I last reviewed Agilent (A) in this August 23, 2024 post at which time the most current financial information was for Q3 and YTD2024. With the release of Q4 and FY2024 results and FY2025 outlook after the November 25 market close, I revisit this existing holding.

Business Overview

When I wrote my prior post, A operated in the life sciences, diagnostics and applied chemical markets and it provided application focused solutions that includes instruments, software, services and consumables for the entire laboratory workflow.

In Q1 2024, it changed its operating segments by moving its cell analysis business from the life sciences and applied markets segment to the diagnostics and genomics operating segment. The purpose of this transition was to further strengthen growth opportunities for both organizations.

Following this reorganization, A continued to have 3 reportable business segments:

- life sciences and applied markets;

- diagnostics and genomics; and

- Agilent CrossLab.

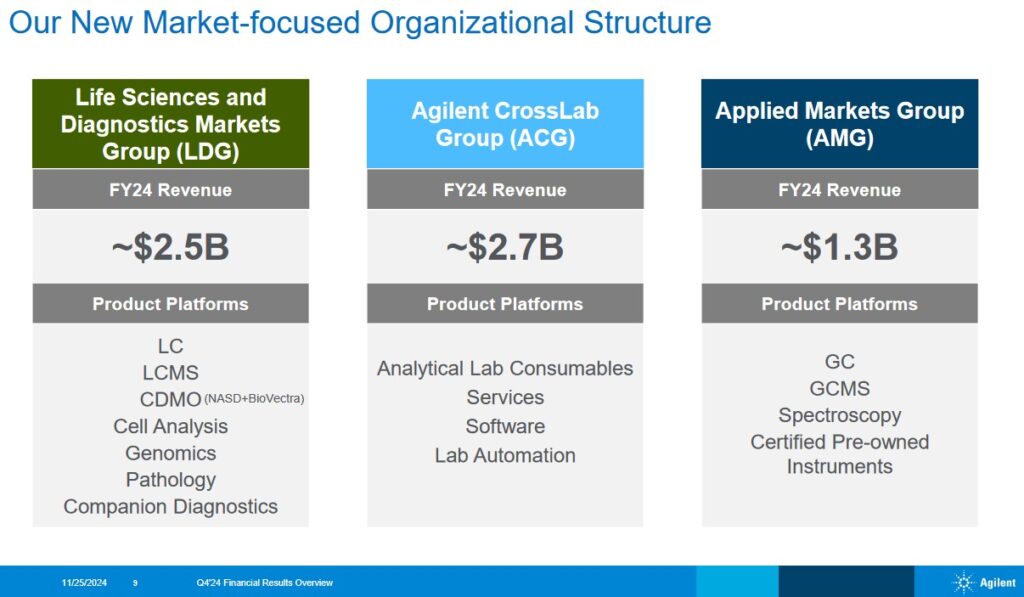

New Market-Focused Organizational Structure

On November 25, A announced a new organizational structure to accelerate the company’s operational transformation to drive higher growth through a market-focused, customer-centric enterprise strategy. The changes are effective immediately.

The new structure organizes A’s businesses according to its end markets and customers. The purpose of this reorganization is to enable closer collaboration among the business groups and better execution on cross-division, customer-first priorities.

Life Sciences and Diagnostics Markets Group (LDG)

This group represents ~38% of A’s revenue. Its primary focus is on A’s pharma, biopharma, clinical, and diagnostics end markets. LDG includes liquid chromatography and mass spectrometry instrument platforms, cell and biomolecular analysis, specialized contract development and manufacturing organization (CDM) services, pathology, companion diagnostics, and genomics.

Applied Markets Group (AMG)

This group represents ~20% of A’s revenue. Its primary focus is on the food, environmental, forensics, chemicals, and advanced materials markets. AMG includes gas chromatography and mass spectrometry, spectroscopy, and vacuum technology platforms.

CrossLab Group (ACG)

This group represents ~42% of A’s revenue. It focuses on supporting A’s customers in all end markets.

ACG will accelerate and strengthen customer connections across all Agilent end markets. This group includes services, software and informatics, automation, and consumables.

When A releases its FY2024 Form 10-K, (see SEC Filings), a more comprehensive overview of the company will be available.

Growth Potential

The company’s website currently reflects that A serves large, attractive markets with a $65B opportunity, growing 4-6%. With FY2024 revenue of ~$6.5B, A has ample growth opportunity.

Financials

Q4 and YTD2024 Results

Material related to the Q4 and FY2024 earnings release is accessible here. The investor presentation reflects the Q4 and FY2024 results by by geography, product type, end market, and segment.

Looking at the ‘reconciliations of revenue by region excluding acquisitions, divestitures, and the impact of currency adjustments (core)’ schedules reflected within the Financial Information report, we see the following:

- A’s FY2024 revenue by business segment suffered a ~5% YoY decline. The Q4 results, however, were 1% better than in Q4 2023.

- A’s FY2024 revenue by region suffered a ~5% YoY decline. The Q4 results, however, were 1% better than in Q4 2023.

- China and Hong Kong, a key growth market, suffered a 12% YoY reduction in revenue. The Q4 results, however, were only 2% lower than in Q4 2023.

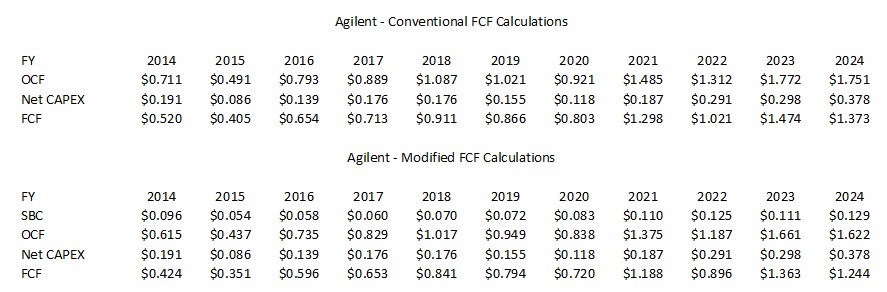

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In my recent Zoom Communications (ZM) post, I provide my rationale for adjusting a company’s OCF and FCF to account for stock-based compensation (SBC).

The following reflects A’s FCF using the conventional and modified methods. Fortunately, A’s SBC is nothing remotely close to that of many technology companies!

Capital Allocation

A’s capital allocation priority is to reinvest in the business. Share repurchases and dividend distributions are also a component of A’s capital allocation.

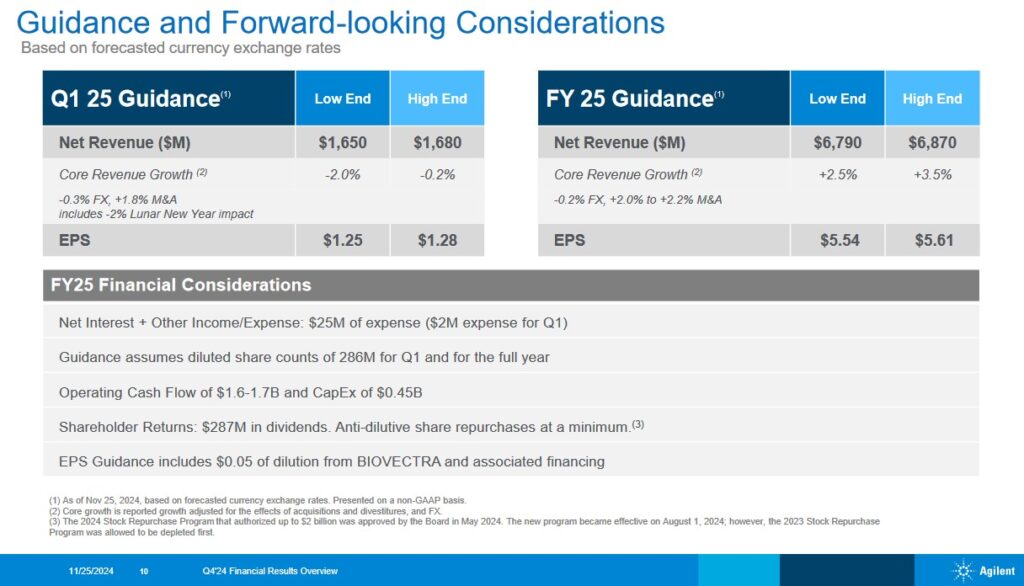

Q1 and FY2025 Guidance

The following reflects A’s Q1 and FY2025 guidance.

A’s management is typically conservative with guidance and the FY2025 guidance is no exception. On the earnings call, management indicated there remains considerable uncertainty as to the extent industry conditions will improve. This cautionary outlook is despite Chinese government stimulus and the aging fleet of instruments which its biopharma clients should be updating.

Risk Assessment

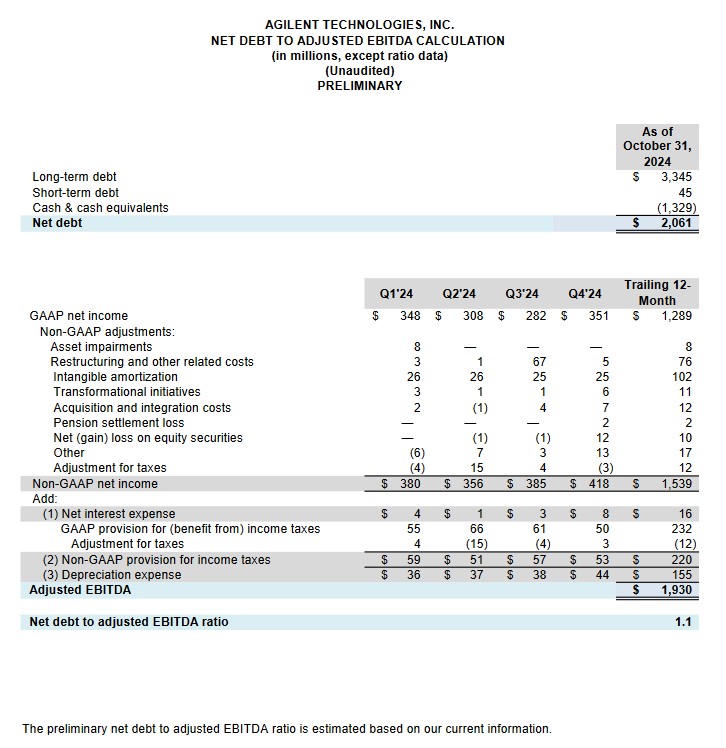

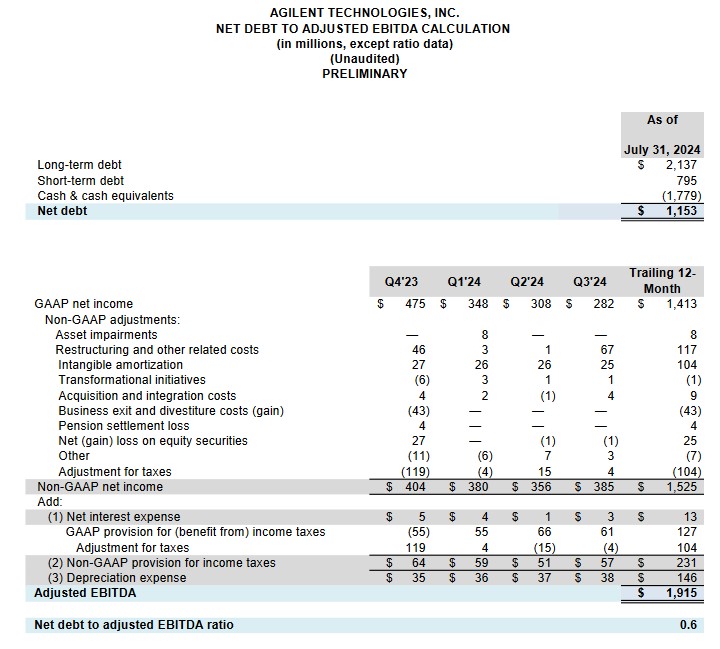

A’s net debt to adjusted EBITDA ratio is 1.1 versus 0.6 at the end of Q3 2024.

At the end of Q3 2024, A had ~$0.795B of short-term debt and ~$2.137B of long-term debt. At FYE2024, A had $0.045B of short-term debt and $3.345B of long-term debt. Investors need to remember that A completed a couple of acquisitions which I touched upon in my prior post (Sigsense Technologies and BIOVECTRA). In FY2024, A disbursed ~$0.862B to acquire businesses and intangible assets, net of cash acquired but these acquired businesses contributed little to A’s earnings.

While A’s net debt to adjusted EBITDA ratio is almost double what it was at the end of Q3 2024, investors should not be alarmed; A’s credit ratings remain unchanged from the time of my prior post.

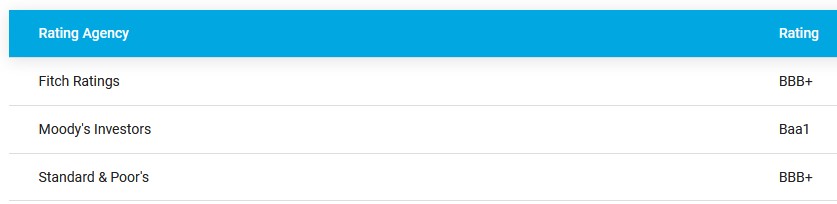

A’s website reflects the following credit ratings.

- Moody’s completed its most recent review on May 3, 2023 at which time A’s rating was upgrade from Baa2 to Baa1.

- S&P Global completed its most recent review on April 16, 2024 and affirmed A’s BBB+ rating with a Positive outlook.

- Fitch completed its most recent review on May 20, 2024 and affirmed A’s BBB+ rating with a Stable outlook.

All three rating agencies define A as having an adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of A to meet its financial commitments.

Dividend and Dividend Yield

As I compose this post, the company’s dividend history has yet to reflect the ~5% increase in the quarterly dividend ($0.236 increased to ~$0.248) declared on November 20, 2024.

The dividend yield is typically below 1% and should have little bearing on whether to invest in the company or not. Investors should expect the bulk of A’s future total investment return to continue to be predominantly in the form of capital appreciation.

The weighted average shares outstanding (in millions of shares) in FY2013 was ~345. In Q4 2024, it was ~287.

Repurchases in FY2018 – FY2024 (in $B) were 0.422, 0.723, 0.469, 0.788, 1.139, 0.575, and 1.15. Unfortunately, A’s shares were generally overvalued with the exception of the last couple of years.

Management’s FY2025 guidance includes anti-dilutive share repurchases at a minimum.

The 2024 Stock Repurchase Program that authorizes the repurchase of up to $2B was approved by the Board in May 2024 and became effective on August 1, 2024.

Valuation

In FY2024, A generated $4.43 and $5.29 of diluted EPS and adjusted diluted EPS. With shares having closed @ ~$134 on November 26, the PE and adjusted PE are ~30.2 and ~25.3.

Management’s FY2025 adjusted diluted PE range is ~$5.54 – ~$5.61. Using the current share price, the forward adjusted diluted PE range is ~23.9 – ~24.2.

We can expect the broker estimates to be amended over the coming days but for now, the forward-adjusted diluted PE using current broker estimates are:

- FY2025 – 20 brokers – ~24 using a mean of $5.58 and low/high of $5.54 – $5.66.

- FY2026 – 18 brokers – ~21.8 using a mean of $6.15 and low/high of $5.95 – $6.42

- FY2027 – 9 brokers – ~19.8 using a mean of $6.77 and low/high of $6.51 – $7.25.

These valuations are superior to those at the time of my August 23 post but are higher than at the time of prior posts.

In FY2024, A generated $1.373B of FCF using the conventional calculation and $1.244B using the modified calculation.

The diluted weighted average shares outstanding in FY2024 was ~291 million shares. Under the conventional FCF calculation method, A generated ~$4.72 of FCF/share. Divide the current ~$134 share price by ~$4.72 and we get a P/FCF of ~28.4. Under the modified calculation method, A generated ~$4.27 of FCF/share. Divide the current ~$134 share price by ~$4.27 and we get a P/FCF of ~31.4.

A’s FY2025 guidance includes OCF of $1.6 – $1.7B and CAPEX of $0.45B.

Using a $1.65B OCF mid-point, the FCF for FY2025 using the conventional calculation should be ~$1.2B (~$1.65B – ~$0.45B).

In Q4 2024, the weighted average shares outstanding (in millions of shares) was ~287. A’s guidance is for anti-dilutive share repurchases at a minimum. Let’s give A the benefit of the doubt that it will lower the weighted average shares outstanding in FY2025 to ~285 million.

Divide ~$1.2B of FCF by ~285 million shares and we get FCF/share of ~$4.21. Using the current ~$134 share price, the forward P/FCF is ~31.8.

If the FY2025 SBC is comparable to that in FY2024 (say ~$0.125B), the FY2025 modified OCF should be closer to ~$1.525B (~$1.65B – ~$0.125B). Deduct CAPEX of $0.45B and we get modified FCF of ~$1.075B.

Divide FCF of ~$1.075B by ~285 million shares and we get FCF/share of ~$3.77. Divide the current ~$134 share price by ~$3.77 and we get a forward P/FCF of ~35.5.

Final Thoughts

My A exposure consists of 500 shares held in a ‘Core’ account the FFJ Portfolio acquired at an average cost of ~$120.66; A was not a top 30 holding when I completed my 2024 Mid Year FFJ Portfolio Review.

In my opinion, A’s valuation is insufficiently compelling to warrant to purchase of additional shares. I consider A to be fairly valued at ~$140. With shares currently trading at ~$134, the share price would need to rise only ~4.5% before I consider them to be fairly valued. Rather than deploy cash sitting on the sidelines to increase my A exposure, I prefer to seek more attractive investment opportunities. If the share price were to retrace to the upper $120s, I might add to my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long A.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.