In my March 27, 2024 Automatic Data Processing (ADP) guest post at Dividend Power I conclude shares are overvalued.

I have been an ADP shareholder for decades. The majority of my exposure is through a tax efficient Registered Retirement Savings Plan (RRSP) account for which I do not disclose details. I have made no additional RRSP contributions following my retirement in May 2016. Through the accumulation of cash from the portion of dividend income received from the various holdings in my RRSP that was not automatically reinvested, however, I have increased my exposure in July 2020 (see post), January 2023 (see post), and July 2023. I also acquired 100 shares @ ~$197.74 in a taxable ‘Side’ account in the FFJ Portfolio (see post) on January 26, 2022.

I need to increase my ADP exposure in taxable accounts to offset the shares held in RRSPs that I will eventually need to sell as part of my RRSP meltdown strategy.

As luck would have it, ADP’s share price has fallen from the ~$330 level in the first week of June 2025. Following the release of Q1 2026 results and FY2026 outlook on October 29, ADP’s share price closed at $261.22.

Let’s look at ADP’s valuation.

Business Overview

You are likely familiar with ADP. It does, after all:

- operate in 140+ countries;

- has more than 1.1 million clients ranging from small businesses to large multi-national corporations for whom it provides Human Capital Management (HCM) and HR Outsourcing (HRO) services; and

- distributes payroll to more than 42 million people.

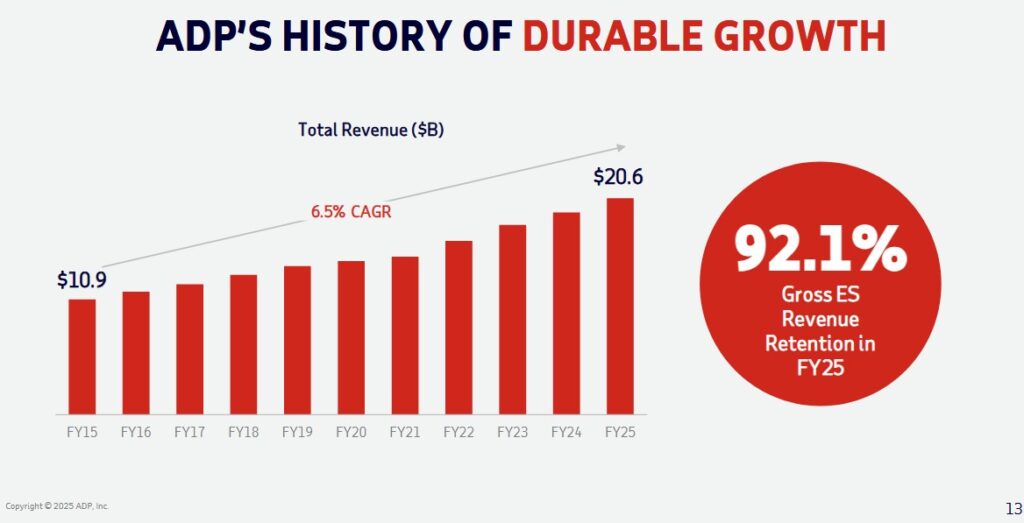

Between FY2015 – FY2025, ADP has reported a ~6.5% compound annual total revenue growth rate.

Please review the company’s website and read Part 1 Items 1 (Business) and 1A (Risk Factors) in the FY2025 Form 10-K that is accessible through the SEC Filings section of the company’s website if you are unfamiliar with ADP.

Financials

Q1 2026 Results

The material released on October 29, 2025 is accessible here.

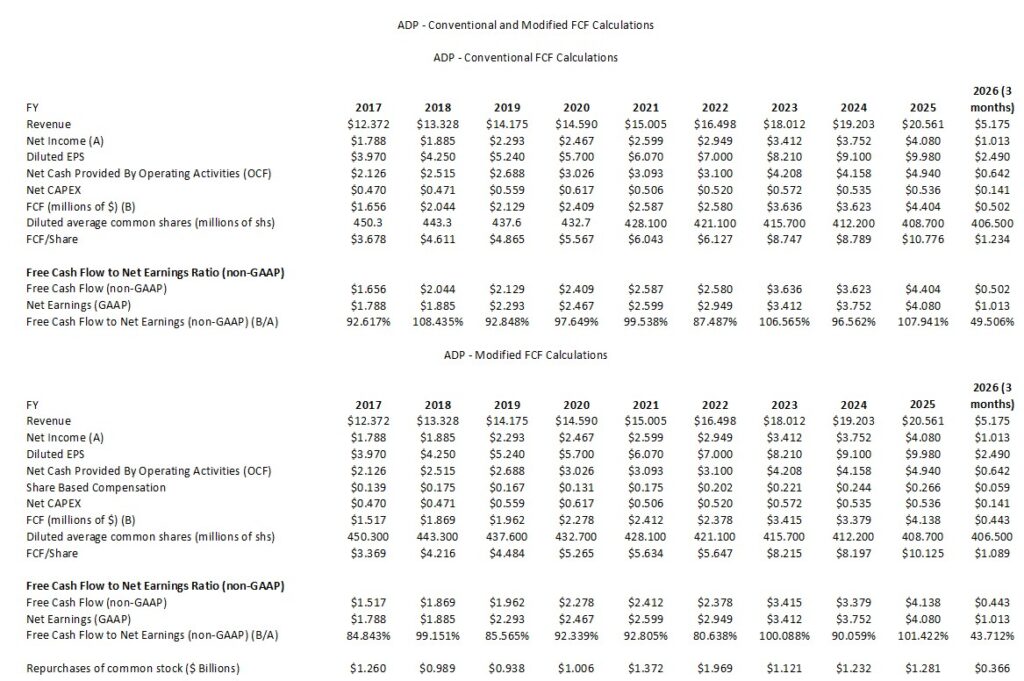

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2017 – FY2025 and Q1 2026)

In several posts I express my thoughts about the way many companies calculate Free Cash Flow (FCF). Since FCF is a non-GAAP metric, there is no standardization in its calculation.

In most cases, companies merely deduct net CAPEX from net cash flows from operating activities. ADP, however, calculates FCF by subtracting CAPEX and Additions to Intangibles from Net Cash Flows provided by operating activities. I am more conservative and also deduct share based compensation (SBC) to arrive at ADP’s modified FCF.

NOTE: You are cautioned not to read into the weak Q1 2026 FCF/Net Earnings Ratio. Given ADP’s historical FCF/Net Earnings Ratio, we are likely to see a significant improvement as FY2026 progresses.

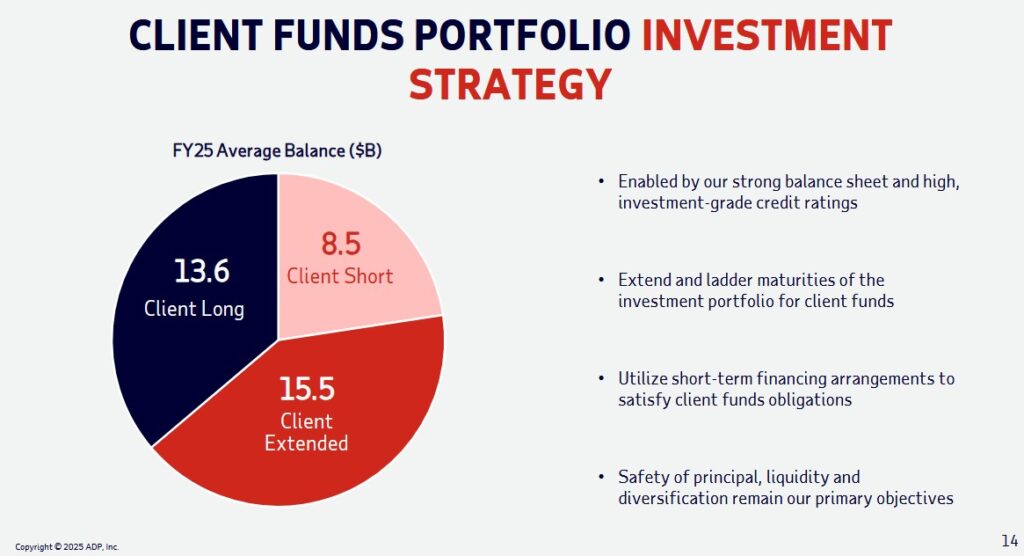

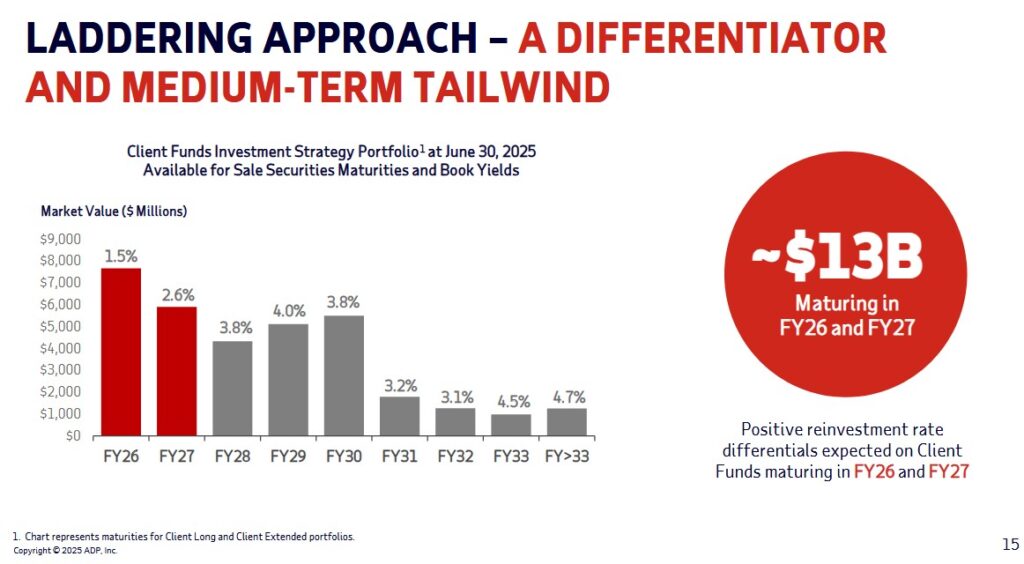

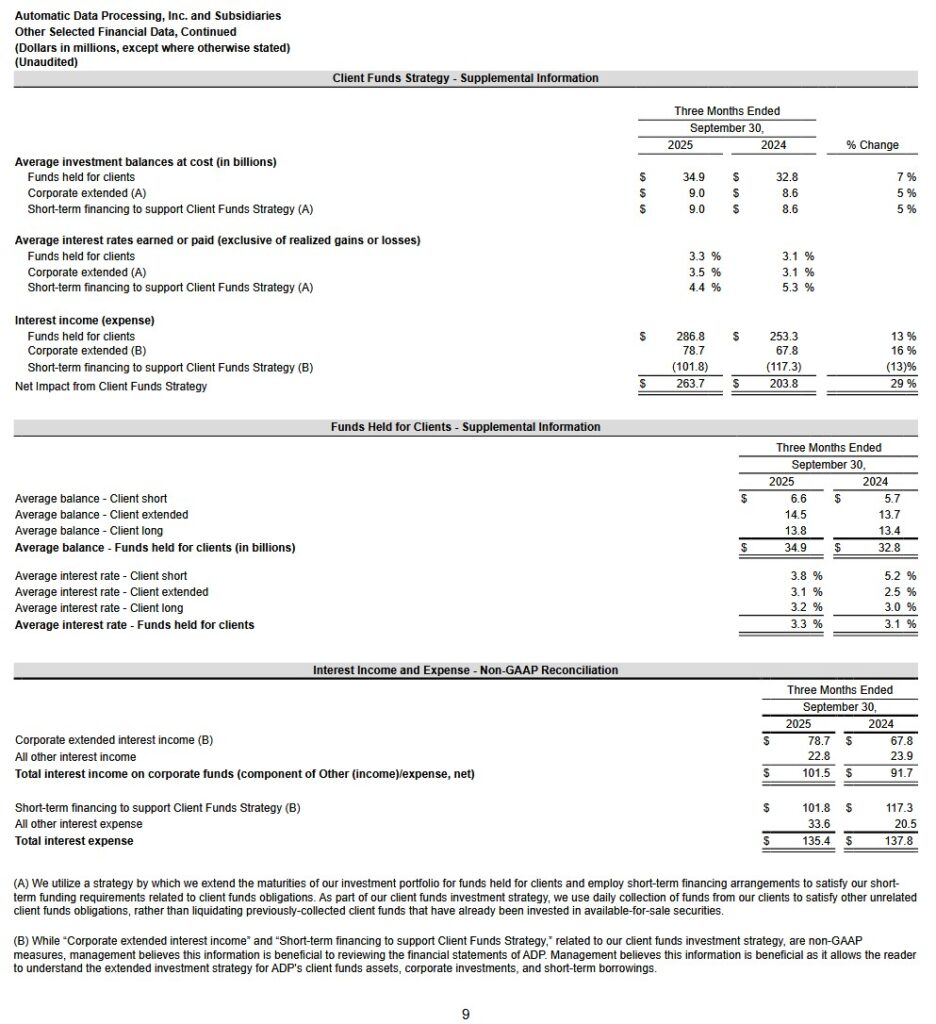

Clients Funds Investment Strategy

Note 5 in ADP’s FY2025 Form 10-K starting on page 63 of 97 provides a comprehensive overview of ADP’s Clients Funds Investment Strategy.

The purpose of this Investment Strategy is to generate income from significant client fund balances. When deemed prudent, ADP will further enhance its investment returns by investing long and borrowing short to take advantage of the yield spread.

This strategy allows ADP to average its way through an interest rate cycle by laddering the maturities of investments out to 5 years (in the case of the extended portfolio) and out to 10 years (in the case of the long portfolio). ADP’s short-term financing arrangements necessary to satisfy short-term funding requirements relating to client funds obligations supports this investment strategy.

The following reflects the Q1 2024 and Q1 2025 results of ADP’s Client Funds Investment Strategy.

Management provided the following commentary on its Q1 2026 earnings call:

Client funds interest revenue increased more than we anticipated in Q1, helped by stronger average client funds balance growth, while the yield curve has declined marginally since our last update. This impact is more than offset by our stronger client funds balance growth. We are now forecasting average client funds balances to grow 3% – 4% in FY2026, and we are continuing to expect an average yield of ~3.4%. Accordingly, we are increasing our full year forecast for client funds interest revenue by $10 million to a range of $1.30B – $1.32B. We are also increasing our expected net impact from our extended investment strategy by $10 million to a range of $1.26B -$1.28B.

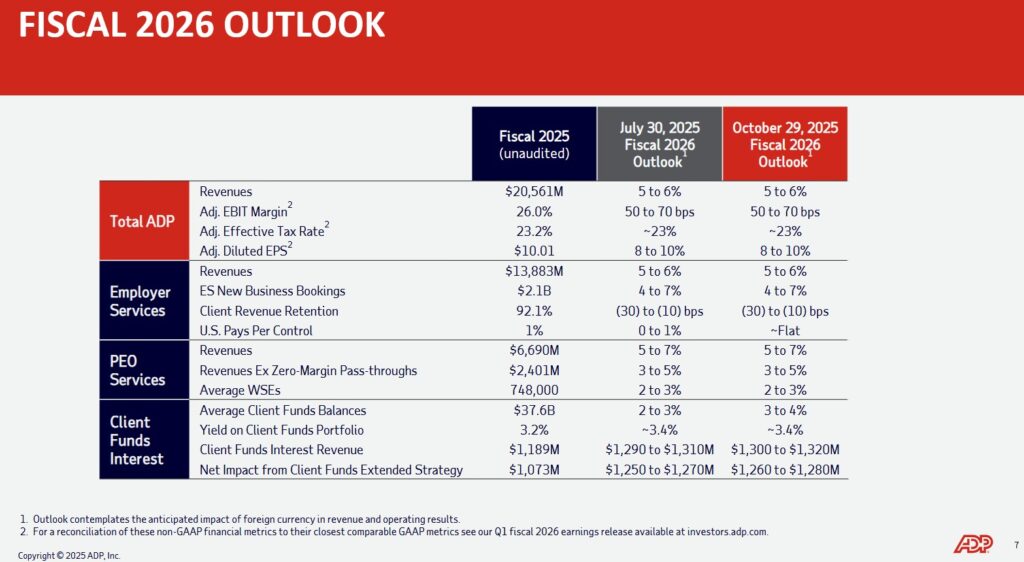

FY2026 Outlook

The following reflects ADP’s FY2025 results and current and prior FY2026 outlook.

Risk Assessment

Every investment comes with potential reward and risk. Regrettably, some investors never assess an investment’s potential risks OR they overestimate their risk tolerance.

My investor profile is such that I invest in high quality companies with a promising future. I am, therefore, prepared to forego ‘potential reward’ if the risk is likely to lead to a ‘loss of sleep’.

While the credit rating agencies are not infallible, I take into consideration their take on a company’s risk. The following are ADP’s senior domestic unsecured long-term debt ratings:

- Moody’s: Aa3 with a stable outlook – affirmed on October 15, 2024

- S&P Global: AA- with a stable outlook – affirmed on March 17, 2025

- Fitch: AA- with a stable outlook – affirmed on October 17, 2025

All 3 ratings are the lowest tier of the high grade investment grade category. These ratings define ADP as having a very strong capacity to meet its financial commitments. These ratings differ from the highest-rated obligors only to a small degree.

NOTE: Equity investors have greater risk exposure than senior domestic unsecured long-term debt holders. Investing in a company whose credit ratings are the lowest investment grade levels, therefore, means an equity investor assumes non-investment grade risk.

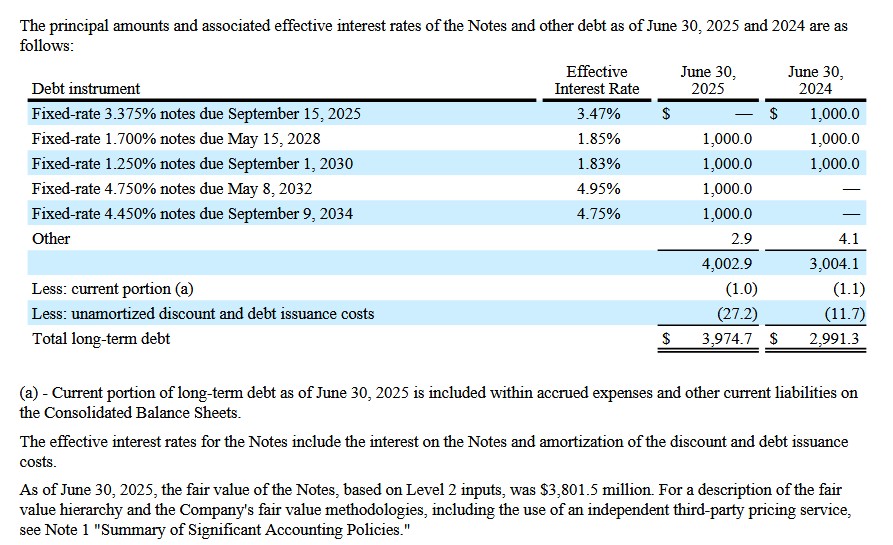

I also look at the details of a company’s Operating Leases, Short-Term Financing, and Long-Term Debt.

As I compose this post, ADP’s Q1 2026 Form 10-Q is unavailable. I, therefore, reference Notes 7, 9, and 10 in its FY2025 Form 10-K which detail the company’s financing arrangements.

ADP’s long-term debt at the end of Q1 2026 is $3.976B which is very similar to the amount owing at FYE2025.

ADP has no long-term debt maturing until May 15, 2028. This leaves it with ~2.5 years to accumulate ~$1B in order to retire the debt due on May 15, 2028. This should be easily attainable thus leaving ADP with considerable flexibility from a capital allocation perspective.

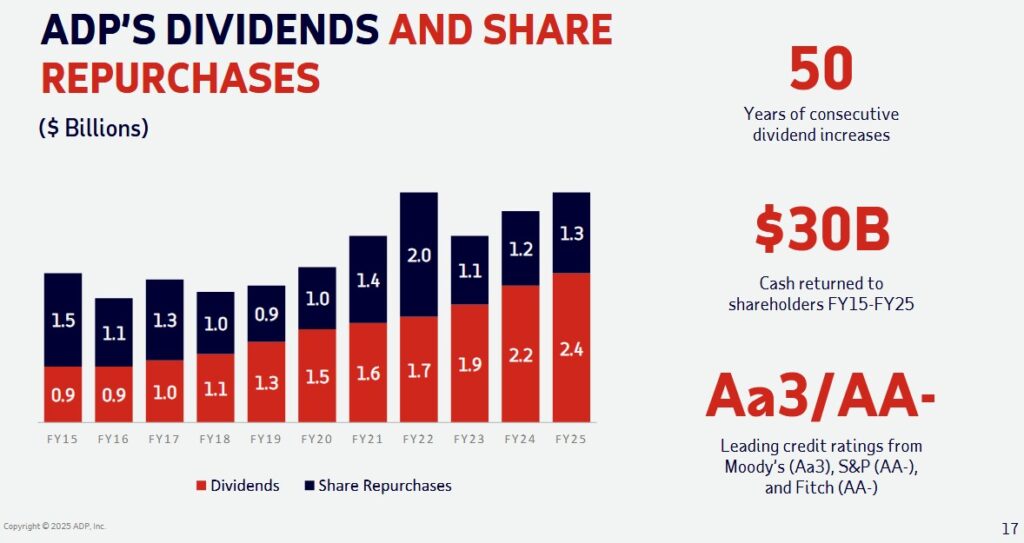

Dividends and Share Repurchases

Dividend and Dividend Yield

ADP has increased its dividend for 50 consecutive years in November 2024 (see dividend history). Relying on dividend metrics to make investment decisions, however, is a fundamentally flawed method by which to invest. Investors would be wise to look at the TOTAL potential return.

The following is extracted from ADP’s 2025 Investor Day presentation.

I anticipate ADP will announce in early November at least a 10% increase to the current $1.54 quarterly dividend.

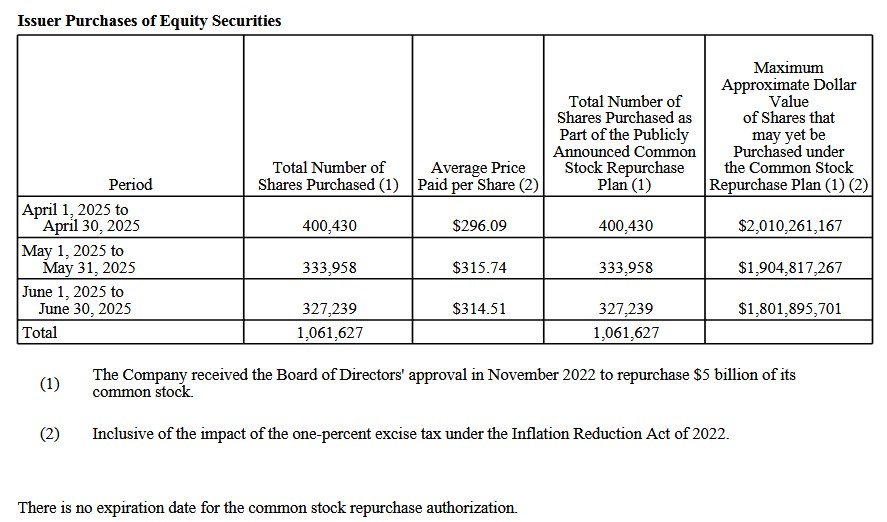

Share Repurchases

Management has done a commendable job of reducing the issued and outstanding shares. In the FY2017 , there were 450.3 million outstanding shares. In Q1 2026, the weighted average outstanding shares was 406.5 million.

ADP repurchased 4.4 million shares in FY2025 as compared to 5.1 million shares repurchased in FY2024. It considers several factors in determining when to execute share repurchases, including, among other things, actual and potential acquisition activity, cash balances and cash flows, issuances due to employee benefit plan activity, and market conditions.

Earlier, I mention that many investors may come out ahead if a company prioritizes share repurchase over dividend distributions. Naturally, this is not applicable to every company. Furthermore, the price at which shares are repurchased has a significant impact on shareholder returns. Repurchase shares when they are undervalued and shareholders benefit. Investors, however, suffer if shares are repurchased when the valuation is in the stratosphere.

Regrettably, ADP repurchased richly valued shares in Q4 2025.

I hope ADP’s shares can remain undervalued long enough to permit ADP to repurchase shares at more favorable valuations.

Valuation

The following reflects my valuation estimate when my March 27, 2024 guest post was published at Dividend Power.

ADP’s forward adjusted diluted PE levels using the current ~$249 share price and brokers’ adjusted diluted earnings estimates are:

- FY2024: 20 brokers – current mean $9.21 and $9.05/$9.21 low/high range; ~27.0 using the mean.

- FY2025: 20 brokers – current mean $10.16 and $9.80/$10.16 low/high range; ~24.5 using the mean.

- FY2026: 12 brokers – current mean $11.25 and $10.66/$11.25 low/high range; ~22.1 using the mean.

Management’s FY2024 adjusted diluted EPS forecast is ~$9.05 – ~$9.22. Using the current ~$249 share price, the forward adjusted diluted PE range is ~27X – ~27.5X.

In the first half of FY2024, ADP generated $1.099B in FCF. If ADP were to generate ~$2.7B in FCF in FY2024 and the weighted average outstanding shares for the year were to be 412 million, we arrive at ~$6.55 FCF/share. Using the current ~$249 share price, the P/FCF per share is ~38.

In my opinion, ADP appears to be overvalued.

In FY2025, ADP generated $9.98 and $10.01 of diluted EPS and adjusted diluted EPS. Current FY2026 guidance calls for a 8% – 10% increase from FY2025’s adjusted diluted EPS (~$10.81 – ~$11.01).

ADP’s closing share price on October 29, 2025 is $261.22 giving us a forward adjusted diluted PE of ~23.7 – ~24.2.

ADP’s forward adjusted diluted PE levels using the current brokers’ adjusted diluted earnings estimates are:

- FY2026: 16 brokers – current mean $10.93 and $10.85/$11.00 low/high range; ~24 using the mean.

- FY2027: 16 brokers – current mean $11.96 and $11.39/$12.40 low/high range; ~21.8 using the mean.

- FY2028: 9 brokers – current mean $13.02 and $12.49/$13.35 low/high range; ~20 using the mean.

The FCF/Net Earnings Ratio in Q1 2026 is likely to improve as the year progresses. On a modified basis, I envision the ratio will likely be ~90% – ~95%. If my estimate is correct, ADP’s P/FCF valuation will be slightly worse than on an adjusted PE basis. Nevertheless, my valuation estimates using adjusted earnings and FCF are superior to ADP’s valuation at just about every point in the last few years.

Final Thoughts

ADP’s more than 1.1 million clients and payroll distribution to more than 42 million people is impressive. We, however, need to put these numbers in perspective. The total global addressable market is significantly larger so ADP has ample growth opportunities.

The headlines like to report negative news. Some people will fixate on the number of employees being laid off by Amazon, UPS, Intel, Nestle, Accenture, Ford, etc.. Of these laid off employees, many will go on to form new companies. Despite the risks posed by artificial intelligence, the odds are that 10 – 15 years from now, more people will be employed than at present. The type of jobs, however, may differ from today.

We also have to consider that over an extended period, the amount of money that flows through ADP’s ‘Funds held for clients’ Balance Sheet line item is likely to increase. Through its ‘Client Funds Investment Strategy’, ADP should be able to generate more income. Naturally, interest rate behavior will influence how much income from this source ADP will be able to generate.

ADP is not a capital intensive business. It may allocate billions of dollars over the years to make strategic and bolt-on acquisitions. Furthermore, a good percentage of the ~$1B ADP spends annually on R&D actually improves its products and services. It is not, however, a capital intensive business (eg. railroads, auto manufacturers, airlines) that needs to spend BILLIONS annually on CAPEX just to ‘keep the lights on’. In addition, it is not like the Mag 7 constituents that are spending BILLIONS on AI infrastructure.

At the outset of this post I state that I have been an ADP shareholder for decades. Never in my wildest dreams did I imagine that ADP’s 1990 annual revenue and net earnings of ~$1.7B and ~$0.212B would be considerably less than the revenue and net earnings of ~$5.175B and ~$1.013B it generated in Q1 2026.

What are the odds of ADP being far more valuable 10, 20, or 30 years from now? Probably pretty strong.

Having said all this, I acquired another 200 shares @ $269.78 in a ‘Core’ account in the FFJ Portfolio on October 29. I plan to acquire additional shares if ADP’s valuation remains attractive.

ADP was my 13th largest holding when I completed my 2025 Mid-Year Portfolio Review. I intend to keep it within the top 20 holdings.

I wish you much success on your journey to financial freedom!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ADP.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.