I last reviewed Blackstone (BX) in this post following the release of Q3 and YTD2024 results. Now that we have BX’s Q4 and FY2024 results, I revisit this existing holding.

Coincidentally, the account in which I hold BX shares unexpectedly reported multiple entries with a February 5, 2025 trade date but back dated settlement dates. The settlement dates are the dates on which I received BX distributions in 2024.

When the February, May, August, and November 2024 distributions were posted, the entire amount was reflected as a distribution of earnings. As a Canadian resident holding these shares in taxable account, 15% of the distribution was withheld (tax).

The ‘Tax Info/Dividends’ section of BX’s website now shows that BX has amended the breakdown of these 2024 distributions. Each distribution now consists of a Qualified Dividend and a Return of Capital (ROC). Prior to these adjustments, I would have had to declare what I received as income on my 2024 tax return.

The ROC component of the quarterly distributions, however, are tax efficient. This is because ROC represents a repayment of a portion of my original investment and thus reduces my adjusted cost base (ACB). BX’s ACB when I completed my January 31, 2025 FFJ Portfolio Holdings report was $112.569. It is now $110.7349.

The lowering of my ACB will impact the capital gains tax owing when I eventually sell my BX shares. Fortunately, I can postpone my tax obligation for as long as I decide not to dispose of my shares.

Industry Overview

In prior BX posts I touch upon PwC’s ‘2023 Global Asset and Wealth Management Survey‘. The results of this survey suggest ~1 in 6 asset and wealth management companies globally are likely to disappear or be acquired by 2027. This is twice the normal turnover rate.

There are far too many asset managers chasing a finite number of great deals. The behemoths such as BX may do fine but many much smaller asset managers will likely suffer.

On Apollo Global Management, Inc.’s (APO) Q4 2024 earnings call, CEO Marc Rowan says that industry participants will need to reinvent their businesses because of competitive forces. He anticipates that a wave of partnerships between alternative and big asset managers will shake up Wall Street. His prediction is for large private capital companies to increasingly distribute their investments, such as corporate buyouts, to traditional asset managers that prioritized raising their clients’ exposure to unlisted assets. He states that BlackRock’s (BLK) acquisition of private credit manager HPS Investment Partners and infrastructure group Global Infrastructure Partners should be taken as a wake-up call to the investment industry.

The industry’s largest private capital groups such as BX, Brookfield (BAM and BN), APO, and KKR are muscling their way into the area of managing money for wealthy individual investors and ordinary retirement savers. Senior executives within the industry predict the management of trillions of dollars for individual investors in addition to the $13T the industry manages for institutions.

Historically, traditional asset managers have prioritized investing in unlisted assets as they carry higher fees and greater diversification than public markets. Expansion efforts into new markets come as investors increasingly view public stock and bond portfolios as commodity products; the fees on public funds are expected to fall.

Rowan expects firms such as those listed above to become suppliers of products similar to traditional asset managers. Partnerships between two areas of finance that have for decades been treated as distinct markets reflect the increasing lending ties between private capital groups and the broader banking system.

Following the collapse of Silicon Valley Bank and Credit Suisse in 2023, private capital groups have formed loan origination ventures with large banks (eg. Citigroup and JPMorgan). This is because regulations and capital constraints curtailed the banks’ ability to lend.

In these loan origination ventures, private capital firms use their investors’ cash to fund loans sourced by the large banks. Flow arrangements are then formed to distribute slices of the originated loans; they sell pieces to large banks in search of higher-yielding assets.

Another change within the industry is that private equity firms are finding new ways to keep a tighter grip on portfolio companies if they get into financial distress. Provisions are being added to debt documents to curb creditor voting rights. In addition, private equity firms are pushing back against so-called cooperation agreements between lenders. Such agreements allow creditors to act as one entity during negotiations with distressed borrowers and let them reject restructuring proposals that would crush the value of their debt.

BX, for example, has on more than one occasion added terms in recent debt sales by portfolio companies to limit the voting rights of any single holder in future credit decisions. The added terms limit the rights of individual debtholders at 20% regardless of the size of their stake while allowing the borrowers to increase this voting cap for specific creditors. The result is to give the companies and their private equity owners power to determine which investors will have a bigger say in future votes.

We are essentially witnessing a power struggle between buyout firms and debt investors. In most instances, creditors are ceding power and protections in exchange for high-yielding debt.

In essence, the world of high finance is evolving. Conservative investors may, therefore, wish to limit their asset management exposure to the largest and most influential industry participants.

Buyout Groups Seek Alternative Ways To Cash Out

After a prolonged drought in dealmaking, pension funds and buyout groups found other other ways to cash in their investments in 2024.

Global secondary market volumes reached $162B in 2024. This was a 45 % increase from 2023 and 20+% from the previous peak in 2021.

The secondary market is where investors in private equity or other private funds sell their stakes to new investors for cash. In some instances, the fund managers sell company stakes to their new funds.

Because private equity firms have struggled to exit investments through IPOs or sales at sufficiently attractive valuations, many portfolios became too heavily weighted towards private equity. In 2024, however, many Limited Partners (LPs) wanting to rebalance their investment holdings turned to the secondary markets to try to find buyers for their investment stakes. Meanwhile the General Partners (GPs) which manage the private equity firms were also looking for alternative ways to cash in their investments.

As noted above, the secondary volume boomed in 2024. The LPs, often institutions such as pension funds, endowments or sovereign wealth investors, sold record volumes on the secondary market. They sold ~$87B of fund stakes representing a 36% increase from the previous record set in 2021.

Meanwhile, GPs sold ~$75B of assets in 2024 representing a 44% increase from the prior year. Roughly $63B came from asset managers selling their assets from one of their funds to one of their newer funds. This is known as a continuation vehicle (CV).

CVs have become a popular option for private equity firms to return money to the investors in one fund without having to find a buyer for the whole of a portfolio company. This is particularly advantageous where a sale might not achieve a favorable valuation for the manager.

Business Overview

BX is one of the world’s leading managers of alternative assets. In recent years, it has rapidly grown its fee-earning assets under management (AUM). Its assets are relatively well balanced among

private equity, real estate, hedge funds, and credit.

The FY2024 Form 10-K is currently unavailable as I compose this post on February 6. BX’s website and Part 1 of the FY2023 Form 10-K, however, provide ample information to learn about the company.

The ‘Our Businesses‘ section of BX’s website has a menu of the areas in which BX invests.

The ‘Press Releases Archives‘ section of BX’s website provides an indication of just how active BX has been of late.

Financials

Q4 and FY2024 Results

The most recent results are accessible in the Press Release and Earnings Presentation and in the accompanying Supplemental Financial Data. In particular, refer to pages 22 – 25 of 43 for a high-level overview of the various funds BX manages.

I also encourage you to listen to Blackstone President Jon Gray discuss Q4 results.

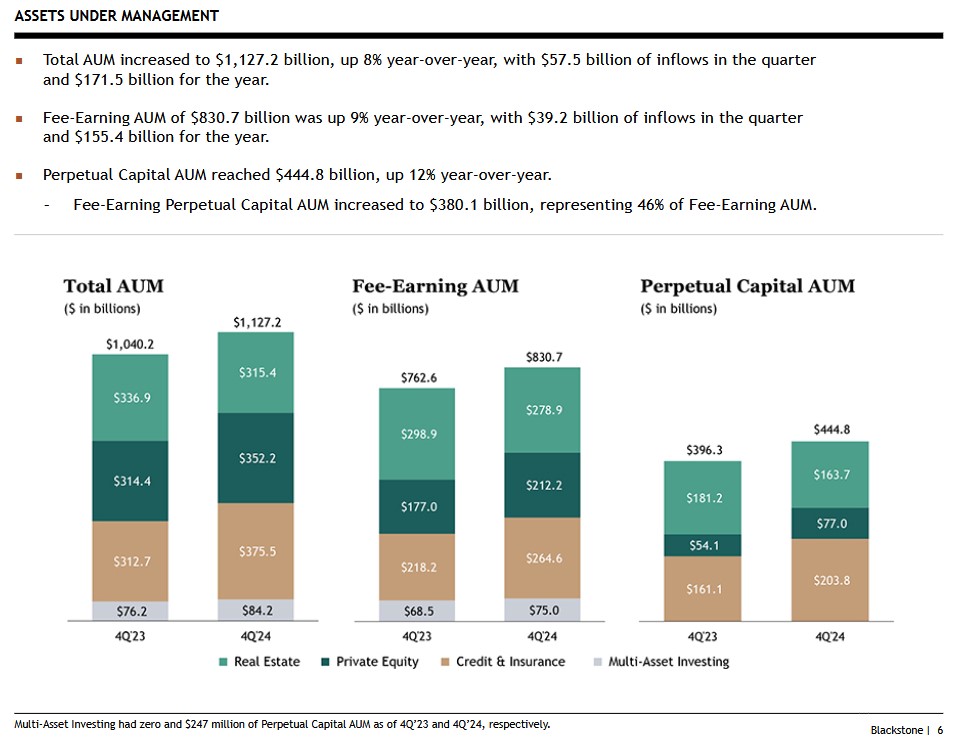

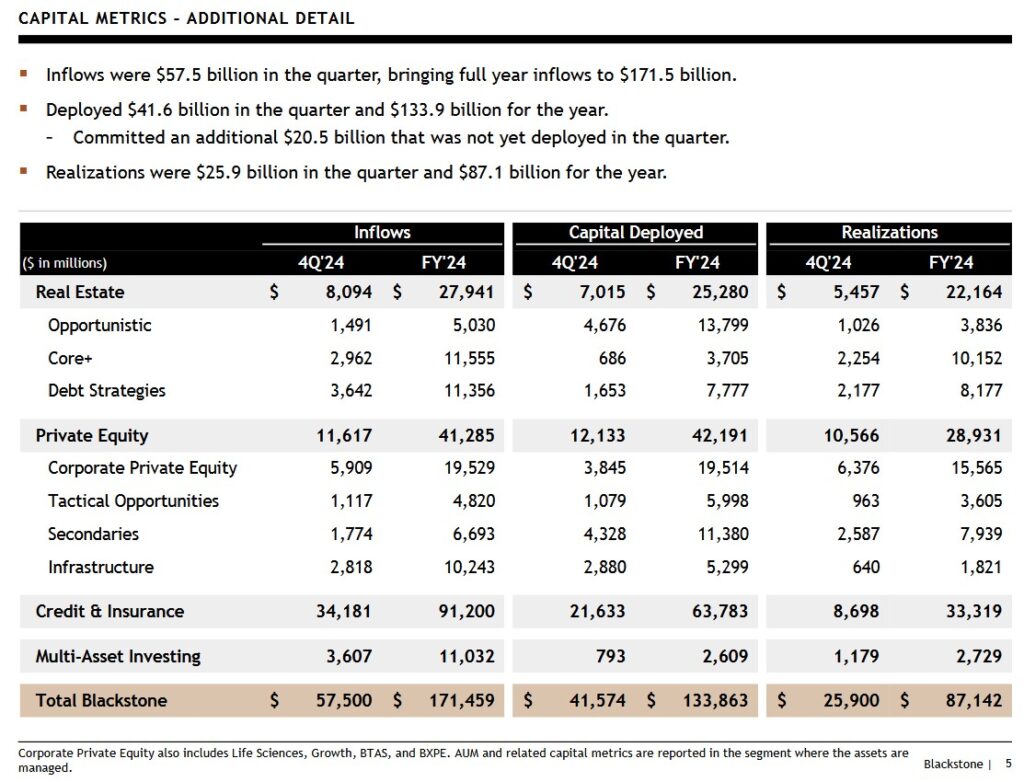

- BX’s Q4 inflows of ~$57.5B compare favorably to its quarterly run rate of ~$38.2B in the prior 8 quarters.

- It also also deployed ~$41.6B in Q4 versus a quarterly run rate of ~$23.1B a quarter over the past couple of years.

- Reported realizations of ~$25.9B were also above its quarterly run rate of ~$17.6B in the previous 8 calendar quarters.

On the Q4 2024 earnings call, Michael Chae (CFO) states:

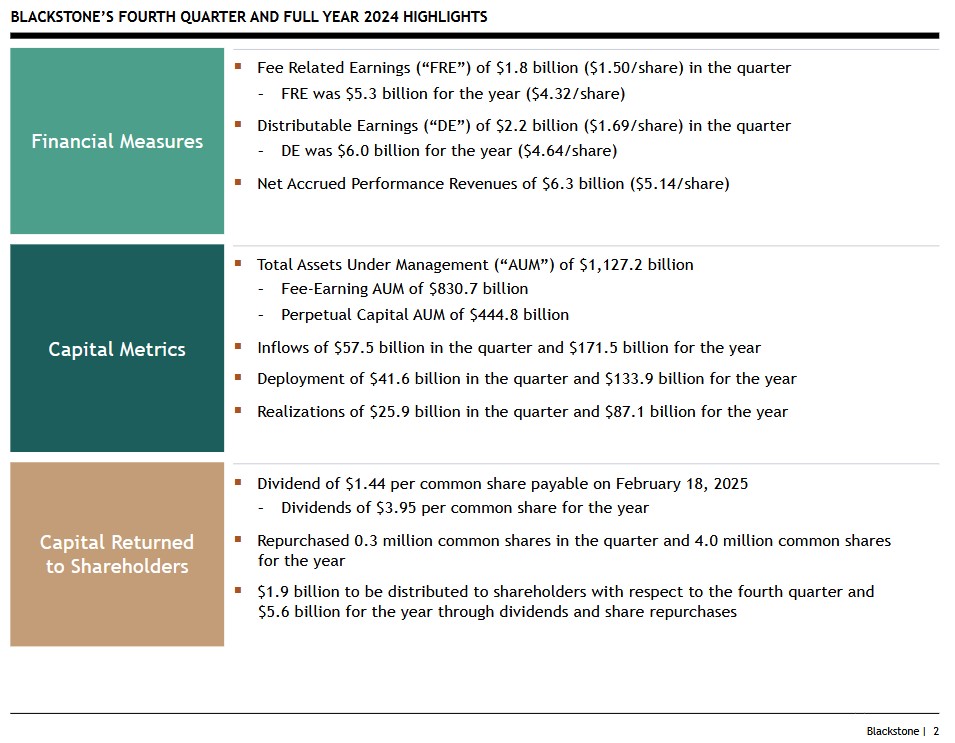

The firm delivered strong results amid a complex external environment in 2024 with robust growth across all key financial and operating metrics. Distributable earnings grew 18% to $6B. Fee-related earnings increased 21% to a full year record of $5.3B. Net realizations rose 12% to $1.4B, supported by the strong performance in BXMA – another example of the benefits of our diverse business mix.

The firm’s expansive breadth of growth engines lifted total AUM up 8% to more than $1.1T, another record, with $171B of inflows for the year. Inflows deployment and overall fund appreciation all accelerated meaningfully in 2024 expanding the foundation of future value. We achieved these results against a backdrop where the market for large-scale realizations was very challenged for much of the year and the significant underlying earnings power of our real estate business has yet to reemerge, reflecting the breadth and power of our platform.

FY2025 Outlook

BX does not provide specific details in its outlook. Michael Chae, however, provided the following on the Q4 earnings call.

In 2025, we will see the full year benefit from funds that were activated throughout 2024.

Our platform and perpetual strategies has continued to expand overall now comprising 46% of the firm’s fee-earning AUM, setting a higher baseline for management fees as we enter 2025.

There is significant underlying momentum in our credit & insurance business segment where FRE and DE grew 26% and 24%, respectively, in 2024 and with robust inflows and record deployment, the business is exceptionally well positioned to deliver strong financial performance again in 2025.

Finally, with respect to realizations, we see a much more constructive environment for realizations in 2025. In the near term, we would expect disposition activity to be concentrated in our private equity strategies, as real estate exit markets strengthen over time and for overall activity levels to be meaningfully higher in the second half of the year. Meanwhile, net accrued performance revenue on the firm’s balance sheet stood at $6.3B at year-end or $5.14 per share. And performance revenue eligible AUM reached a record $561B. These are strong indicators of our future realization potential.

Risk Assessment

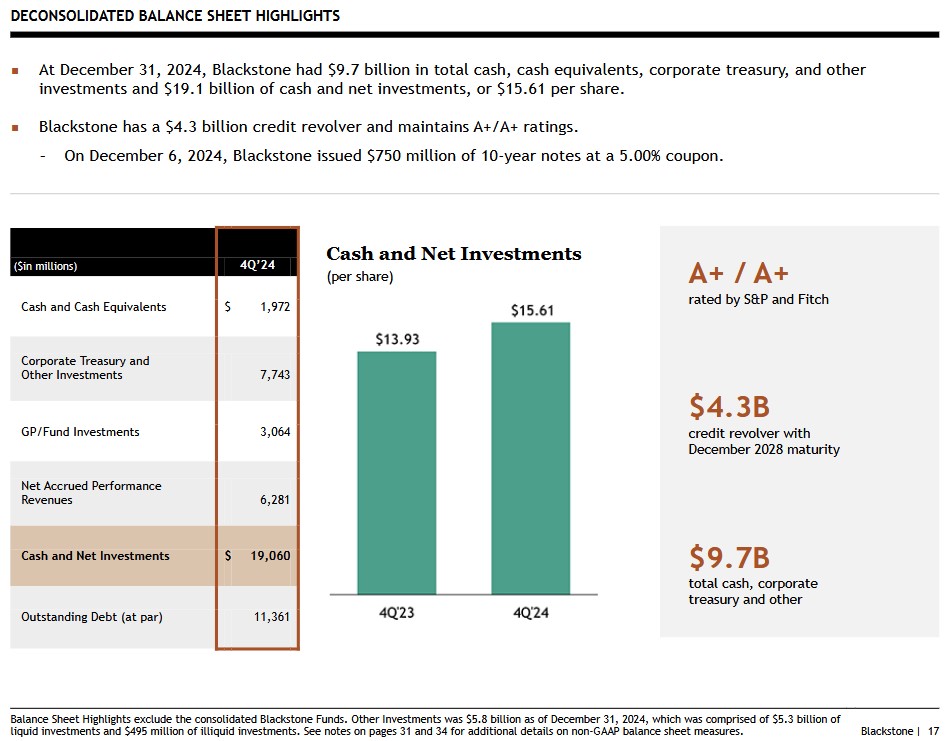

BX’s senior unsecured domestic long-term debt ratings are at the top of the upper-medium-grade investment-grade tier. There is no change from prior reviews.

- S&P Global assigns an A+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch assigns an A+ long-term unsecured debt credit rating with a stable outlook;

These ratings define BX as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

These are BX’s deconsolidated Balance Sheet highlights for Q4 2024.

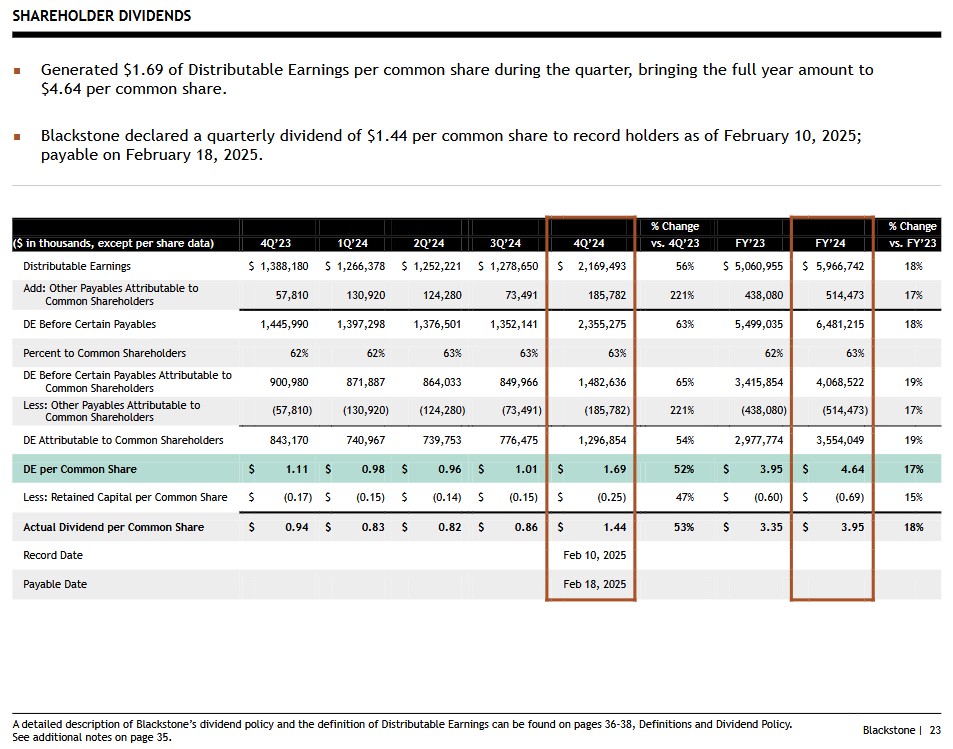

Dividends and Share Repurchases

Dividend and Dividend Yield

The next distribution of $1.44 is payable on February 18. I will initially incur a 15% dividend withholding tax. At a later date, however, BX may divide this amount between a qualified dividend and a ROC.

BX’s quarterly distributions are unconventional and fluctuate depending on DE. The distribution policy states:

‘We intend to pay to holders of common stock a quarterly dividend representing approximately 85% of The Blackstone Group Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to shareholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.’

I do not calculate BX’s forward dividend yield because the quarterly dividend is unpredictable.

I look at an investment’s total potential long-term return perspective (capital gains and dividend income). Inconsistency in BX’s quarterly dividend, therefore, is irrelevant for my purposes.

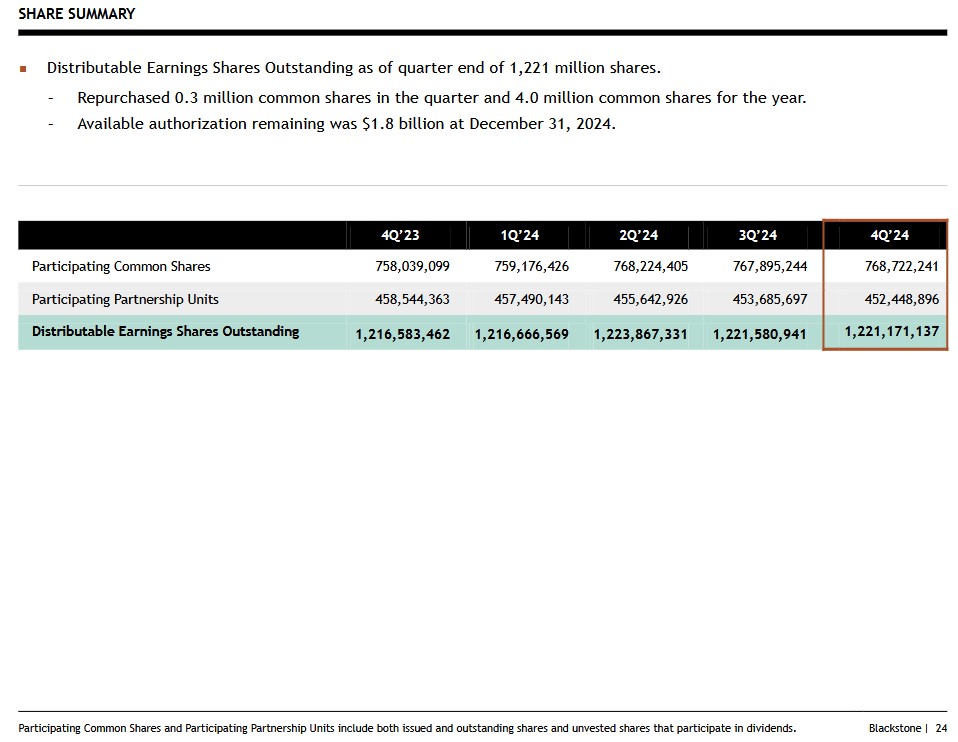

Share Repurchases

BX focuses heavily on optimizing its capital allocation. The extent to which it repurchases shares depends on whether there is a meaningful deterioration in BX’s share price relative to the true underlying value.

Valuation

I typically look at:

- diluted EPS – P/E;

- adjusted diluted EPS – adjusted P/E; and

- Free Cash Flow (FCF) – P/FCF

metrics to gauge the valuation of most companies I analyze. These metrics, however, are of little relevance when trying to assess BX’s performance and outlook.

BX uses DE and FRE to more accurately measure its performance. Definitions for these, and other terms, are within the FY2023 Form 10-K.

The very manner in which BX operates makes it virtually impossible to forecast these metrics. This explains why BX does not provide guidance.

BX is not easy to value because it raises large pools of capital from clients for deployment thus resulting in multiple multi-billion-dollar acquisitions annually. Because it continually makes sizable acquisitions or divestitures, earnings estimates can quickly become outdated.

Some of the assets are meant to be perpetual holdings. In other cases, BX uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs. It is not, therefore, unusual to see wide swings in YoY GAAP results.

I expect fluctuations in quarterly FRE and DE. My interest, however, lies in the long-term trend of these two metrics. I, therefore, like to compare annual FRE and DE over several years.

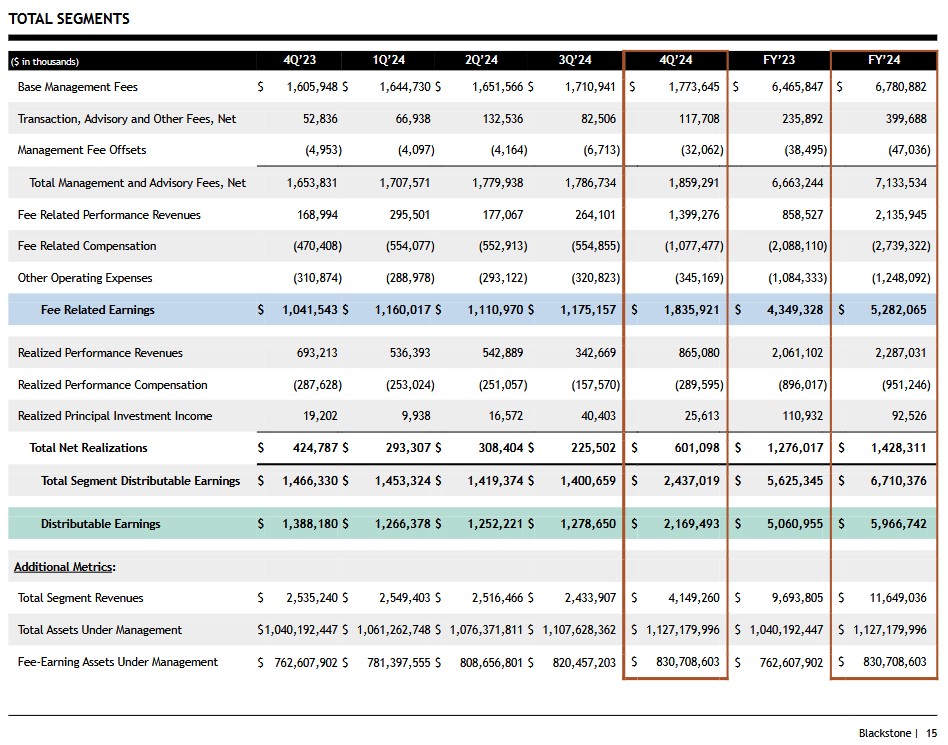

When we compare BX’s DE and FRE for FYE 2017 – FY2024 and the most two recent quarters, we see a noticeable increase over the years. At December 31, 2016, for example, BX had $366.6B of AUM. At FYE2024 it had $1,127.2B! As AUM grows, it stands to reason that DE and FRE should also grow over the very long-term.

Naturally, DE and FRE will fluctuate depending on market/economic conditions. If conditions are not conducive to the immediate sale of certain assets, BX may elect to continue to manage the AUM until such time as conditions improve.

Final Thoughts

I last made an outright purchase on May 9, 2023 @ ~$81.65. All additions to my BX exposure subsequent to that purchase are by way of the automatic reinvestment of the quarterly distributions.

I currently hold 1,511 BX shares in a ‘Core’ account in the FFJ Portfolio. It was my 11th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review and my 8th largest holding when I completed my 2024 Year End FFJ Portfolio Review. I would now own roughly 16 – 20 more shares had the 2024 distributions been properly allocated at the outset.

BX’s recent results point to 2025 being a better year for fundraising, deployments, and realizations. Management’s expectations are for the second half of the year to be better than the first.

Their outlook includes a material step-up in fee-related earnings in 2025. This is due, in part, to the end of fee holidays on certain flagship products. Furthermore, the expectation is for a recovery in the commercial real estate market as new construction has declined substantially and the cost of capital is improving.

My exposure will increase slightly following the automatic reinvestment of the February 18 distribution. I also intend to acquire additional shares at some point but am currently in no rush to do so.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BX, BLK, BAM.to, and BN.to.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.