![]()

In my August 17, 2022 Chevron (CVX) post, I touch upon why I think the demise of oil and gas is overblown. At the time, CVX’s share price was ~$154. The share price has exhibited wild swings in the past 3 years with the current share price being ~$150 as I compose this post on August 5, 2025. CVX has, obviously, not created shareholder wealth from a capital appreciation perspective.

In several previous posts I state how I endeavor to acquire shares in great companies when they have temporarily fallen out of favor. CVX is such a company.

I am not a proponent of investing for dividend income. The automatic reinvestment of $18.82 in dividend distributions subsequent to my August 2022 post, however, is the primary reason for my CVX exposure having risen from 2,073 shares (July 31, 2022 FJJ Portfolio Report) to 2,484 shares (July 31, 2025 FFJ Portfolio Report).

Despite the increase in the number of shares held, the value of my CVX exposure has only risen from ~$339,000 in July 2022 to ~$376,700 in July 2025. As a long-term investor, however, a 3 year holding period is not a long time.

I last reviewed CVX in this August 4, 2024 post at which time the most current results were for Q2 and YTD2024. With the release of Q2 and YTD2025 results on August 1 and the recent completion of the Hess Corporation acquisition, this is an opportune time to revisit CVX.

Business Overview

The 2024 Form 10-K and Annual Report and the company’s website have a wealth of information to learn about the company.

Hess Corporation Acquisition

In my August 4, 2024 post, I touch upon CVX’s proposed acquisition of Hess Corporation and state:

In early 2024, XOM accused CVX of attempting to circumvent XOM’s right-of-first-refusal provision by negotiating the Hess deal and announced its decision to seek arbitration on this proposed acquisition. CNOOC joined XOM by moving to arbitration to assert its right over Guyana’s oil field.

XOM and CNOOC are confident their interpretation of intent in a Guyanese oil contract signed a decade ago will prevail. CVX has countered that after thorough due diligence, the provision does not apply to a corporate merger.

This Block officially entered production in December 2019 and marked a significant milestone, as production was achieved in less than 5 years after the initial discovery in 2015.

In 2019, fewer than 100 barrels per day were being produced. By 2027, however, oil production is expected to reach 1.3 million barrels per day.

While CVX’s proposed acquisition was announced in October 2023, it was not until July 18, 2025 when it officially completed its acquisition. This ~$53B acquisition closed after CVX won a landmark legal battle against Exxon Mobil (XOM). The International Chamber of Commerce (ICC) panel’s decision is final as there is no appeals process; the ICC is the court that oversaw the arbitration case.

CVX’s and Hess’s information technology workers have been meeting regularly to plan the integration. Converting technology and combining employees from both companies, however, is scheduled to take a few months.

It is fortunate that the ICC’s ruling is in CVX’s favor because it now has access to the largest oil discovery in decades – the prolific Stabroek Block off the coast of Guyana. This Block holds more than 11 billion barrels of oil and is one of the fastest growing oil regions in the world. Through this acquisition, CVX now has a 30% stake in Exxon’s (XOM) oil discovery offshore of Guyana. This is arguably the biggest oil discovery of the century and will hopefully help turn around CVX’s lagging performance.

Permian Basin

The booming Permian Basin represents ~50% of the US’s record-high 13.4 million barrels per day of crude oil; CVX and XOM are the top producers in the Permian. Both, however, are approaching their Permian interests differently.

XOM produces 1.6 million barrels of oil equivalent a day, including natural gas, and plans to increase its volumes to 2.3 million barrels daily in the Permian by 2030.

CVX, however, is focusing on free cash flow (FCF) generation. It reached its 2025 target of 1 million barrels daily in Q2 2025 and plans are to keep its Permian output relatively steady going forward.

Lobbying

CVX’s Chairman & CEO has forged strong ties with various high level US government officials in its fights against drilling restraints and climate laws. This lobbying includes efforts to push the US government to streamline the pipeline permitting process and to encourage fossil-fuel export deals.

Over the years, CVX has taken the political risks of remaining active in Venezuela given that it has the world’s largest oil reserves; it has operated in that country for over 100 years. It has been pumping ~300,000 barrels of crude oil a day which represents a sizable portion of Venezuela’s output. Despite these risks, CVX argued that its exit from the country would create an opportunity for China and Russia.

In May 2025, the Trump administration pulled CVX’s license to extract oil in Venezuela to exert pressure on the country’s socialist dictator.

Just recently, however, the Trump administration has abruptly reversed course. On the Q2 2025 earnings call with analysts, CVX’s Chairman & CEO stated:

We’ve been operating in Venezuela for over 100 years and our presence has played an important role in regional energy security as well as maintaining American economic interests. Since our license changed in May, we’ve been engaged with the U.S. government working closely with the administration to ensure our compliance with our country’s policies towards Venezuela. This month, it looks like there will be a limited amount of oil that will begin flowing to the U.S. from the Venezuela operations that we have an interest in, consistent with U.S. sanctions policy. And crude from Venezuela is sought after and very valuable to U.S. Gulf refiners that are specifically built to process heavy grades.

And so it serves as a reliable source of supply for the American economy. We don’t expect the flows from Venezuela will have a material impact on our results here in the third quarter although it will, at the margin, help satisfy some of the debt we’re owed. And over time, we hope to continue recovering that.

Financials

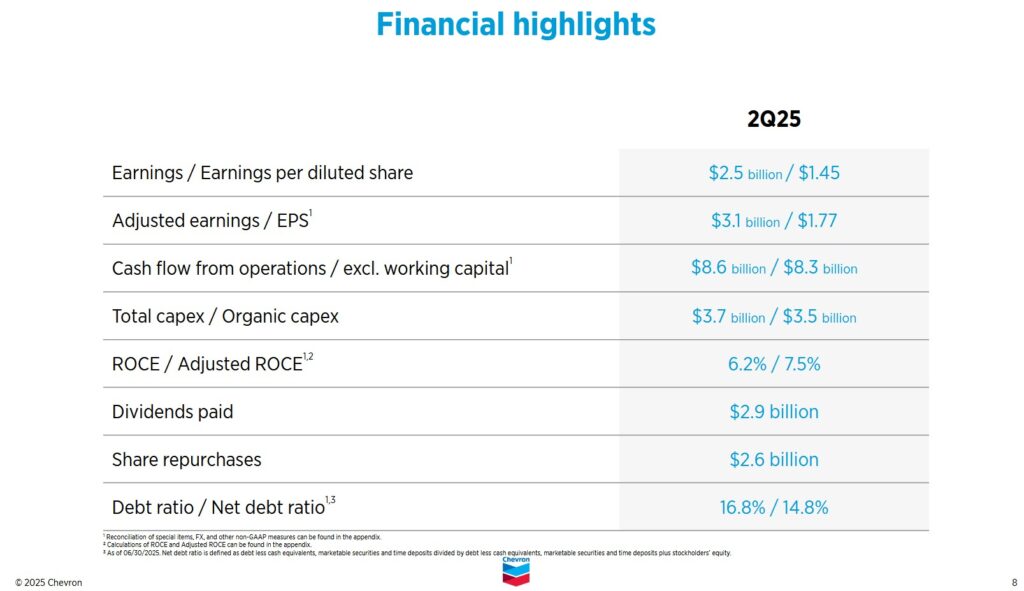

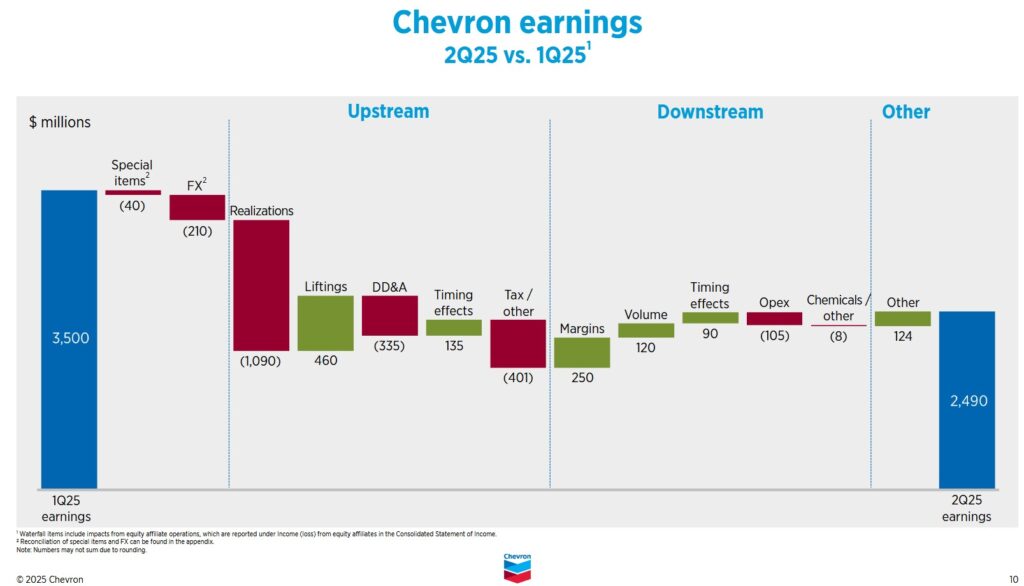

Q2 and YTD2025 Results

Material pertaining to CVX’s Q2 and YTD2025 earnings release is accessible here. The Q2 2024 Form 10-Q is currently unavailable. When published, it will be available here.

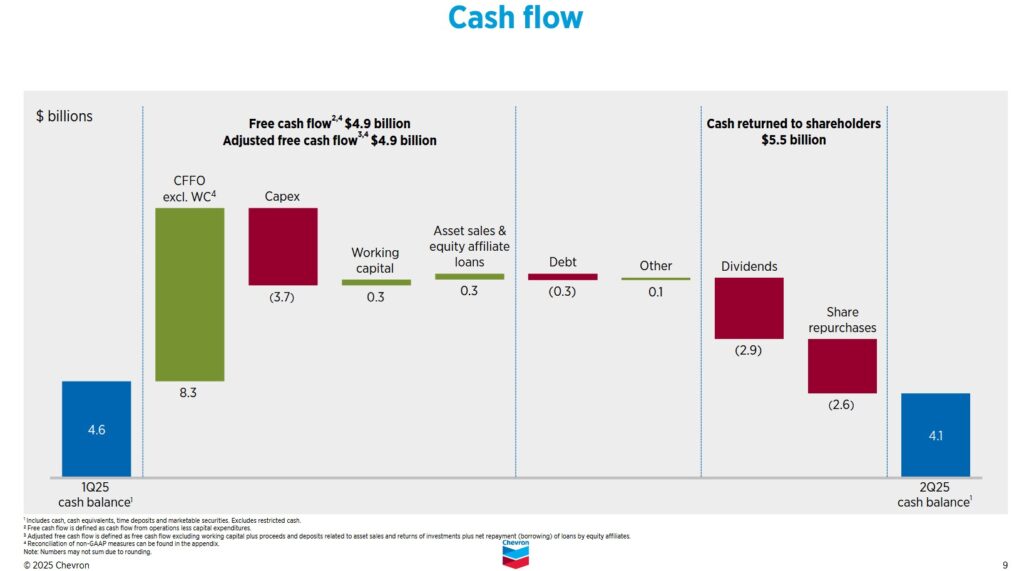

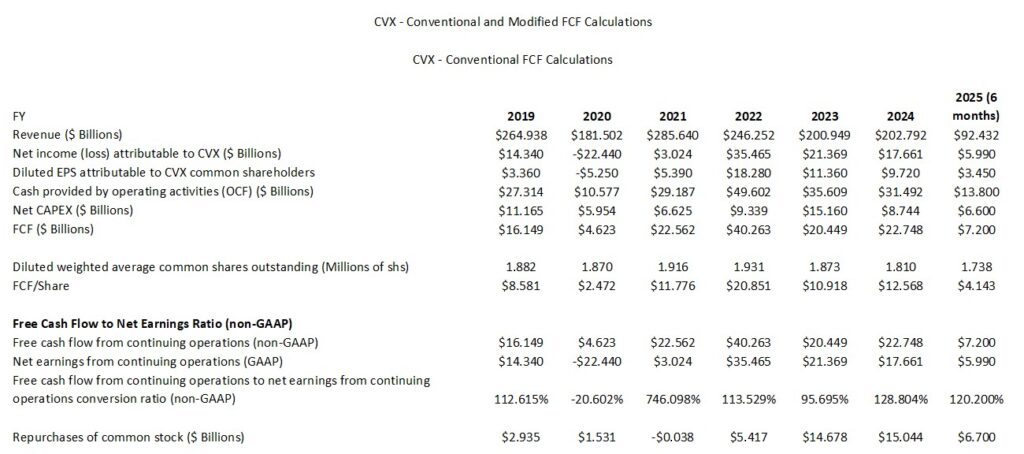

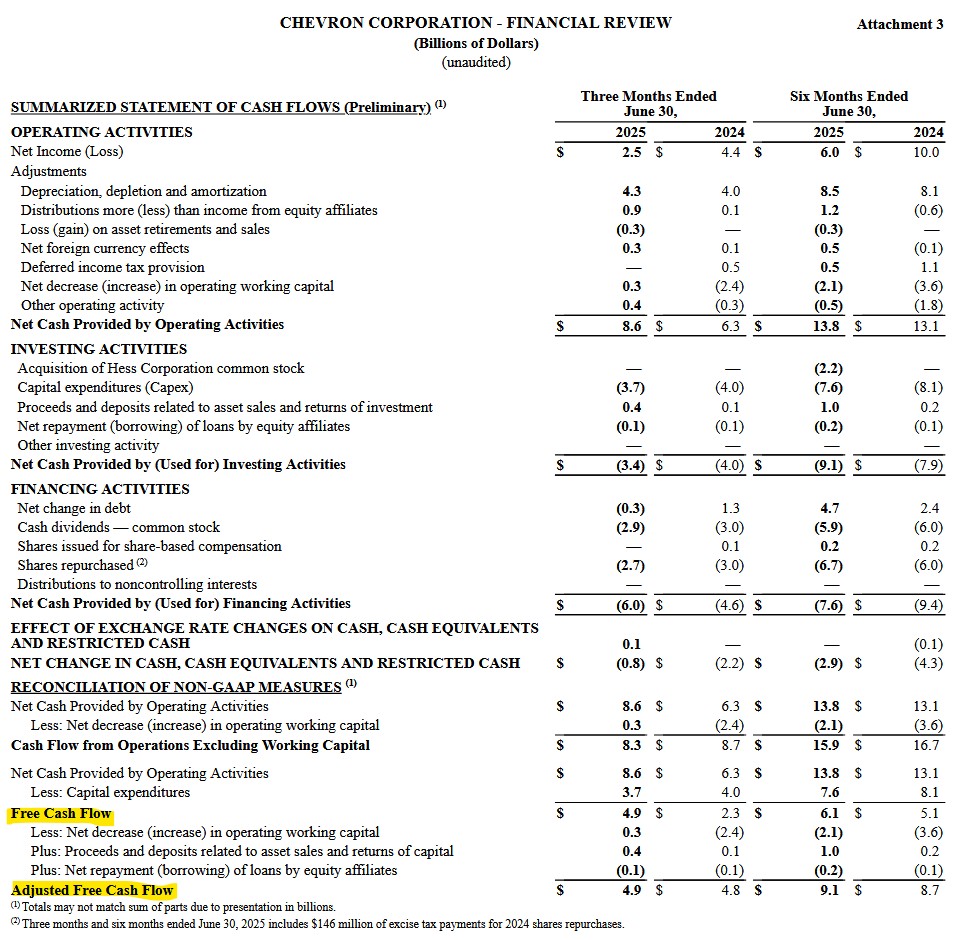

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

CVX is a highly capital intensive business as borne out by its annual CAPEX levels. High CAPEX has its advantages and disadvantages. A key advantage is the high barriers to entry. You may get new industry participants but they can not compete directly with CVX. Going forward, we will witness more industry consolidation with CVX likely to be an acquirer.

An investment in CVX over the last few years has not been for the faint of heart. Results have been ‘all over the map’. This is not surprising given the behavior of Brent, WTI (West Texas Intermediate) crude oil prices, and natural gas prices.

Despite challenging business conditions, CVX is highly focused on its capital allocation. Strong FCF has enabled CVX to increase its dividend and to make a significant dent in the number of outstanding shares.

Generally, I expect a ‘share based compensation’ (SBC) line item in the Consolidated Statements of Cash Flows. No such line item is reported by CVX although there is undoubtedly an element of SBC. I am, therefore, unable to determine CVX’s FCF calculated using the modified method. Having said this, the magnitude of CVX’s SBC is unlikely to materially alter the company’s FCF.

NOTE: CVX reports YTD2025 FCF of ~$6.1B versus my $7.2B calculation. The $1B variance is attributed to the ‘Proceeds and deposits related to asset sales and returns of investment’ which I take into consideration in determining FCF. CVX takes these proceeds into consideration to arrive at $9.1B of adjusted FCF.

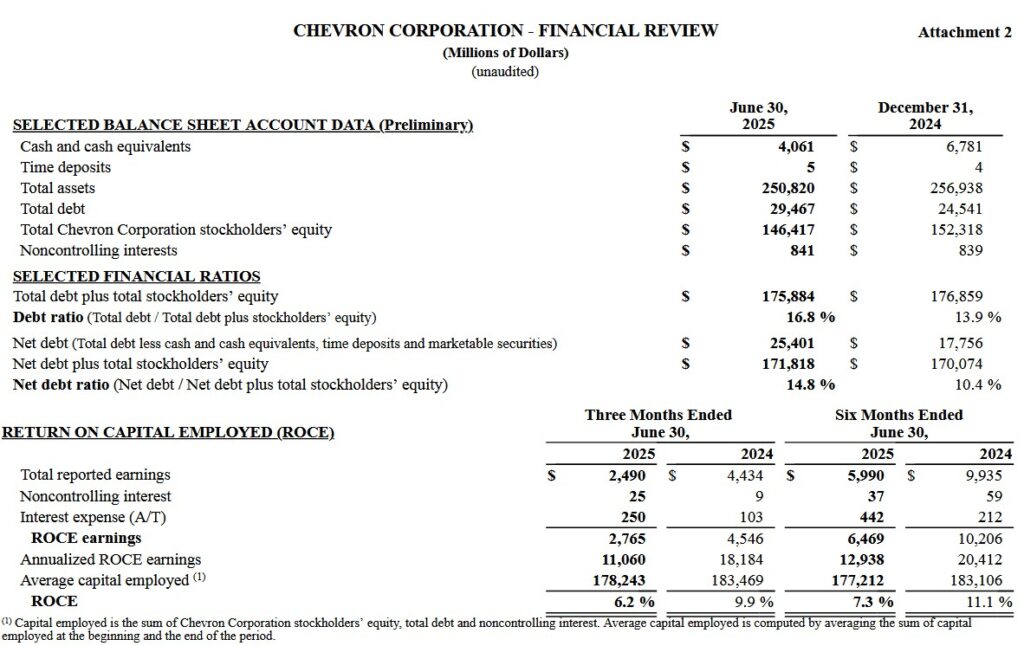

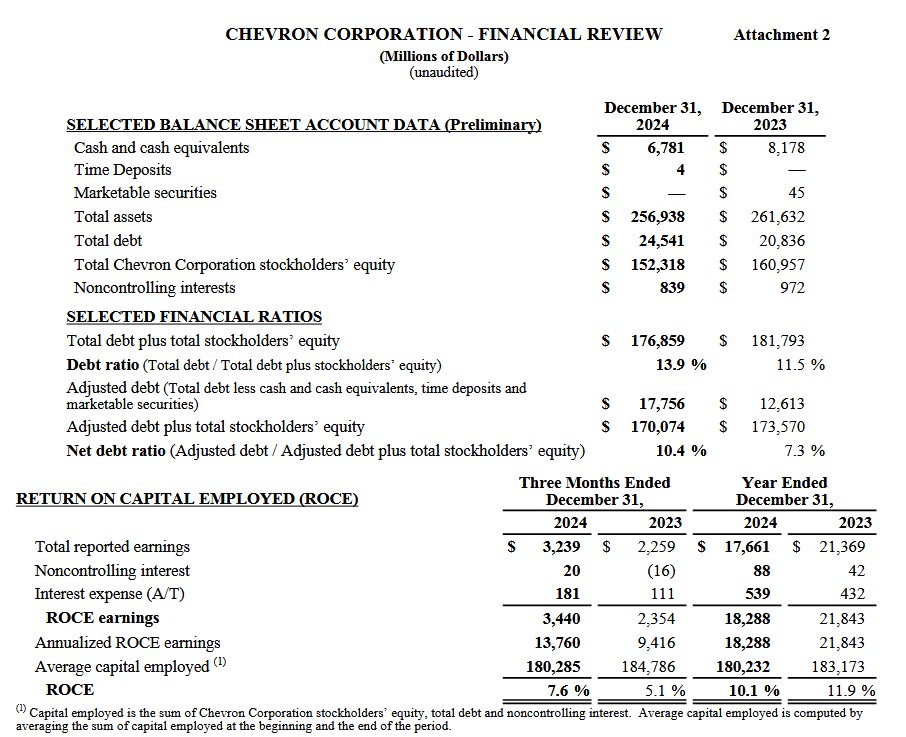

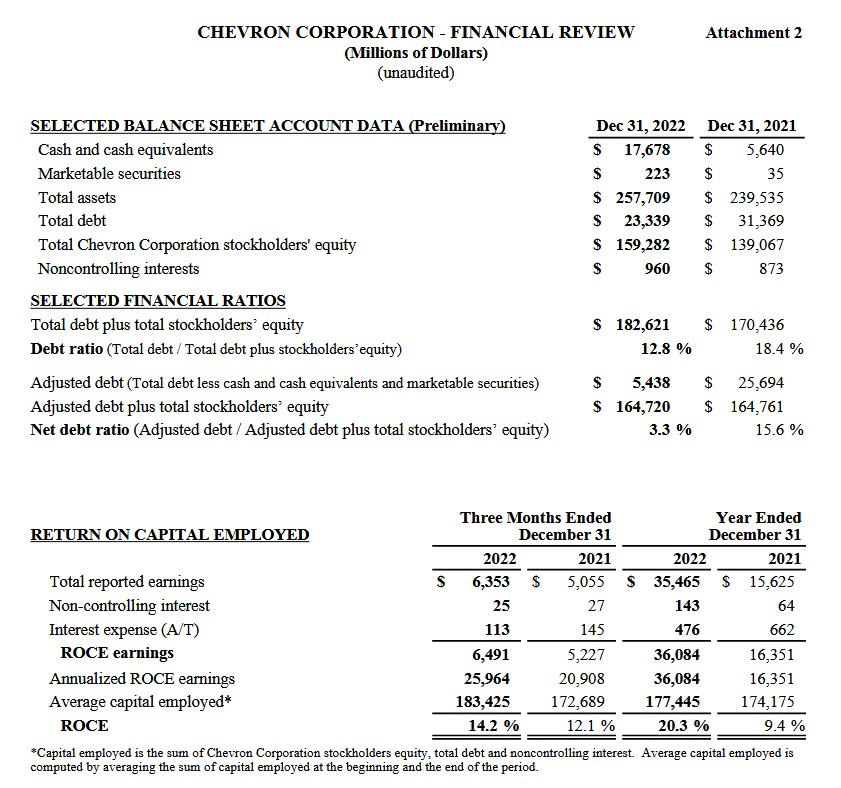

Return On Capital Employed (ROCE)

Return on Capital Employed (ROCE) measures how efficiently a company uses all of its capital (debt and equity) to generate profits. It is a key metric for evaluating a company’s profitability and capital efficiency over the long term. It shows how much profit (before interest and tax) a company earns for each dollar of capital employed in the business.

Given the volatility of CVX’s business, we must look at its ROCE results over a period of several years.

CVX’s ROCE in recent years has exhibited wide fluctuations with YTD2025 results being only 7.3%. CVX, however, now appears to be in a position where ROCE should show a marked improvement.

FY2025 Outlook

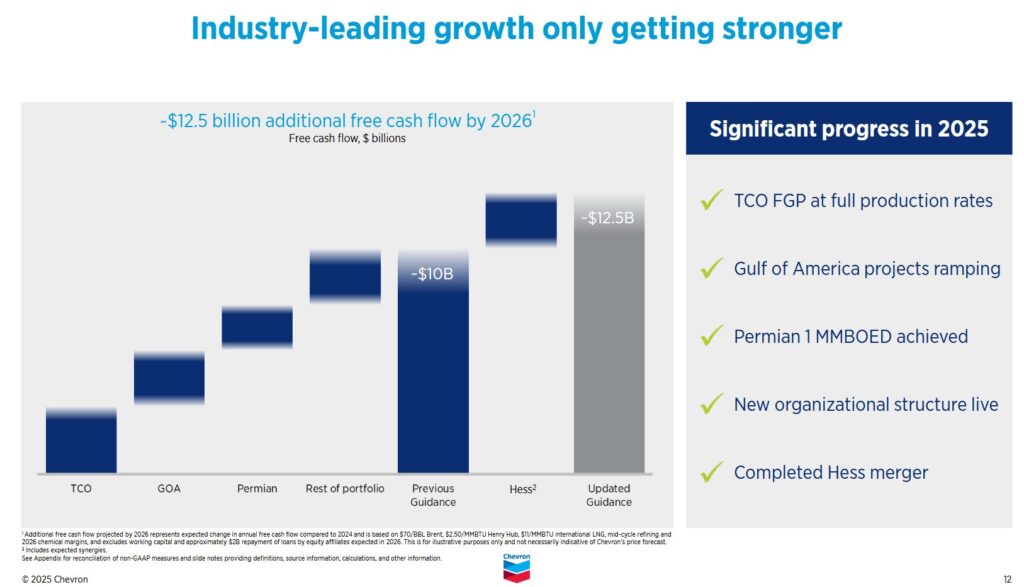

With the closure of the Hess acquisition, CVX now expects to realize $1B in synergies by FYE2025. This is 6 months sooner than previously expected.

When CVX released its FY2024 results in January 2025, the forecast was for $10B of FCF growth over the next two years. Following the completion of the Hess acquisition, management anticipates ~$12.5B additional FCF growth by 2026! Given this outlook, I anticipate CVX will continue to reward shareholders with attractive annual dividend increases and meaningful share repurchases.

Earlier in 2025, CVX outlined the reorganization of its business units. This reorganization entails the elimination of ~8,000 positions or ~17.7% of the 45,298 employees at December 31, 2024 (page 5 of 151 in the FY2024 Form 10-K). This is one component of CVX’s plans to achieve $2B – $3B in structural cost reductions by the end of 2026.

Oil prices are subject to supply decisions made by major producers in the Middle East. In addition, there are fears that tariff fights could squeeze fuel demand. Trying to forecast Brent, WTI (West Texas Intermediate) crude oil prices is difficult at best even for industry experts.

Risk Assessment

Some investors fixate on an investment’s potential return and overlook the various risk aspects of the investment to their detriment. I, however, encourage investors to read the ‘Risks’ section of a company’s Form 10-K.

While I try to assess a company’s risk, I also look at how the rating agencies perceive the company’s risk.

CVX’s current domestic long-term unsecured debt ratings and outlook are:

- Moody’s: Aa2 (stable) last reviewed November 14, 2023.

- S&P Global: AA- (stable) last reviewed September 19, 2024.

The rating assigned by Moody’s is the middle tier of the high-grade investment-grade category. It is one tier above the rating assigned by S&P Global.

Both ratings define CVX as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Dividend and Dividend Yield

CVX’s dividend history is accessible here.

The 3rd $1.71/share quarterly dividend is scheduled for distribution on September 10, 2025.

Management expects a significant improvement in FCF, and therefore, I anticipate at least a $0.10/share increase in the quarterly dividend will be declared in early February 2026. This would mark the 39th consecutive year of dividend increases.

CVX’s diluted weighted average shares outstanding in FY2011 (in millions) was ~2,001. In the first half of FY2025, CVX repurchased ~$6.7B and the diluted weighted average shares outstanding in Q2 2025 was 1,724.

On January 25, 2023, CVX announced that its Board authorized a new $75B share repurchase program (the ‘2023 Program’) with no fixed expiration that took effect on April 1; the previous authorization was $25B. The 2023 Program took effect on April 1, 2023, and does not have a fixed expiration date.

The plan is to continue to steadily repurchase shares across commodity cycles. With a breakeven Brent price of around $50/barrel to cover CAPEX and the dividend and with excess balance sheet capacity, CVX is positioned to return more cash to shareholders in any reasonable oil price scenario. Rather than the Board having to revisit the share repurchase authorization every few years, the repurchase authorization has been set where this matter does not need to be revisited as frequently.

In my August 4, 2024 post I tried to approximate the weighted average number of outstanding diluted shares in FY2024 and wrote:

In Q2 and YTD2024, CVX repurchased $3B and $6B of its shares lowering the weighted average to 1,833 in Q2 2024.

CVX is targeting share repurchases of ~$17.5B in FY2024 meaning it expects to repurchase another ~$11.5B.

Assuming the weighted average share price of all shares repurchased in FY2024 is ~$150 and CVX repurchases ~$17.5B shares, it will end up repurchasing ~116,666,667 shares in the year.

The weighted average shares outstanding for the 3 months ending December 31, 2023 was 1,868 million. Deduct ~116.7 million shares from the outstanding number of shares in the last quarter of FY2023 and CVX should have ~1,751 million shares outstanding at FYE2024. Average 1,868 million and 1,751 million and we get ~1,810 million shares as the weighted average shares outstanding in FY2024.

As luck would have it, 1,810 million is what CVX reported on page 81 of 151 in its FY2024 Form 10-K.

On the Q2 2025 earnings call, management stated it would provide its outlook and guidance for share repurchases at its November 12, 2025 Investor Day.

Valuation

In the first half of FY2025, CVX generated diluted EPS and adjusted diluted EPS of $3.45 and $3.95.

I am not even going to attempt to forecast CVX’s FY2025 adjusted diluted earnings. Even the broker estimates are ‘all over the map’ although the gap could narrow after the Q2 and YTD2025 results have been thoroughly analyzed.

For now, however, CVX’s forward adjusted diluted PE estimates using the current earnings estimates and a ~$151 share price are:

- FY2025: ~19.2 using a mean of $7.87 and a low/high range of $5.45 – $10.06 from 23 brokers.

- FY2026: ~15.7 using a mean of $9.59 and a low/high range of $6.68 – $14.77 from 24 brokers.

- FY2027: ~12.6 using a mean of $12.01 and a low/high range of $8.80 – $16.81 from 18 brokers.

I prefer to assess CVX’s valuation based on FCF. To determine CVX’s approximate valuation based on FCF, I use the average of my YTD2025 $7.2B FCF estimate and CVX’s YTD2025 $6.1B FCF and $9.1B adjusted FCF. The average of all 3 is ~$7.47B.

If CVX generates $14B of FCF in FY2025 and the diluted weighted average shares outstanding for the year ends up being ~1,724 million (using the Q2 2025 number as being the average for the year), the FCF/share could be ~$8.12. The company has generated ~$4.14 in the first half of the year. I, however, anticipate slightly better results in the second half of the year. Using a FY2025 ~$8.50 FCF/share estimate and a ~$151 share price, the forward P/FCF is ~17.8.

Final Thoughts

Following the successful acquisition of Hess Corporation and $2B – $3B in structural cost reductions, this appears to be an opportune time to acquire CVX shares before its performance improves.

As noted earlier, management forecasts ~$12.5B of additional FCF by 2026. After reinvesting in the business, considerable cash should be available for share repurchases and dividend increases.

CVX operates in a volatile and highly capital intensive industry. As a relatively conservative investor wanting exposure to integrated oil and gas producers, I limit my exposure to CVX and XOM, the 2 largest industry participants.

I currently hold 2,484 CVX shares in 3 different ‘Core’ accounts in the FFJ Portfolio. When I completed my 2025 Mid-Year Portfolio Review, it was my 4th largest holding; shares were trading at ~$143.20. Depending on CVX’s share price when I receive the quarterly dividend payments (less the 15% dividend withholding tax), I should be able to increase my CVX exposure by 15 – 20 shares/quarterly without having to outright purchase more shares. I, therefore, currently have no plans to make any outright CVX purchases.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CVX and XOM.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.