I have minimal exposure to Carrier Global Corporation (CARR) and pay virtually no attention to this holding. In fact, my last review was in this August 3, 2021 post at which time the most current financial information was for Q2 2021!

With the release of Q1 2025 results on May 5, 2025 I revisit this holding. While the company’s risk profile is much improved I consider shares to be too richly valued.

Business Overview

CARR operates through 2 business segments: Heating, Ventilating and Air Conditioning (HVAC) and Refrigeration.

The best way to learn about the company is to review its website and Part 1 Item 1 in the most current From 10-K that is accessible through the SEC Filings section of the company’s website.

Financial Results

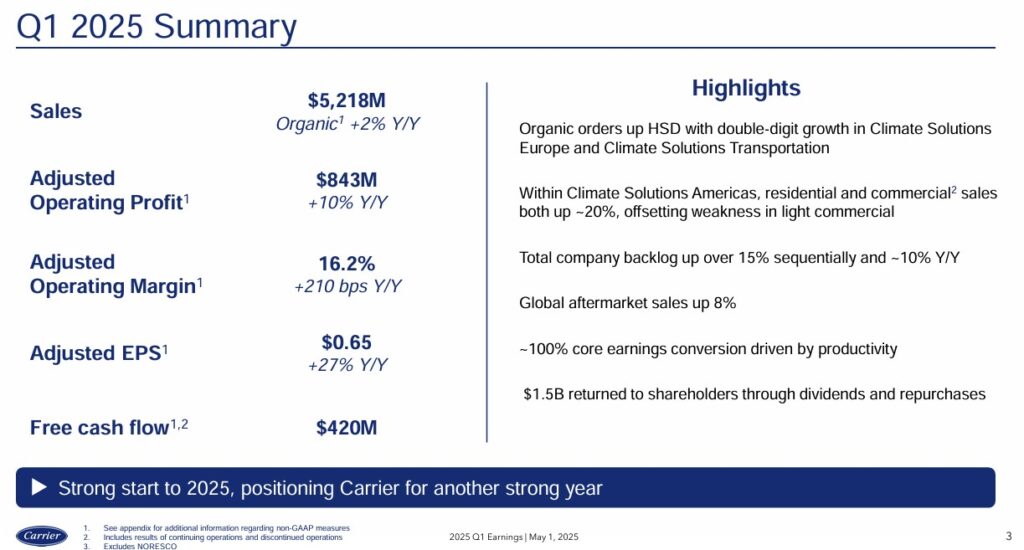

Q1 2025

In Q1, CARR had an unfavorable 5% net impact from acquisitions and divestitures and marginal headwind from FX.

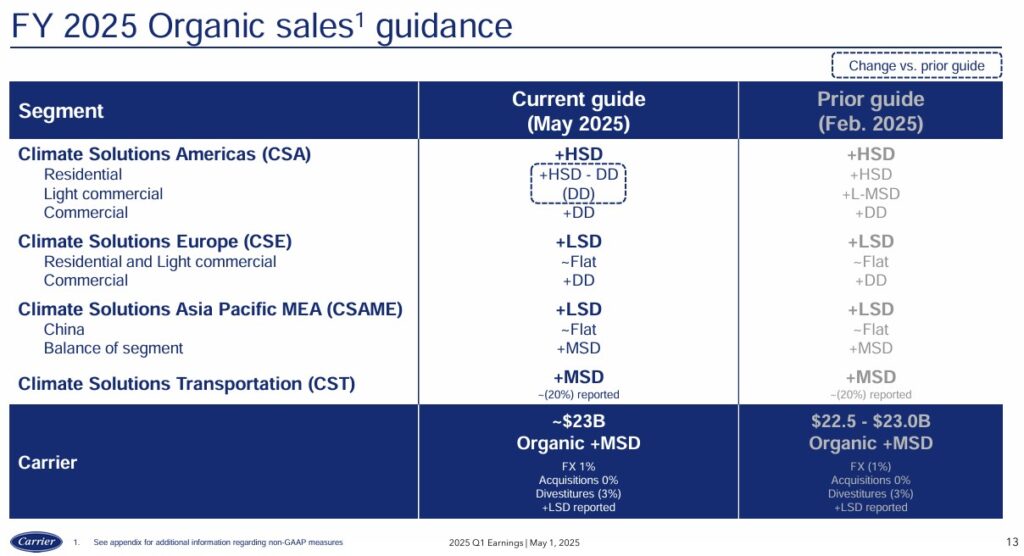

Organic sales were in line with expectations with stronger than expected performance in Climate Solutions Americas. This, however, was partially offset by weaker performance in Climate Solutions, Asia, Middle East and Africa. Europe and Transportation results were as expected.

Adjusted operating margin expanded by 210 bps YoY. The absence of commercial refrigeration was about a 70 bps tailwind to margin.

Adjusted EPS of $0.65 was up 27% YoY driven by improved adjusted operating profit, lower net interest expense from deleveraging, and a lower share count.

Free cash flow (FCF) of $0.42B was also stronger than expected, driven by higher net income, lower than expected seasonal working capital requirements and lower CAPEX.

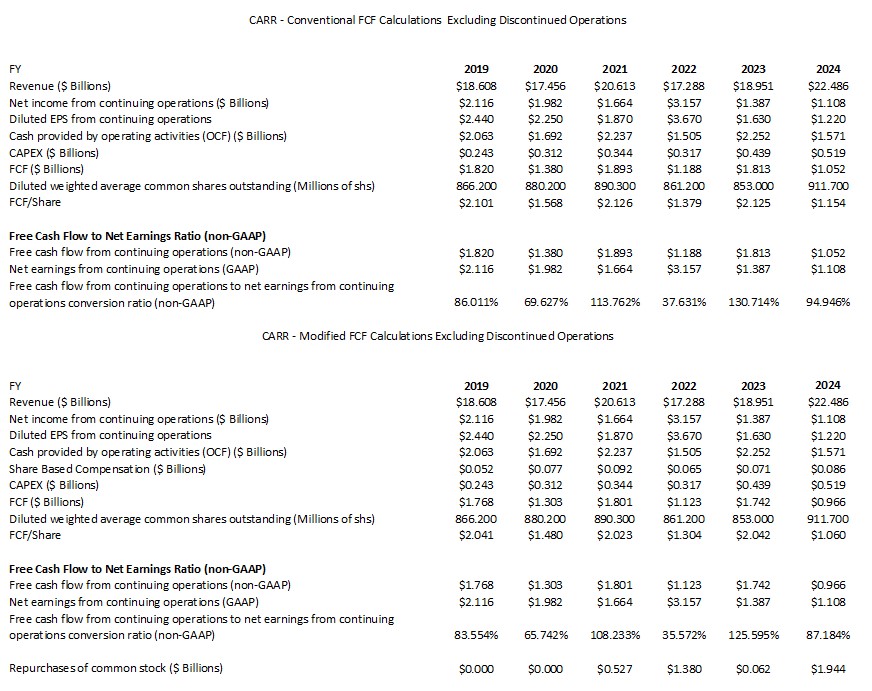

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

FCF is a non-GAAP metric, and therefore, its method of calculation is inconsistent. Historically, CARR deducts CAPEX from OCF to calculate its FCF. In recent posts, however, I explain my rationale for also deducting share-based compensation (SBC) from a company’s OCF.

CARR has been undergoing a transformation subsequent to its spin-off from United Technologies (now RTX). This is borne out by wild swings in its annual results.

The first table below excludes the results from discontinued operations.

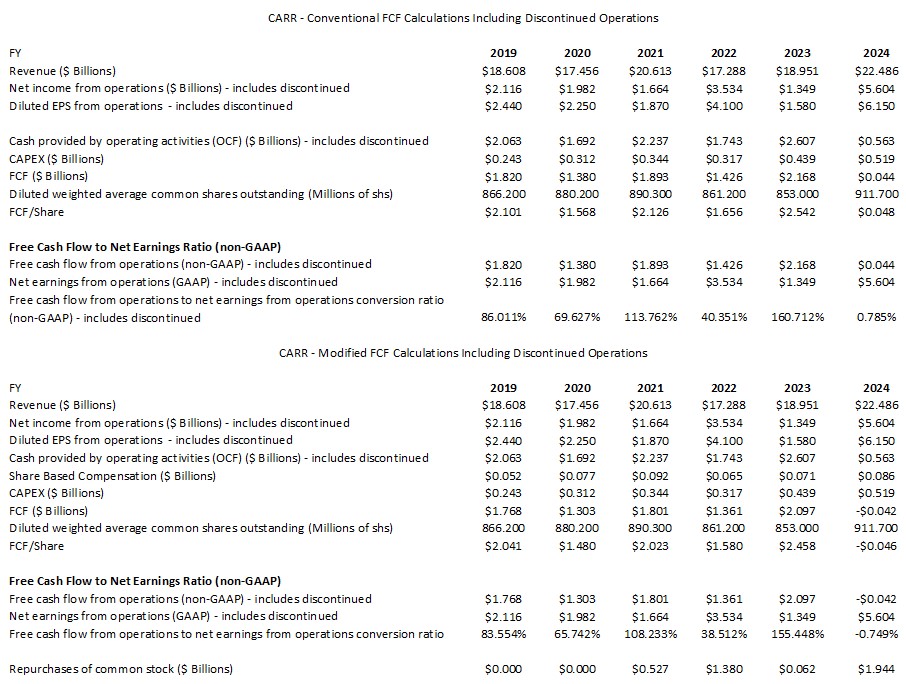

The following table includes discontinued operations to demonstrate what CARR shareholders have had to put up with in recent years.

Now that CARR has undergone an extensive transformation, management anticipates there will be better earnings and FCF stability.

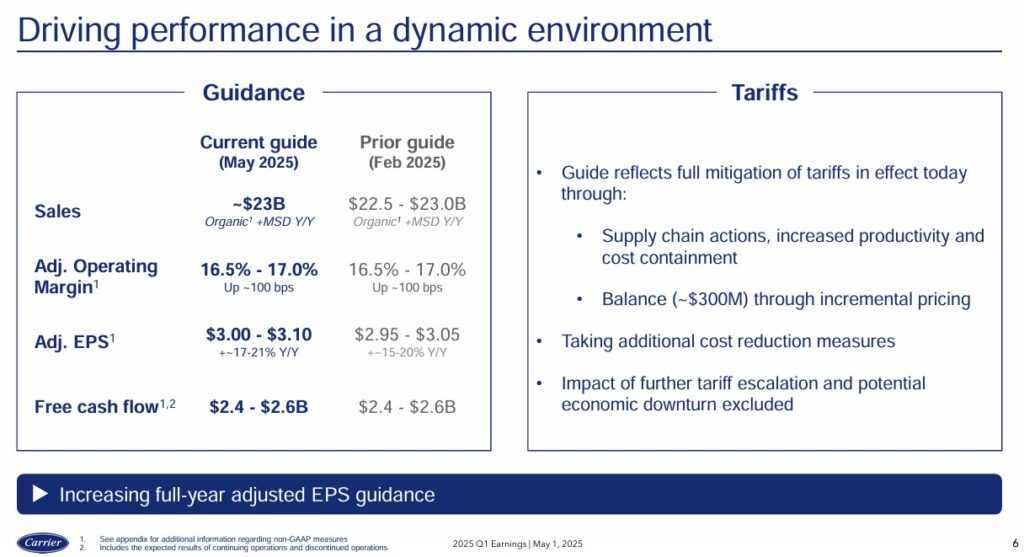

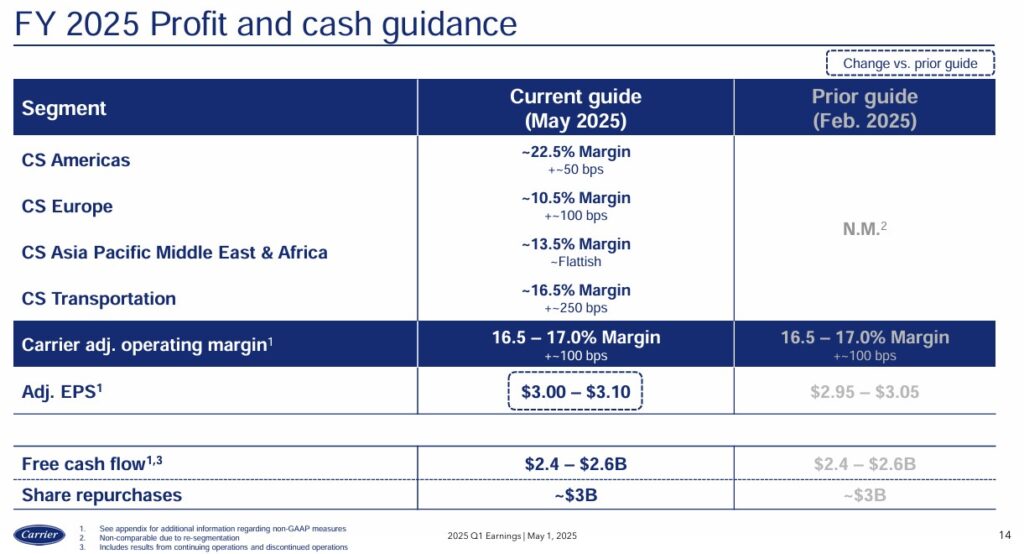

FY2025 Guidance

The following reflects CARR’s most current guidance.

CARR has grown its US headcount by ~20% over the past 5 years and continues to invest in its US workforce and factories.

On the tariff front, virtually all of its imports from Mexico are US MCA compliant. Being USMCA compliant means that goods meet the rules and requirements set out in the U.S. – Mexico – Canada Agreement. Compliance allows for smooth cross-border trade.

For the tariffs currently in effect, China is about 80% of CARR’s current US tariff exposure. CARR is fully mitigating its tariff exposure through supply chain and productivity actions with the balance of ~$0.3B being addressed through price increases.

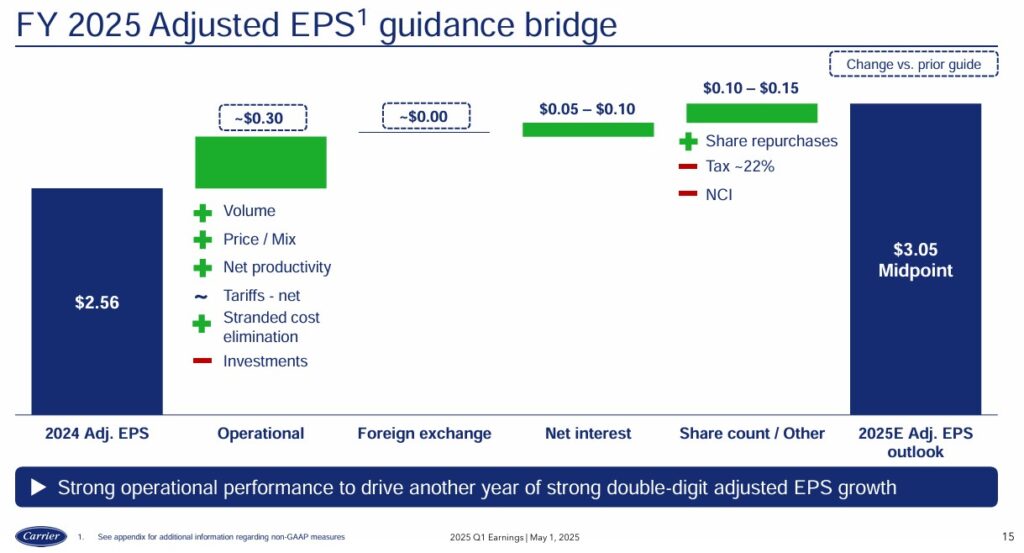

Based on its strong start to FY2025 and current FX rates, CARR is increasing our full year adjusted EPS guidance.

Risk Assessment

There is a considerable improvement in CARR’s level of risk following my August 3, 2021 post. Its current domestic unsecured long-term credit ratings are:

- Moody’s assigns a Baa1 rating with a stable outlook.

- S&P Global assigns a BBB+ rating with a stable outlook.

- Fitch assigns a BBB+- rating with a stable outlook.

CARR’s domestic unsecured long-term credit rating at the time of my prior review were:

- Moody’s assigns a Baa3 rating with a stable outlook.

- S&P Global assigns a BBB rating with a stable outlook.

- Fitch assigns a BBB- rating with a stable outlook.

All 3 rating agencies have increased CARR’s credit rating by 2 tiers!

The current ratings are all the top tier of the lower-medium grade investment-grade category. These ratings define CARR as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity for CARR to meet its financial commitments.

Dividend

CARR’s website does not currently maintain a dividend history. When I last reviewed CARR, it was scheduled to distribute its 3rd consecutive $0.12/quarter dividend on August 10, 2021.

On May 2, 2025, it is scheduled to distribute its 2nd consecutive $0.225 quarterly dividend.

CARR’s capital allocation priorities include funding organic growth, acquisitions and capital returns to shareowners through a growing and sustainable dividend and share repurchases. A company that prioritizes dividend growth ‘pigeon holes’ itself because it attracts a shareholder base that expects consistent dividend increases. Growing the company’s dividend, however, might not be the most optimal means by which to increase shareholder value.

In my opinion, dividend metrics should have little bearing on the investment decision making process. The focus should be on a company’s total potential shareholder return.

Share Repurchases

Since CARR’s initial share repurchase authorization in February 2021, the Board has authorized the repurchase of up to $7.1B of CARR’s outstanding common stock. This includes a $3B increase approved in October 2024.

As of FYE2024 (December 31, 2024), CARR:

- repurchased 70.1 million shares of common stock for an aggregate purchase price of $3.9B; and

- had ~$3.2B remaining under the current authorization.

At FYE2024, the weighted average diluted shares outstanding was 911.7 million.

In Q1 2025, CARR repurchased $1.288B of its common shares and the weighted average was reduced to 878.3 million. In April 2025, CARR repurchased an additional $0.32B worth of shares and management continues to target $3B of share repurchases in FY2025.

Valuation

My preference is to gauge a company’s valuation based on cash flow. I do, however, also consider GAAP and non-GAAP earnings guidance.

Management’s FY2025 adjusted EPS guidance is now $3 – $3.10. Using the current ~$70 share price, the forward adjusted diluted PE range is ~22.6 – ~23.3.

The forward-adjusted diluted PE levels using the current share price and broker estimates are:

- FY2025 – 24 brokers – ~23.5 using a mean of $2.99 and low/high of $ 2.80 – $3.06.

- FY2026 – 22 brokers – ~20.5 using a mean of $3.42 and low/high of $ 3.19 – $3.70.

- FY2027 – 10 brokers – ~18.3 using a mean of $3.82 and low/high of $ 3.55 – $4.20.

Take these earnings estimates with a ‘grain of salt’. I don’t know how anybody can consistently accurately predict how a company is going to perform 2+ years from now…especially in the current environment.

Management’s FY2025 FCF guidance is $2.4B – $2.6B and the plan is to repurchase $3B of shares. It has already repurchased $1.608B of shares in 2025 leaving another ~$0.892B to be repurchased (using the $2.5B mid-point). If it repurchases shares at an average price of $71, that is another ~12.563 million shares.

The weighted average diluted shares outstanding in Q1 2025 was 878.3 million. Depending on when shares are repurchased and the purchase price, it is quite possible the diluted weighted average shares outstanding in FY2025 could drop to ~873 million. Divide $2.5B of FCF by ~873 million shares and the FCF/share could be ~$2.86. Using the current ~$69.60 share price, the forward P/FCF is ~24.3.

If we estimate that CARR’s SBC in FY2025 will be ~$0.09B, the FY2025 drops to ~$2.41B. Divide $2.41B of FCF by ~873 million shares and the FCF/share could be ~$2.76. Using the current ~$69.60 share price, the forward P/FCF is ~25.2.

Final Thoughts

CARR has certainly tested shareholder patience following its spin-off from UTX (now RTX). It appears its transformation, however, is complete and more stable results are possible.

Management’s FY2025 guidance calls for FCF of $2.4B – $2.6B which is a range the company has never achieved since becoming a stand-alone public entity.

The 2 tier improvement in its domestic unsecured long-term credit ratings assigned by 3 rating agencies subsequent to my August 3, 2021 post is also encouraging.

I was a UTX shareholder when it divested CARR in April 2020 and received CARR shares in a retirement account for which I do not disclose details and also in a ‘Side’ account within the FFJ Portfolio.

I ended up selling the shares in the retirement account in October 2022 as part of my Registered Retirement Savings Plan (RRSP) melt-down strategy. The ‘Side’ account, however, still has 419 shares.

CARR has never been a top 30 holding. While its risk profile is much improved following its extensive restructuring, I consider shares to be overvalued by ~$15/shares. I do not intend to increase my exposure other than through automatic dividend reinvestment.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CARR.

Disclaimer: I do not know your individual circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.