In several previous posts I have touched upon our need to ‘meltdown’ our Registered Retirement Savings Plans (RRSP) before the mandatory date by which they are automatically converted to Registered Retirement Income Funds (RRIF); the deadline by which a RRSP must be converted to a RRIF is by December 31 of the year the RRSP owner turns 71. Fortunately, we have a number of years to go before we turn 71 which gives us time to use the strategy.

Unless we meltdown our RRSPs, we will face minimum mandatory annual RRIF withdrawals that place us in the highest tax bracket.

Following the completion of our 2023 tax returns in April 2024, my wife and I each withdrew ‘$X’ from our respective RRSPs; we rely heavily on guidance from our tax accountants.

The performance of our RRSP holdings has been exceptional this year. Our tax accountants have, therefore, recently instructed us to make further withdrawals prior to calendar year end.

I identified Broadridge as an overvalued company and sold shares @ $231.4316/share on December 3.

Given my recent sale and the fact I last reviewed BR in this August 7, 2024 post, I revisit this existing holding.

Business Overview

BR operates in two reportable segments, Investor Communication Solutions (ICS) and Global Technology and Operations (GTO), which are both highly competitive.

The majority of BR’s clients operate in the financial services industry. Its largest single client in FY2021, FY2022, FY2023, and FY2024 accounted for ~6%, ~7%, 7%, and 8% of consolidated revenues.

Part 1 Item 1 in the FY2024 Form 10-K is a good source of information to learn about the company.

The December 7, 2023 Investor Day Presentation in which BR includes its new 3-year growth objectives for FY2024 – FY2026 is also an excellent source of information.

Financials

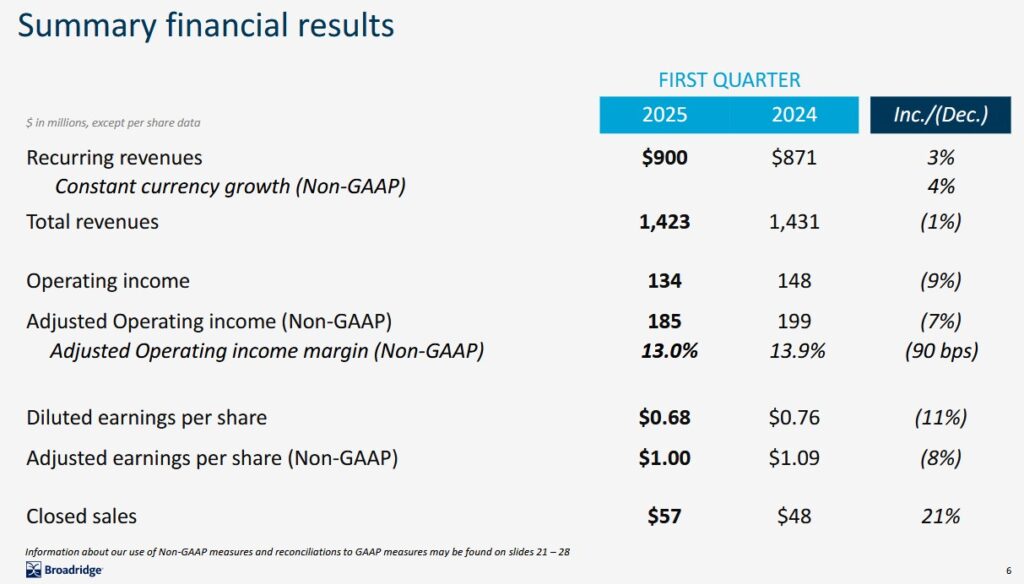

Q1 2025 Results

Material related to BR’s Q1 2025 is accessible here. Q1 is typically a weak quarter so investors should not read too much into these results.

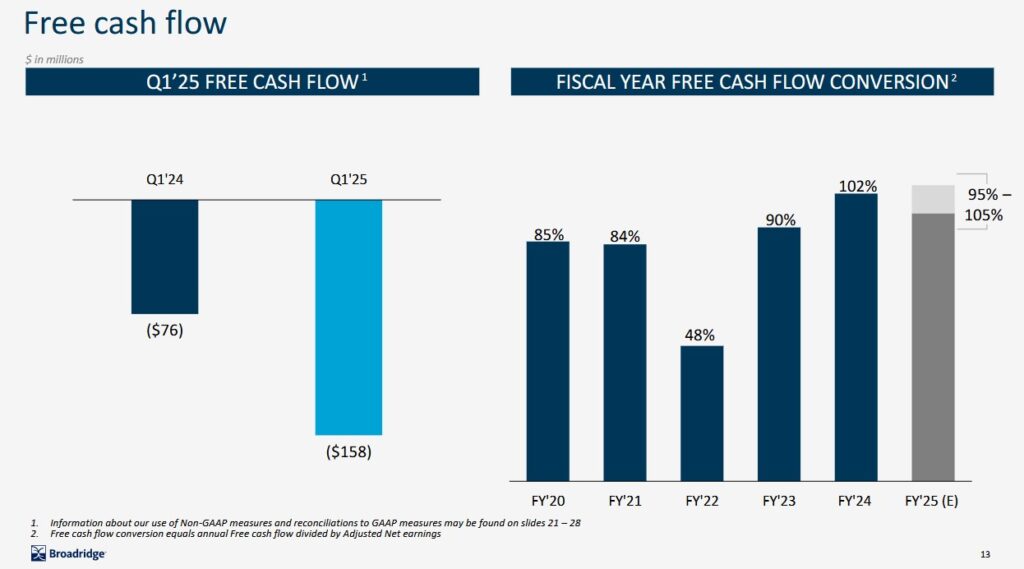

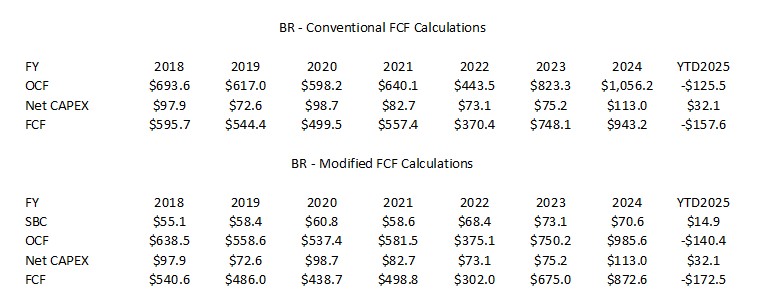

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

FCF is a non-GAAP measure so the manner in which companies calculate FCF is not standardized. In most cases, companies will deduct CAPEX from Net cash flows from operating activities. Following this method of calculation FCF, BR reports FCF as reflected below.

Many companies employ the use of share based compensation (SBC) as part of their employee compensation plans. This cost is reflected in the Income Statement. Because SBC involves no cash outlay, however, the SBC is added back to determine Net cash flows from operating activities.

Suppose, BR were to compensate their employees 100% by way of SBC. Since there is no cash outlay, the full amount of its employee compensation is added back in the Condensed Consolidated Statement of Cash Flows to determine Net cash flows from operating activities.

If, on the other hand, BR were to have no SBC and were to disburse funds to pay its employees, nothing would be added back in the Condensed Consolidated Statement of Cash Flows.

By merely changing the manner in which it compensates its employees we get very different Net cash flows from operating activities! How does this make any sense? Is the use of SBC not a form of ‘financing’? Would it be more proper to reflect SBC within the Cash Flows From Financing Activities section of the Condensed Consolidated Statement of Cash Flows? This way, FCF would not be distorted.

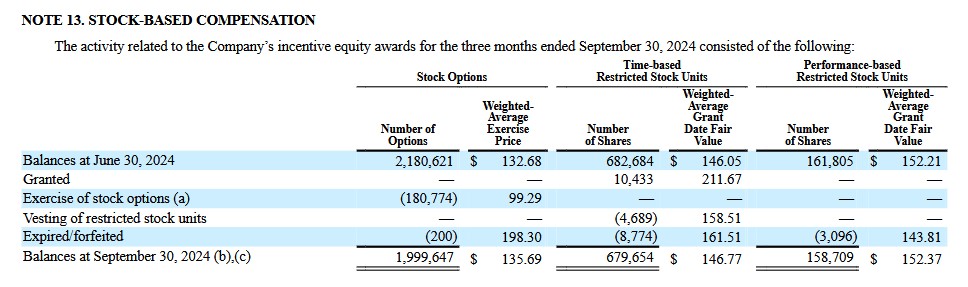

In the Q1 2025 Form 10-Q we see the following on page 23 of 75.

BR may have improved its cash flow by issuing stock options and restricted share units (RSUs) but at some point in time, a ton of shares are going to be issued to my detriment.

I recognize a company might have to increase wages and salaries if it eliminates the SBC component of its compensation programs. At least, however, I know the extent of employee remuneration. Right now, however, it looks like some employees are going to ‘make out like bandits’. Although BR may on occasion repurchase shares to partially offset the shares issued under the SBC programs, I am certain the purchase prices are nothing remotely close to the exercise prices reflected above.

BR’s SBC pales in comparison to that of some technology companies which are notorious for having a sizable component of employee compensation in the form of SBC.

An increasing number of companies (eg. Salesforce, Workday, Zoom) that rely on SBC as part of their employee compensation are coming to the realization that their SBC compensation programs are not sustainable; the weighted average number of diluted shares outstanding have risen dramatically in recent years.

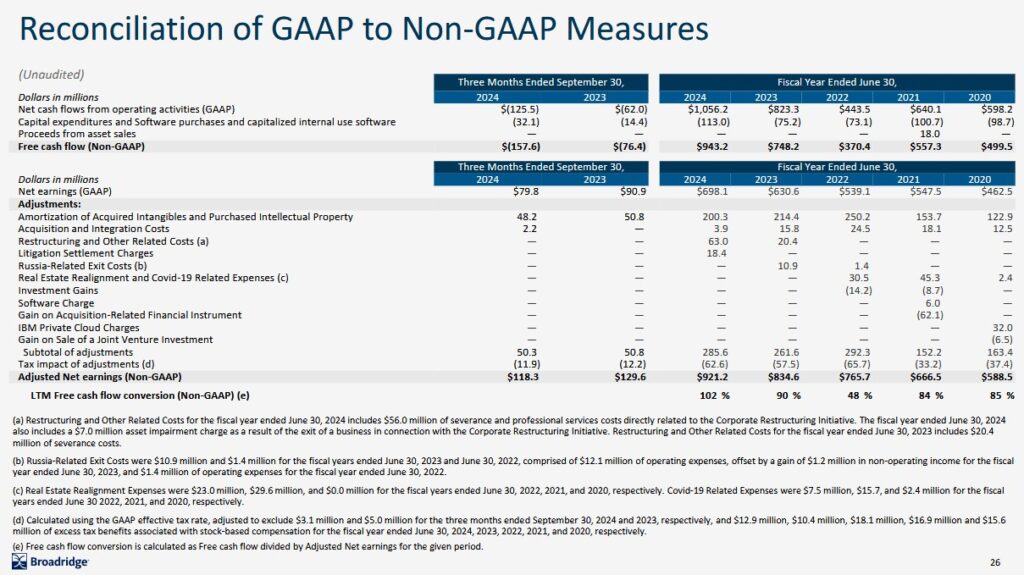

After reading much about the flaws with the ‘conventional’ method of calculating FCF, I have decided to use a much more conservative method. The following reflects FCF using the ‘conventional’ method and my ‘modified’ version.

BR’s FCF is less than what it reflects on its earnings presentations.

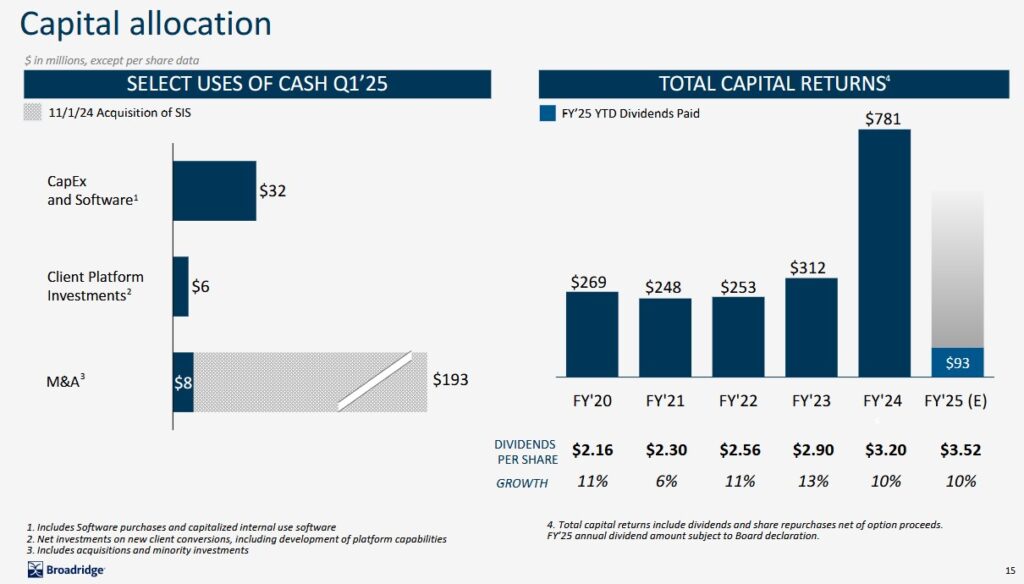

Capital Allocation

In FY2024, the return of capital in the form of share repurchases (~$0.485B) and dividend distributions (~$0.368B) was more balanced than in prior years.

Q1 is typically a challenging quarter so the capital allocation was ~$0 toward share repurchases and ~$0.093B toward dividend distributions.

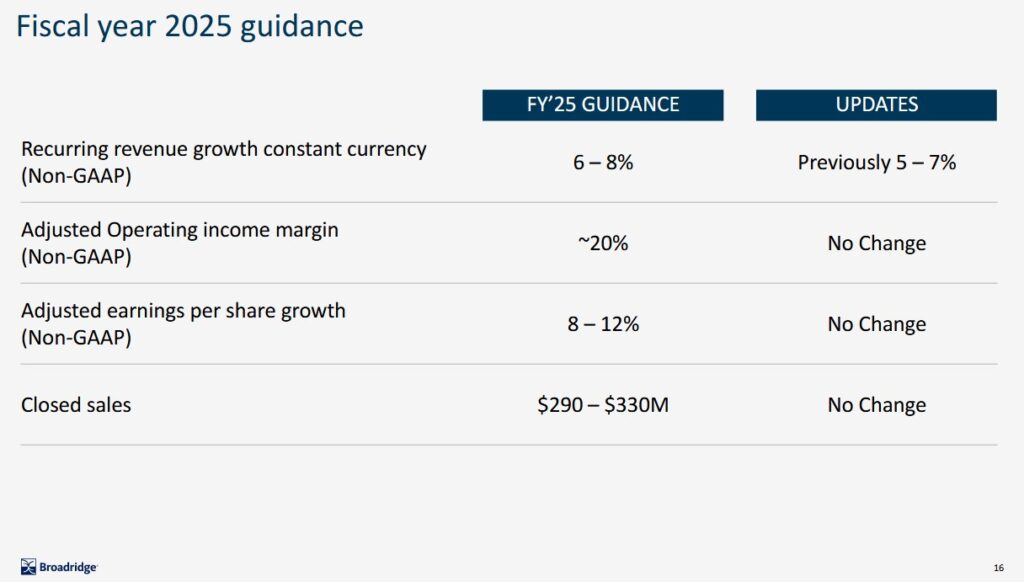

FY2025 Guidance

The following reflects BR’s current and prior FY2025 guidance.

BR increased recurring revenue growth outlook reflects the acquisitions I touched upon in my prior post.

The organic recurring revenue growth of 6% – 7% over the next 3 quarters is to be driven by a $0.450B sales backlog, mid- to high single-digit position growth and the lapping of the E-Trade deconversion.

Risk Assessment

Note 11 within the Q1 2025 Form 10-Q starting on page 20 of 75 has details of BR’s credit facilities.

All BR’s domestic senior unsecured debt ratings are at the top tier of the lower-medium grade investment-grade category. There is no change from the time of my last review.

- Moody’s: Baa2 with a stable outlook. This rating was downgraded from Baa1 on May 15, 2023;

- S&P Global: BBB with a stable outlook. This rating was downgraded from BBB+ on June 13, 2023;

- Fitch: BBB+ and a stable outlook and affirmed on June 21, 2024. This rating is unchanged from the time of my prior reviews.

These ratings define BR as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Despite the rating downgrades, BR’s credit risk remains acceptable for my purposes.

Dividends and Share Repurchases

Dividend and Dividend Yield

On November 14, 2024, BR’s Board declared a quarterly dividend of $0.88/share payable on January 3, 2025 to stockholders of record on December 13, 2024.

BR’s dividend history does not currently reflect this increase as I compose this post.

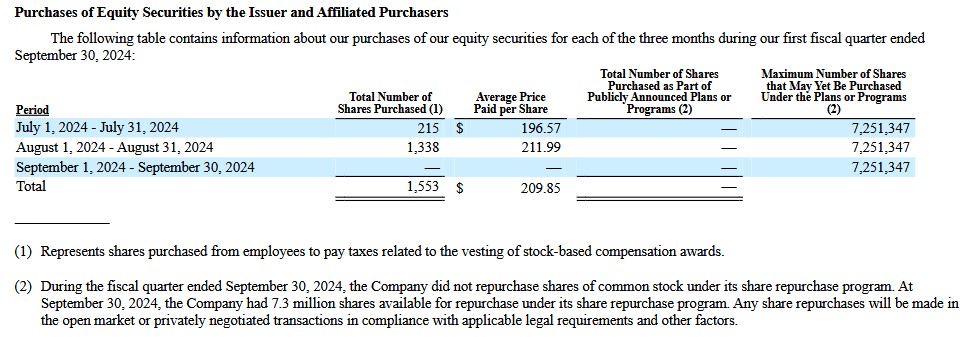

Share Repurchases

The weighted average shares outstanding in FY2012 – FY2024 (in millions rounded) are 128, 125, 124, 124, 122, 121, 120, 119, 117, 118, 119, 119, and 119. In Q1 2025, it was 118.1.

The following reflects BR’s share repurchase activity in Q1 2025.

Valuation

When I wrote my August 7, 2024 post, BR had just reported FY2024 GAAP EPS and non-GAAP EPS of $5.86 and $7.73. Using the August 6 $218.55 closing share price, the diluted PE and adjusted diluted PE were ~37.3 and ~28.3.

The FY2025 outlook called for 8% – 12% growth in non-GAAP EPS or ~$8.35 – ~$8.66 thus giving us a forward adjusted diluted PE of ~25.2 – ~26.2.

BR’s valuation using the current broker guidance at the time was:

- FY2025 – 6 brokers – mean of $8.44 and low/high of $8.35 – $8.56. Using the mean, the forward adjusted diluted PE is ~25.9.

- FY2026 – 6 brokers – mean of $9.27 and low/high of $9.16 – $9.42. Using the mean, the forward adjusted diluted PE was ~23.6.

- FY2027 – 1 brokers – mean of $10.10 and low/high of $10.10 – $10.10. Using the mean, the forward adjusted diluted PE was ~21.6.

Using FCF in the manner BR calculates it, the FY2025 FCF target was ~95% – ~105%.

If the FCF conversion ended up being 95% of the non-GAAP EPS FY2025 outlook of ~$8.35 – ~$8.66, the FY2025 FCF range was ~$7.93 – ~$8.23. With shares trading at ~$218.55, the forward P/FCF range was ~26.6 – ~27.6.

If the FCF conversion ended up being 105% of the non-GAAP EPS FY2025 outlook of ~$8.35 – ~$8.66, the FY2025 FCF range was ~$8.77 – ~$9.09. With shares trading at ~$218.55, the forward P/FCF range was ~24 – ~25.

BR generated $0.68 and $1.00 of diluted EPS and adjusted diluted EPS in Q1 2025. If it meets its FY2025 8% – 12% growth in non-GAAP EPS guidance (~$8.35 – ~$8.66), the forward adjusted diluted PE using the current $235.43 share price is ~27.2 – ~28.2.

BR’s valuation using the current broker guidance is:

- FY2025 – 8 brokers – mean of $8.52 and low/high of $8.45 – $8.57. Using the mean, the forward adjusted diluted PE is ~27.6.

- FY2026 – 8 brokers – mean of $9.37 and low/high of $9.20 – $9.51. Using the mean, the forward adjusted diluted PE was ~25.1.

- FY2027 – 6 brokers – mean of $10.33 and low/high of $10.03 – $10.53. Using the mean, the forward adjusted diluted PE was ~22.8.

If the FCF conversion ends up being 95% of the non-GAAP EPS FY2025 outlook of ~$8.35 – ~$8.66, the FY2025 FCF range was ~$7.93 – ~$8.23. With shares trading at ~$235.43, the forward P/FCF range is ~29 – ~30.

If the FCF conversion ended up being 105% of the non-GAAP EPS FY2025 outlook of ~$8.35 – ~$8.66, the FY2025 FCF range was ~$8.77 – ~$9.09. With shares trading at ~$235.43, the forward P/FCF range is ~26 – ~27.

Using the more conservative approach in calculating FCF where we deduct SBC, we readily know that the P/FCF will be higher than reflected above.

Final Thoughts

My current exposure is currently 286 shares in a ‘Core’ account in the FFJ Portfolio.

BR was my 9th largest holding when I completed my 2023 Year End FFJ Portfolio Review It was not a top 30 holding, however, when I completed my 2024 Mid Year FFJ Portfolio Review. This is because I sold 549 shares @ ~$199 on June 5, 2024 for tax planning purposes (see June 11, 2024 post). After the December 3 sale, BR is most certainly not a top 30 holding.

A fair price is ~$205 (my opinion) based on BR’s current FY2025 guidance. I, therefore, have no immediate plans to add to my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BR.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.