The following recent posts focus on the asset management industry.

- Brookfield Asset Management Exposure Increased

- Brookfield Corporation – Targeting DE of $5B by 2030

- Consider Investing In Asset Managers

- Select Your Asset Manager Investment Wisely

- BlackRock – An Asset Manager Investment For The Long Term

In keeping with the asset manager theme, I revisit Blackstone Inc. (BX) given that:

- it has released its Q3 and YTD2024 results on October 17; and

- I last reviewed it in this July 19 post at which time it had released its Q2 and YTD2024 results.

I believe the best time to invest in great companies is in times of uncertainty. Blackstone (BX) is also of the opinion that the best investments are made in times of uncertainty. It has, therefore, been actively making several new commitments. This bodes well for future Fee Related Earnings (FRE) and Distributable Earnings (DE).

Business Overview

BX’s website and Part 1 of the FY2023 Form 10-K provide ample information from which to learn about the company.

The ‘Our Businesses‘ section of BX’s website has a menu of the areas in which BX invests.

The ‘Press Releases Archives‘ section of BX’s website provides an indication of just how active BX has been of late.

Financials

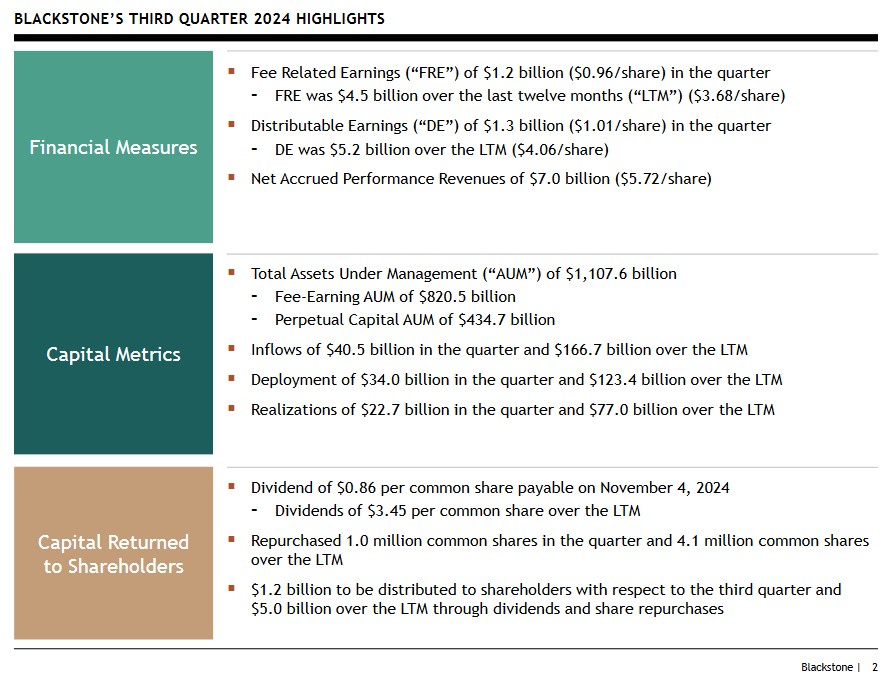

Q3 and YTD2024 Results

The most recent results are accessible in the Press Release and Earnings Presentation and in the accompanying Supplemental Financial Data. In particular, refer to pages 22 – 26 which reflect a high-level overview of the various funds BX manages.

I also encourage you to listen to Blackstone President Jon Gray on Q3 results.

Source: BX – Q3 2024 Earnings Presentation – October 17, 2024

On the Q3 2024 earnings call, Stephen Schwarzman (Chairman, CEO & Co-Founder) states:

In anticipation of improving markets, we substantially increased our investment pace starting in Q4 2023 which coincided with the peak of the 10-year treasury yield. Since then, Blackstone has deployed $123B, representing one of the most active periods in our history and double the prior year comparable period. We’ve been planting the seeds of future value at what we believe is a favorable time.

As the reference firm in our industry, we have a distinctive ability to convene the key decision makers from our limited partners to discuss what’s happening around the world. The insights we draw from our expansive platform and portfolio are highly valuable to them. Most recently, we’ve been engaging with our clients in a number of important areas, including the revolution underway and artificial intelligence. The build out, the digital energy infrastructure needed to support AI. The renewable energy transition, the rise of private credit, the development of the secondaries market or alternatives, extraordinary advances in drug development in the life sciences area. The emergence of India as one of the most important major economies and the cyclical recovery in commercial real estate.

Today, Blackstone is the largest data center provider in the world with holdings across the U.S., Europe, India and Japan. Last month, we announced another major expansion by agreeing to acquire Australian data center operator AirTrunk, valuing it at USD ~$16.1B (including debt) in one of the year’s biggest digital infrastructure tie-ups., the largest data center operator in the Asia Pacific region. We were uniquely positioned to execute on this investment given our expertise in this sector, the scale of our capital, the global integration of our teams and our connectivity to the world’s largest data center customers.

The Blackstone portfolio consists of $70B of data centers and over $100B in prospective pipeline development, including AirTrunk and facilities under construction.

Turning to the recovery in commercial real estate.

With the cost of capital moving lower, we’ve previously discussed our expectation of a new cycle of increasing values and improving investor sentiment towards the sector. One indication of this shift, now underway, is the renewed interest in the asset class from limited partners and financial advisers, notably for BREIT, repurchase requests in September were down over 90% from their peak. And we’re seeing encouraging signs in terms of new sales. BREIT is clearly moving towards positive net flows based on current trends. The vehicle’s largest share class has outperformed the public REIT index by ~50% annually since its inception nearly 8 years ago. We believe BREIT standing as the largest vehicle of its kind by far, with strong investment performance and exceptional portfolio construction, including ~90% concentrated in warehouses, rental housing and data centers. This positions the vehicle extremely well in the context of improving flows to private real estate. Historically, in multiyear recovery periods following a downturn, private real estate has delivered approximately double the returns of all REITs. As the largest owner of commercial real estate, this dynamic should be quite positive for Blackstone and our investors. Overall, our limited partners have benefited significantly from the exceptional balance of the firm and the careful way we’ve positioned their capital in a volatile world.

Looking forward, our business is accelerating and we are in the early days of penetrating markets of enormous size and potential.

Source: BX – Q3 2024 Earnings Presentation – October 17, 2024

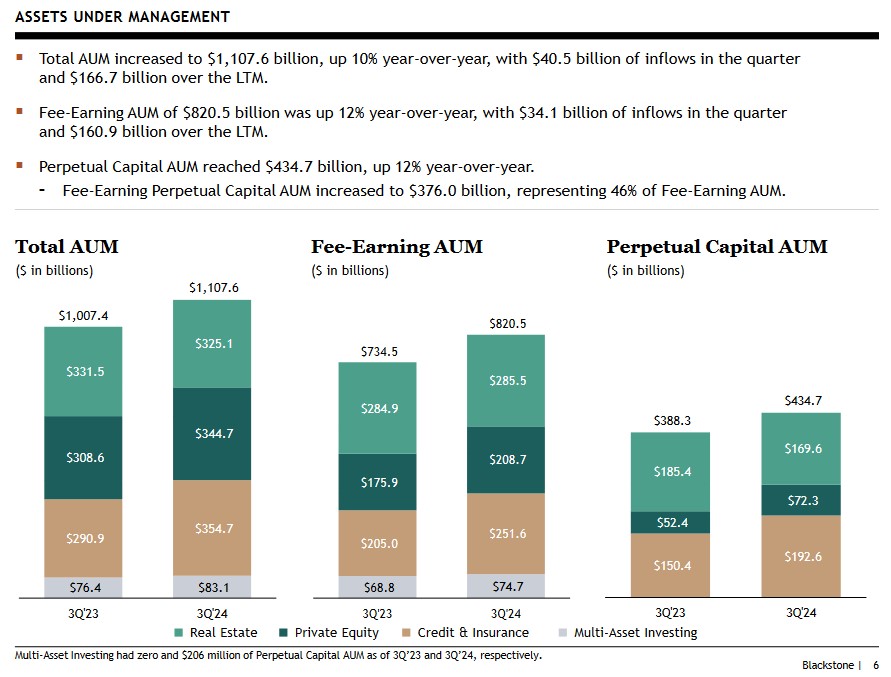

BX has a diverse range of growth engines that enable it to continually generate inflows, deploy capital, and generate realizations.

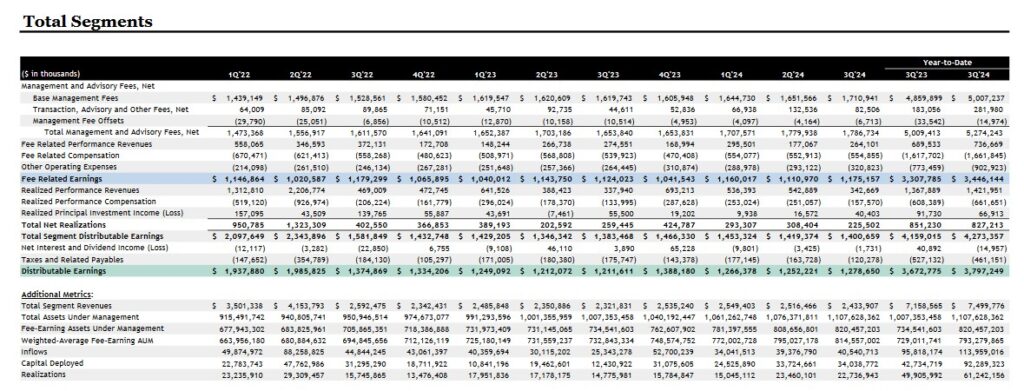

Within BX’s Q3 2024 Supplemental Financial Data document, we see the extent to which BX has generated quarterly FRE and DE over the past couple of years. There are additional pages that provide a breakdown by segment (Real Estate, Private Equity, Credit and Insurance, and Multi-Asset Investing).

BX is experiencing a dramatic increase in demand for all forms of investment grade private credit. This has led to the Credit and Insurance segment having the highest level of Total AUM of the 4 segments and management thinks the private-credit boom is just getting started.

- Real Estate: $325B

- Private Equity: $345B

- Credit and Insurance: $355B

- Multi-Asset Investing: $83B

Source: BX – Q3 2024 Earnings Presentation – October 17, 2024

Over the past several quarters, BX has stated that it would deploy significant capital ahead as management believes some of the best investments are made during times of uncertainty. In Q3, for the second consecutive quarter, BX invested or committed over $50B – the highest in more than 2 years.

New commitments were concentrated in digital infrastructure, renewable energy and power solutions, and enterprise software.

The largest commitment in Q3 was AirTrunk (see above for Stephen Schwarzman’s comments on the Q3 earnings call).

In private equity, BX agreed to acquire Smartsheet, a work management software company, for $8.4B. This represents one of the largest privatizations in 2024.

BX’s credit business had its second busiest deployment quarter in history, investing over $18B, up more than 50% from Q2. This was driven by significant activity in global direct lending as well as BX’s infrastructure and asset-based credit strategies.

Management states that the recovery is underway in commercial real estate. In January, BX made the call that values in the sector were bottoming thus leading to the decision to invest or commit $22B in real estate in the first 9 months of FY2024. This nearly 2.5x the same period in FY2023.

BX’s $30B global flagship fund is now nearly 40% committed. While the recovery will play out over time, the combination of lower base rates, lower borrowing spreads and lower new supply is positive for BX’s real estate business.

Another key development is the secular rise of private credit and the integrated platform BX has been building to offer clients and borrowers a one-stop solution across the full spectrum of credit strategies. BX currently manages the largest third-party private credit business in the world with $432B across corporate and real estate credit; this is a 20% YoY increase.

BX has one of the largest businesses in direct lending, Collateralized Loan Obligations, real estate debt and private investment grade credit. Total inflows across the combined platform were over $100B in the last 12 months.

In BX’s noninvestment-grade strategies, there continues to be significant opportunity to generate excess returns for clients relative to liquid markets.

Credit Ratings

BX’s senior unsecured domestic long-term debt ratings are at the top of the upper-medium-grade investment-grade tier. There is no change from prior reviews.

- S&P Global assigns an A+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch assigns an A+ long-term unsecured debt credit rating with a stable outlook;

These ratings define BX as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

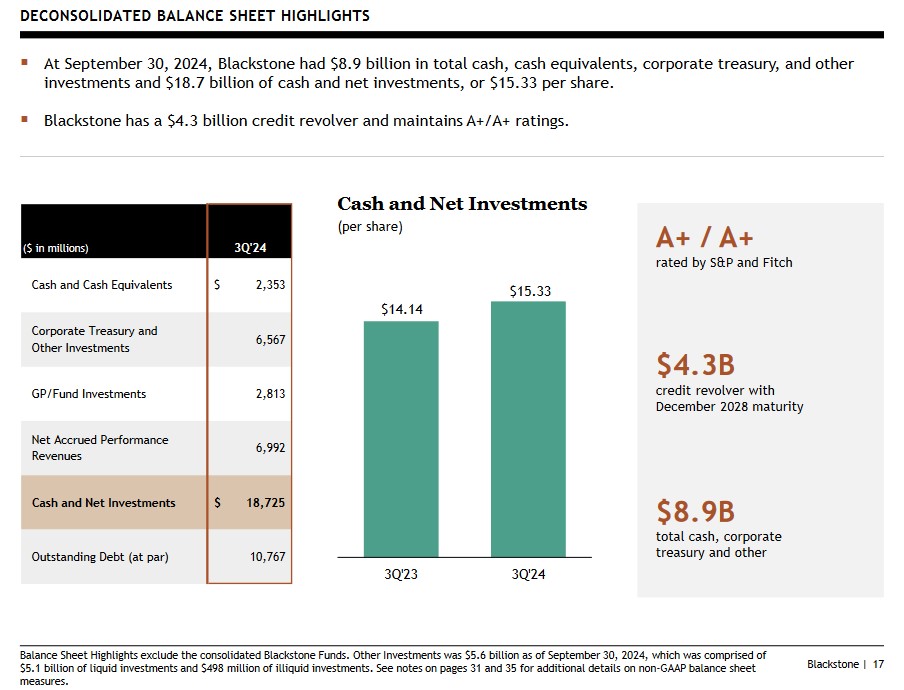

These are BX’s deconsolidated Balance Sheet highlights for Q3 2024.

Source: BX – Q3 2024 Earnings Presentation – October 17, 2024

Dividends and Share Repurchases

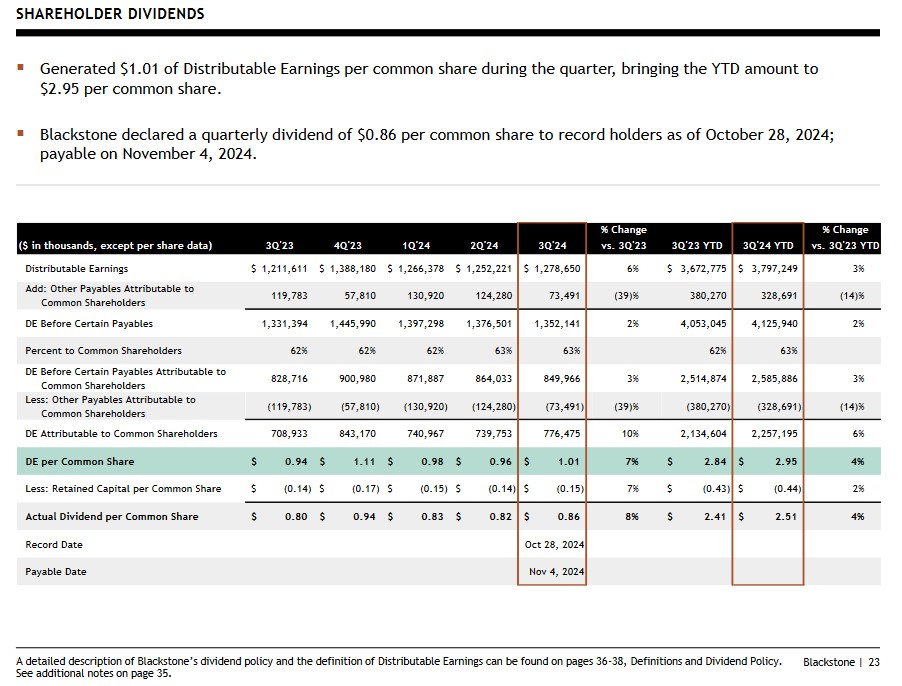

Dividend and Dividend Yield

BX has declared a $0.86 dividend payable on November 4. I incur a 15% dividend withholding tax since I hold shares in a taxable account and am a Canadian resident. I will, therefore, only receive $0.731/share.

BX’s quarterly distributions are unconventional and fluctuate depending on DE. The distribution policy states:

‘We intend to pay to holders of common stock a quarterly dividend representing approximately 85% of The Blackstone Group Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to shareholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.’

I do not calculate BX’s forward dividend yield because the quarterly dividend is unpredictable.

Source: BX – Q3 2024 Earnings Presentation – October 17, 2024

I look at an investment’s total potential long-term return perspective (capital gains and dividend income). Inconsistency in BX’s quarterly dividend, therefore, is irrelevant for my purposes.

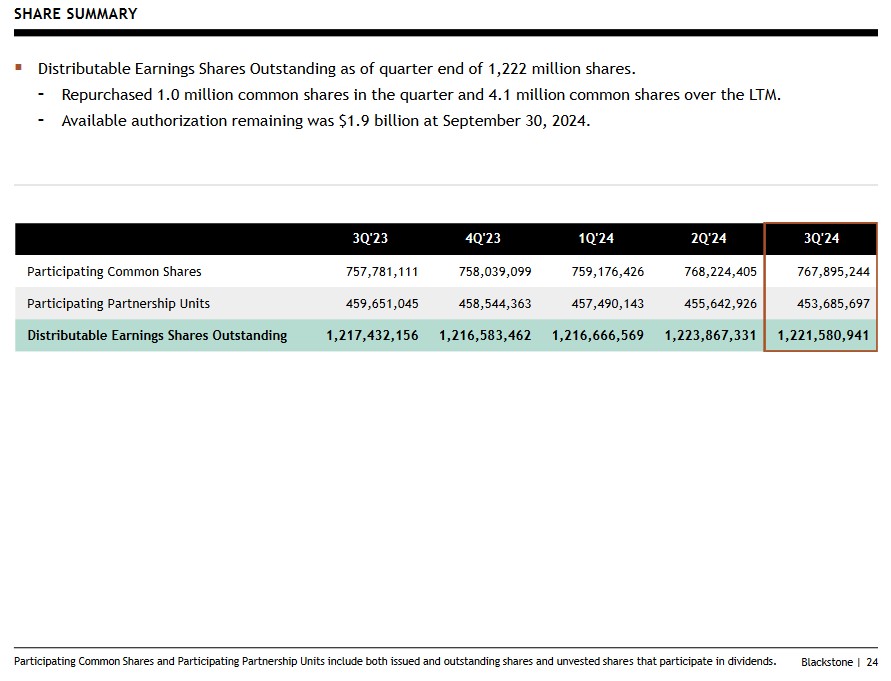

Share Repurchases

BX is hyper-focused on capital allocation. The extent to which it repurchases shares depends on whether there is a meaningful deterioration in BX’s share price relative to the true underlying value.

Source: BX – Q3 2024 Earnings Presentation – October 17, 2024

Valuation

I typically look at:

- diluted EPS – P/E;

- adjusted diluted EPS – adjusted P/E; and

- Free Cash Flow (FCF) – P/FCF

metrics to gauge the valuation of most companies I analyze. These metrics, however, are of little relevance when trying to assess BX’s performance and outlook.

BX uses DE and FRE to more accurately measure its performance; definitions for these, and other terms, are within the FY2023 Form 10-K.

The very manner in which BX operates makes it virtually impossible to forecast these metrics which explains why BX does not provide guidance.

BX is not easy to value because it raises large pools of capital from clients for deployment thus resulting in multiple multi-billion-dollar acquisitions annually. Because it continually makes sizable acquisitions or divestitures, earnings estimates can quickly become outdated.

Some of the assets are meant to be perpetual holdings. In other cases, BX uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs. It is not, therefore, unusual to see wide swings in YoY GAAP results.

Fluctuations in quarterly FRE and DE are to be expected so they do not factor into my investment decision making process. I am more interested in the long-term trend of these two metrics. I, therefore, like to compare annual FRE and DE over several years.

When we compare BX’s DE and FRE for FYE 2017 – FY2023 and the most two recent quarters, we see a noticeable increase over the years. At December 31, 2016, for example, BX had $366.6B of AUM. At the end of Q3 2024 it had $1,107.6B! As AUM grows, it stands to reason that DE and FRE should also grow over the very long-term.

Naturally, DE and FRE will fluctuate depending on market/economic conditions. If market/economic conditions are not conducive to the immediate sale of certain assets, BX may elect to continue to manage the AUM until such time as market/economic conditions improve.

Rather than reflect BX’s FY2017 – FY2023 and Q1 – Q2 2024 highlights again, they can be accessed through my July 19 post. The Q3 2024 highlights are found earlier in this post.

Final Thoughts

On the Q3 earnings call, management states that BX plans to list some of its largest investments since the recent technology-fuelled rally is signaling a likely return of investor interest in initial public offerings (IPOs). Should it do so, we can expect much stronger results from BX than those of recent quarters.

The last few years have brought challenges in the efforts of many asset managers to ‘cash out’ of investments made in prior years. Opportunities to ‘cash out’ of investments to drive returns for investors still remains sluggish. On the Q3 earnings call, however, management states that there are several signs that dealmaking is bouncing back; BX’s private-equity nondisclosure agreements were up 2.5x in September 2024 versus September 2023. This suggests an increase in discussions about potential deals.

While BX’s ability to ‘cash out’ of investments made in prior years has been a challenge, its level of acquisitions in recent quarters bodes well for FRE and DE in the coming years. There is a highly probability BX could have $1.5T – $2T AUM by 2034!

Naturally, not every investment will proceed according to plan as pointed out in my recent Select Your Asset Manager Investment Wisely post. BX, however, has such a massive investment portfolio that a few ‘less than stellar’ investments should not have a material impact on its results.

Alternative asset exposure (eg. private equity, private debt, hedge funds, real estate, commodities, structured products, venture capital) can produce attractive long-term investment returns. Directly investing in alternative assets, however, is beyond my risk tolerance.

While BX is an attractive long-term investment, it is essential to recognize that it is impossible to determine how well each investment within BX’s various funds are performing. Another key consideration is that many of the underlying assets can not be easily and quickly liquidated. BX investors must, therefore, invest for the very long term.

My BX investment, is made on the premise that BX is in the business of making money for highly sophisticated investors. Given that wealthy investors entrust billions with BX, I am ‘following the money’. Furthermore, senior BX executives have significant share ownership and have considerable incentive to ensure BX’s long-term success.

I currently hold 1505 BX shares in a ‘Core’ account in the FFJ Portfolio; it was my 11th largest when I completed my 2024 Mid Year FFJ Portfolio Review.

I last added to my Blackstone (BX) exposure on May 9, 2023 @ ~$81.65 and shares now trade at ~$170 following the release of BX’s Q3 2024 results on October 17, 2024.

Although I like BX’s long-term outlook, I am reluctant to increase my exposure in an environment where many investors are treating the equities market like a casino.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BX, BlackRock (BLK), Brookfield Asset Management (BAM.to) and Brookfield Corporation (BN.to).

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.