![]()

Enbridge Inc. (ENB) is a leading North American energy infrastructure company.

It operates in a highly regulated environment where pipeline capacity remains constrained due to lack of new infrastructure.

Investor sentiment currently appears to be negative and I expect investor sentiment will change in the future which will lead to an increase in ENB’s earnings multiples.

On the basis of my analysis, I have acquired additional ENB shares.

Summary

- ENB is currently attractively valued.

- The company has a high quality broad network of midstream assets which are geographically diversified.

- The barriers to entry are high as a result of the regulated nature of the major pipeline and gas utility assets and new pipeline projects often get delayed or cancelled.

- ENB’s assets will likely become increasingly scarce over time which should result in an increase in value going forward.

- ENB has an enviable dividend track record and strong Distributable Cash Flow per Share (DCF) should permit ENB to continue to reward investors with attractive dividend growth.

Introduction

This article discloses a recent purchase made by my daughter and her boyfriend who have embarked on their journey to create financial freedom.

The current euphoria around FAANG companies (Facebook, Amazon, Apple, Netflix, and Alphabet (fka Google) and SMART companies (Square, Match, Alteryx, Roku, and Trade Desk) and the behavior of many retail investors reminds me of the dot.com bubble.

Here are some recent articles which give me reasons to be concerned about the current investing environment.

https://www.google.ca/amp/s/www.nytimes.com/2020/07/08/technology/robinhood-risky-trading.amp.html

FAANG companies are certainly formidable and some of the SMART companies might thrive over the long-term. My concern, however, is the level of euphoria around these companies which leads me to believe investing in them at this juncture is a risky proposition. I cannot, in good conscience encourage my daughter and her boyfriend to invest in these ‘high fliers’. I do, however, want them to invest for the long-term and for this reason shares were recently acquired in attractively valued Enbridge Inc. (ENB).

Industry Overview

The energy industry is highly regulated. New pipelines under consideration, for example, must contend with onerous environmental and other permitting issues. New pipeline projects get caught up in political gamesmanship and this often results in many project delays and cancellations. This should continue to result in an increase in the value of current pipeline assets because pipeline capacity will likely become increasingly scarce as we move forward.

Pipelines are approved by regulators (Federal Energy Regulatory Commission, National Energy Board, and at the state, provincial, and local levels for cross-border Canadian pipelines) only when there is an economic need and pipeline development takes 3+ years.

Project economics are locked in through long-term contracts with producers before breaking ground on the project. As a result, if contracts cannot be secured, a pipeline will not be built.

Contract quality is primarily assessed by term, with long-term contracts (10+ years) being preferred with take-or-pay provisions. Contract quality does not directly support efficiency but rather speaks to the sustainability of future excess returns.

Companies which are primarily oriented around pipelines are the strongest positioned as they obtain the longest terms contracts which tend to be made up mostly of capacity reservation fees and a more modest transportation fee. Although shippers are obligated to use the pipeline, they are not required to do so. They must, however, pay the reservation charges which essentially ensure rents for the pipelines.

The smaller transportation fees are only paid based on actual volumes shipped.

The complexity of developing new pipeline projects in North America is borne out by the fact that earlier this month:

- a U.S. judge ordered the Dakota Access pipeline to be shut down and emptied while it awaits an environmental review;

- the U.S. Supreme Court upheld a lower court decision blocking a permit needed by TC Energy Corp. to continue construction south of the border on its long-delayed Keystone XL pipeline project.

Both these recent announcements followed the outright cancellation of the US$8B Atlantic Coast Pipeline by Dominion Energy Inc. and Duke Energy Corp..

Interestingly, Dominion Energy Inc. and ENB are top competitors and just recently, Berskshire Hathaway Inc. announced that through Berkshire Hathaway Energy it had executed a definitive agreement to acquire Dominion Energy’s natural gas transmission and storage business for ~US$9.7B. Clearly, Buffett and his team view this industry as attractive.

Business Overview

ENB is a leading North American energy infrastructure company. Its core businesses include:

- Liquids Pipelines which transports ~25% of the crude oil produced in North America;

- Gas Transmission and Midstream which transports ~20% of the natural gas consumed in the United States;

- Gas Distribution and Storage which serves ~3.8 million retail customers in Ontario and Quebec;

- Renewable Power Generation which generates ~1,750 megawatts (MW) of net renewable power in North America and Europe.

A comprehensive overview of ENB’s business can be found in its most recent 10-K. Further information is provided in this investment community presentation.

As a midstream company, ENB processes, transports, and stores natural gas, natural gas liquids, crude oil, and refined products. While there are several ways in which a midstream Company can build moats, efficient scale is the dominant source.

Hydrocarbons are produced and consumed in different places and in different forms from the manner in which they are extracted from the ground. Midstream firms transport and process hydrocarbons and once a transport route is established, there is usually little need to build a competing route because to build a competing route would lower returns for both routes below the cost of capital. As a result, pipelines are viewed as businesses with wide moats because they efficiently serve markets of limited size.

In addition to its midstream portfolio, Enbridge has diversified its business in recent years. It operates regulated natural gas utilities and Canada’s largest gas distribution company that serves residential, commercial, and industrial customers in Ontario and upstate New York.

Regulated returns on equity (ROE) on the gas utility and gas distribution assets consistently exceed 10% compared with the 9.6% average allowed ROE for U.S. utilities. ENB’s utilities provide additional attractive assets to the portfolio that exceeds the company’s cost of capital and generate higher returns than its U.S. counterparts.

Q1 2020 Financial Results

ENB’s Q1 2020 results can be accessed here; Q2 results are scheduled to be released July 29th.

GAAP earnings attributable to common shareholders for Q1 decreased by $3.32B or $1.65/ share compared with Q1 2019. The period-over-period comparability of earnings attributable to common shareholders was impacted by certain unusual, infrequent factors or other non-operating factors, including a non-cash impairment of ENB’s investment in DCP Midstream of $1.736B and non-cash unrealized derivative fair value losses of $1.956B.

While GAAP earnings were impacted by sizable non-cash impairment charges, we see that ENB’s distributable cash flow (DCF) per share remains relatively steady and strong.

Virtually all of ENB’s cash flows are driven by market pull, with direct connections to end use markets. In fact, 95% of ENB’s customers are investment grade with strong balance sheets. Another attractive feature is that it has conservative financial policies which reflect low business risk and the stability and predictability of cash flow.

Looking at the highlights of Q1 (page 4 of 31) we see that ENB continued with disciplined capital allocation. It sold $0.4B of assets (the sale of the Montana-Alberta Tie Line and the Ozark Gas system) at very good valuations and also announced on May 7th that it is selling to CPPIB 49% of its 50% equity interest in three French offshore wind projects which are in development.

ENB also reduced 2020 costs by $0.3B which includes salary rollbacks across all levels of the organization.

In addition, it boosted excess liquidity by $5B to $14B to provide a larger buffer in case debt capital markets shut down for an extended period. ENB also expects ~ $1B of capital expenditures to be deferred to FY2021.

On the Q1 conference call with analysts, senior management reaffirmed its financial guidance range for 2020 DCF per share of $4.50 – $4.80/share.

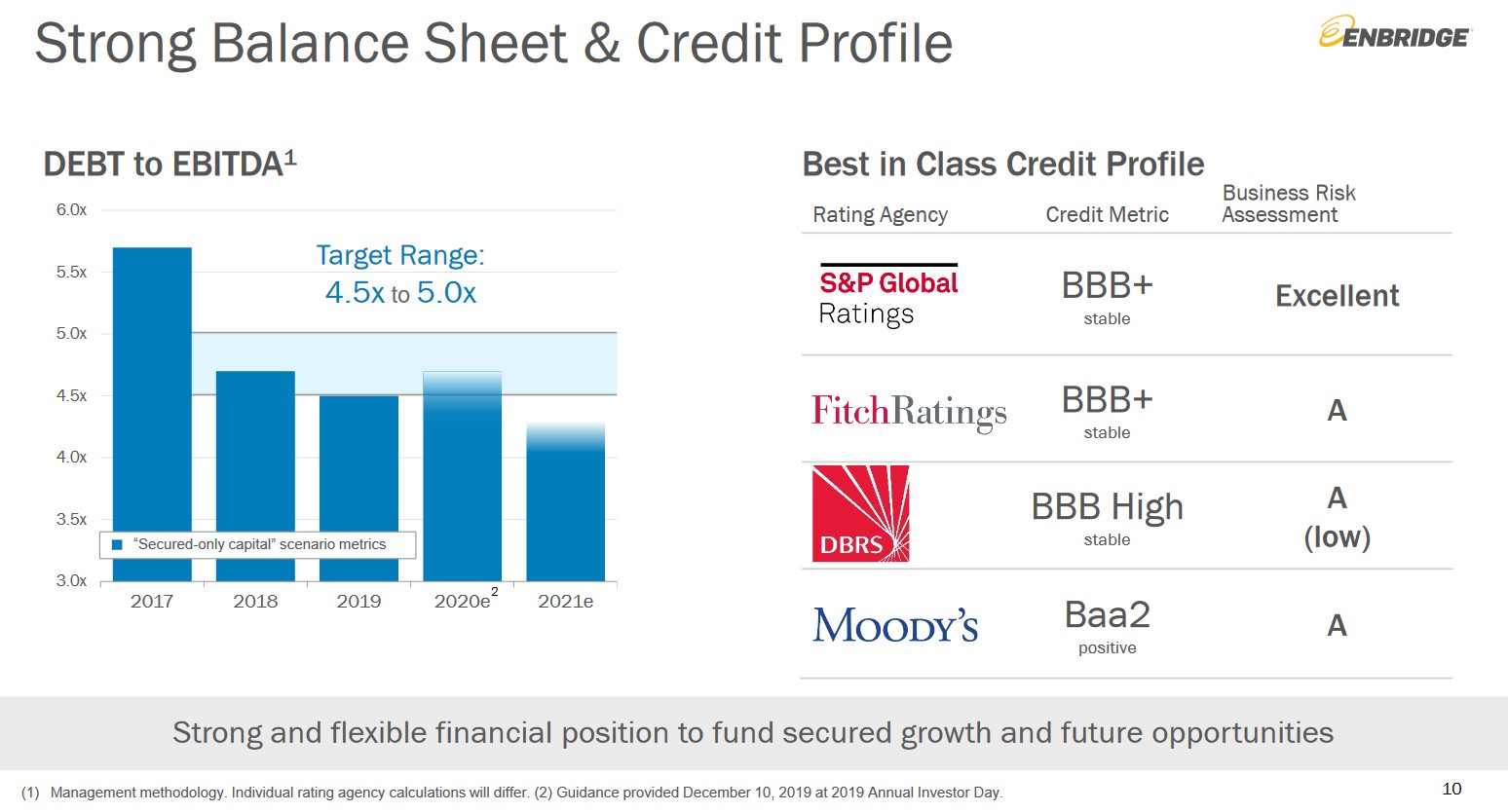

Credit Ratings

ENB’s credit ratings from 4 ratings agencies can be found below.

The ratings from all agencies, except Moody’s, are the top tier of the ‘lower medium grade’ category. Moody’s rating is the middle tier of the ‘lower medium grade’ category.

Source: ENB – June 2020 Investment Community Presentation

All ratings are acceptable for my purposes.

Dividend and Dividend Yield

Details about ENB’s dividend track record can be found here.

I expect ENB’s next two quarterly dividend payments will remain at $0.81/share. On the basis of an annual $3.24 dividend and the current stock price of ~$40, investors receive a ~8.1% dividend yield.

The $3.24 in dividend payments investors can expect to receive in FY2020 is ~67.5% – ~72% of projected 2020 DCF per share of $4.50 – $4.80/share. This exceeds ENB’s conservative <65% dividend payout ratio target but I am fully confident ENB’s dividend is not at risk.

Valuation

I expect pipeline capacity to become increasingly scarce over time given the significant challenges in obtaining all the appropriate approvals to build new pipelines. This suggests to me there is more contract certainty with existing pipeline assets because volumes will be high since there are no competing alternatives. So, if ENB’s cash flows become more certain, I would expect investors might be willing to pay up to invest in ENB.

While Earnings per Share (EPS) are certainly an important metric, we see from investor presentations and analyst conference calls that DCF per share is the metric on which management focuses.

With shares trading at ~$40 and management targeting $4.50 – $4.80/DCF per share we get a forward Price/DCF range of ~8.33 – ~8.88 which is superior to the levels reflected in my February 18, 2019 article.

On a forward adjusted EPS basis, the consensus mean estimate from 18 brokers is $2.47 with estimates ranging from $1.59 – $2.73. Using the current ~$40 stock price and the consensus mean forward adjusted EPS estimate we arrive at a forward adjusted PE of ~16.19.

I view ENB’s current valuation as attractive.

Final Thoughts

In an environment where pipeline capacity remains constrained due to lack of new infrastructure, I expect pipeline companies will have the upper hand during re-contracting negotiations; it comes down to law of supply and demand. If there is limited pipeline capacity then energy producers will have to increasingly compete for limited access thus placing ENB in an enviable position.

Investor sentiment currently appears to be negative and I do not expect earnings multiples to contract much further. In fact, I expect investor sentiment will change in the future which will lead to an increase in ENB’s earnings multiples.

I also view ENB’s current dividend yield as attractive and am of the opinion ENB’s cash flows are very durable.

I recommend ENB as an investment if you want:

- exposure to a high quality broad network of midstream assets which are geographically diversified;

- stable cash flow and high barriers to entry as a result of the regulated nature of the major pipeline and gas utility assets;

- a strong probability of continued annual dividend growth.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long ENB.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.