![]()

I last reviewed Intuitive Surgical (ISRG) in this January 23, 2026 post at which time the most current results were for Q4 and FY2025. With the release of Q1 2026 results following the April 21, 2026 market close this is an opportune time to revisit this existing holding.

Business Overview

Please reference prior ISRG posts that are accessible through The FFJ Archives section of this site.

ISRG develops, manufactures, and markets da Vinci surgical systems and the Ion endoluminal system. Its products and related services enable physicians and healthcare providers to improve the quality of and access to minimally invasive care. The da Vinci surgical system is designed to enable surgeons to perform a wide range of surgical procedures within our targeted general surgery, urologic, gynecologic, cardiothoracic, and head and neck specialties and consists of a surgeon console or consoles, a patient-side cart, and a high-performance vision system. The Ion endoluminal system is a flexible, robotic-

assisted, catheter-based platform for which the first cleared indication is minimally invasive biopsies in the lung and consists of a system cart, a controller, a catheter, and a vision probe. Both systems use software, instruments, and accessories.

The Overview section commencing on page 25 of 51 in the Q1 2026 Form 10-Q provides a good overview of the company, a trade and tariffs update, an overview of the macroeconomic environment, and an explanation of the company’s business model. The company’s website and the FY2025 Form 10-K are also very good sources of information.

As of March 31, 2026, ISRG’s installed base is 6,477 in the US, 2,257 in Europe, 2,049 in Asia, and 612 in the rest of the world for a total of 11,395. In comparison, the global installed base in 2020 was ~6,000.

From a ‘top-line’ perspective, ISRG annual revenue in FY2019 was ~$4.479B. In Q1 2026 alone, revenue was ~$2.771B.

ISRG used to be ‘the only game in town’ but competition is increasing. With an increase in competition, the expectation is for price reductions and an increase in innovation. Nevertheless, ISRG is investing heavily in research and development to remain the industry leader. While this bulletin from the American College of Surgeons is from May 2023, it provides an indication of how the overall use of robotic surgery is likely to continue to grow significantly over the coming years.

Da Vinci 5 Cleared for Cardiac Procedures

On January 26, 2026 ISRG announced that the U.S. Food and Drug Administration (FDA) had cleared the da Vinci 5 system for certain cardiac procedures, including mitral valve repair and IMA (internal mammary artery) mobilization for cardiac revascularization.

Acquisition of ab medica, Abex, Excelencia Robótica, and their Affiliates

A March 2, 2026 Press Release regarding this acquisition is accessible here.

On March 1, 2026, ISRG acquired the da Vinci and Ion distribution businesses previously operated by ab medica, Abex, Excelencia Robótica, and their affiliates for ~$0.5331B in cash, net of the effective settlement of existing receivables of $32.6 million. No gain or loss was recognized upon settlement, as amounts were stated at fair value. As a result of the acquisition, Intuitive assumed direct distribution responsibilities for Italy, Spain, Portugal, Malta, San Marino, and associated territories.

Further details regarding this acquisition are found in Note 7 in the Q1 2026 Form 10-Q that is accessible through the SEC Filings section of ISRG’s website.

Product Recalls And Safety Alerts

ISRG is currently managing several active product recalls and safety alerts as of early 2026. The most significant recent actions involve stapling components and robotic arm software.

- SureForm 30 Gray Reloads (Stapler): This is currently the highest-priority alert. On March 18, 2026, the FDA issued an Early Alert notifying the public that these specific gray reloads (designed for extra-thin tissue) may fail to form a complete staple line. ISRG has instructed hospitals to quarantine and return all affected units. Notably, the recall applies only to the gray reloads; the blue and white reloads remain safe for use.

- Robotic Arm Diagnostic Issue: The recall initiated in late 2025 affects the Universal Surgical Manipulator (USM). The USM is a key component of the Intuitive Surgical da Vinci Xi and X robotic systems, essentially acting as the robotic arms that hold and move the surgical instruments and endoscope. This was classified by the FDA as a Class 2 recall in early 2026. It involves a field-test software failure where technicians were not alerted if a component passed or failed, potentially leaving fatigued mechanical parts in service.

- Recent Field Safety Notice: As recently as April 20, 2026, international regulators (such as BfArM in Germany) have posted updated Field Safety Notices regarding the da Vinci Xi and X systems, indicating ongoing corrective actions.

Separately from hardware recalls, ISRG disclosed a cybersecurity incident in March 2026. This was a phishing attack that compromised internal administrative networks. ISRG, however, clarified that the da Vinci and Ion platforms were not affected, as the surgical networks are segmented from the business networks.

Financials

Q1 2026 Results

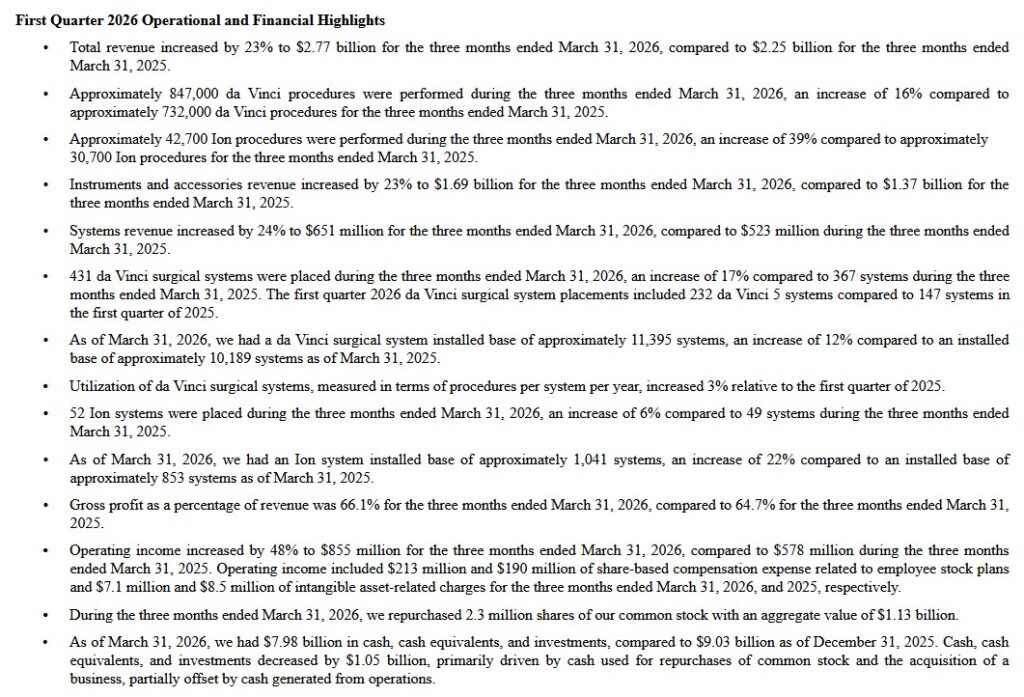

The following Q1 2026 operational and financial highlights are extracted from ISRG’s Q1 2026 Form 10-Q.

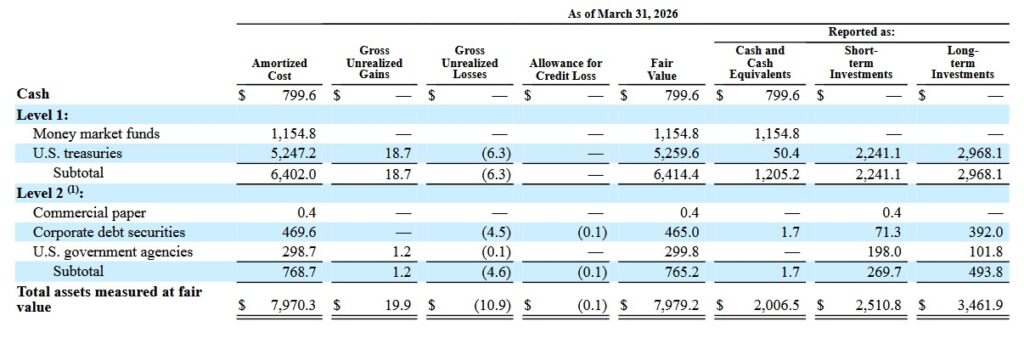

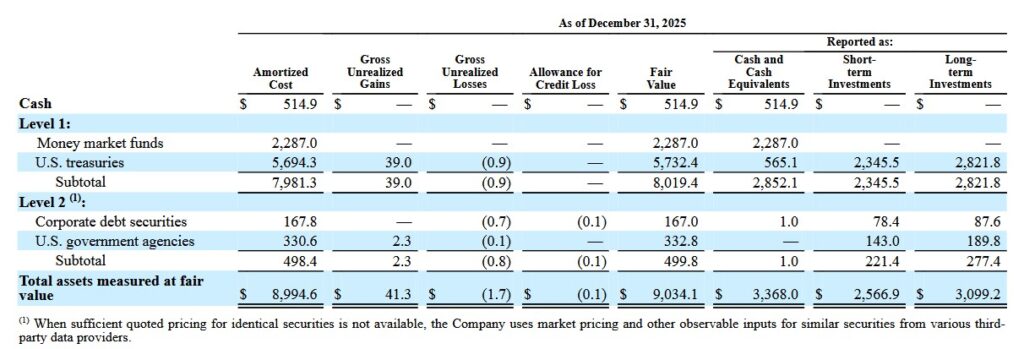

The following tables reflect the magnitude of ISRG’s cash, cash equivalents, and investments at the end of Q1 2026 and FYE2025.

Level 1 and Level 2 investments refer to categories in the fair value hierarchy under U.S. GAAP (ASC 820). They are used to classify financial assets based on valuation input observability.

Level 1 investments are assets valued using quoted prices in active markets for identical instruments. Examples include publicly traded stocks or mutual funds with real-time exchange prices. They carry the lowest valuation risk due to high liquidity and transparency.

Level 2 investments use observable inputs other than Level 1 quotes. Examples include quoted prices for similar assets, interest rate curves, or model-derived values with market-corroborated data. Corporate bonds or certain derivatives are often level 2 investments with moderate valuation risk from indirect pricing.

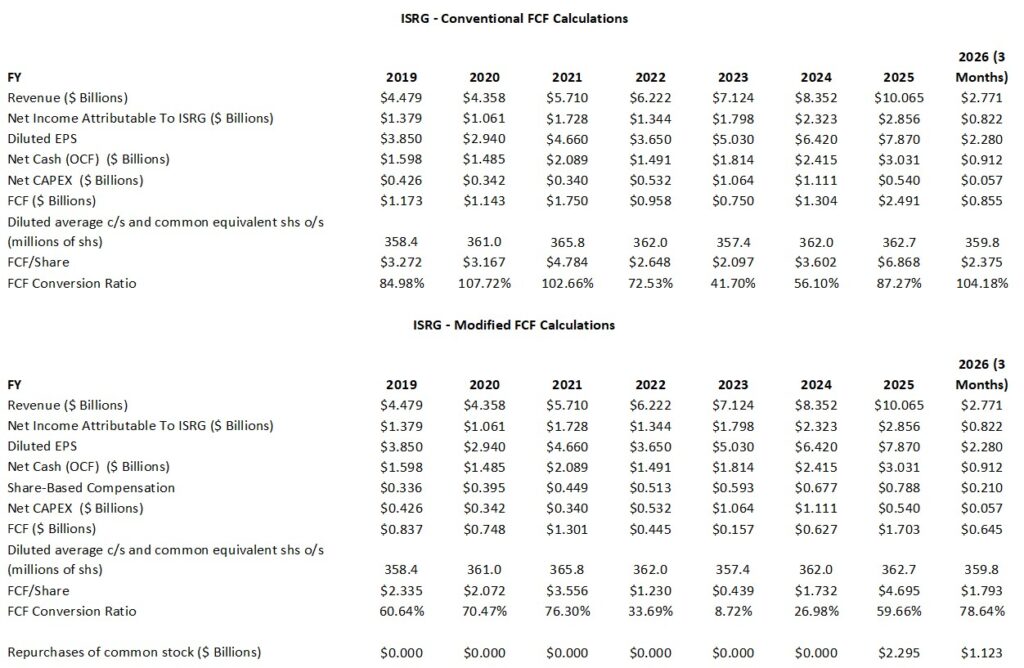

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2025 and Q1 2026)

In my September 28, 2024 How Stock Based Compensation Distorts Free Cash Flow post, I touch upon how a company’s FCF can be distorted. In several subsequent posts, I take a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, its computation is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. They do not, however, deduct share-based compensation (SBC). Given the magnitude of ISRG’s SBC, I think it is prudent to deduct it.

The following reflects ISRG’s FCF calculated using the conventional method and my modified method where I deduct SBC.

Return On Invested Capital (ROIC)

It is important to at a company’s ROIC track record because this metric provides an indication of a company’s efficiency. In essence, how much profit does a company generate for every dollar invested in the company? Is a company actually creating value or ‘burning’ cash for the sake of growth?

There are, however, some ‘shortcomings’ with ROIC which I point out in that post.

ISRG’s annual ROIC in recent years might only be in the low teens according to various sources. It, however, has a considerable sum in cash and cash equivalents, short-term, and long-term investments which negatively impacts the ROIC calculations.

Slightly less than $8B was held in cash and cash equivalents and short-term and long-term investments versus total assets of ~$20.1B at Q1 2026. In addition, ISRG has no debt. If we include all ~$8B in ‘Invested Capital’ in a ROIC calculation, ROIC looks artificially low because cash earns a very low return compared to ISRG’s normal business operations. Deciding exactly how much of this cash is ‘excess’ versus ‘operating’ is subjective.

If a large percentage of ISRG’s cash and cash equivalents and short-term and long-term investments are classified as ‘excess’, the ROIC skyrockets. This is because ROIC measures the return on the capital actually working in the business. In financial modeling, ‘excess cash’ is often removed from the denominator because it is not an ‘operating asset’. It is merely sitting in highly liquid and low risk accounts/financial instruments.

Although subject to debate, perhaps at least 40% of the $8B (ie. ~$3.2B) is ‘excess’. If we consider ~$3.2B to be ‘excess’ and $4.8B is capital actually working in the business, ISRG’s ROIC is well in excess of the ‘teens’.

FY2026 Outlook

ISRG’s revised FY2026 outlook includes:

- Worldwide da Vinci procedure growth of ~13.5% – ~15.5%.

- Non-GAAP gross profit margin of 67.5%-68.5% of revenue. This range reflects 100 bps of impact from tariffs, as well as higher input costs in other areas, including freight and semiconductor memory.

- Pro forma operating expense growth of ~11% – ~14% due to higher spending in support of advancing early-stage R&D programs, as well as incremental expenses associated with the acquisition of ISRG’s distributor for Italy, Spain, and Portugal.

- Non-cash stock compensation expense of ~$0.89B – ~$0.92B (no change from prior outlook).

- Other income, comprised mostly of interest income, of ~$0.315B – ~$0.335B due primarily to lower average cash balances following share repurchase activity in Q1.

- The FY2026 pro forma income tax rate estimate is ~22% – ~23% of pre-tax income (no change from prior outlook).

ISRG’s prior FY2026 outlook included:

- Worldwide da Vinci procedure growth of ~ 13% – 15% compared to 18% in 2025.

- Non-GAAP gross profit margin of 67% – 68% of revenue in 2026 compared to 67.6% in 2025. This range includes an estimated impact from tariffs of 1.2% of revenue, plus or minus 10 bps.

- Non-GAAP operating expense growth of 11% – 15% in 2026 compared to 12% in 2025. This is due to higher spending in support of advancing early-stage R&D programs, as well as incremental expenses associated with the acquisition of ISRG’s distributor for Italy, Spain, and Portugal.

- Non-cash stock compensation expense of ~$0.89B – ~$0.92B.

- Other income, comprised mostly of interest income, of ~$0.355B – $0.375B.

- The 2025 pro forma income tax rate was ~21%. The FY2026 estimate is 22% – 23% of pre-tax income.

Risk Assessment

No rating agency rates ISRG because it has no debt.

The following commentary is provided on page 42 of 51 in the Q1 2026 Form 10-Q.

Our principal source of liquidity is cash provided by our operations. Cash and cash equivalents plus short- and long-term investments decreased by $1.05B to $7.98B as of March 31, 2026, from $9.03B as of December 31, 2025, primarily as a result of cash used for repurchases of common stock and the acquisition of a business, partially offset by cash generated from operations.

Our cash requirements depend on numerous factors, including market acceptance of our products, the resources we devote to developing and supporting our products, and other factors. We expect to continue to devote substantial resources to expand procedure adoption and acceptance of our products. We have made substantial investments in our commercial operations, product development activities, facilities, and intellectual property. Based on our business model, we anticipate that we will continue to be able to fund future growth through cash provided by our operations. We believe that our current cash, cash equivalents, and investment balances, together with income to be derived from our business, will be sufficient to meet our liquidity requirements for the foreseeable future. However, we may experience reduced cash flow from operations as a result of macroeconomic and geopolitical headwinds.

Dividends

ISRG does not distribute a dividend.

Share Repurchases

In Q1 2026, ISRG’s share repurchases were as follows:

ISRG’s Board has authorized an aggregate of $13.0B of funding for the common stock repurchase program since its establishment in March 2009. The most recent authorization occurred in May 2025, when the Board increased the authorized amount available under the Repurchase Program to $4.0B, including amounts remaining under previous authorization. As of March 31, 2026, the remaining amount of share repurchases authorized by ISRG’s Board under the Repurchase Program was ~$0.6B.

I anticipate ISRG’s Board will soon increase the authorized amount available under the Repurchase Program.

Valuation

ISRG is almost always overvalued when analyzed using conventional valuation metrics. When analyzing ISRG’s valuation, however, it is essential to consider that displacing the da Vinci and ION systems after installation is difficult due to high switching costs, surgeon training lock-in, and a recurring revenue ecosystem that creates powerful network effects.

Surgeons undergo extensive training on da Vinci and ION platforms, developing proficiency that makes switching to competitors time-consuming, risky, and costly. Hospitals generally prefer retaining familiar systems to attract/retain talent.

Hospitals optimize operating rooms, service contracts, supply chains, and capital budgets around da Vinci and ION, making replacement expensive and disruptive.

Instruments and accessories constitute a meaningful proportion of ISRG’s annual recurring revenue. The instruments and accessories are proprietary, with patented interfaces generating high-margin consumables per procedure. This razor-and-blade model, plus clinical data from thousands of procedures, reinforces stickiness and data advantages competitors are currently unable to quickly match.

ISRG also continue to expand its addressable market, it generates attractive margins, and it has NO debt.

Given the above, I am prepared to ‘pay up’ to increase my ISRG exposure. Having said this, ISRG’s share price is volatile (the current 52 Week Range is $425.00 – $609.08) so I try to be patient and to acquire shares when there is share price weakness.

As I compose this post, ISRG’s share price is ~$482. Using this purchase price and the current broker estimates, ISRG’s forward-adjusted diluted PE levels are:

- FY2026 – 23 brokers – ~46.3 based on a mean of $10.41 and low/high of $10.14 – $10.76.

- FY2027 – 23 brokers – ~41 based on a mean of $11.78 and low/high of $10.86 – $12.61.

- FY2028 – 16 brokers – ~35.9 based on a mean of $13.43 and low/high of $11.96 – $14.93.

The valuations using FCF are likely higher as ISRG’s FCF/share is generally lower than diluted EPS and adjusted diluted EPS.

In my January 23, 2026 post I reflected the following:

As I compose this post, ISRG’s share price is ~$527. Using this purchase price and the current broker estimates, ISRG’s forward-adjusted diluted PE levels are:

- FY2026 – 28 brokers – ~53.2 based on a mean of $9.90 and low/high of $9.28 – $10.65.

- FY2027 – 28 brokers – ~46.6 based on a mean of $11.31 and low/high of $10.56 – $12.26.

- FY2028 – 12 brokers – ~40.5 based on a mean of $13.01 and low/high of $12.03 – $14.40.

The valuations using FCF are likely higher as ISRG’s FCF/share is generally lower than diluted EPS and adjusted diluted EPS.

For comparison, the following was my approximate estimate of ISRG’s valuation at the time of my September 3, 2025 post.

When I wrote my July 24 post, ISRG’s shares were trading at ~$499.935. Shares were definitely not a bargain but I added a few shares to my exposure. With shares currently at ~$441 and no material change to the company’s long-term outlook, I think ISRG presents an attractive long-term investment opportunity.

As noted in my prior post, ISRG generated YTD2025 diluted EPS of $3.72 and $4.00 of adjusted diluted EPS. Despite the headwinds management presented on the Q2 2025 earnings call, there is a good probability that FY2025 diluted EPS and adjusted diluted EPS could be ~$7.45 and ~$8.00. The diluted PE and adjusted diluted PE using my September 3 purchase price are ~60 and ~56.

Using this purchase price and the current broker estimates, ISRG’s forward-adjusted diluted PE levels are:

- FY2025 – 28 brokers – ~54.8 based on a mean of $8.16 and low/high of $7.95 – $8.31.

- FY2026 – 27 brokers – ~48.2 based on a mean of $9.27 and low/high of $8.73 – $9.77.

- FY2027 – 20 brokers – ~41.5 based on a mean of $10.79 and low/high of $10.10 – $11.81.

- FY2028 – 7 brokers – ~36.6 based on a mean of $12.21 and low/high of $11.31 – $13.92.

Although I look at brokers’ earnings estimates, I am extremely reluctant to place any reliance on them. My reasoning for excluding estimates beyond the current fiscal year is that I have no idea how anybody, especially in the current environment, can determine how a company will perform over the next few years. The variance in the brokers’ earnings estimates clearly indicates there is no consensus on how ISRG is likely to perform going forward.

Looking at ISRG’s valuation from a P/FCF perspective, there is a considerable variance in FCF when we use the conventional and modified methods (see table provided in my July 24 post). This is because ISRG issues significant shareholder based compensation.

If we assume that ISRG can generate a similar amount of FCF/share in the second half of FY2025 as in the first half, we arrive at ~$5.626 and ~$3.53 of FCF/share. Both are well below my estimates of ~$7.45 in diluted EPS and ~$8.00 adjusted diluted EPS. ISRG’s valuation from a FCF perspective when using my $447.26 purchase price is ~79.5 and ~126.7.

The following was my approximate estimate of ISRG’s valuation at the time of my October 23, 2025 post.

With ISRG’s current ~$543 share price and current broker estimates, we now see that the forward-adjusted diluted PE levels are:

- FY2025 – 29 brokers – ~63.6 based on a mean of $8.54 and low/high of $8.05 – $8.75.

- FY2026 – 29 brokers – ~56.6 based on a mean of $9.60 and low/high of $8.93 – $11.23.

- FY2027 – 23 brokers – ~49 based on a mean of $11.09 and low/high of $10.26 – $12.23.

- FY2028 – 9 brokers – ~42.9 based on a mean of $12.67 and low/high of $11.74 – $14.25.

On the Q3 earnings call, management states that capital expenditures for FY2025 will be ~$0.625B – ~$0.675B. This reflects planned facility construction activities.

If it can generate similar OCF in Q4 as in the prior 3 quarters, FY2025 OCF should be ~$2.85B. Deduct ~$0.65B in CAPEX and the conventional FCF for FY2025 should be ~$2.2B.

With the resurgence in ISRG’s share price, I suspect ISRG will not repurchase any more shares in the remainder of FY2025. If I use a weighted average number of outstanding shares of 363 million for FY2025, FY2025’s conventional FCF/share should be ~$6.06/share (~$2.2B/363 million shares).

On a modified basis, I anticipate SBC in Q4 will be ~$0.79B which is the mid-point of management’s revised guidance. By deducting ~$0.79B of SBC from my ~$2.2B FCF calculated using the conventional method, the modified FY2025 FCF should be ~$1.41B. Use a weighted average number of outstanding shares of 363 million for FY2025, FY2025’s modified FCF/share should be ~$3.88/share (~$1.41B/363 million shares).

Using the current ~$543 share price, the forward P/FCF is ~90 and ~140 (conventional and modified).

Final Thoughts

According to Market Research Future’s Surgical Robots Market report, the value (in USD) of the global surgical robots market was ~$12.25B in 2024 and ~$14.03B in 2025. Estimates call for the value of the market size to grow to $54.43B by 2035. This is a ~14.5% CAGR during the 2025 – 2035 forecast period.

ISRG’s FY2025 annual revenue was ~$10.065B so in the event market growth estimates are wildly overestimated and the market size ‘only’ grows to ~$40B by 2035, there is ample opportunity for top line growth at ISRG.

When I completed my 2025 Year-End Investment Holdings Review, ISRG was my 3rd largest holding. At the time, shares traded at $566.36. In addition, a couple of young investors I am helping on their journey to financial freedom also have ISRG exposure.

ISRG’s valuation is generally ‘rich’. Given my long-term outlook about the company, however, I think this is an opportune time to acquire shares if you have a long-term investment time horizon.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ISRG.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.