Companies with an investor base that expects annual dividend increases are, in my opinion, trapped and should be avoided. Emerson Electric (EMR), a Dividend King because it has consistently increased its annual dividend for at least 50 consecutive years, is a good example.

I suspect many of us have investment holdings we rarely/never look at. EMR is one such holding.

In preparation for this post, I had to hunt through records to determine when I initiated an EMR position. Lo and behold, I acquired several hundred shares on July 2, 2009 @ ~$32.15/share – very shortly after the Great Financial Crisis. I added to my exposure on July 20, 2015 @ ~$52.55 and on September 16, 2016 @ ~$51.07. My exposure has also increased by way of the automatic reinvestment of the dividend income.

As I compose this post on November 24, shares trade at ~$130.

As a testament to how little attention I pay to EMR, I have only written about this holding in posts dated February 8, 2017, November 8, 2017, and in my June 17, 2021 guest post at Dividend Power. Had I not been asked to write the 2021 guest post, I would not have even looked at this holding. These posts are accessible through the Archives.

The reason I have decided to revisit this existing holding is because my wife and I must withdraw funds from our retirement accounts in 2025; this is part of our Registered Retirement Savings Plan (RRSP) meltdown strategy. As explained in prior posts, it is essential we withdraw funds from these accounts prior to the mandatory date by which the funds in these accounts get converted to Registered Retirement Income Funds (RRIFs). Unless we do this, the annual RRIF withdrawals will be taxed at the highest personal tax rate during our retirement years.

Although EMR has a stock calculator page on its website, I prefer to use this site when assessing the annual total rate of return over various time frames.

In several posts I stress the importance of acquiring shares at attractive valuations. Depending on the holding period, we can readily see that the returns from an EMR investment vary significantly!

Had I sold our EMR shares in late March 2020 when the world shut down because of COVID, my average annual total rate of return would have been ~7%. Applying the Rule of 72, it would have taken just over a decade to double my investment.

Since I have never sold any EMR shares, the annual total rate of return using my initial investment date is ~12.73%; I have been reinvesting the dividend income. Applying the Rule of 72 and my investment doubled in ~5.7 years. Had I not reinvested the dividends, the rate of return would be just shy of 11%.

In hindsight, I should have deployed funds used to acquire EMR shares toward other much larger holdings which have generated far superior returns.

The past, however, is the past. I am more interested in trying to determine how EMR is likely to perform going forward.

Business Overview

The best sources of information to learn about the company are EMR’s website and the FY2024 Form 10-K.

Details of recent acquisitions/divestitures is found at the beginning of Part 1 Item 1 – Business in the FY2024 Form 10-K commencing on page 3 of 152.

The company operates in a highly competitive and highly regulated market.

Its total backlog at the end of FY2024 was $8.448B versus $7.773B at FYE2023.

Aspen Technology Acquisition

In May 2022, EMR closed the combination of its industrial software businesses with AspenTech to create a global industrial software leader. With the close of this transaction, EMR owned 55% of new AspenTech on a fully diluted basis and AspenTech shareholders owned the remaining 45%.

On November 5, 2024, EMR announced it had made a proposal to acquire all outstanding shares of common stock of AspenTech and that it had commenced a process to explore strategic alternatives, including a cash sale, for the Safety & Productivity segment.

A presentation that accompanied this November 2024 announcement is accessible here.

National Instruments Corp Acquisition

In May 2022, EMR initially offered $48 to acquire National Instruments Corp. (NI), a test-and-measurement company. This initial approach kicked off 8 months of stonewalling before NI started a strategic review in January 2023.

After a prolonged bidding process EMR finally ending up acquiring NI for $60/share, or $8.2B in October 2023. Technically, EMR’s effective cost is $59.61/share because it bought 2.3 million shares of NI at much lower prices to try to force NI to come to the negotiating table.

What EMR identified in NI was the resiliency of the chunk of sales to life-sciences and research organizations customers; the life-sciences and university customers accounted for ~31% of NI’s sales. EMR’s management also identified growth opportunities in semiconductors and electric vehicles.

Funding for the bulk of this acquisition came from the ~$8B in after tax proceeds from the sale of a majority stake in EMR’s climate-technologies division to Blackstone (BX).

Financials

Q4 and FY2024 Results

Details of EMR’s Q4 and FY2024 results are accessible here.

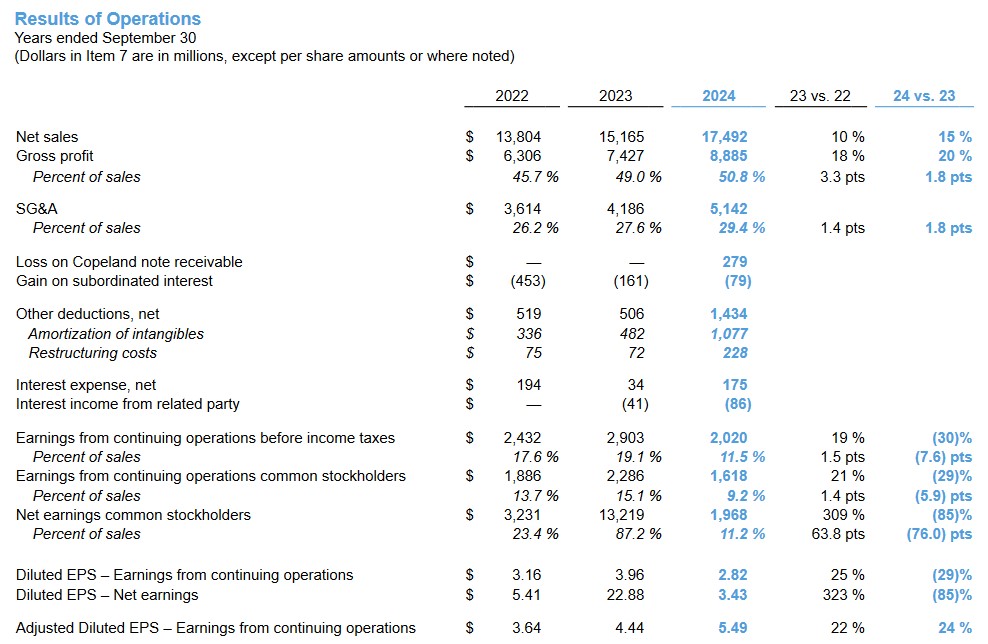

The following is a snapshot of EMR’s results of operations in FY2022 – FY2024. The surge in FY2023 diluted EPS is attributed to earnings of $18.92/share from discontinued operations (the climate-technologies division sold to Blackstone).

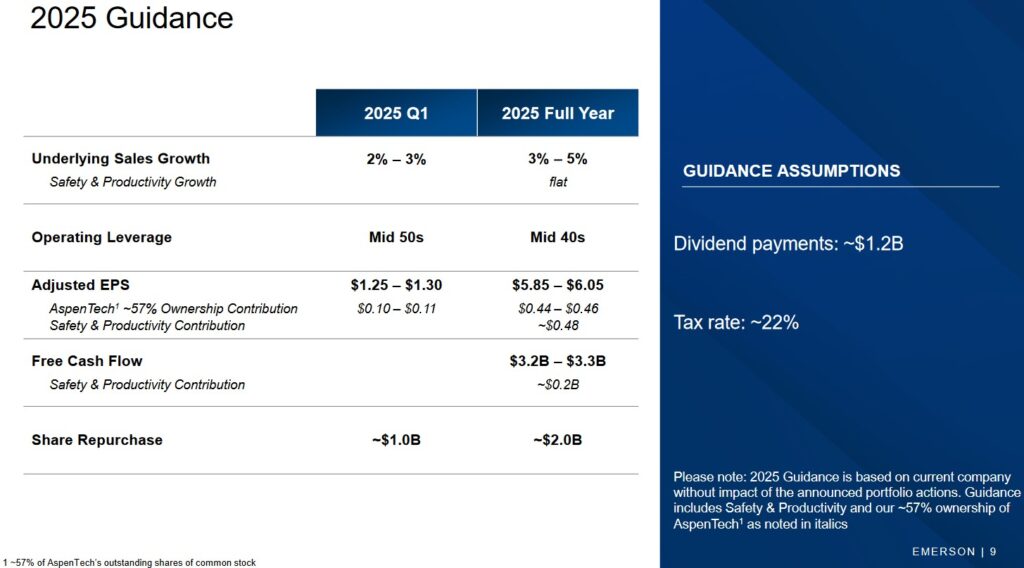

Q1 2025 and FY2025 Guidance

EMR’s guidance is as follows.

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

In my most recent Copart post, I explain why I have decided to deduct stock based compensation (SBC) when calculating a company’s Free Cash Flow (FCF).

Using EMR as an example, we see on page 70 of 152 in the FY2024 Form 10-K the exercise of employee stock options in the $50s.

Go to page 17 of 152 in the FY2024 Form 10-K. In Q4 of FY2024, EMR repurchased over 2.5 million shares at an average price of $103.04! How is this fair to EMR shareholders?

If EMR were to eliminate the granting of stock options, you would think that it would need to increase salaries/wages to retain its employees. This would be picked up in the Consolidated Statements of Earnings. The ‘costs’ associated with the SBC, however, are not reflected thus boosting EMR’s earnings.

Looking at EMR’s Consolidated Statements of Cash Flows for the FY2019 – FY2021 time frame we see OCF (in billions of $) of 3.006, 3.083, and 3.575.

In FY2022 – FY2024, OCF from continuing operations was 2.048, 2.71, and 3.317. If we include cash from discontinued operations of 0.874, (2.073), and 15, we get cash provided by operating activities of 2.922, 0.637, and 3.332.

For my FCF calculations, I will use OCF from continuing operations.

If we deduct SBC in FY2019 – FY2024 (0.120, 0.110, 0.224, 0.125, 0.25, and 0.26), OCF from continuing operations drops to 2.886, 2.973, 3.351, 1.923, 2.46, and 3.057.

CAPEX was (in billions of $) 0.594, 0.538, 0.581, 0.299, 0.363, and 0.419.

Deduct CAPEX from OCF and we get FCF (in billions of $) of 2.292, 2.435, 2.77, 1.624, 2.097, and 2.638.

In contrast, some online sources reflect EMR’s FCF as being (in billions of $) 2.56, 2.40, 2.79, 2.91, 2.55, and 2.913. The bulk of the variance between my calculations and those reflected in some online sources is because I exclude SBC and exclude cash from discontinued operations to arrive at EMR’s OCF.

Risk Assessment

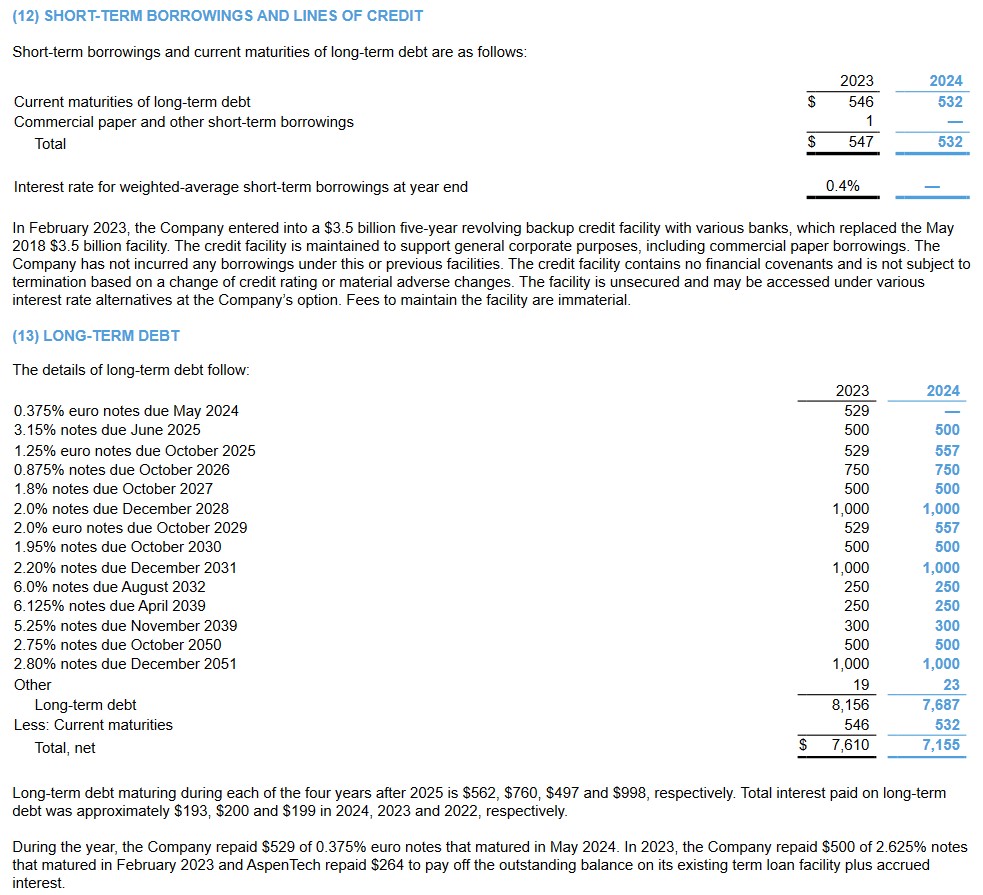

The following table is found in EMR’s FY2024 Form 10-K. We see from the note below the schedule of long-term debt that EMR has $2.817B of low interest debt maturing after 2025.

Should EMR undertake further acquisitions, the interest rates associated with any acquisition related debt is unlikely to be at sub 2% rates.

In the 1990s, EMR’s domestic unsecured long-term debt was assigned a AAA rating by Moody’s. Over the years, the rating was downgraded and by February 2002, an A2 rating was assigned and it has remained unchanged since then.

S&P Global also downgraded EMR’s domestic unsecured long-term debt over the years and in February 2002, an A rating was assigned and has remained at this level.

Both ratings are the middle tier of the upper medium grade investment grade category. These ratings define EMR as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

EMR’s credit risk is acceptable for my purposes.

Dividends and Share Repurchases

Dividend and Dividend Yield

Some investors fixate on dividend metrics. In my opinion, this is extremely short-sighted. Investors would be far better off looking at how a company deploys its capital; annual dividend increases are not necessarily always the best use of funds.

EMR is a Dividend King meaning it has increased its dividend annually for at least 50 consecutive years. Looking at the dividend history, however, it is readily apparent that some of these annual increases are negligible. EMR is clearly desperate to keep its track record intact!

The most recent quarterly dividend increase was $0.0025 ($0.5275 increased from $0.525). There are other instances in recent years where the dividend increases are also negligible.

This is what happens when a company’s dividend policy creates a shareholder base fixated on dividend metrics. EMR has essentially trapped itself. If EMR were to announce the temporary suspension of dividend increases, its shareholder base would revolt and the share price would likely plunge.

Share Repurchases

The weighted average diluted shares outstanding in FY2010 and FY2024 were 757 million and 574 million respectively.

In FY2019- FY2024, EMR repurchased shares in the amount of (in billions of $) 1.25, 0.942, 0.5, 0.5, 2.0, and 0.435. During the same period, SBC was (in billions of $) 0.12, 0.11, 0.224, 0.125, 0.25, 0.26.

In addition, we know that EMR distributed (in billions of $) 1.209, 1.209, 1.21, 1.223, 1.198, and 1.201 of dividends during this time frame. EMR shares have been undervalued roughly 100% of the time between 2109 – 2024. Imagine if EMR had had the flexibility to repurchase undervalued shares to the tune of ~$7.2B instead of being committed to distributing dividends. If it had been able to repurchase shares at an average price of $90 during this period, the weighted average diluted shares outstanding would likely be under 500 million ($7.2B – $90/share = 80 million shares). This is certainly not an exact calculation but we see the ramifications of being captive to a dividend policy.

EMR’s Q1 and FY2025 guidance now calls for share repurchases to the tune of $1B in Q1 and $2B in FY2025. These repurchase plans are aggressive relative to repurchases in recent years. You would think it would have made a whole lot more sense to aggressively repurchase shares when they were grossly undervalued during the 2021 – 2023 period.

Now? EMR’s shares are currently overvalued and it wants to aggressively repurchase shares?

Valuation

When I analyzed EMR in my June 17, 2021 guest post at Dividend Power, I noted that management’s FY2021 guidance was diluted GAAP EPS of $3.55 – $3.65 and adjusted diluted EPS of $3.85 – $3.95. Management was also targeting $4.75 – $5.00 of adjusted diluted EPS for FY2023.

At the time of that post, EMR’s share price was ~$97.50. Using management’s FY2021 guidance, the forward diluted PE was ~26.7 – ~27.5 and the forward adjusted diluted PE was ~24.7 – ~25.3.

EMR regularly acquires and divests so I anticipated that EMR in 2-3 years would be somewhat different than EMR in 2021. I, therefore, placed minimal reliance on management’s FY2023 adjusted diluted earnings target to gauge the company’s valuation.

So, how did EMR do relative to this FY2021 guidance? It generated $3.82 of GAAP diluted EPS and $4.10 of adjusted diluted EPS in FY2021.

How did EMR perform relative to management’s FY2023 adjusted diluted EPS target? It generated $3.72 of GAAP EPS and $4.44 of adjusted diluted EPS. That is well short of management’s target.

Clearly, much can happen over time. The further out on the calendar we go, the greater the probability actual results will differ from estimates. This is why I am very reluctant to complete discounted cash flow forecasts. You can arrive at very different results depending on the input metrics. How anyone can rely on DCF calculations using input 10+ years into the future has always puzzled me!

Fast forward to almost 3.5 years after that June 17, 2021 guest post and the share price is currently ~$130. Management’s FY2025 adjusted diluted EPS guidance is $5.85 – $6.05 thus giving us a forward adjusted diluted PE of ~21.5 – ~22.2.

Using the following forward-adjusted diluted EPS broker estimates, EMR’s forward adjusted diluted PE levels are:

- FY2025 – 20 brokers – ~21.8 using the mean of $5.96 and low/high of $5.86 – $6.15.

- FY2026 – 18 brokers – ~20.4 using the mean of $6.38 and low/high of $4.82 – $6.70.

- FY2027 – 6 brokers – ~18.5 using the mean of $7.04 and low/high of $6.67 – $7.30.

Earnings can be more easily manipulated than cash flow which is why I also gauge a company’s valuation based on its cash flow.

Management’s FY2025 FCF forecast is $3.2B – $3.3B. We should, however, deduct SBC. If the SBC in FY2025 is comparable to the $0.26B in FY2024, the FCF forecast becomes $2.94B – $3.04B.

The diluted weighted average shares outstanding in FY2024 was 574 million. EMR intends to repurchase $1B and $2B of its shares in Q1 and FY2025. Let’s be generous and estimate that the diluted weighted average shares outstanding in FY2025 will drop to 572 million. Take the $2.99B mid-point of the FY2025 FCF forecast of $2.94B – $3.04B and divide this by 572 million shares. We get FCF/share of ~$5.23. Divide the current ~$130 share price by ~$5.23 and we get a P/FCF estimate of ~24.9.

Based on EMR’s track record and outlook and the current euphoric market conditions, I think shares are currently slightly overvalued.

Final Thoughts

In my opinion, Emerson Electric is a trapped Dividend King. Having increased its dividend for 67 consecutive years, the investor base has come to expect an annual dividend increase. Dividend distributions, however, are not necessarily the most efficient form of capital allocation.

I say EMR is trapped because if it decides dividend increases are to be a lower capital allocation priority, the investor base will likely be up in arms. It could also lead to some ‘dividend ETFs and funds’ culling their EMR exposure thus putting downward pressure on the company’s share price.

EMR has been in ‘transition’ for the past several years and thus a direct comparison of YoY results is difficult; it has been a bit of a ‘dog’s breakfast’ – much like other major conglomerates such as Honeywell, 3M, United Technologies, and General Electric. Each of these companies operated in several different and unrelated ‘spaces’ which had to compete against each other to receive proper funding to grow. These conglomerates have slowly been unwound (or are in the process of being unwound) thus enabling the ‘spun off’ parts to focus on their ‘core’ business with less ‘red tape’.

Unfortunately, the divestiture of various business lines is disruptive as a considerable level of resources is required to successfully separate from the ‘parent’.

On a positive note, EMR benefits from a reduction in the number of competitors than can adequately address in-demand automation services. It has a large customer base and switching automation equipment suppliers is fraught with risk. As a result, once EMR is embedded in a customer’s processes, the probability is low that a customer will switch to a competitor. This enables EMR to generate higher-margin recurring revenue in the form of maintenance, upgrades, and overhauls; a high percentage of its revenue is derived from aftermarket services.

Having said all this, my EMR exposure is through a retirement account for which I do not disclose details. It has never been a top 30 holding and is not even remotely close to being a top 30 holding.

Although EMR’s credit risk is acceptable, I have several holdings where the risk profile is far superior to that of EMR. The company has a considerable amount of debt maturing over the next few years. While the risk of being unable to meet its obligations is very low, I would much rather invest in debt free/virtually debt free companies whose capital allocation options are not held hostage by the need to maintain a Dividend King status.

Given my plan to reduce the number of holdings, EMR is a strong candidate for sale as part of our RRSP meltdown strategy.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long EMR.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.