented purchases, HD’s management stated:

And so if you go back a bit to the environment that we’ve been working through this period of moderation, the first thing we saw was a shift in spending — PCE spending from goods back into services. And we’re effectively through that transition, the relative share spend is more or less equal to where it was before the pandemic. And then we had, some certainly some pull forward in our segment. I’d say we’re not completely through the pull forward, but largely. I mean we’re now going on 4 years from the first spring of the pandemic when people were buying lots of grills and patio furniture etc. We’re largely working our way through that. And then the higher interest rate started to impact the housing market in housing turnover in particular, which is down some 40%. And I think last quarter, last month, we saw numbers that on an annualized basis, we’re approaching 40-year lows. That’s also impacting customers’ interest in financing larger projects. Everyone’s expecting rates are going to fall.

So we’re deferring those projects. But again, what more recently has happened is a broader concern with the macro economy. There’s just a lot of noise with political and geopolitical environment, unemployment ticked up, inflation keeps eating away at disposable income. And I think people just took a pause as we progress through the quarter or more of a pause because of these macro uncertainties.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In FY2015 – FY2023 and the first half of FY2024, OCF, CAPEX, and FCF were:

- OCF was (in ~B$) 9.4, 9.8, 12.0, 13.2, 13.7, 18.8, 16.6, 14.6, 21.2, and 11.0.

- CAPEX was (in ~B$) 1.5, 1.6, 1.9, 2.4, 2.7, 2.5, 2.6, 3.1, 3.2, and 1.6.

- FCF was (in ~B$) 7.9, 8.2, 10.1, 10.8, 11.0, 16.3, 14.0, 11.5, 18.0 and 9.4.

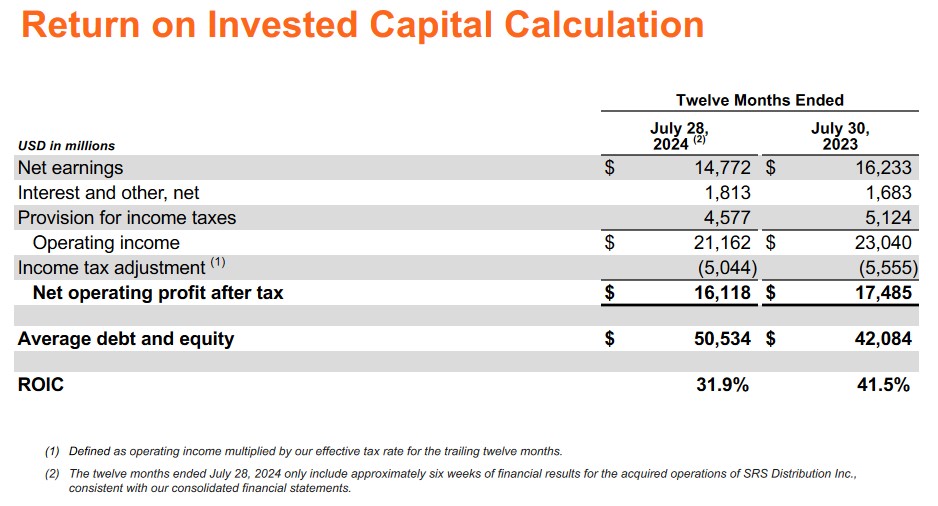

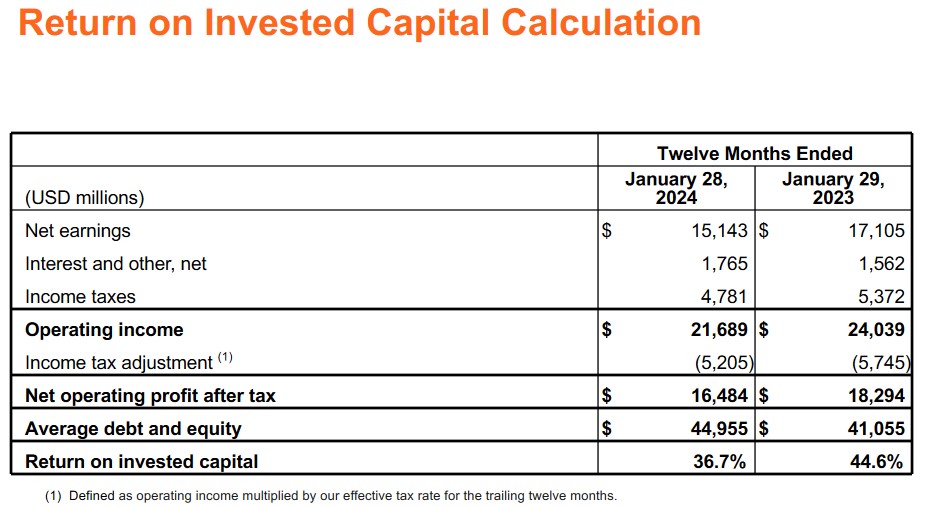

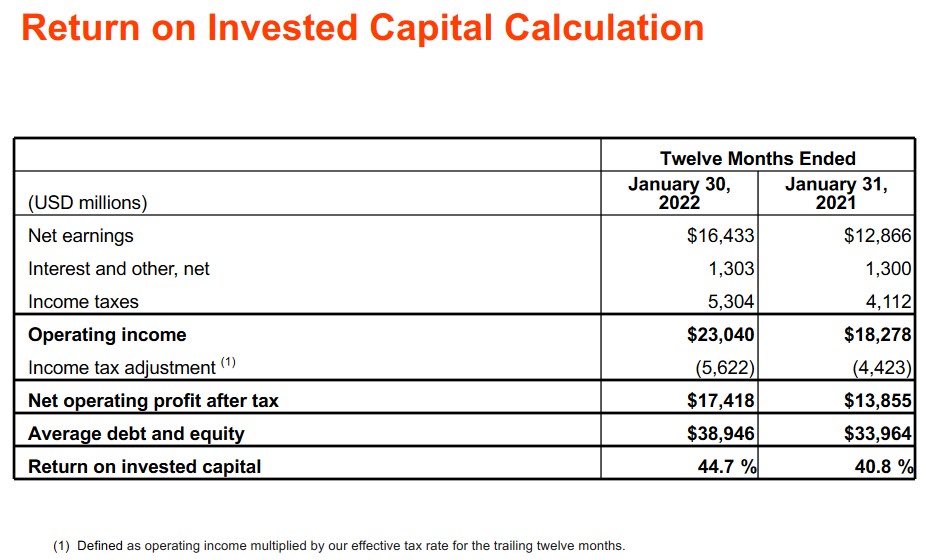

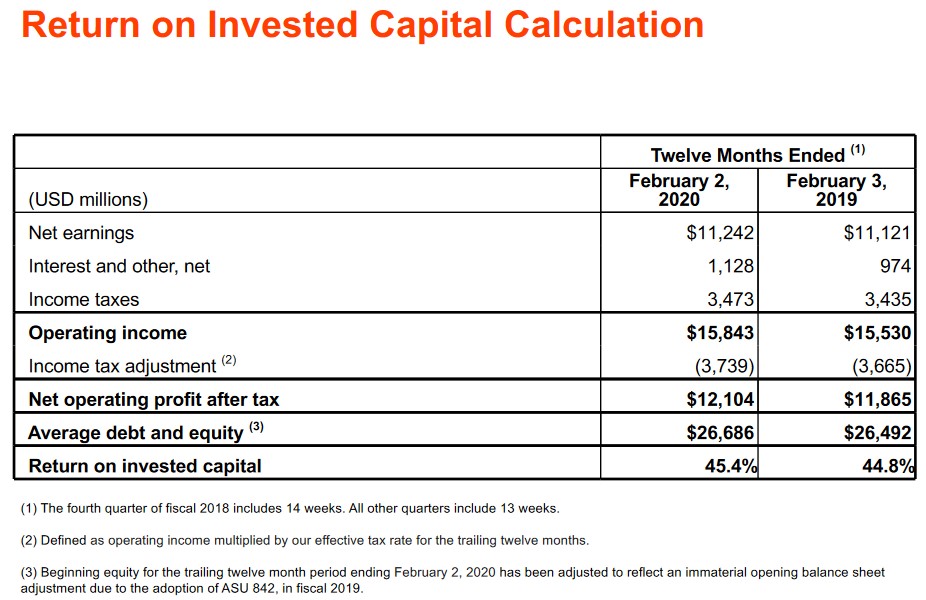

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level. HD’s ROIC in recent years consistently exceeds this level.

Capital Allocation

HD’s capital allocation principles are:

- reinvest in the business to drive growth faster than the market;

- pay a quarterly dividend after meeting the needs of the business; and

- return excess cash to shareholders through share repurchases after reinvesting in the business and paying a dividend.

Investors can expect CAPEX of ~2% of sales on an annual basis.

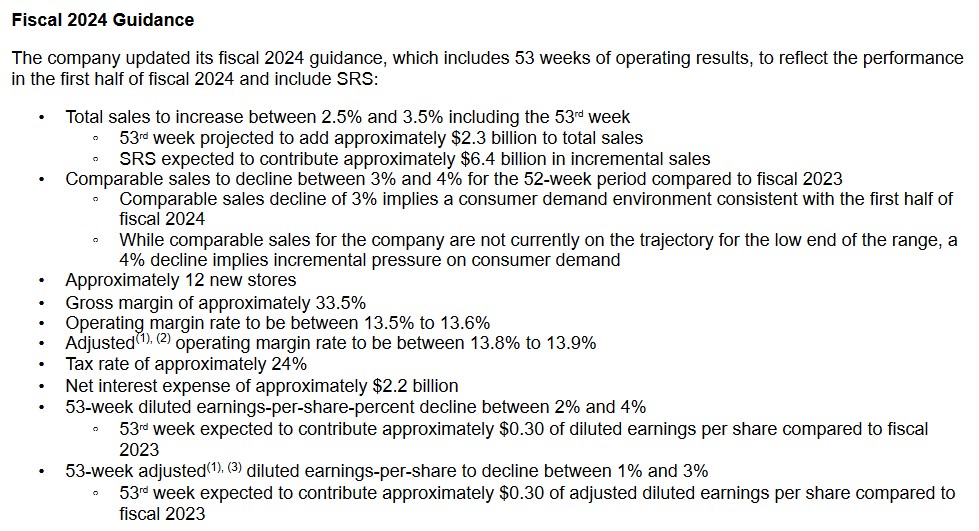

FY2024 Guidance

The following is HD’s most recent guidance.

On the Q2 earnings call, management states that higher interest rates and greater macroeconomic uncertainty is pressuring consumer demand more broadly. This is resulting in weaker spend across home improvement projects. Furthermore, spring projects were impacted by the extreme weather changes in Q2. When looking at the performance in the first half of the year and the continued uncertainty around underlying consumer demand, HD is adopting a more cautious sales outlook for the year.

NOTE: There were 52 weeks in FY2023 versus 53 weeks in FY2024.

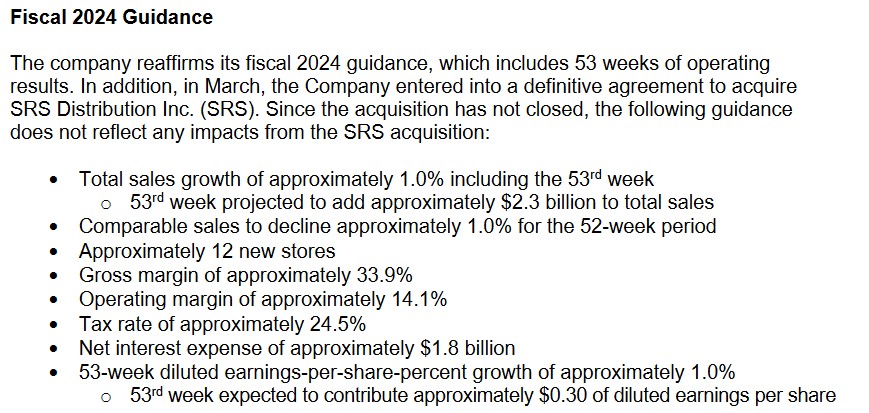

The following is HD’s guidance released with its Q1 2024 results.

Risk Assessment

There is no change to HD’s senior unsecured domestic currency credit ratings following my prior post. The ratings and outlook remain:

- Moody’s: A2 and stable – last reviewed March 28, 2024;

- S&P Global: A and stable – last reviewed March 28, 2024.

- Fitch: A and stable – last reviewed May 10, 2024.

These ratings are the middle tier of the upper-medium grade category. They define HD as having a STRONG capacity to meet its financial commitments. However, it is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

These investment-grade ratings are acceptable for my purposes.

Dividends and Share Repurchases

Dividend and Dividend Yield

HD’s dividend history is accessible here.

Share Repurchases

In FY2016 – FY2023, HD repurchased $6.88B, $8B, $9.963B, $6.965B, $0.791B, $14.809B, $6.696B, and $7.951B of issued and outstanding shares for a total of ~$62.055B. The dramatic drop in the value of shares repurchased in FY2020 is because HD suspended share repurchases in March 2020 when COVID-19 hit North America. HD resumed share repurchases in Q1 2021.

The diluted weighted average common shares outstanding in FY2019 – FY2023 (in billions) are 1.097, 1.078, 1.058, 1.025, and 1.002.

In August 2023, HD’s Board approved a $15B share repurchase authorization. As of April 28, 2024, ~$11.7B of the $15B share repurchase authorization remained available. In March 2024, HD paused share repurchases as a result of the pending acquisition of SRS Distribution.

HD is currently at a 2.6x debt-to-EBITDA ratio. The focus is to reduce this to ~2.0x before the resumption of repurchases – likely to occur in 2026.

Valuation

In FY2023, HD generated $15.11 of diluted EPS; I am unable to ascertain its adjusted diluted EPS as HD has only just begun to provide adjusted diluted EPS results.

YTD2024, HD has generated diluted EPS and adjusted diluted EPS of $8.23 and $8.34. The current FY2024 guidance, however, is for a 53-week diluted EPS decline of 2% – 4% and a 53-week adjusted diluted EPS decline of 1% – 3%. We can, therefore, anticipate diluted EPS of ~$14.51 – ~$14.81. With shares having closed at $355.66 on August 14, the forward diluted PE is ~24 – ~24.5.

I expect adjusted diluted EPS broker estimates to be amended slightly lower over the coming days but for now, this is HD’s forward valuation based on currently available estimates:

- FY2024 – 22 brokers – mean of $14.84 and low/high of $14.53 – $15.18. Using the mean estimate, the forward adjusted diluted PE is ~24.

- FY2025 – 31 brokers – mean of $15.62 and low/high of $14.56 – $17.34. Using the mean estimate, the forward adjusted diluted PE is ~22.8.

- FY2026 – 20 brokers – mean of $17.04 and low/high of $15.55 – $18.99. Using the mean estimate, the forward adjusted diluted PE is ~20.9.

HD has generated YTD FCF of ~$9.4B. Let’s give HD the benefit of the doubt that it will generate $15B in FY2024 despite the difficult business environment. The diluted weighted average common shares outstanding in Q2 and the first half of FY2024 is 992 million. No change is expected since share repurchases have been paused until HD deleverages.

If we divide $15B by 992 million shares, we get ~$15.12 FCF/share. Divide $355.66 by $15.12 and we get P/FCF of ~23.52.

A more reasonable valuation for me would be if shares were to retrace to ~$310 or less. If HD’s share price were to retrace to ~$310 and we use a diluted EPS of ~$14.51 – ~$14.81, we would be looking at a ~24 – ~21.4 PE.

On a FCF basis, ~$310/$15.12 is a P/FCF of ~20.5.

Final Thoughts

I initiated a position on April 4, 2022 with the purchase of 200 shares @ ~$303.36 and acquired an additional 50 shares @ ~$301.64 on August 2, 2022. My HD exposure is currently limited to 259 shares in a ‘Side’ account within the FFJ Portfolio; the additional 9 shares were acquired through the automatic reinvestment of dividends. HD was not a top 30 holding when I completed my 2024 Mid Year FFJ Portfolio Review.

In my February 22, 2023 post I stated:

As noted in my prior post, HD has benefited from a backlog of contracted jobs that piled up during the pandemic. Its results, however, are closely intertwined with those of the US housing market. In recent months US home sales have slowed as US policymakers have sought to blunt the highest inflation in decades by raising interest rates.

According to data released by the Federal Reserve Bank of New York on February 16, 2023, total household debt in Q4 2022 increased by $394B billion (2.4%) to $16.90T. Balances now stand $2.75T higher than at the end of 2019, before the pandemic recession.

Furthermore, the share of current debt becoming delinquent increased again in Q4 for nearly all debt types, following two years of historically low delinquency transitions.

Something has to give. If interest rates continue to rise, I envision fewer homeowners being able to make home improvements relative to when we were in a very low-rate environment. This will likely negatively impact HD’s performance.

Given my outlook, I had anticipated HD’s weak results would be reflected in its share price. HD’s share price, however, has not behaved as I had hoped. We now have a $355.66 share price versus the ~$295.50 at the time of my February 22, 2023 post yet HD’s results are weaker.

A higher share price with lowered guidance. Go figure!

The combination of HD and SRS is expected to accelerate HD’s growth with the residential professional customer and establishes HD as a leading specialty trade distributor across multiple verticals. I like this. However, HD’s current valuation is somewhat too high to entice me to immediately acquire additional shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long HD.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.