High entry barriers fortify Union Pacific (UNP). My UNP exposure, however, is minimal with my only purchase being 200 shares @ $142.17 on March 9, 2020 while I was on a ski vacation in British Columbia; we were days from experiencing a ‘shut down’ of the North American economy because of the COVID pandemic.

My thought process behind this investment was that international trade would likely fall off the map. I expected North America’s major railroads to suffer in the short-term but envisioned that ‘one day’ business conditions would improve.

What I like about the North American railroad industry is the high entry barriers. There are, however, there are some drawbacks to investing in this industry.

This is a very highly regulated industry with participants typically experiencing moderate growth.

Industry participants can’t quickly and significantly grow their network. Once the rail tracks are in place, that’s it. While the railroads make enhancements/improvements to their network on an ongoing basis, they rarely make wholesale changes.

The Association of American Railroads (AAR) is also good source of information to gain a better understanding of the North American rail industry. The website includes a map showing the various North American rail networks. The website also includes comprehensive data and analysis on North American freight rail.

Looking at the map on the AAR website, we see the rail network of each Class I industry participant. UNP has no network in the Eastern part of the US or Canada. If one of UNP’s customers has a shipment coming from the Far East to a port in California, for example, UNP or BNSF will be the rail carrier of choice. If the shipment needs to make its way to the Eastern States, a UNP or BNSF rail car will eventually hooked up to a Class I industry participant that has a network in the Eastern States. This is why we often see rail cars from several different railroads being pulled simultaneously.

UNP also has several maps on its website so you can get a better understanding of the magnitude of its rail network.

The highly capital intensive nature of the industry acts as a deterrent to potential new entrants. However, the capital intensive nature also has significant drawbacks.

It costs a fortune to maintain a rail network!

Just think of the cost of 1 locomotive. There are many types of locomotives, different manufacturers, and locomotives using 4, 6, or 8 axles so the cost of a locomotive fluctuates drastically. In addition, they are powered by electricity or diesel and there is both a solid second hand and brand new market. Regardless of what type of locomotive required, we’re looking at millions of dollars just for 1 locomotive.

Think of how many cars a UNP locomotive pulls! A 4 axle locomotive will struggle to pull 100 cars at a time. UNP may have some 4 axle locomotives but most images of UNP locomotives I have seen show locomotives with more than 4 axles.

Next, think of how many locomotives UNP owns. It is easy to see how a railroad could spend billions of dollars a year just to remain operational.

Well publicized strike action is not uncommon in this industry. The Class I railroads must negotiate labor contracts with several different unions and contracts are not negotiated all at once.

We also have to consider various types of mishaps some of which are significant. A train derailment with cars carrying toxic chemicals is not unheard of.

Despite all the drawbacks reflected above, rail is typically the safest and the most efficient method by which to move significant volumes of freight over long distances.

It is also an industry with a shrinking number of industry participants. Mergers and acquisitions are rare and when they do happen, obtaining the appropriate regulatory approvals is a major undertaking. Think of Canadian Pacific’s acquisition of Kansas City Southern where the process began in early 2021 and completion was in early 2023.

Some investors may wonder if several smaller Class 2 and 3 railroads could merge their operations to ultimately become a Class 1 railroad. These railroads are so small, the rationale for merging does not make much sense.

Essentially, the North American Class 1 railroads enjoy their oligopoly.

Despite all the benefits of being an investor in North American Class 1 railroads, my UNP exposure is negligible. When I completed my 2024 Year End FFJ Portfolio Review, it did not even rank as a top 30 holding. I only have 212 shares in a ‘Side’ account within the FFJ Portfolio with 12 shares having been purchased through the automatic reinvestment of dividend income.

I last reviewed UNP in a May 10, 2024 guest post at Dividend Power. Prior to this guest post, I last reviewed UNP in this October 23, 2022 post.

With UNP’s release of Q4 and FY2024 results on January 23, 2025, I now take this opportunity to revisit this small holding.

Business Overview

The best way to learn about UNP is to review the company’s website and the Part 1 of the most recent Form 10-K.

Financials

Q4 and FY2024 Results

UNP’s most recent financial results are accessible here.

FY2024 cash from operations of ~$9.35B was up ~$1B from FY2023.

UNP’s cash flow conversion rate improved to 87% and free cash flow increased from $1.5B to $2.8B.

UNP’s adjusted debt-to-EBITDA ratio finished the year at 2.7x versus 3.0x in FY2023.

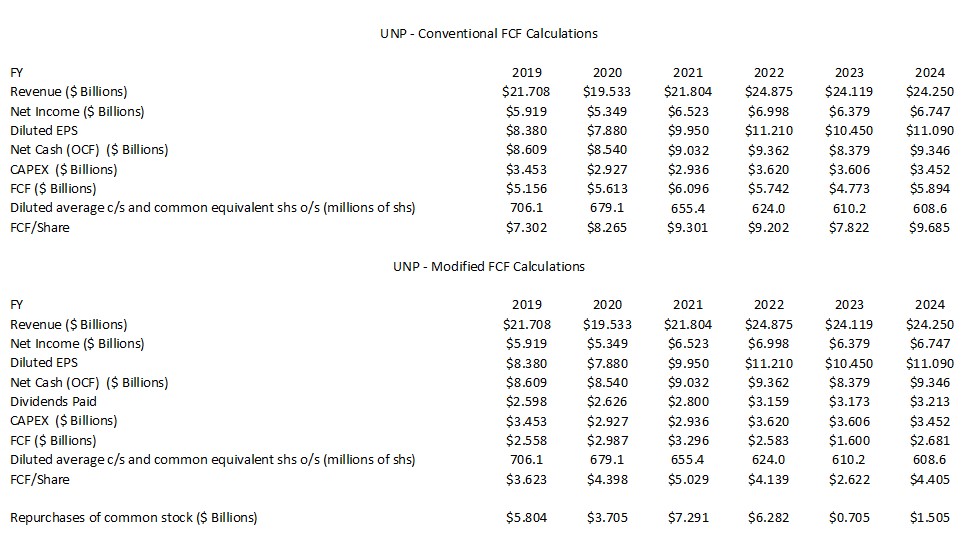

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2024)

In several previous posts I touch upon why I am now taking a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. As explained in prior recent posts, I think we need to look at FCF using the conventional method AND a modified method; the modified method also deducts share-based compensation (SBC).

Interestingly, UNP does not deduct SBC in determining its FCF nor does it reflect SBC as a line item on its consolidated statements of cash flows. It does, however, deduct dividends paid when presenting its FCF. The modified version of the FCF calculation found below, therefore, does not deduct SBC but it does deduct dividends paid

Under the conventional method of calculating FCF, UNP’s $5.894B of FCF was ~87% of $6.747B of Net Income. This cash flow conversion rate is an improvement from the prior year’s ~74.8%.

Deducting dividends paid to determine FCF, however, we get a ~40% cashflow conversion rate ($2.681B/$6.747B) versus ~25% in FY2023 ($1.6B/$6.379B) in FY2023.

FY2025 Outlook

UNP’s FY2025 outlook is as follows:

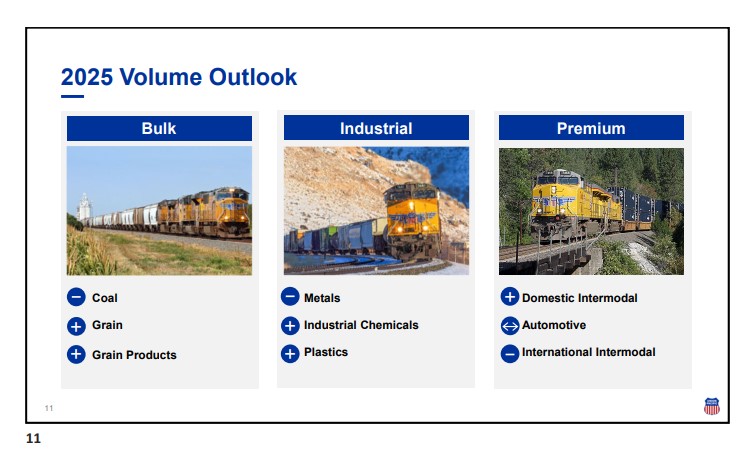

- Volume impacted by mixed economic backdrop, coal demand, and challenging YoY international intermodal comparisons;

- EPS growth consistent with attaining the 3-year CAGR target of high-single to low-double digit;

- Industry-leading operating ratio and return on invested capital;

- No change to long-term capital allocation strategy;

- Capital plan of $3.4B (similar to FY2024); and

- Share repurchases of $4.0B – $4.5B.

The $3.4B capital plan will consist of:

- $1.9B Infrastructure Replacement (Rail, Ties, & Ballast);

- $0.6B Capacity & Commercial Facilities (Locomotive Modernizations & Freight Cars);

- $0.4B Technology & Other (Intermodal and Manifest Terminals & Siding Extensions); and

- $0.5B Locomotive & Equipment (Tech-Enabled Operations & Customer Experience)

UNP currently has over 200 track construction projects in progress.

The need to spend $3.4B just to remain operational is indicative of the capital intensive nature of this business.

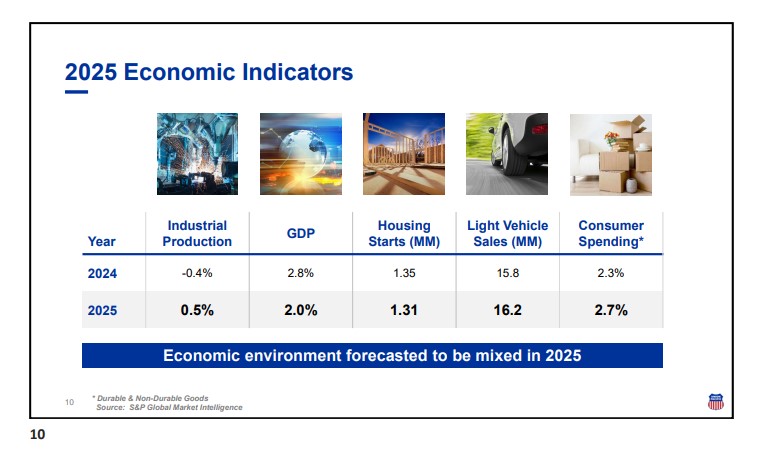

UNP used the following economic indicators to arrive at its FY2025 volume outlook. They are S&P Global’s forecast from their January report.

The 2025 economic indicators reflect a mixed picture and is not materially different from what UNP shared at its September 2024 Investor Day.

On the January 23, 2025 earnings call, UNP indicated that it is keeping a watchful eye on possible tariff, interest rate, and regulatory changes that could impact volumes. This makes UNP’s ability to forecast very challenging. At present, UNP anticipates a soft economic environment in 2025.

Credit Ratings

The FY2024 Form 10-K is currently unavailable so I encourage you to look at Note 14 in the Q3 2024 Form 10-Q that is accessible through the SEC Filing section of UNP’s website.

UNP has debt. A lot of debt! This, however, is to be expected from a highly capital intensive business.

Moody’s continues to assign an A3 senior unsecured domestic debt rating. This rating was raised from Baa1 on July 29, 2022. The current outlook is stable.

S&P Global continues to assign an A- rating. The outlook remains stable with the last review having been conducted on August 6, 2024.

Fitch last reviewed UNP on September 4, 2024 and it continues to assign an A- rating.

These ratings are the lowest tier within the upper medium grade investment grade category. They define UNP as having a very strong capacity to meet its financial commitments. The ratings differ from the highest-rated obligors only to a small degree.

These ratings are acceptable for my purposes.

Dividends

On the Q4 earnings call, management reiterated that it remains committed to its industry-leading dividend payout ratio of ~45% of earnings.

UNP’s dividend history is accessible here; it does not consistently increase its dividend after every 4 quarters.

As mentioned in several prior posts, dividend metrics should not determine investment decisions. It would be best to focus on a company’s competitive advantages and capital allocation efficiency. We should also ensure that management’s interests are closely aligned with those of shareholders.

In some instances, dividend distributions are not the most optimal means by which a company can allocate its capital. Focus on an investment’s total potential shareholder return (dividends AND capital gains).

In Q2 2023, UNP paused all share repurchases and did not expect to be back in the market for the remainder of 2023. This decision was made in recognition of cash flows that were negatively impacted by the current environment which resulted in lower volumes and higher costs. The decision was no reflection of UNP’s existing capital allocation strategy:

- reinvest in the business;

- dividend distributions; and

- share repurchases.

This explains the drop in UNP’s share repurchases in FY2023 and, to a lesser extent, in FY2024.

When I initiated a UNP position in March 2020, the diluted weighted average number of shares in FY2017 – FY2019 (in millions of shares) was 801.7, 754.3, and 706.1. In FY2023 and FY2024, UNP repurchased $0.705B and $1.505B of shares and by Q4 2024, the diluted weighted average number of shares outstanding had been reduced to 605.2.

In FY2025, UNP plans to repurchase ~$4B – ~$4.5B of its shares.

Valuation

Following the release of UNP’s Q4 and FY2024 results, the share price has surged to ~$248. Using the FY2024 diluted EPS of $11.09, the trailing PE is ~22.4.

Investors, however, would be wise to look at how a company is expected to perform as opposed to how it has already performed.

Management is targeting EPS growth consistent with attaining the 3-Year CAGR target of High-Single to Low-Double Digit. Using a 10% growth rate, we get ~$12.20 EPS for FY2025. With shares trading at ~$248 at the January 23 market close, the forward diluted PE is ~20.3.

UNP’s FY2024 FCF/share using the conventional method of calculation is ~$9.685. Using the current share price, the P/FCF is ~25.6. If we use ~$7.713 calculated using the modified FCF method of calculation, the P/FCF is ~32.2.

The valuation using broker forward adjusted diluted EPS estimates is:

- FY2025: 30 brokers, mean estimate $12.06, low/high range $11.56 – $12.58. The valuation using the mean estimate is ~20.6.

- FY2026: 27 brokers, mean estimate $13.45, low/high range $12.19 – $14.24. The valuation using the mean estimate is ~18.4.

- FY2027: 8 brokers, mean estimate $14.86 low/high range $12.53 – $16.01. The valuation using the mean estimate is ~16.7.

- FY2028: 3 brokers, mean estimate $16.48 low/high range $15.34 – $17.26. The valuation using the mean estimate is ~15.1.

Since UNP has just released its 2024 results and its 2025 outlook, the broker estimates are likely to be revised over the coming days. Even after all the brokers update their estimates, I would not rely on them to make investment decisions. While some estimates may end up being reasonably accurate, I would chalk this up to just being lucky. Nobody can consistently accurately predict future earnings. Furthermore, we have no idea what input data these brokers are using to come up with their estimates. Considering the wide disparity in estimates, it suggests to me that we place very little reliance on them.

General market conditions are such that I am being extremely cautious. UNP currently appears to be somewhat overvalued and based on the currently available information, a share price of ~$220 strikes me as being fair.

Final Thoughts

Although I have minimal UNP exposure, I also own:

- 1014 Canadian Pacific Kansas City (CP.to) shares following a 4 for 1 stock split in May 2021. I acquired shares on March 9 and 12, 2020 in a ‘Core’ account within the FFJ Portfolio.

- 793 Canadian National Railway (CNR.to) shares. I acquired shares on February 3 and April 26, 2016 in another ‘Core’ account.

I am comfortable with my overall exposure to Class 1 railroads despite none of the 3 holdings being a top 30 holding when I completed my 2024 Year End FFJ Portfolio Review.

While there is much to like about UNP, I have no plans to increase my exposure. My focus is on increasing exposure to companies that are less capital intensive.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long UNP, CP.to, and CNR.to.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.