In this September 2019 post, I disclosed a new position in HEICO position with the purchase of 300 shares @ ~$99/share in one of the ‘Side’ accounts in the FFJ Portfolio. What prompted me to analyze this company was an article entitled The Greatest Investor You’ve Never Heard Of: An Optometrist Who Beat The Odds To Become A Billionaire published in Forbes on February 19, 2019. I wish this optometrist had contacted me when he initiated an HEI position in 1992!

Fortunately, I stumbled on this Forbes article in 2019 and since then there has been no looking back.

I last reviewed HEICO (HEI and HEI-a) in this December 18, 2024 post at which time the most currently available financial information was for Q4 and FY2024. When I wrote that post I stated that HEI-a was my:

- 25th largest holding when I completed my 2023 Year End FFJ Portfolio Review; and

- 16th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review.

When I completed my 2024 Year End Review, HEI had become my 9th largest holding.

In addition to being my 9th largest holding, a couple of young investors (27 and 30 years of age) also have HEI-a exposure through their Tax Free Savings Accounts (TFSA) and First Homeowner Savings Accounts (FHSA). I do not, however, include their exposure when ranking my holdings.

Now that HEI has released its Q1 2025 results following the February 26 post market close, I revisit this existing holding.

IMPORTANT:

- HEICO Corporation has two classes of common stock (HEI and HEI.a). Both classes of shares are virtually identical in all economic respects except voting rights. The difference is that each HEI share is entitled to one vote per share while each HEI.a share is entitled to a 1/10 vote per share. This post focuses on the HEI.a shares (non-voting) since these are the shares I own.

- Do not confuse HEICO Corporation with privately owned The Heico Companies.

Business Overview

Fortunately, HEI has a much improved website that includes a section with links to the websites of many subsidiaries. This enables us to learn about their respective operations.

Naturally, HEI’s 2024 Annual Report/Form 10-K is a must read if there is any thought of investing in the company.

HEI’s Disciplined Acquisition Strategy

Acquisitions have been an important element of HEI’s growth strategy.

The following is extracted from HEI’s FY2024 Form 10-K.

Acquisitions have been an important element of our growth strategy over the past thirty-four years, supplementing our organic growth. Since 1990, we have completed approximately 103 acquisitions complementing the niche segments of the aviation, defense, space, medical, telecommunications and electronics industries in which we operate. We typically target acquisition opportunities that allow us to broaden our product offerings, services and technologies while expanding our customer base and geographic presence. Even though we have historically pursued an active acquisition policy, our disciplined acquisition strategy involves limiting acquisition candidates to businesses that we believe will continue to grow, offer strong cash flow and earnings potential, and are available at fair prices.

The About Us and Press Releases sections of the company’s website provide information on several of HEIs’ acquisitions over the years.

HEI makes conservative use of debt and uses its strong cash flow to reduce debt taken on for acquisition purposes. Management regularly articulates that its synergistic acquisitions are structured to be accretive to earnings within the year following closing.

Financials

Q1 2025 Results

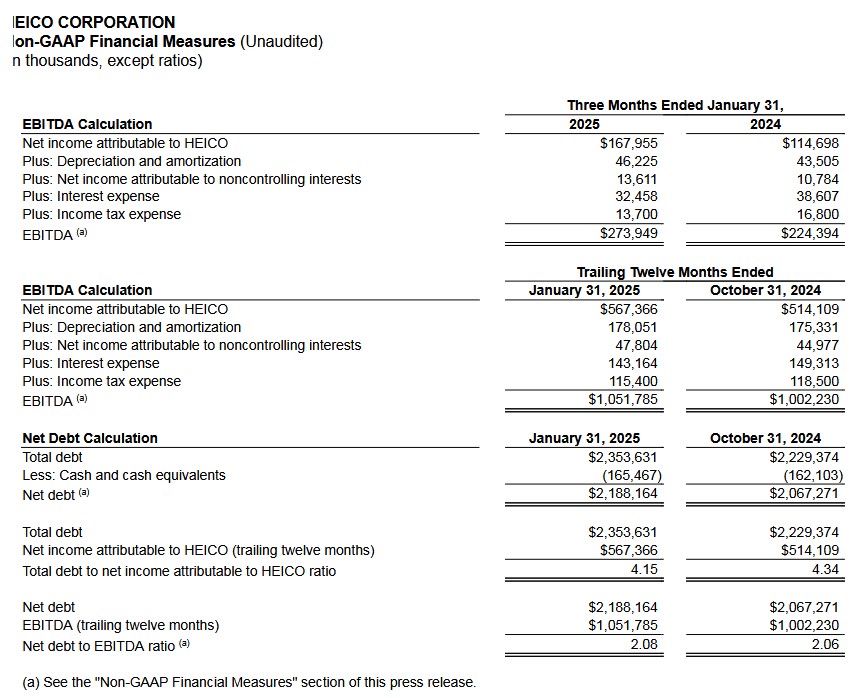

HEI’s most recently released financial results are accessible in the Form 8-K released on February 26.

I provide HEI’s non-GAAP Financial Measures extracted from the February 26 earnings release for ease of reference.

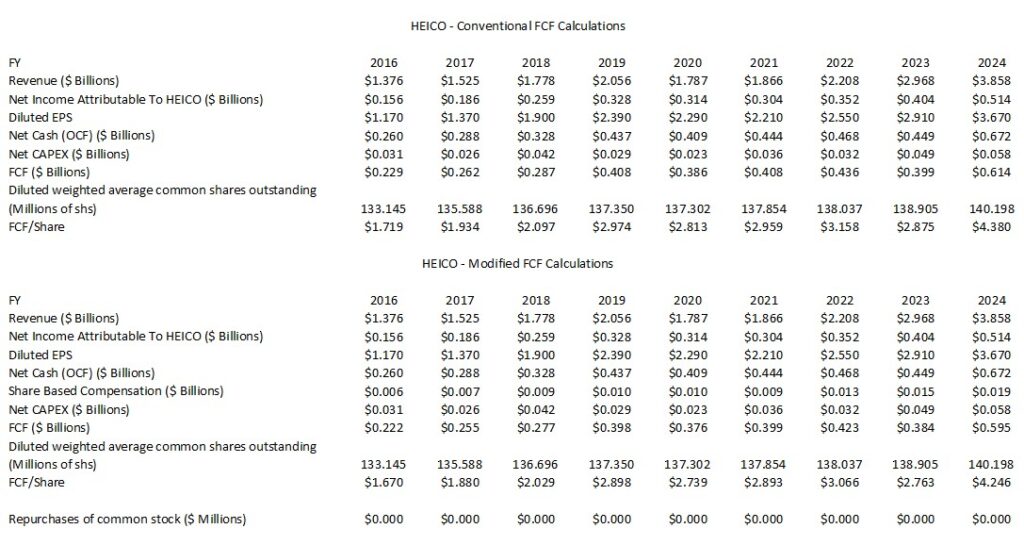

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2016 – FY2024)

FCF is a non-GAAP measure, and therefore, its computation is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows.

In several posts, I touch upon why investors should deduct share based compensation (SBC) when analyzing a company’s FCF.

Unlike many technology companies that issue a ‘boatload’ of shares annually as part of its various SBC programs, HEI’s use of SBC is conservative. As a result, the FCF calculated using the conventional and modified methods does not result in a material variance.

HEI’s Q1 2025 SBC was only $4.671 million.

FY2025 Outlook

HEI typically does not provide net sales and earnings guidance. Management continually states, however, that the company will continue to invest in research and development and execute its successful acquisition program.

Risk Assessment

HEI’s domestic senior unsecured long-term debt ratings are:

- Moody’s: Baa2 with a stable outlook (last reviewed on June 20, 2023)

- Fitch: BBB with a stable outlook (last reviewed on September 4)

Both ratings are in the middle tier of the lower medium-grade investment-grade category. These ratings define HEI as having an adequate capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

*S&P Global does not rate HEI’s debt.*

Once again….do NOT confuse HEICO Corporation with The Heico Companies. These entities are unrelated.

Dividends and Share Repurchases

Dividend and Dividend Yield

Warren Buffett and Charlie Munger (now deceased) use one key test to determine whether it makes sense for a company to distribute a dividend or not. The test is whether a company can continue to create more than $1 of value for every dollar retained. In essence, a company should probably not distribute a dividend (or distribute a very small dividend) when it has the opportunity to reinvest retained earnings profitably.

HEI’s exemplary track record demonstrates that reinvesting in the business is the most optimal means of allocating capital.

Don’t even bother with HEI’s dividend metrics. The vast majority of any potential return will likely continue to be in the form of capital appreciation.

On December 17, 2024, HEI declared its 93rd consecutive semi-annual cash dividend since 1979; the dividend history is accessible here.

Stock Splits and Share Repurchases

HEI has had six 5 for 4 stock splits over the years; twelve stock splits are reflected but investors must remember that HEI has 2 classes of common stock.

HEI issues shares as part of its employee compensation structure. It also issues HEI-a shares to the sellers of many of the companies it acquires thus permitting the sellers to participate in HEI’s wealth creation model. This explains the growth in the diluted weighted average number of outstanding shares in FY2016 – FY2024 reflected in the table provided earlier.

Looking at HEI’s Condensed Consolidated Statements of Cash Flows over the past several years, we see that share repurchases are negligible. They are generally for the redemption of common stock related to stock option exercises as opposed to share repurchases on the open market.

Valuation

Trying to gauge HEI’s valuation based on GAAP earnings is a challenge because of the magnitude of its non-cash depreciation and amortization. I, therefore, prefer to gauge HEI’s valuation using Price/FCF.

Following the release of Q1 2025 earnings, HEI’s and HEI-a’s respective share price has surged to ~$257.50 and ~$209, respectively.

I calculate HEI’s Q1 2025 FCF as follows:

- Net cash provided by operating activities: ~$203 million

- Less Share-based compensation expense: ~$4.671 million

- Less Employer contributions to HEICO Savings and Investment Plan: ~$5.473 million

- Less CAPEX: $17.335 million

- Q1 2025 FCF: ~$175.521 million

If HEI generates a similar amount of FCF over each of the next 3 quarters in FY2025, we can anticipate FY2025 FCF to be ~$702 million.

The diluted weighted average number of common shares outstanding (in millions) in FY2022 – FY2024 and Q1 2025 was 138,037, 138,905, 140,198, and 140,484 million. It seems realistic to expect the FY2025 diluted weighted average number of common shares outstanding to likely increase to ~141,520 million.

Divide ~$702 million of FY2025 FCF by ~141.52 million shares and we get FCF/share of ~$4.96. Using the current share prices reflected above, the forward P/FCF for HEI shares is ~52 and ~42 for HEI-a shares.

Final Thoughts

My Final Thoughts are much the same as those in my December 18, 2024 post.

The 52 Week Price Range of the HEI-a shares is $146.92 – $219.22 and $182.47 – $283.60 for the HEI shares.

Current market conditions suggest that many investors are being somewhat irrational when making investment decisions. Just look at HEI’s share price behavior over the past few months! The underlying fundamentals of the company continue to improve but not to the extent that justify the recent share price surge.

I increased my HEI-a exposure on December 18 with the purchase of 300 shares. In hindsight, I should have acquired more shares in early January and/or mid-February 2025. However, excluding the December 18 HEI-a purchase, I also deployed ~$131,400 in December and January with the purchase of shares in other companies.

This does not strike me as an opportune time to acquire shares and since my purchasing power is not limitless, I wish to retain some ‘dry powder’ that I can deploy if we experience a broad market correction.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long HEI-a.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.