![]()

I have a positive outlook on Chevron Corporation’s (CVX) long-term potential in that in recent years CVX has been repositioned to deliver long-term value to investors.

There is growing demand for its products and efficient capital employment should enable it to continue to generate superior returns relative to its largest competitors.

CVX generates strong cash flow which should allow management to continue to deliver on its four financial priorities (maintain and grow dividend, fund capital programs, continue to strengthen the balance sheet, and return surplus cash to shareholders).

I have acquired additional shares for one of the ‘core’ accounts within the FFJ Portfolio.

I have covered Chevron Corporation (CVX) in several previous articles with the most recent having been published September 3, August 17, and April 8. My long-term outlook has not changed, and therefore, this article is relatively brief.

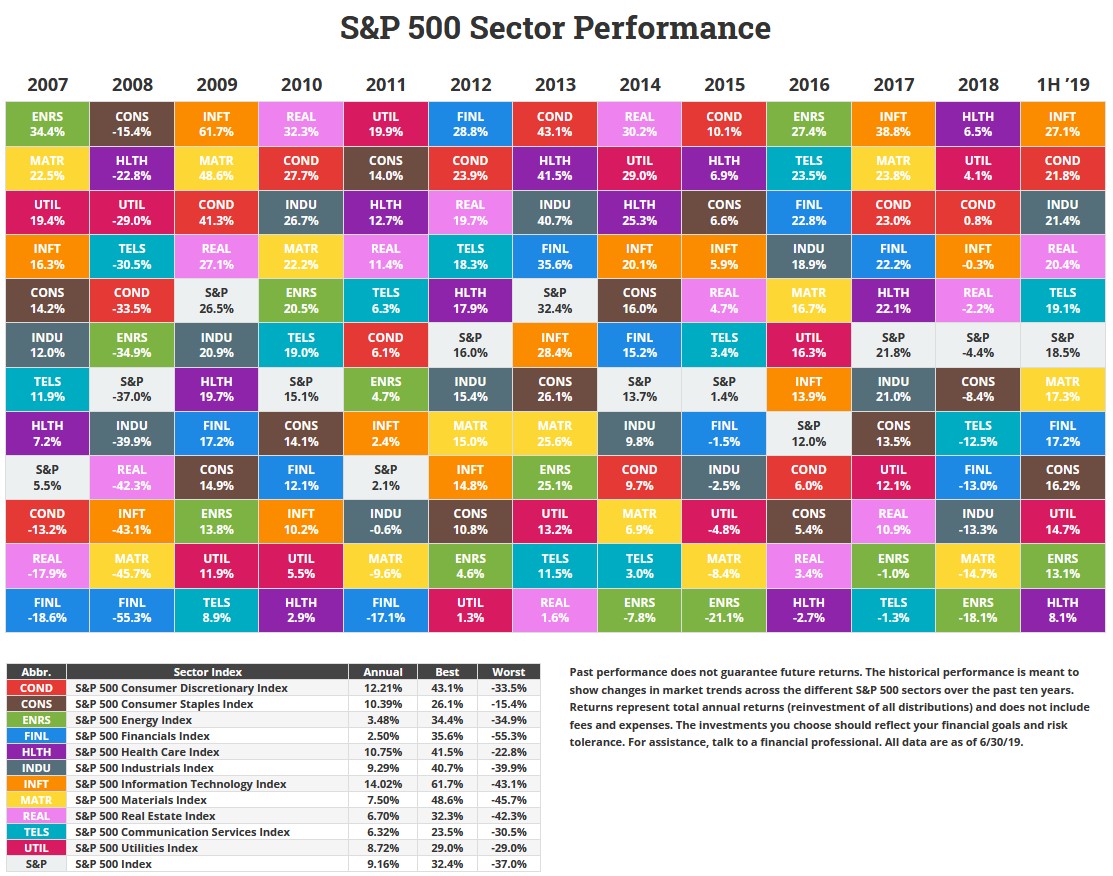

Looking at the annual performance of various sectors within the S&P500 as at June 30 2019 we see that the S&P500 Energy Index (ENRS) has had a rough go of it on an annual basis for the last several years.

When I glance at the list of companies within the iShares U.S. Energy ETF I know the vast majority are companies in which I, given my conservative nature, would never even remotely consider investing. As a result, comparing how this sector has performed relative to the broad market does not impact my investment decision making process.

What I view to be more relevant is how a specific industry participant has performed, and more importantly is likely to perform, against the broad market index.

My exposure to the energy sector is restricted to Enbridge Inc. (ENB.TO) and, to a greater extent, the following major integrated oil and gas companies:

Presently, my interest lies in increasing my exposure to CVX which is one of my largest holdings.

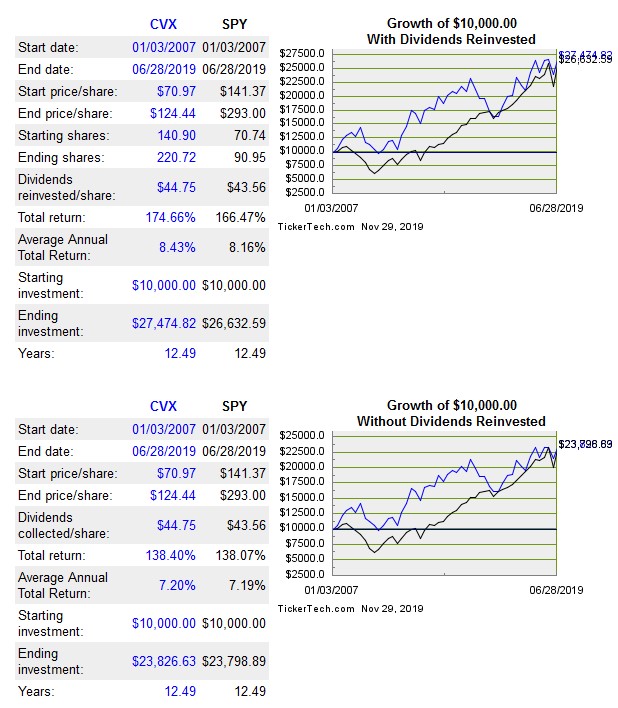

If we look at how CVX has performed relative to the S&P500 for ~12.50 years we see that CVX’s return has been more volatile than the S&P500. We also see, however, that CVX’s overall return, with and without dividend reinvestment, has been comparable to the S&P 500.

Source: Tickertech

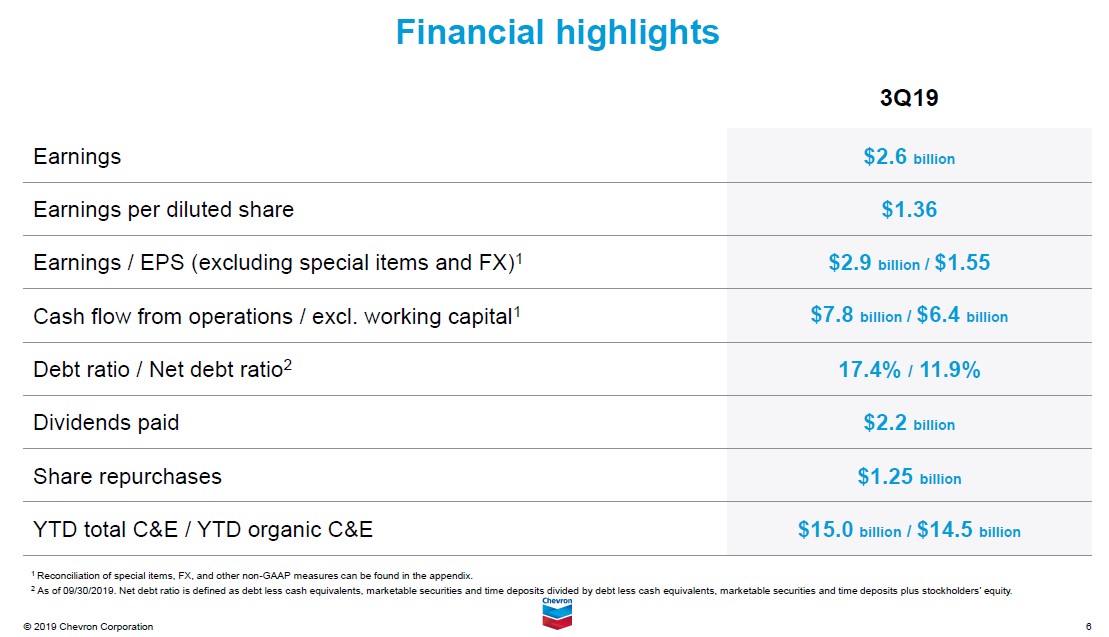

Looking at CVX’s financial highlights presented in its November 2019 Investor Presentation it is apparent a very limited number of companies in the oil and gas sector rival CVX from (1) capital and exploratory expenditure and (2) cash flow from operations perspectives.

Since CVX operates in a cyclical industry I view its discipline around capital and exploratory expenditures as being of utmost importance. I like that ~70% of CVX’s 2019 spend will deliver cash flow within 2 years. Projects in which cash flow is not expected to be generated until several years in the future worries me as this typically translates into greater uncertainty that actual results will match projected results.

Credit Ratings

In my opinion, far too many investors focus almost exclusively on an investment’s potential reward; consideration to risk potential is often an afterthought.

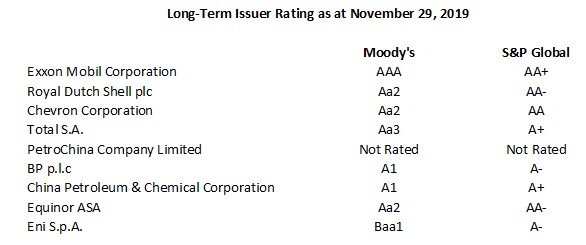

While credit ratings agencies are not infallible, I still like to look at the ratings they have assigned to the companies I review.

The following table reflects the long-term issuer credit ratings assigned by Moody’s and S&P Global as at November 29, 2019 to the largest industry participants.

Both ratings agencies rate CVX’s long-term debt as the middle tier within the high grade of the investment grade category. This gives me some comfort that I am not assuming an inordinate level of risk by way of my CVX investment.

Dividend, Dividend Yield, and Share Repurchases

CVX’s dividend history can be accessed here.

Using CVX’s current $117.13 share price as at November 29th’s market close, the $1.19/quarter or $4.76/annual dividend provides investors with a ~4.06% dividend yield. Being a Canadian resident and holding shares in a non-registered account results in my dividend yield being reduced 15% to ~3.45%. While I do not appreciate this ‘haircut’, I look at CVX from a total return perspective and am willing to accept this reduced dividend yield.

Looking at CVX’s operating performance and bearing in mind that maintaining and growing the dividend is the first financial priority of 4 listed on page 9 of 90 in the November 2019 Investor Presentation, I anticipate CVX will declare at least a $0.05/share increase to its quarterly dividend ($1.19 increasing to $1.24) toward the end of January 2020; shareholders on the date of record in mid-February 2020 will be eligible for this increased dividend.

Returning surplus cash to shareholders is the 4th financial priority reflected on page 9 of 90 in the November 2019 Investor Presentation. Looking at the ‘Diluted Weighted Average Number of Shares Outstanding (000s)’ as at the end of Q3 2019 we see 1,893,928. At the end of FY2012 the total amounted to over 1,950,000.

Valuation

One of my sources indicates the current mean adjusted earnings estimates for FY2019 and FY2020 from 22 and 24 analysts, respectively, are $6.36 and $6.86.

Using the current $117.13 share price we get forward adjusted PE levels of ~18.14 and ~17.1 for FY2019 and FY2020. These levels are no ‘bargain basement’ levels but at the same time are not excessive.

When we look at YTD diluted earnings we see that as at the end of Q3 2019, CVX generated $5.02 in diluted EPS (page 4 of 49 in the Q3 2019 10-Q). If we conservatively estimate that CVX will generate a comparable quarterly EPS in Q4 2019 as in the previous 3 quarters then we arrive at ~$6.70 in diluted EPS. Using the current $117.13 share price we then get a diluted PE of ~17.50. Even if CVX to turn in ‘less than stellar’ Q4 results and diluted EPS came in at ~$6.50, we would be looking at a diluted PE of ~18. These are not a bargain basement levels but I view them as reasonable based on the long-term outlook presented in CVX’s November 2019 Investor Presentation.

Final Thoughts

In this current environment I view many companies in which I wish to increase my position/initiate a position as being richly valued. I am also of the opinion that a broad market pullback within the next few months is not out of the realm of possibility. As a result, purchases have been few and far between and, on a selective basis, am employing the use of options in which I stand to benefit if the underlying stock price remains range bound or declines; I draw your attention to very recent Mastercard Incorporated (MA) and Microsoft Corporation (MSFT) articles.

Using a portion of the premiums I generated from writing option contracts, for which I disclosed details in these recent articles, I have acquired 90 additional CVX shares at a price of $117.177 within one of the ‘Core’ accounts held within the FFJ Portfolio. I will not receive the quarterly $1.19 dividend payable on December 10th as these shares were acquired subsequent to the November 18th date of record. In the grand scheme of things, missing out on ~$91 (90 x $1.19 x 85%) is not something which impacted my investment decision (Reminder: I incur a 15% withholding tax on CVX’s dividend because shares are held in a non-registered account).

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long CVX.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.