In my December 19, 2024 post I disclose initiating a 300 share Cintas (CTAS) position in one of the ‘Side’ accounts in the FFJ Portfolio. I subsequently acquired an additional 200 shares on December 31, 2024 thereby bringing my total exposure to 500 shares.

Although CTAS is in an entirely different industry than Rollins (ROL), another holding in the FFJ Portfolio, there are similarities that appeal to me.

Much like ROL, CTAS is using technology to improve route efficiency/customer service and technician downtime. This video explains how CTAS’s Smart Truck technology provides the company with detailed data to help it refine routing, drive time, and idle time.

Both companies operate in highly fragmented industries. This provides them with the opportunity to grow organically AND through tuck-in acquisitions. On occasion, some acquisitions can be more sizable.

In many instances, tuck-in acquisitions arise when an operator is nearing retirement age. Depending on family dynamics or if the operator has no children interested in participating in the business, the sale of a smaller operation to CTAS may be an ideal ‘exit strategy’.

The location of an acquisition target’s clients relative to CTAS’s existing clients sometimes presents an opportunity to increase route density. Without a significant increase in costs, one technician and one vehicle can generate generate more revenue.

CTAS has several operating facilities. Depending on the location and size of an acquisition, there may be no need for new operating facilities/expansion to existing operating facilities. In certain instances, an acquisition might allow CTAS to bring on additional operating facility capacity.

Furthermore, the addition of new customers presents CTAS with the opportunity to offer a wider breadth of products and services. If, for example, CTAS adds a ‘Work Uniform Service’ client, it creates an opportunity to cross-sell a variety of ‘Facility Services’ (refer to the ‘Solutions’ menu at the top of the company’s website).

Business Overview

Part 1 Item 1 in the FY2024 Form 10-K and the company’s website provide a good overview of the company.

CTAS’s Acquisition Strategy

In FY2022 – FY2024 and the first half of FY2025, CTAS acquired businesses net of cash acquired totaling (in $ Millions) ~$164.2, $46.4, $186.8, and $154.9.

Because of the assumptions used to value the acquired intangible assets, actual results over time could vary from original estimates. Impairment of service contracts and other assets is determined through specific identification. CTAS, however, has recognized $0 impairment for FY2022 – FY2024 and the first half of FY2025. It appears it is disciplined in the price it is prepared to pay for its acquisitions.

CTAS’s acquisitions are not limited to small tuck-in acquisitions. For example, CTAS completed the acquisition of G&K Services for ~$2.2B including acquired net debt in March 2017.

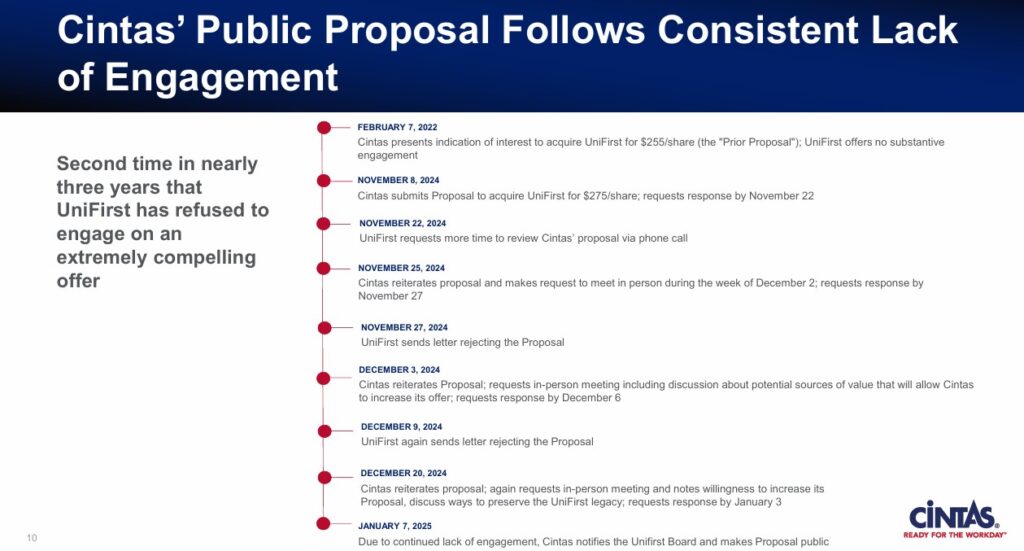

On three occasions, CTAS has endeavored to acquire UniFirst (UNF). In January 2025, CTAS’s most recent offer, was for ~$5.3B.

On March 23, 2025, CTAS terminated its discussions with UNF’s management after being unable to have substantive engagement with UNF regarding key transaction terms.

Financials

Q3 and YTD2025 Results

CTAS’s Q3 and YTD2025 results released on March 26 are accessible through CTAS’s website.

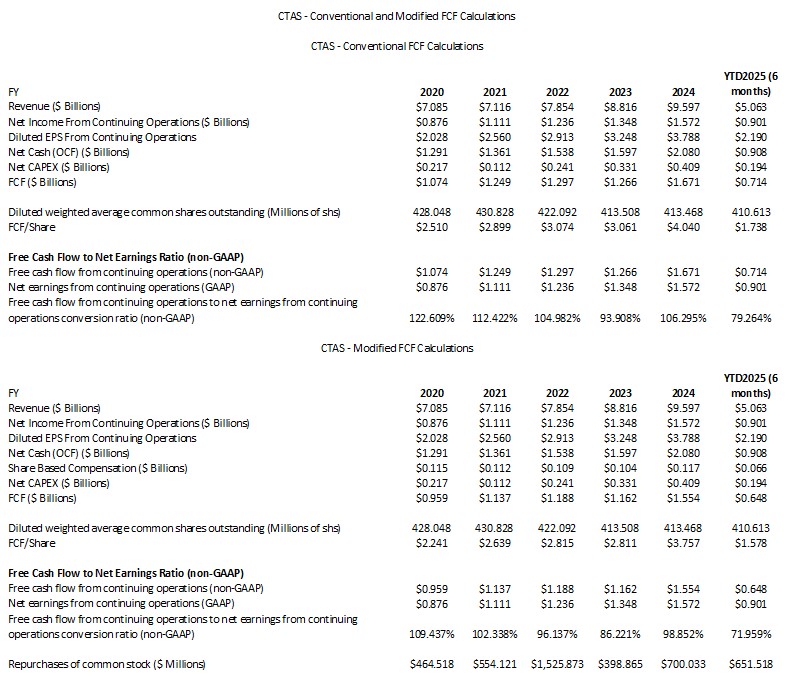

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2020 – YTD2025)

FCF is a non-GAAP measure, and therefore, its method of calculation is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows.

In several posts, I touch upon why investors should deduct share based compensation (SBC) when analyzing a company’s FCF.

At the time of my December 19, 2024 post, I determined CTAS’s FCF as follows using data extracted directly from the Form 10-K filings for FY2020 – FY2024 and the Form 8-K pertaining to Q2 and YTD2025 results.

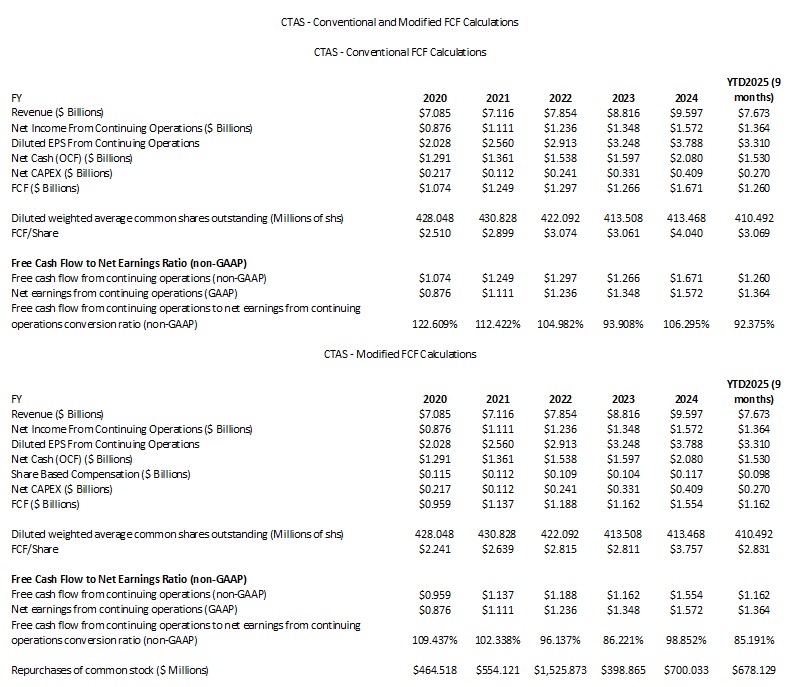

The following is an update using the Q3 and YTD2025 results.

YTD2025 FCF/share falls shy of diluted EPS using the conventional and modified methods of calculation. I anticipate the FY2025 conversion ratio under both methods of calculation will improve by the end of FY2025.

FY2025 Outlook

When CTAS released its Q2 and YTD2025 results, it updated its annual revenue expectations from $10.22B – $10.32B to $10.255B – $10.32B for a total growth rate of 6.9% – 7.5%. The organic growth rate was expected to be 7.0% – 7.7%. Furthermore, the annual adjusted diluted EPS outlook was revised from $4.17 – $4.25 to $4.28 – $4.34 for a growth rate of 12.9% – 14.5%.

With the release of its Q3 and YTD2025 results, CTAS is updating its annual revenue expectations from $10.255B – $10.32B to $10.28B to $10.305B. The $15.0 million reduction at the top of the range reflects the negative impact of the foreign currency exchange rate fluctuations experienced in Q3 and the expected impact for Q4.

The top end of the range for the organic growth rate expectations remains unchanged at 7.7%. The low end of the organic growth rate, however, is being raised from from 7.0% to 7.4%. Although foreign currency exchange rate fluctuations do not impact organic growth rates, they do impact total growth.

CTAS is also raising its diluted EPS guidance from $4.28 – $4.34 to $4.36 – $4.40.

Risk Assessment

At the end of Q2 2025, CTAS had ~$0.631B of debt due within 1 year. The Q2 2025 Form 10-Q was unavailable when I wrote my prior CTAS post. The data from the Q1 2025 Form 10-Q, however, provided information about amounts, the interest rates, and fiscal year maturity of the short- and long-term debt.

At the end of Q3 2025, CTAS had ~$0.45B of debt due within 1 year. The Q3 2025 Form 10-Q is currently unavailable but the data from the Q2 2025 Form 10-Q provides information about amounts, the interest rates, and fiscal year maturity of the short- and long-term debt. The difference between the ~$0.45B outstanding at the end of Q3 and the ~$0.631B outstanding at the end of Q2 is the repayment of ~$0.181B of commercial paper in Q3.

CTAS is scheduled to repay ~$0.45B of senior notes that mature by the end of FY2025 (May 31). The company does not readily have cash and cash equivalents to support this repayment; I envision the use of commercial paper to repay this amount. There is no debt due until fiscal 2027 so using cash provided by operating activities, CTAS should be able to repay any commercial paper advances in FY2026.

CTAS’s domestic senior unsecured long-term debt ratings are:

- Moody’s: A3 with a stable outlook (last reviewed on August 29, 2023)

- S&P Global: A- with a stable outlook (last reviewed on March 10, 2025)

Both ratings are in the bottom tier of the upper medium-grade investment-grade category. These ratings define CTAS as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Dividends and Share Repurchases

Dividend and Dividend Yield

CTAS’s dividend history is accessible here. Please keep in mind that CTAS had a 4:1 stock split in September 2024. This explains why the December 2024 and March 2025 dividends are $0.39 and the September 2024 dividend is $1.56.

Little of CTAS’s total long-term shareholder return is likely to come from the quarterly dividend. I recommend you assign little weight to the dividend as part of your analysis.

Stock Splits and Share Repurchases

CTAS’s stock split history is:

- September 11, 2024: 4:1

- November 18, 1997: 2:1

- April 2, 1992: 2:1

- April 2, 1991: 1.5:1

- April 2, 1987: 2:1

The table provided earlier in this post reflects the dollar value of shares repurchased and the diluted weighted average common shares outstanding in FY2016 – FY2024 and YTD2025.

Valuation

When I last reviewed CTAS in my December 19, 2024 post, CTAS had reported $2.19 of diluted EPS in the first half of FY2025. Using the current ~$183 share price and a conservative FY2025 diluted EPS estimate of ~$4.25 – ~$4.30, the forward diluted PE was ~42.6 – ~43.06.

Management’s revised FY2025 diluted EPS guidance was $4.28 – $4.34 giving us a forward diluted PE of ~42.2 – ~42.8.

Its valuation using broker guidance was:

- FY2025 – 19 brokers – mean of $4.25 and low/high of $4.21 – $4.34. Using the mean, the forward adjusted diluted PE is ~43.06.

- FY2026 – 19 brokers – mean of $4.70 and low/high of $4.54 – $4.92. Using the mean, the forward adjusted diluted PE was ~39.

- FY2027 – 10 brokers – mean of $5.15 and low/high of $4.91 – $5.53. Using the mean, the forward adjusted diluted PE was ~35.5.

I also estimated FCF in the second half of FY2025 would be similar to that of the first half thus giving me a FCF/share of ~$3.44 and ~$3.12 using the conventional and modified methods of calculating FCF. With a ~$183 share price, the P/FCF was ~53.2 and 58.7.

We now know that CTAS has generated $3.31 of diluted EPS in the first 9 months of FY2025. If it generates a comparable amount in Q4, the FY2025 diluted EPS should be ~$4.40 which is the upper end of management’s $4.36 – $4.40 guidance. The share price, however, has risen to ~$206.50 as I finalize this post on the morning of April 2, 2025 thus giving us a forward diluted PE of ~47.

Its valuation using the current broker guidance is:

- FY2025 – 20 brokers – mean of $4.38 and low/high of $4.32 – $4.41. Using the mean, the forward adjusted diluted PE is ~47.1.

- FY2026 – 20 brokers – mean of $4.83 and low/high of $4.69 – $4.94. Using the mean, the forward adjusted diluted PE was ~42.8.

- FY2027 – 12 brokers – mean of $5.31 and low/high of $5.02 – $5.58. Using the mean, the forward adjusted diluted PE was ~38.9.

At the end of Q3, CTAS’s FCF is ~$3.069 and ~$2.831 using the conventional and modified methods of calculating FCF. If it generates a comparable amount of FCF in Q4 as in each of the prior 3 quarters, I estimate CTAS’s FCF calculated using the conventional and modified methods will be ~$4.09 and ~$3.77. Using the current ~$206.50 share price, the forward P/FCF is ~50.5 and ~54.8.

Final Thoughts

CTAS’s valuation based on my FCF estimates is superior to that in December 2024 even though the share price is now ~$25 higher. Using forward EPS estimates, however, the valuation is inferior to that from December. Earnings, however, can more easily be distorted than cash provided by operating activities. I, therefore, I rely more heavily on the P/FCF metric than the P/E metric. Furthermore, I prefer the use of a company’s modified FCF to determine a company’s valuation (see How Stock Based Compensation Distorts Free Cash Flow).

In my previous post, I state the following:

In FY2016, it generated ~$4.8B in revenue and it will likely surpass $10B in revenue in FY2025. A reasonable assumption is that CTAS will generate ~$14B of revenue in FY2035. Should it continue to generate at least an 18% Operating Margin, it stands to reason that its Operating Profit in FY2035 should be ~$2.52B.

If it can continue to generate ~15% – ~17% Net Income From Continuing Operations as a percentage of Revenue, it could generate ~$2.1B – ~$2.38B in FY2035.

If CTAS reduces its debt and continues to steadily repurchase shares, the share price should be much higher a decade from now.

I thought CTAS was overvalued by ~$25 when I acquired shares in December at an average cost of $184.557:

- 300 shares on December 19 @ ~$185.0861

- 200 shares on December 31 @ ~$183.7625

I intend to increase my exposure but will wait for the share price to retrace to at least the low $190s. At ~$192, for example, the forward P/FCF using my estimates under the conventional and modified methods of calculating FCF (~$4.09 and ~$3.77) would be ~47 and ~51. While this valuation is still ‘rich’, CTAS has been ‘overvalued’ for well over a decade. Unless I am prepared to ‘pay up’ to acquire shares in this ‘wide moat’ company, I will never be a shareholder.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CTAS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.