Much has changed following my last Brookfield post on August 13, 2022 post.

On December 9th, 2022, Brookfield completed a distribution and listing of 25% of its asset management business – Brookfield Asset Management Ltd. (BAM). This distribution created two distinct businesses thus enabling shareholders to access a leading pure-play global alternative asset management business, through the Manager. Brookfield Corporation (BN), on the other hand, would continue to focus on allocating capital across the business and growing its cash flows.

Information explaining the rationale for the creation of two publicly traded companies is provided in various documents.

The Q3 2022 Letter To Shareholders states:

BAM

The Manager is increasingly diverse and growing faster than ever. By year-end, we plan to have distributed and listed a 25% interest in it, creating optionality for you to own our pure-play leading alternative asset manager. Initially, we expect it to generate approximately $2 billion of distributable earnings, pay out approximately 90% of that in cash dividends, and have no debt (actually net cash of $3 billion). If we achieve our growth plans, over the next five years we should double distributable earnings—and we plan to return over 90% of that to shareholders through dividends.

BN

The Corporation, post spinoff, will own circa $150 billion of private and listed investments, including a 75% interest in the newly listed Manager. As a result, we will have one of the largest discretionary pools of alternative assets globally. The Corporation will not face any restrictions on how we use this capital, and our sole focus will be on allocating capital among our operating businesses and new business initiatives, while targeting a 15%+ total return for our shareholders over the long term. We will leverage the Manager to source investment opportunities and opportunistically look to grow our business as opportunities arise. In this environment, we feel the odds favor something large and interesting showing up.

Additional information is provided in various additional documents.

November 9 2022 Notice of Special Meeting of Shareholders and Management Information Circular

Q4 2022 Letter To Shareholders

December 9, 2022 Press Release

With the release of BAM’s Q2 and YTD2024 results on August 7, I revisit this existing holding.

BN released its Q2 and YTD2024 results on August 8. I intend to publish a post once my schedule becomes less hectic.

Business Overview

Brookfield is one of the world’s largest asset managers in what is a highly competitive and highly fragmented industry.

Many asset managers will likely fall by the wayside over the coming years. The larger industry participants such as Brookfield, Blackstone, BlackRock, KKR, Apollo Global Management, however, should continue to thrive. These firms have the reputation and track record of success that enable them to raise funds from sophisticated investors to engage in transactions the smaller industry participants are unable to handle.

I can not give justice to explaining BAM in this post. It is preferable you read BN’s FY2023 Annual Report. The BN website also provides a good overview of this conglomerate. The component of BN’s website that is specific to BAM provides additional information.

Oaktree Capital Management

In September 2019, BAM announced the completion of its acquisition of ~61.2% of Oaktree Capital Group. Additional information about Oaktree is accessible here.

At FYE2022 and FYE2023, this ownership interest had increased to ~64% and ~68%, respectively. In April 2024, BAM acquired an additional 5% interest in Oaktree bringing its ownership stake to ~73%.

Financials

Q2 and YTD2024 Results

Refer to the August 7, 2024 earnings release and supporting material.

Net income for BAM, the publicly traded entity, totaled ~$0.124B in Q2 2024 versus ~$0.109B in Q2 2023. BAM owns a ~27% interest in Brookfield Asset Management, the asset management business with the other ~73% owned by Brookfield Corporation.

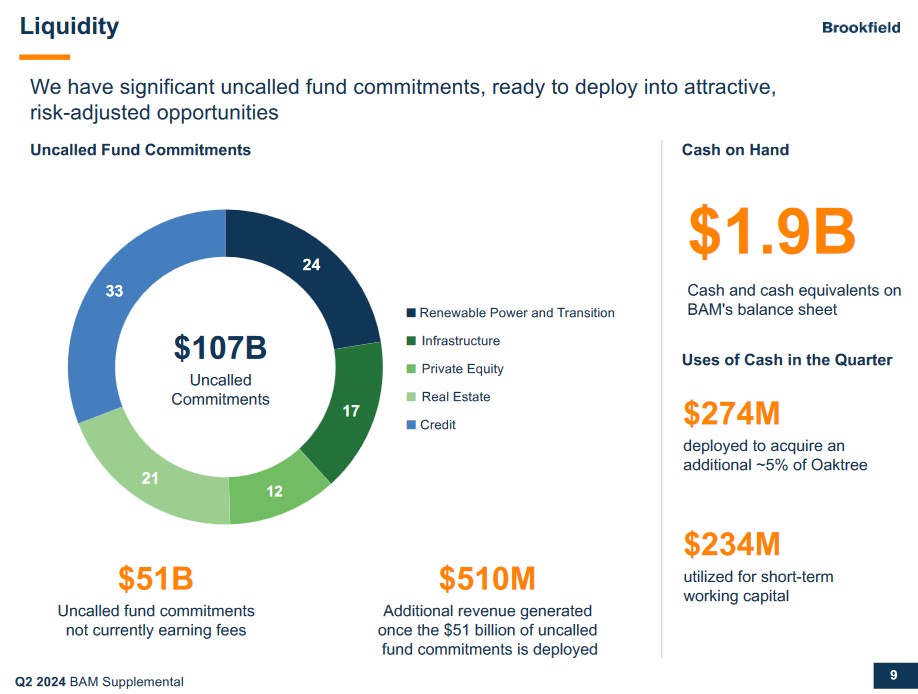

At the end of Q2 2024 there was a total of ~$107B of uncalled fund commitments. These uncalled fund commitments include ~$51B which is not currently earning fees. Once deployed, however, it will earn ~$0.51B of fees annually.

BAM also held ~$1.9B of cash and equivalents on its balance sheet at the end of Q2.

BAM is able to maintain strong and consistent fundraising levels due to the diversity of its capabilities globally and through access to many different forms of capital.

Although equity markets have been somewhat volatile of late, risk appetite and liquidity in capital markets are strong.

Source: BAM – 2023 Investor Day Presentation – September 12, 2023

Risk Assessment

No rating agency rates BAM’s debt. The ratings are assigned to BN and are currently:

- Moody’s: A3 with a stable outlook and rating affirmed on April 10, 2024

- S&P Global: A- with a stable outlook and rating affirmed on April 16, 2024

- Fitch: A- with a stable outlook and rating affirmed on October 27, 2023

All 3 ratings are the lowest tier of the of the upper medium grade investment grade category. These ratings define BN as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Dividends and Share Repurchases

Dividend and Dividend Yield

BAM’s 2023 – 2024 dividend history is accessible here.

BAM’s Board declared a quarterly dividend of USD $0.38/share payable on September 27, 2024 to shareholders of record as of the close of business on August 30, 2024. This marks the 3rd consecutive quarterly dividend at this level.

BAM aims to return 90% – 100% of its Distributable Earnings (DE) to its shareholders in the form of a dividend or share repurchases. If BAM achieves its 5-year growth target, BAM investors are going to be richly rewarded.

Share Repurchases

BAM opportunistically increases shareholder returns with share repurchases. These repurchases, however, are often partially offset by increases in additional paid-in-capital related to stock

based compensation plans.

Valuation

I typically look at:

- diluted EPS – P/E;

- adjusted diluted EPS – adjusted P/E; and

- Free Cash Flow (FCF) – P/FCF

metrics to gauge the valuation of most companies I analyze. These metrics, however, are of little relevance when trying to assess the performance and outlook of asset managers.

BAM uses non-GAAP measures such as Distributable Earnings (DE), Fee-Bearing Capital, Fee-Related Earnings (FRE), Liquidity, and Capital Resources, to more accurately measure its performance. A Glossary of Terms is found on pages 36 – 37 in the Q2 2024 Supplemental Information.

BAM is not easy to value. It raises large pools of capital from clients for deployment and several multi-billion-dollar acquisitions are generally made annually. In addition, BAM is in no hurry to sell assets and will refrain from selling during unfavorable conditions. A quarter in which asset sales are low following the same quarter in the prior year when asset sales were high can result in a significant YoY variance. It is, therefore, of utmost importantance to analyze BAM’s long term performance.

Over the long-term, the non-GAAP metrics reflected above have improved.

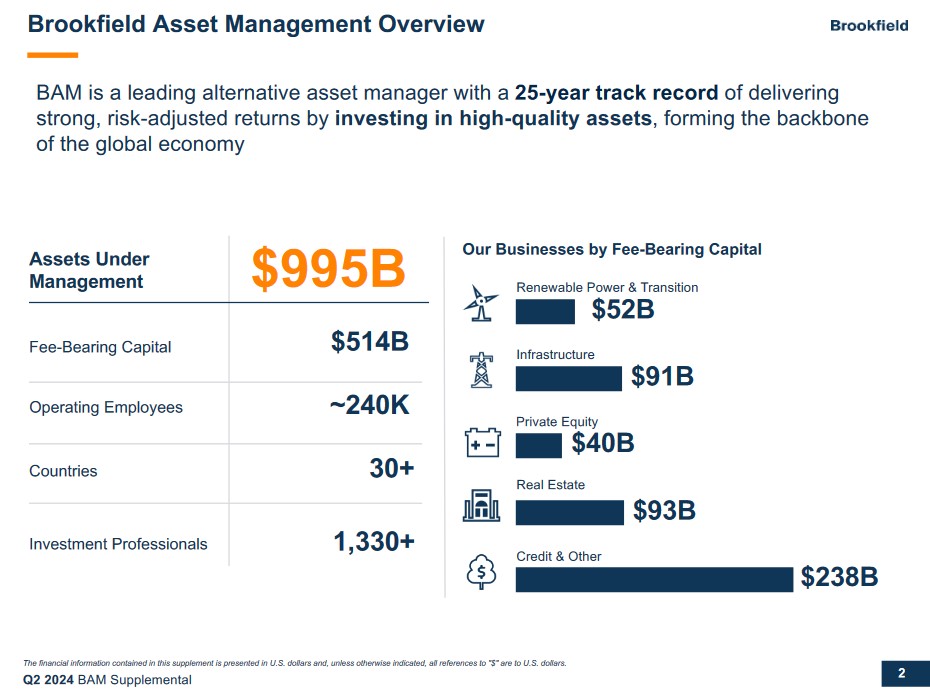

Given that growth in Assets Under Management (AUM) is more than likely to lead to higher DE and FRE, it is encouraging to see the growth in AUM:

- August 13, 2020 : ~$550B; and

- Q2 2024: ~$995B.

Final Thoughts

The Brookfield conglomerate is far too complex to cover in a brief post; I recommend you read the material for which I have provided links earlier in this post.

If you do not have the bandwidth to review all this information, consider that Brookfield’s expertise and a track record of success is leading sophisticated investors to commit more money to BAM for investment purposes.

Brookfield’s mandate is to generate attractive returns for its sophisticated investor while controlling risk. In addition to earning fees for its efforts, BAM stands to participate further when target returns are achieved. In essence, BAM’s compensation structure provides the required incentive to perform exceptionally well. Naturally, not every investment will be a success. BAM, however, has so many investments on the go at any one time that the occasional setback is not a death knell.

At the September 12, 2023 Investor Day, management set a 5-year growth target to more than double DE to $5B by 2028. This growth will come from increasing Fee-Bearing Capital, which is expected to reach $1T over the next 5 years.

Source: BAM – 2023 Investor Day Presentation – September 12, 2023

My decision making process when it comes to investing in BAM, Blackstone (BX), and BlackRock (BLK) is fairly simplistic. I want private equity exposure, however, require the expertise of asset managers with a proven track record of success.

When I completed my 2023 Year End FFJ Portfolio Review, I had exposure to various Brookfield entities. My aggregate exposure to these entities resulted in ‘Brookfield’ being my 11th largest holding.

On June 5, 2024, however, I was ‘forced’ to sell 100% of my ‘Brookfield’ exposure in a particular ‘Side’ account within the FFJ Portfolio for tax planning purposes; I disclosed this in my June 11 post. I never intended to sell BAM shares but the Canadian government’s decision to change the tax treatment of capital gains forced my hand.

One of these sales was 157 Brookfield Asset Management Ltd. shares (the TSX listed shares) for which I received @ CDN$53.92/share.

The sale of shares in several ‘Brookfield’ entities resulted in its ranking dropping to 23rd when I completed my 2024 Mid Year FFJ Portfolio Review.

I have made a deliberate decision to limit my exposure to just 6 Canadian companies; Brookfield Asset Management Ltd. and Brookfield Corporation are two of these companies.

Following the release of BAM’s Q2 2024 results on August 7, I purchased 500 BAM shares @ CDN$53.814 through a ‘Side’ account in the FFJ Portfolio.

BAM and BN will hold their Investor Day on September 10. All BAM/BN affiliates will hold their Investor Day on September 24.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BAM, BN, BX, and BLK.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.