Buy undervalued Danaher (DHR) shares amid market challenges.

In my December 8, 2024 Danaher (DHR) post, I disclose the purchase of an additional 100 shares in a ‘Core’ account in the FFJ Portfolio. My ~$233.97 purchase price was just a shade above the ~$229 price I paid to acquire 100 additional shares on November 18.

Following the release of DHR’s Q4 and FY2024 results on January 29, 2025, DHR’s share price plunged from the previous day’s ~$247.80 closing share price. After reviewing DHR’s results and FY2025 outlook, I acquired an additional 100 shares @ ~$226.47. I now hold 800 DHR shares in the FFJ Portfolio.

Business Overview

I reference my December 19 post in which I provide a brief business overview. The best way to learn about DHR, however, is to read its Form 10-K that is accessible through the SEC Filings section of the company’s website.

Financials

Q4 and FY2024 Results

Refer to the material available in the Quarterly Earnings section of DHR’s website.

Underwhelming is an accurate interpretation of DHR’s FY2024 results. FY2024 revenue was flat relative to FY2023 and adjusted operating margin and adjusted diluted EPS slipped relative to FY2023.

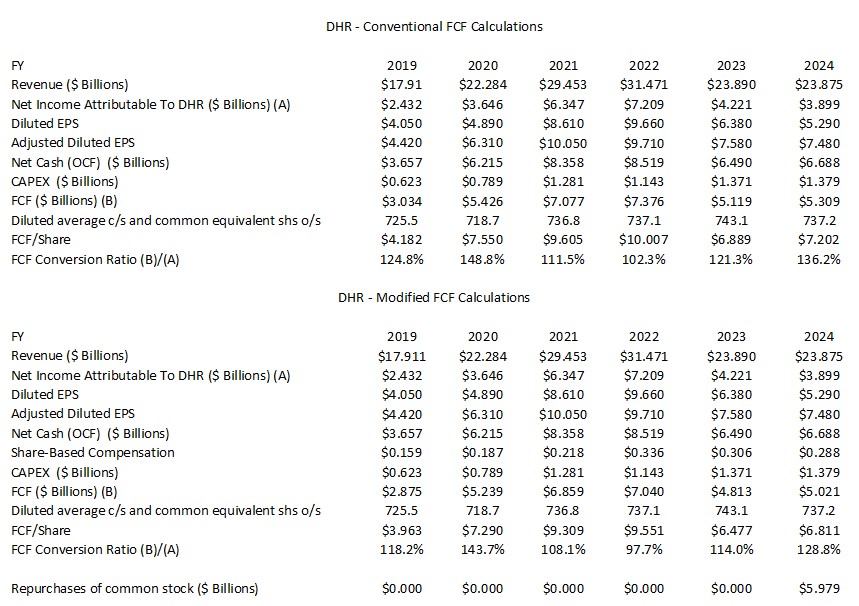

On a positive note, FCF increased 3.5% to $5.309B versus $5.119B in FY2023.

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2020 – FY2024)

In several recent posts I express my thoughts about the way many companies calculate Free Cash Flow (FCF). Since FCF is a non-GAAP metric, there is no standardization in its calculation.

In most cases, companies merely deduct net CAPEX from net cash flows from operating activities. I think it is also necessary to deduct share based compensation (SBC).

Many companies employ SBC as part of their employee compensation plans and reflect this cost within the Income Statement. Because SBC involves no cash outlay, however, companies add back SBC to determine net cash flows from operating activities in the Condensed Consolidated Statement of Cash Flows.

Suppose, however, that DHR were to compensate employees 100% by way of SBC. Since there is no cash outlay, the full amount of its employee compensation is added back in the Condensed Consolidated Statement of Cash Flows to determine net cash flows from operating activities.

If, on the other hand, DHR were to have no SBC and were to actually disburse funds to pay its employees, nothing would be added back in the Condensed Consolidated Statement of Cash Flows.

By merely changing the manner in which it compensates its employees we get very different net cash flows from operating activities! How does this make any sense? Is the use of SBC not a form of ‘financing’? Would it be more proper to reflect SBC within the Cash Flows From Financing Activities section of the Condensed Consolidated Statement of Cash Flows? This way, we would arrive at similar FCF results no matter how a company chooses to compensate its employees.

The following table reflects data extracted from the FY2019 – FY2024 reconciliation of GAAP and non-GAAP financial measures and supplemental forward-looking information documents that are accessible here. The section with the modified FCF calculations deducts share based compensation (SBC) from total operating cash provided by continuing operations.

Strong free cash flow generation is one of the most important metrics at DHR. FY2024 marks the 33rd consecutive year of FCF to net income conversion which exceeds 100%. If we deduct SBC to determine FCF, however, DHR just fell short of 100% in FY2022.

FY2025 Outlook

DHR provides forecasted sales only on a non-GAAP core revenue basis. This is because of the difficulty in estimating the other components of GAAP revenue (eg. currency translation, acquisitions, and divested product lines).

For Q1 2025, DHR anticipates that non-GAAP core revenue will decline low-single digits YoY. For FY2025, it expects that non-GAAP core revenue will increase ~3% YoY. This outlook includes 6% – 7% growth in biotechnology. Life science (low-single digit) and diagnostic (flat to low-single-digit) growth, however, both remain weak.

Pricing pressure in China diagnostics, weak respiratory results, negative exchange-rate effects, and a higher tax rate are likely to depress earnings. Modest adjusted EPS growth in FY2025, however, is likely. Most of this growth is likely to be the result of significant shares repurchases in FY2024 and FY2025.

Risk Assessment

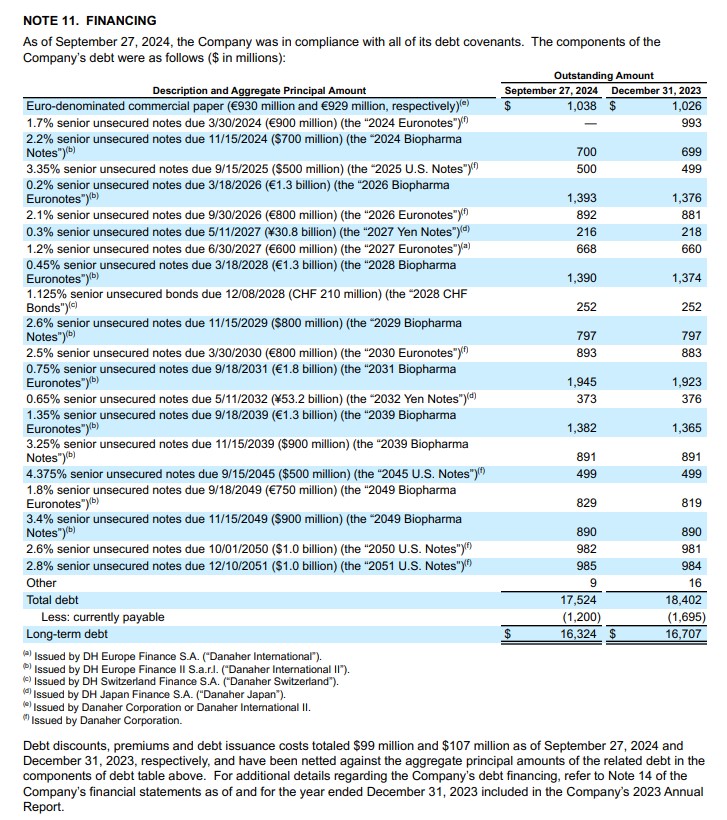

The following schedule reflects DHR’s long term debt at the end of Q3 2024. In comparison, the current portion of DHR’s debt was $0.505B and the long-term debt was $15.5B at FYE2024.

DHR borrows at very attractive rates and the scheduled maturity dates are well staggered.

DHR’s credit ratings are unchanged from my last review.

- Moody’s: Upgraded to A3 from Baa1 on October 10, 2022. This rating was last reviewed on June 18, 2024 and the outlook remains stable.

- S&P Global: Upgraded to A- from BBB+ on June 11, 2022. This rating was last reviewed on June 11, 2024 and the outlook remains stable.

Both ratings are at the bottom tier of the upper-medium investment-grade tier and define DHR as having a STRONG capacity to meet its financial commitments. However, DHR is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

These ratings satisfy my conservative investment profile.

Dividend and Dividend Yield

DHR’s quarterly dividend is likely to remain a negligible portion of the total investment return. Do not, however, fixate on dividend metrics. Focus on total potential long-term investment returns!

DHR will distribute its 4th consecutive $0.27/share quarterly dividend on January 31, 2025.

When it declared its quarterly dividend in December 2023 for distribution at the end of January 2024, it lowered the quarterly dividend to $0.24. This arose because of the Veralto spin-off. The $0.27/share quarterly dividend, however, was restored with the declaration of the dividend payable on April 26, 2024.

There were 710.2, 725.2, 718.7, 736.8, 737.1, and 743.1 million diluted average common stock and common equivalent shares outstanding in FY2018 – FY2023. In Q4 2023 and 2024, the diluted weighted average shares outstanding was 746.1 and 728.2.

The increase in recent years is primarily the result of the conversion of On April 15, 2022, all outstanding shares of the 4.75% MCPS Series A converted and on April 15, 2023, the 5% MCPS Series B converted.

On July 22, 2024, DHR’s Board approved a new repurchase program authorizing the repurchase of up to an additional 20 million shares of common stock from time to time on the open market or in privately negotiated transactions.

In several recent years, DHR has repurchased no shares. In FY2024, it repurchased $5.979B of its shares.

On the Q4 earnings call, management states that in FY2024 and into the start of 2025, DHR deployed ~$7B of capital toward the repurchase of 28 million shares. This includes ~20 million shares purchased in Q2 and Q3 and ~8 million shares purchased in Q4 and into January 2025.

Hopefully DHR’s share price will remain depressed thus enabling it to continue to aggressively repurchase shares.

Valuation

DHR generated $6.38 and $7.38 of diluted EPS and adjusted diluted EPS in FY2024. Both are greater than what I anticipated when I wrote my December 8 post. Using my January 29 $226.47 purchase price, the diluted PE and adjusted diluted PE are ~35.5 and ~30.7.

DHR’s valuation using the current broker guidance is:

- FY2025 – 27 brokers – mean of $7.79 and low/high of $7.57 – $8.55. Using the mean, the forward adjusted diluted PE is ~29.1.

- FY2026 – 25 brokers – mean of $8.72 and low/high of $8.20 – $10.00. Using the mean, the forward adjusted diluted PE was ~26.

- FY2027 – 12 brokers – mean of $9.72 and low/high of $8.92 – $11.40. Using the mean, the forward adjusted diluted PE was ~23.3.

- FY2028 – 6 brokers – mean of $10.93 and low/high of $10.12 – $11.70. Using the mean, the forward adjusted diluted PE was ~20.7.

DHR typically reports significant depreciation and amortization expenses every year which depresses earnings; in FY2023 and FY2024, it reported ~$2.174B and ~$2.377, respectively. It also reported ~$0.265B in impairment charges related to an indefinite-lived trade name within the genomics consumable business included in the Life Sciences segment. This determination was primarily the result of softness in the genomics market, including but not limited to the discontinuation of drug development programs announced in the third quarter and weaker demand at some of the business’s larger customers as well as reduced demand due to the reprioritization of drug development programs at other customers.

DHR consistently reports significant non-cash items that depress earnings. Management also focuses very heavily on the FCF metrics. Investors would, therefore, be wise to look at DHR’s valuation based on FCF.

Using my January 29 $226.47 purchase price and $7.202 of FCF/share in FY2024 (conventional FCF calculation), the P/FCF is ~31.4. Using $6.811 of FCF/share in FY2024 (modified FCF calculation), the P/FCF is ~33.3.

Final Thoughts

DHR was my:

- 28th largest holding when I completed my 2023 Year End FFJ Portfolio Review;

- 22nd largest holding when I completed my 2024 Mid Year FFJ Portfolio Review; and

- 19th largest holding when I completed my 2024 Year End FFJ Portfolio Review.

DHR continues to experience short-term headwinds and management’s FY2025 outlook suggests investors should not expect much of a rebound.

On the bright side, DHR’s capital allocation is exemplary. While DHR’s share price is under pressure, the company is repurchasing a significant number of shares.

Once growth trends normalize, I think DHR will be able to generate low double-digit earnings growth; this is unlikely to begin until 2026 – 2027 at the earliest.

DHR’s share price could slip further from current levels. At $226.47, however, I stand to have capital appreciation of ~17% if DHR’s share price improves to ~$265 – a level I consider fair.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long DHR.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.