Can Becton Dickinson (BDX) regain investor confidence?

Although I reviewed this existing holding as recently as this February 7, 2025 post, it is worth revisiting given the ~18% share price plunge following the release of Q2 and YTD2025 results and revised FY2025 guidance on May 1.

My medical instruments and supplies (BDX) and life sciences and diagnostics holdings (Thermo Fisher (TMO), Danaher (DHR), Agilent (A)) are struggling largely due to budget cuts at the National Institutes of Health; the government and academic spending environment will likely remain weak for the foreseeable future. Intuitive Surgical (ISRG) is my only holding that has yet to lose investor confidence (denoted by share price behavior).

In my prior post, I touched upon the planned separation of the Biosciences and Diagnostics business that was announced on February 5. On the Q2 2025 earnings call, management stated that the separation process is advancing well and is on schedule. This business unit makes diagnostic products such as those used to detect infectious diseases and cancers.

BDX is in talks with Thermo Fisher (TMO) and Danaher (DHR) for a potential sale. It is, however, also exploring a Reverse Morris trust tax-free deal with smaller diagnostics industry participants such as Revvity, Waters Corp, and Qiagen. More details on this matter are to be provided in the summer of 2025.

The plan is to complete this transaction in FY2026; the company’s fiscal year end is at the end of September.

Business Overview

Good sources of information to learn about BDX are its website and its FY2024 Annual Report/Form 10-K.

Financials

Q2 and YTD2025 Results

BDX’s most recent results are accessible here.

The company continues to struggle to consistently deliver strong operating results. Although top line growth is a challenge, it is doing a reasonably good job of mitigating the impact on the bottom line.

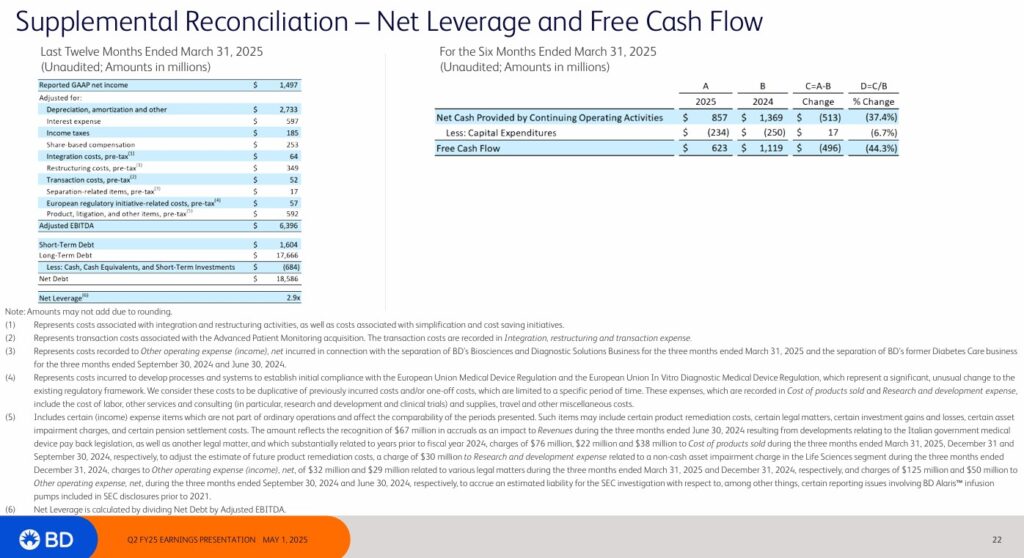

Net leverage (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, and FYE2024 was 2.6x, 2.8x, 2.6x, 2.6x, and 3.0x. This had been reduced to 2.9x at the end of Q2 2025. Management’s expectation, however, is to reduce this to 2.5x within 12 – 18 months.

BDX’s cash generation is weighted to the second half of the fiscal year given the timing of tax and other payments. Tariffs will have a modest impact on cash in the second half, but BDX remains committed to deleveraging.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

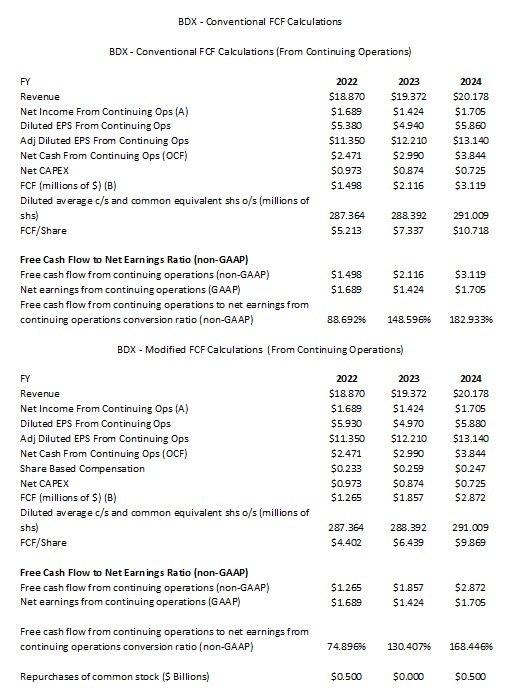

BDX merely deducts CAPEX from its net cash provided by continuing operating activities to determine its FCF. In several prior posts, I explain my rationale for deducting share based compensation (SBC) when determining FCF.

The following table reflects BDX’s FCF using the conventional method used by BDX and the modified method where I deduct SBC. We see from the calculations that FCF exceeds net income from continuing operations in FY2023 and FY2024 but not in FY2022.

In the first half of FY2025, BDX generated $0.857B of cash from continuing operations and incurred CAPEX of $0.234B. SBC in the same 6 month period is $0.149B. Using these YTD2025 figures, BDX’s conventional and modified FCF is $0.623B and $0.474B, respectively. The low first half FCF reflects the timing of planned onetime cash payments.

BDX’s YTD2025 ‘Net Cash Provided by Continuing Operating Activities’ of $0.857B was insufficient to cover $0.234B of CAPEX, debt repayment of ~$0.876B, ~$0.75B for accelerated share repurchases, and ~$0.600B for dividend distributions which total $2.46B. The difference between $2.46B and $0.857B is ~$1.603B.

To come up with the cash to cover this net outflow, BDX’s short-term debt increased $0.34B, its cash and equivalents declined by $1.050B, and its Net maturities and sales of investments was $0.413B for a total of $1.803B. The ~$0.2B variance ($1.803B – $1.603B) is primarily $0.179B ‘Other, net’ investing activities outflows.

BDX provides no FCF guidance. I, however, envision BDX’s FY2025 FCF falling well short of FY2024 FCF.

FY2025 Guidance

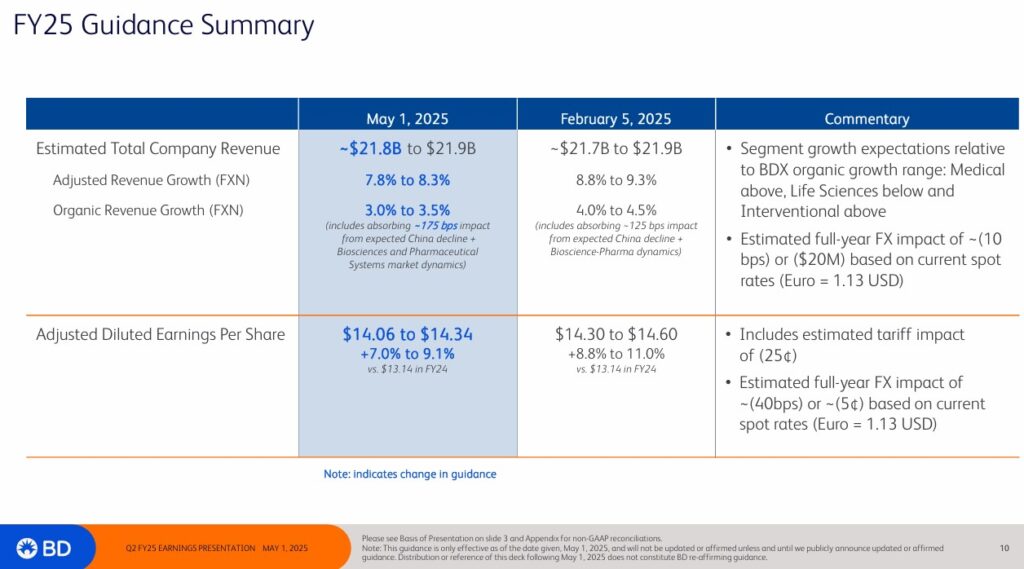

The following is BDX’s current and prior FY2025 guidance.

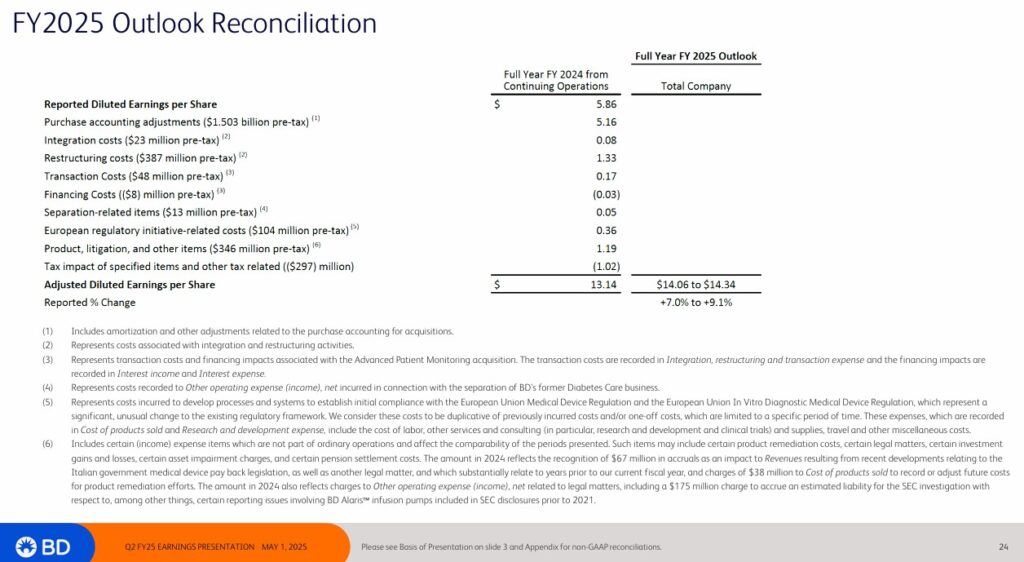

The following reflects BDX’s reconciliation for its current FY2025 guidance. The reconciliation for earlier FY2025 guidance is found in my February 7 post.

Risk Assessment

BDX’s net leverage ratio (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, and FYE2024 was 2.6x, 2.8x, 2.6x, and 3.0x. BDX’s target is under 3.0x. At the end of Q2 2025 is was 2.9x. The commitment is to deleverage to ~2.5x.

There are no changes to BDX’s domestic senior unsecured debt ratings from the time of my most recent prior posts.

All 3 ratings are the middle tier within the lower medium grade category. They define BDX as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity for BDX to meet its financial commitments.

These ratings are satisfactory for my purposes.

Dividend and Dividend Yield

BDX’s dividend history is accessible here.

BDX is somewhat trapped because with 53 consecutive years of dividend increases, its shareholder base EXPECTS dividend increases. If BDX were to re-prioritize its capital allocation and to lower the importance of dividend increases, the shareholder base will most likely revolt. Any dividend cut/freeze would most likely lead to a drop in BDX’s share price.

As per prior posts, a company’s dividend metrics are of little importance in my investment decision making process. My interest lies in the total potential investment return and whether the return is commensurate with the risk I am assuming.

BDX’s share repurchases over the years have been ‘all over the map’. During the FY2010 – FY2024 time frame, BDX repurchased (in $B) 0.75, 1.5, 1.5, 0.45, 0.4, 0, 0, 0.22, 0, 0, 0, 1.75, 0.5, 0, and 0.5 for a total of $7.57B.

The diluted average common shares outstanding (millions of shares) in FY2010 was 240.136. In FY2024, this had ballooned to 291.009 but in Q2 2025, this had been reduced to 287.737.

In addition to the issuance of shares as part of its various SBC programs, BDX has made several acquisitions (eg. Carefusion, C.R. Bard, Parata Systems, Edwards LifeSciences’ Critical Care) over the years. These acquisitions have been funded through the use of debt and the issuance of new shares. A history of BDX’s recent mergers and acquisitions is accessible here.

The years in which BDX repurchased no shares (or few shares) is because the priority was to reduce debt taken on for acquisition purposes.

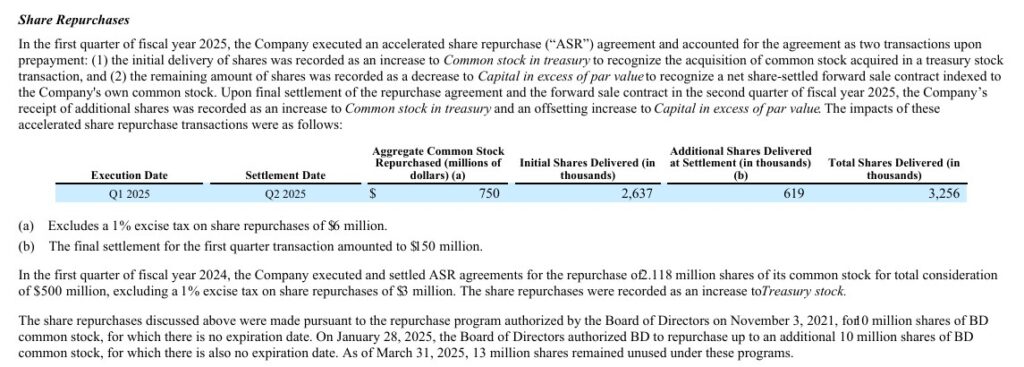

The following information about BDX’s share repurchases is extracted from the Q2 2025 Form 10-Q.

Valuation

In my February 7, 2025 post, I touch upon the significant variances between BDX’s GAAP and non-GAAP earnings for the past decade. The variances are primarily attributed to purchase accounting adjustments, restructuring costs, and integration costs. There may have been variances prior to BDX embarking on the path of major acquisitions (the first major acquisition post Financial Crisis was the 2015 acquisition of Carefusion) but nothing like in FY2015 – FY2024. In the past decade, BDX has reported significant earnings adjustments. At some point in time, investors begin to wonder whether these adjustments should really be considered ‘adjustments’ or whether there are really part of normal business operations.

With the BD2025 strategy nearing its end, I hope these annual adjustments become less significant.

In my February 7, 2025 post I wrote:

Using management’s revised FY2025 outlook of ~$14.30 – ~$14.60 adjusted diluted EPS and my ~$226.86 purchase price, the forward adjusted diluted PE range is ~15.5 – ~15.9.

BDX’s current forward adjusted diluted PE levels using the adjusted diluted EPS broker estimates are:

- FY2025 – 15 brokers – mean of $14.41 and low/high of $14.12 – $14.53. Using the mean, the forward adjusted diluted PE is ~15.74.

- FY2026 – 15 brokers – mean of $15.66 and low/high of $15.33 – $15.92. Using the mean, the forward adjusted diluted PE is ~14.48.

- FY2027 – 6 brokers – mean of $16.94 and low/high of $16.61 – $17.42. Using the mean, the forward adjusted diluted PE is ~13.4.

Revisions to these estimates are likely over the next several days.

BDX’s YTD FY2025 FCF falls short of its Q1 disbursements (share repurchases, debt repayment, and dividends). I, however, envision an improvement in FCF over the remainder of the current fiscal year.

Following the separation of the Biosciences & Diagnostic Solutions segment in FY2026, I expect proceeds from the separation will be reinvested in the business (acquisition, debt reduction, share repurchases). At this point, I have no way of determining BDX’s financials post FYE2026 and am merely hoping management will do what is best for its shareholders.

Management’s revised FY2025 outlook now calls for ~$14.06 – ~$14.34 of adjusted diluted EPS. With the share price having plunged to ~$169.60 at the May 1, 2025 close, the forward adjusted diluted PE range is ~11.8 – ~12.06.

Using the adjusted diluted EPS broker estimates, BDX’s forward adjusted diluted PE levels are:

- FY2025 – 15 brokers – mean of $14.29 and low/high of $14.08 – $14.45. Using the mean, the forward adjusted diluted PE is ~11.9.

- FY2026 – 15 brokers – mean of $15.29 and low/high of $14.27 – $15.76. Using the mean, the forward adjusted diluted PE is ~11.1.

- FY2027 – 10 brokers – mean of $16.46 and low/high of $15.39 – $17.05. Using the mean, the forward adjusted diluted PE is ~10.3.

With no FY2025 FCF guidance provided by management and only $0.623B and $0.474B of conventional and modified FCF generated in the first half of the year, I estimate that FY2025 conventional and modified FCF might only be ~$1.6B and ~$1.2B given that cash generation is weighted to the second half of the fiscal year.

If the weighted average diluted shares outstanding in FY2025 drops to ~286 million from 287.737 million in the first half of the year, BDX’s FCF/share is ~$5.60 (~$1.6B/~286 million) and ~$4.20 (~$1.2B/~286 million) calculated using the conventional and modified FCF methods. Using the current ~$169.60 share price, the forward P/FCF is ~30.3 and ~40.4.

Final Thoughts

BDX was my:

- 27th largest holding when I completed my 2023 Year End Review;

- 24th largest holding when I completed my 2024 Mid Year Review; and

- 25th largest holding when I completed my 2024 Year End Review.

It is entirely possible that it is no longer a top 30 holding.

As noted earlier, my medical instruments and supplies and life sciences and diagnostics holdings are struggling of late. Nevertheless, I still like these companies as long-term holdings and within the past few months have increased my exposure in A, BDX, DHR, ISRG, and TMO.

Many investors have lost confidence in BDX as it has yet to demonstrate strong organic sales growth. I remain confident it is making the right strategic decisions and upon completion of the separation of the Biosciences and Diagnostics business, I anticipate an improvement in BDX’s results.

While tempting to increase my BDX exposure at the current valuation, I will stick my the current 639 shares held in one of the ‘Core’ accounts within the FFJ Portfolio. My plan is to deploy cash sitting on the sidelines toward the purchase of additional shares in other companies once I find their valuation to be appealing.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BDX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.