I last reviewed Becton Dickinson (BDX) in this August 6, 2024 post at which time I thought the company was on the path to improved returns; BDX had recently released its Q3 and YTD2024 results and revised FY2024 guidance and announced its plan to acquire Edwards Lifesciences’ Critical Care Product Group.

On September 3, 2024, BDX announced the completion of this acquisition and on November 7, it released its Q4 and FY2024 results and FY2025 outlook.

Time to revisit this existing holding.

Business Overview

Good sources of information to learn about BDX are its website and its FY2024 Annual Report/Form 10-K.

Financials

Q4 and FY2024 Results

BDX’s Q4 and YTD2024 results are accessible here.

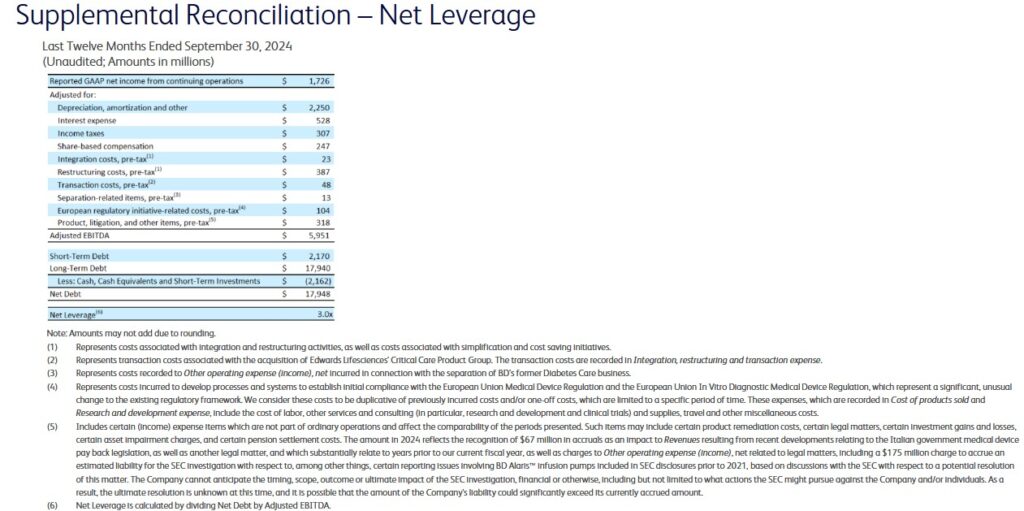

Net leverage (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, and FYE2024 was 2.6x, 2.8x, 2.6x, 2.6x, and 3.0x. Management’s expectation, however, is to reduce this to 2.5x within 12 – 18 months.

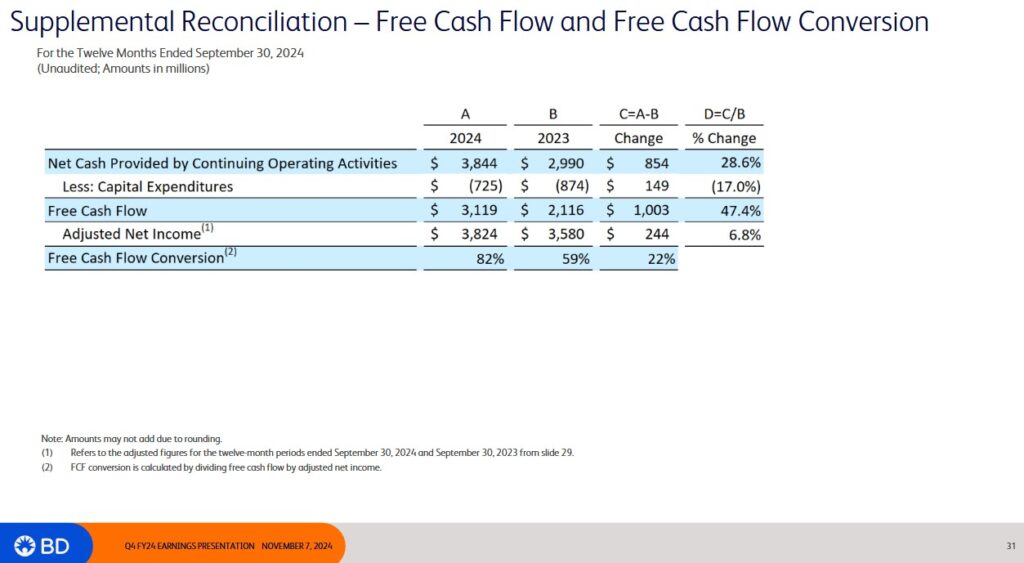

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

The following reflects the manner in which BDX calculates its FY2023 and FY2024 FCF.

In recent posts, I state why I am deducting share based compensation (SBC) when determining FCF; my recent Danaher (DHR) post explains my rationale for doing so.

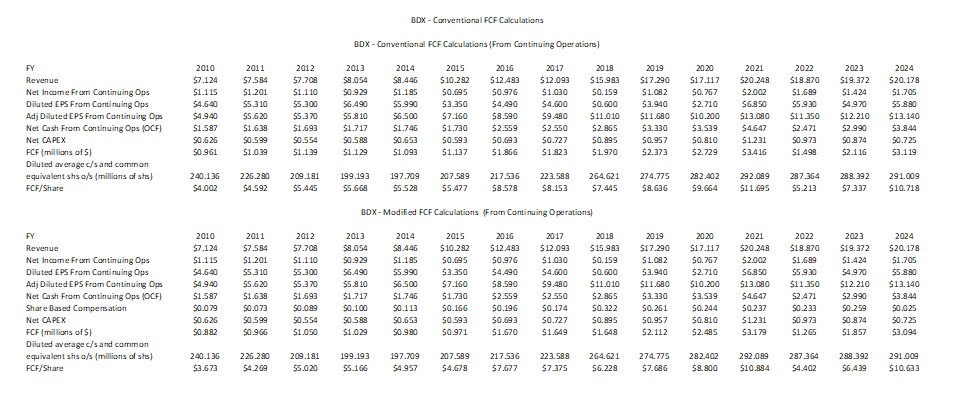

The table below reflects BDX’s FCF:

- calculated in the typical fashion where net CAPEX is deducted from Net cash from continuing operations; and

- where SBC and CAPEX are both deducted from Net cash from continuing operations.

BDX’s SBC is nothing close to that of many technology companies. The difference in FCF/share calculated in the conventional and modified methods, therefore, is relatively insignificant.

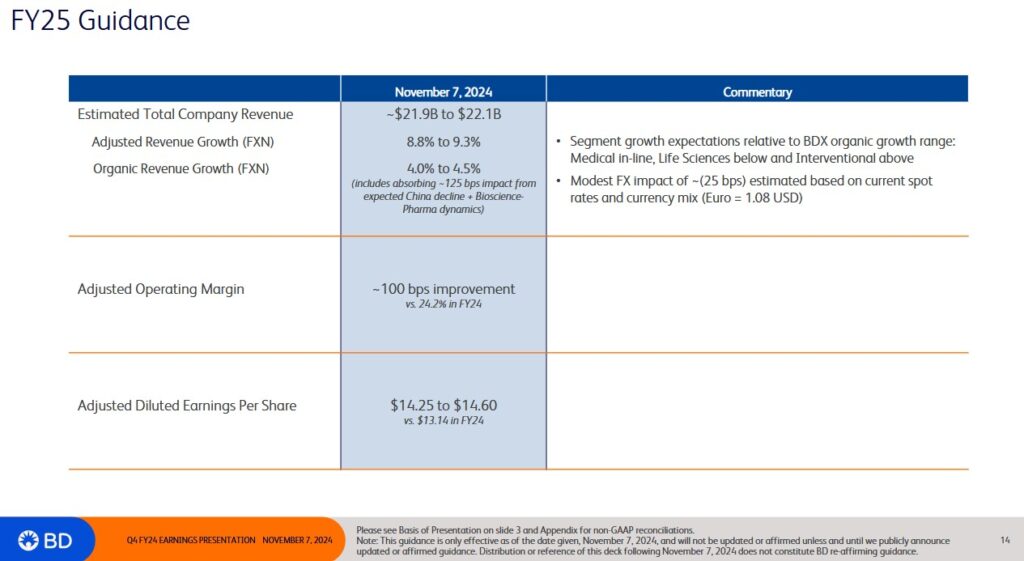

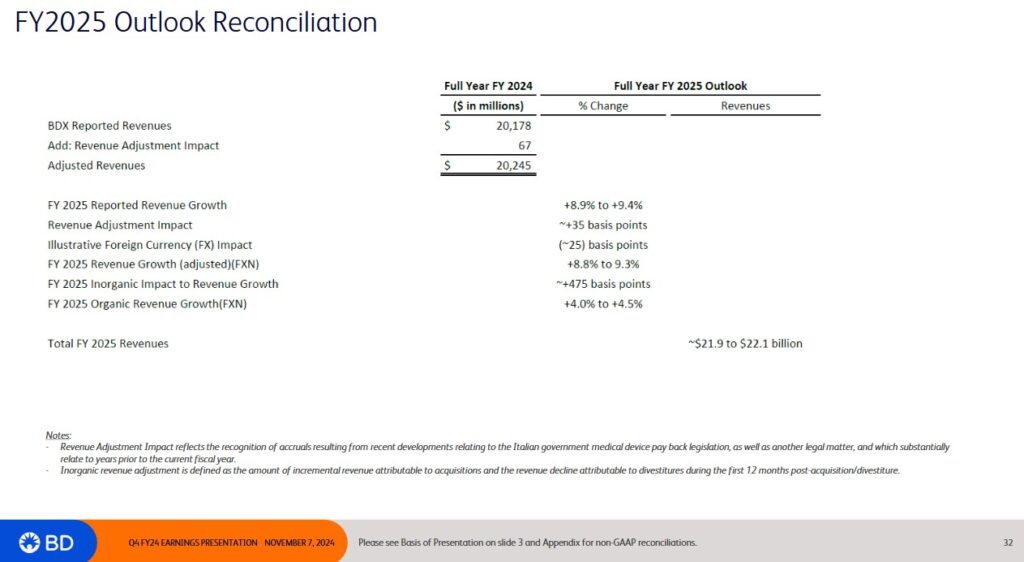

FY2025 Outlook

The following is BDX’s FY2025 outlook.

Risk Assessment

BDX’s net leverage ratio (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, and FYE2024 was 2.6x, 2.8x, 2.6x, and 3.0x. BDX’s target is under 3.0x.

There are no changes to BDX’s domestic senior unsecured debt ratings from the time of my August 6, 2024 post.

All 3 ratings are the middle tier within the lower medium grade category. They define BDX as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity for BDX to meet its financial commitments.

These ratings are satisfactory for my purposes.

Dividend and Dividend Yield

BDX’s dividend history is accessible here.

Some investors fixate on dividend metrics and may use BDX’s track record of 53 consecutive years of dividend increases as a deciding factor to invest in the company. A company’s dividend metrics are of little importance to me in my investment decisions making process. My interest lies in the total potential investment return and whether it commensurate with the risk I am assuming.

The diluted average common shares and common equivalent shares is reflected in the table provided earlier.

In FY2024, BDX executed and settled accelerated share repurchase agreements for the repurchase of 2.118 million shares of its common stock for total consideration of ~$0.5B. The purchase was made pursuant to the repurchase program authorized by the Board on November 3, 2021, for 10 million shares for which there is no expiration date.

In my prior BDX post, I state that I anticipated no share repurchases following the Edwards Lifesciences’ Critical Care Product Group acquisition until such time as BDX’s net leverage ratio was reduced to 2.5x. I thought this was unlikely to be achieved until early/mid-2026. BDX’s FY2025 outlook, however, includes plans to deploy ~$1B towards share repurchases over the next 12 – 18 months.

Valuation

Unfortunately, I was ‘asleep at the switch’. I started analyzing BDX the evening of December 11. By the time I finished my morning workout at the gym on December 12, BDX’s share price had popped. Instead of acquiring share at ~$221, I ended up acquiring shares at ~$227.56. In the grand scheme of things, this increase is insignificant since I only added 100 shares to my exposure in one of the ‘Core’ accounts within the FFJ Portfolio; my exposure is now 536 shares.

Management’s FY2025 outlook calls for ~$14.25 – ~$14.60 adjusted diluted EPS. Using my ~$227.56 purchase price, the forward adjusted diluted PE range is ~15.6 – ~16.

Using the adjusted diluted EPS broker estimates, BDX’s forward adjusted diluted PE levels are:

- FY2025 – 14 brokers – mean of $14.42 and low/high of $14.31 – $14.52. Using the mean, the forward adjusted diluted PE is ~15.8.

- FY2026 – 13 brokers – mean of $15.73 and low/high of $15.51 – $15.97. Using the mean, the forward adjusted diluted PE is ~14.47.

- FY2027 – 5 brokers – mean of $16.54 and low/high of $14.52 – $17.56. Using the mean, the forward adjusted diluted PE is ~13.8.

These forward adjusted diluted PE levels are much lower than at the time of prior reviews.

If we look at BDX’s FCF in recent years (calculated using the conventional and modified methods), we see considerable YoY changes. Using the current share price and the FY2024 FCF/share of $10.718 and $10.633 calculated using the conventional and modified methods, we get a P/FCF valuation of ~21.2 and ~21.4.

Final Thoughts

If BDX’s portfolio shift into higher-growth areas is just about done, I envision improvements in its earnings and FCF over the coming years. Should performance improve and the share count be reduced ($1B planned share repurchase over the next 12 – 18 months), I expect investors who have shied away from the company because of its less than stellar performance in recent years will start to look at BDX more closely.

One of my objectives from investing is to make the value of our investment portfolio grow at a much faster pace than the rate of inflation. At ~$275, I think BDX becomes fairly valued. If it reaches this level within the year, my return is ~20.8% ((~$275 – ~$227.56)/~$227.56) which is well above the current rate of inflation.

BDX was my 27th largest holding when I completed my 2023 Year End FFJ Portfolio Review and my 24th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review. I will be completing a similar review at the end of 2024 at which time I will be able to determine if it is still a top 30 holding. At the moment, I suspect it is not a top 30 holding despite the recent addition of 100 shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BDX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.