My last Accenture (ACN) review is in this December 19, 2025 post. With the release of Q2 and YTD2026 results and updated FY2026 guidance on March 19, I revisit this existing holding.

Business Overview

I reference my prior post in which I provide a very high level overview. The best way to learn about ACN, however, is to:

- review the company’s website; and

- read the FY2025 Form 10-K that is accessible through the SEC Filings section of the company’s website.

ACN maintains a list of its top-tier ‘Diamond’ clients. It does not, however, publicly release an exhaustive list because they represent ACN’s most sensitive and strategic competitive relationships. The firm, however, does periodically highlight specific long-term partners in its annual reports and case studies.

ACN most important client relationships are assigned ‘Diamond’ status. Such a client relationship typically meets the following internal criteria:

- These clients typically generate over $0.1B in annual revenue for ACN.

- They must utilize multiple ACN services (eg combining Strategy, Technology, and Operations).

- These must be long-term clients as opposed to one-off projects. As of March 2026, 195 of Accenture’s top 200 clients have been with the firm for 10+ years.

ACN had ~305 diamond clients at FYE2025 versus ~310 at FYE2024.

In FY2025, ACN delivered a record 129 quarterly bookings of more than $0.1B. According to the most recent earnings report from March 2026, ACN continues to see massive scale in its largest deals. In Q2 FY2026, ACN reported a record 41 clients signed bookings greater than $0.1B in a single quarter.

ACN typically has a 10+ year relationship with its ‘Diamond’ partnerships (195 of its top 200 clients). It does not publicly disclose the names of its ‘Diamond’ clients but its revenue mix as of Q2 2026 suggests its ‘Diamond’ client concentration is:

- Products (Retail, Travel, Life Sciences): 30% of revenue

- Health & Public Service: 20% of revenue

- Financial Services: 19% of revenue

- Communications, Media & Tech: 17% of revenue

- Resources (Energy, Chemicals): 14% of revenue

Based on recent 2025 and 2026 disclosures, the following are the major companies confirmed or widely recognized as being part of ACN’s ‘Diamond’ clients.

- Technology & Ecosystem Partners: Microsoft, SAP, Oracle, Salesforce, AWS, and Google Cloud (these are both partners and major clients).

- Health & Life Sciences: Bristol Myers Squibb (recently highlighted for scaling 30+ generative AI solutions).

- Financial Services: Cabel, Poste Italiane, and many top 200 global banks.

- Consumer Goods & Retail: Unilever, Marriott, and Shiseido.

- Resources & Industrials: Sumitomo Metal Mining and Halliburton.

- Public Sector & NGO: UNICEF (specifically for ethical AI and digital upskilling).

Financial Results

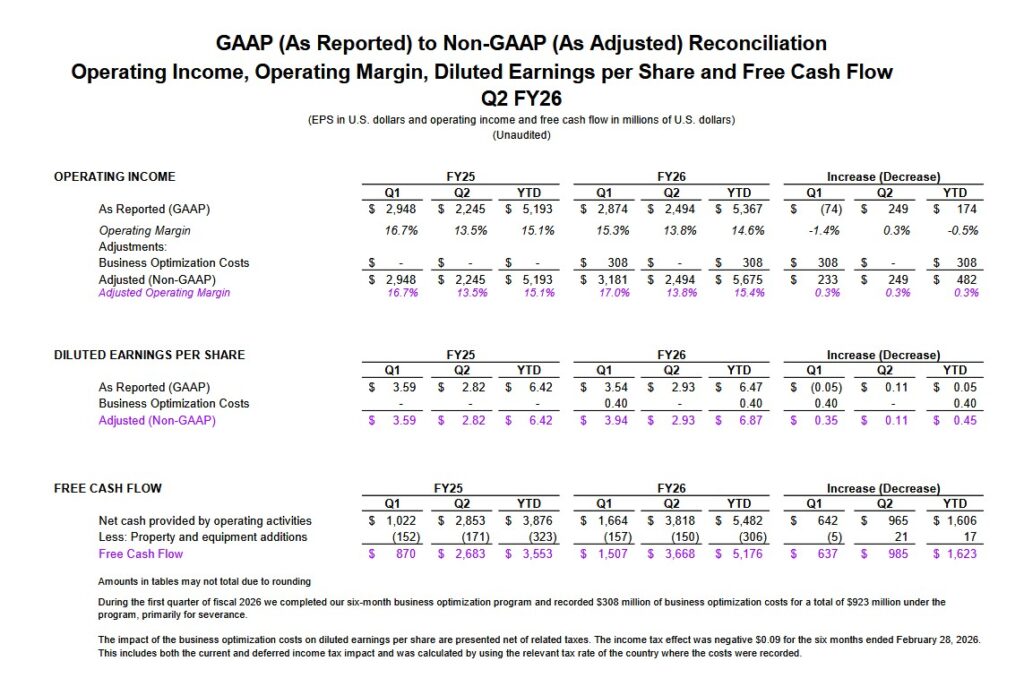

Q2 and YTD2026 Results

Form 8-K and Form 10-Q found within SEC Filings section of ACN’s website reflect Q2 and YTD2026 results.

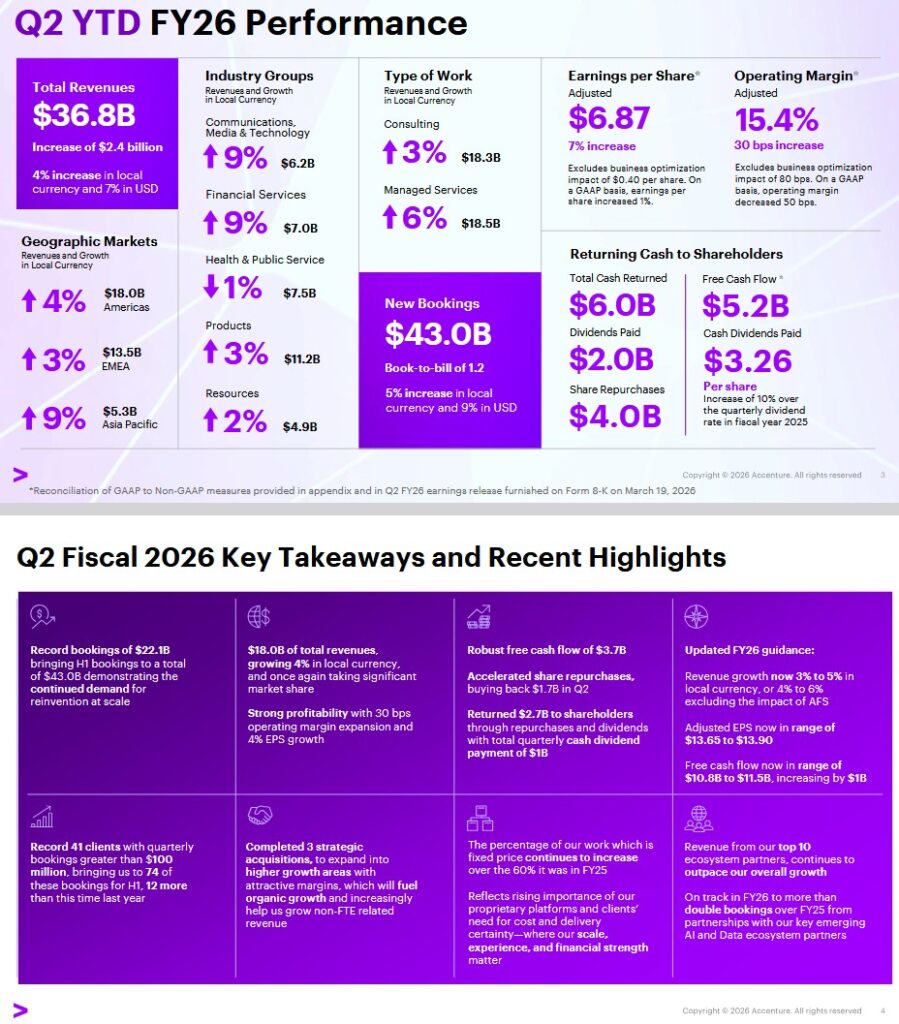

The following is from the Q2 2026 earnings presentation.

On the Q2 2026 earnings call, management states:

We delivered another strong quarter with $18B of revenue, growing 4% in local currency and once again taking significant marketshare. We had record bookings of $22.1B, bringing H1 bookings to a total of $43B.

We had a record 41 clients with quarterly bookings greater than $100 million, bringing us to 74 of these bookings in the first half, 12 more than this time last year, demonstrating the continued demand for reinvention at scale.

We delivered 30 basis points of operating margin expansion with strong EPS growth YoY, generating significant free cash flow while investing significantly in our business.

We closed 3 strategic acquisitions, deploying $1.6B of capital, and we now expect to deploy $5B in acquisitions this year with capacity to do more for the right opportunities.

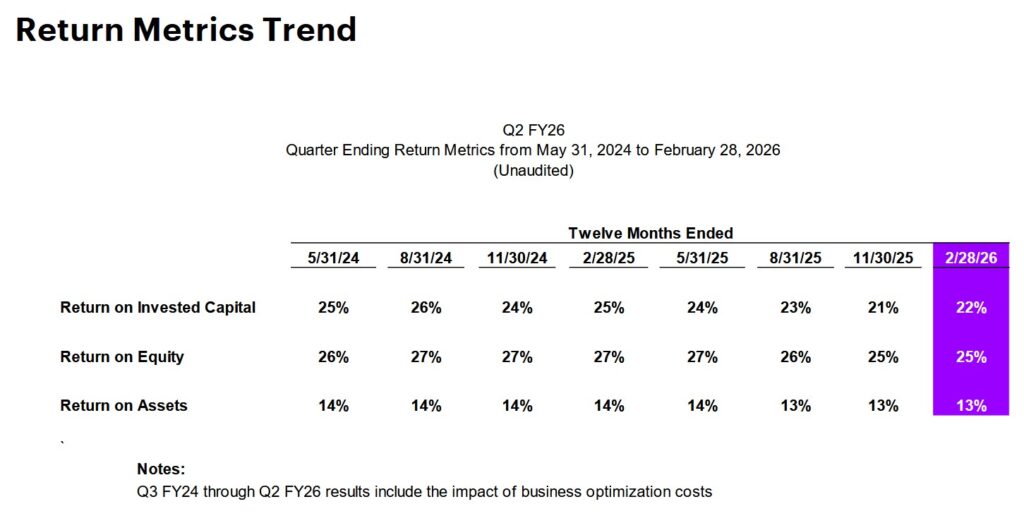

ACN’s most recent return metrics are found below and are accessible in supporting materials.

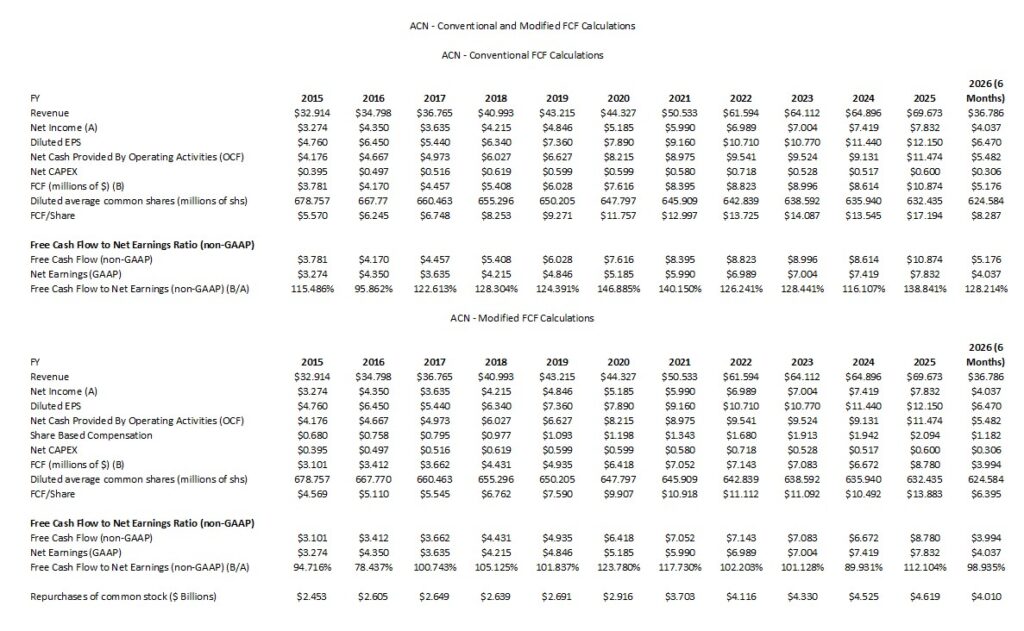

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2015 – FY2025 and YTD2026 (6 Months))

In my September 28, 2024 How Stock Based Compensation Distorts Free Cash Flow post, I touch upon how a company’s FCF can be distorted. In several subsequent posts, I take a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. They do not, however, deduct share-based compensation (SBC). Given the magnitude of ACN’s SBC, I think it is prudent to deduct it.

We see that the magnitude of ACN’s SBC has a material impact on the company’s FCF. We see from the following that ACN does not deduct SBC when it calculates FCF.

We see from the following that ACN does not deduct SBC when it calculates FCF.

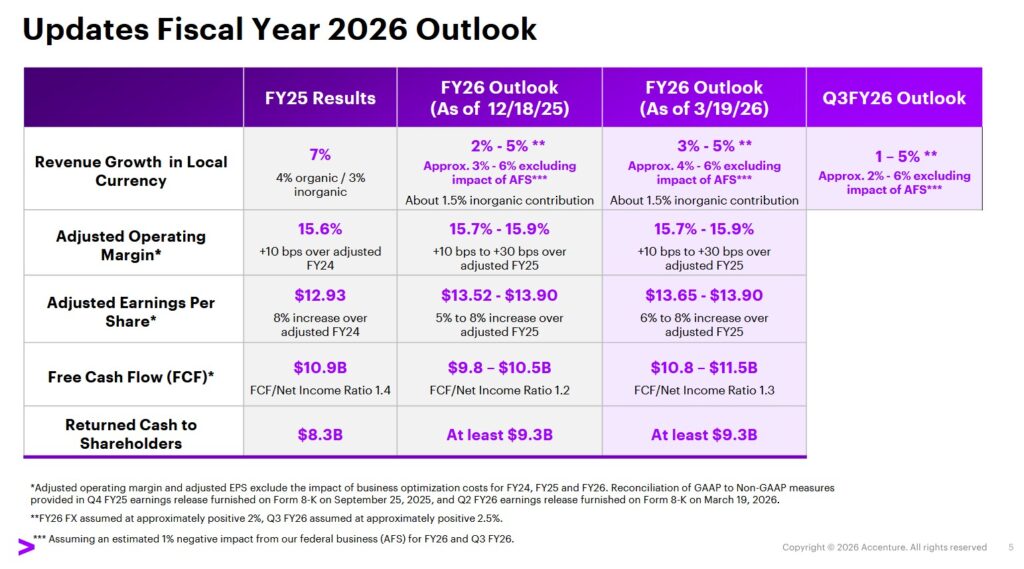

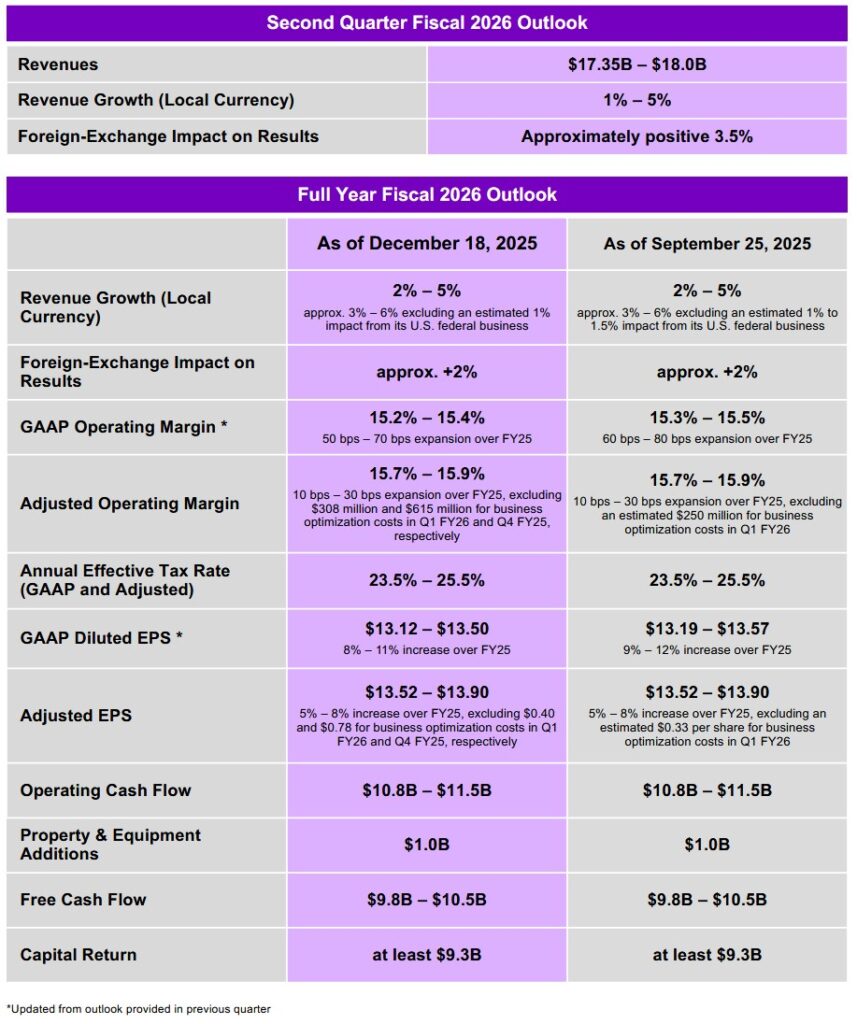

FY2026 Outlook

This is ACN’s current FY2026 outlook.

The following is what ACN provided for its outlook in its Q1 2026 earnings presentation.

Risk Assessment

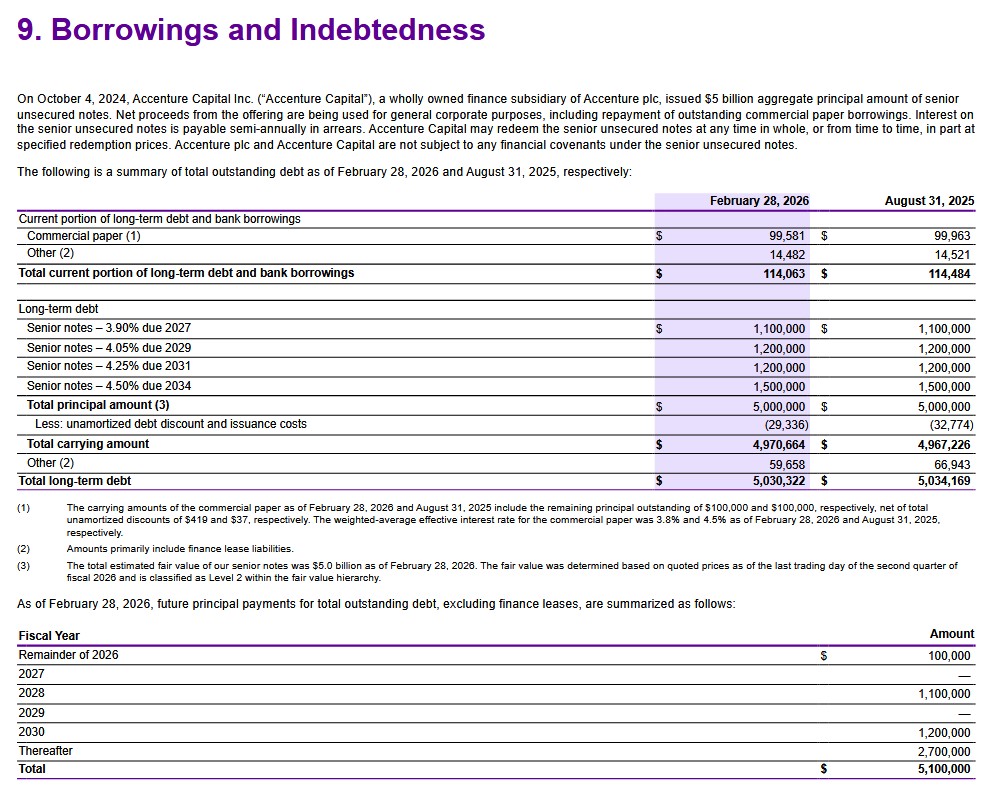

The risk aspect of an investment is important. This is why I am particularly interested in the maturity schedule of a company’s long-term debt as well as the interest rates.

At the end of Q2 2026, ACN’s current portion of long-term debt and long-term debt were similar to what it reported at the end of Q1 2026 and FY2025.

ACN’s Aa3 long term issuer rating was affirmed by Moody’s on October 1, 2024 with a stable outlook. This is the bottom tier of the high grade investment grade category.

S&P last reviewed ACN on April 24, 2025 at which time it affirmed its AA- rating with a stable outlook. This is the bottom tier of the high grade investment grade category.

Moody’s and S&P Global define ACN as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Dividends

ACN distributes a quarterly dividend (see history).

Dividend metrics are of very little relevance in my investment decision making process. If they are important to you, you may wish to check with your broker about the the dividend withholding tax rate and whether the ACN dividends are eligible for automatic dividend reinvestment.

ACN’s dividends are not eligible for automatic dividend reinvestment through the discount brokers I use.

Share Repurchases

In FY2011, ACN’s diluted weighted average Class A ordinary shares was 743,211,312. In Q2 2026 it was 622,640,891. If ACN is to continue to aggressively repurchase shares, I WANT the share price to remain depressed.

The following is found on page 34 of 151 in the Q2 Form 10-Q:

We intend to continue to use a significant portion of cash generated from operations for share repurchases during the remainder of fiscal 2026. The number of shares ultimately repurchased under our open-market share purchase program may vary depending on numerous factors, including, without limitation, share price and other market conditions, our ongoing capital allocation planning, the levels of cash and debt balances, other demands for cash, such as acquisition activity, general economic and/or business conditions, and board and management discretion. Additionally, as these factors may change over the course of the year, the amount of share repurchase activity during any particular period cannot be predicted and may fluctuate from time to time. Share repurchases may be made from time to time through open-market purchases, in respect of purchases and redemptions of Accenture Canada Holdings Inc. exchangeable shares, through the use of Rule 10b5-1 plans and/or by other means. The repurchase program may be accelerated, suspended, delayed or discontinued at any time, without notice.

In Q2, ACN accelerated its share buybacks and repurchased 6.8 million shares for $1.7B at an average price of $246.09/share.

In the first half of FY2026, ACN repurchased ~$4.001B of its outstanding shares versus ~$2.346B in the corresponding prior year period (see Consolidated Cash Flows Statements For the Six Months Ended February 28, 2026 and 2025 found on page 10 of 151 in the Q2 2026 Form 10-Q).

ACN repurchased ~2.5x the number of shares in the first half of FY2026 as it repurchased in the first half of FY2025. Given this, I am grateful that ACN’s share price is coming under pressure.

Valuation

ACN has not amended its diluted EPS guidance for FY2026 from $13.19 – $13.57 ($13.38 mid-point). It has, however, amended its adjusted diluted EPS guidance to $13.65 – $13.90 ($13.775 mid-point) from $13.52 – $13.90 ($13.71 mid-point). With shares trading at ~$193.70 as I compose this post, the forward diluted PE is ~14.48 and the adjusted diluted PE is ~14.06 (using the mid-points).

Using the current broker adjusted diluted EPS estimates, ACN’s forward-adjusted diluted PE levels are:

- FY2026 – 24 brokers – ~14 based on a mean of $13.87 and low/high of $13.65 – $14.15.

- FY2027 – 25 brokers – ~13 based on a mean of $14.98 and low/high of $14.54 – $15.49.

- FY2028 – 15 brokers – ~11.9 based on a mean of $16.27 and low/high of $14.73 – $17.35.

ACN’s FCF conversion ratio is generally in excess of 100% when calculated in the manner in which ACN calculates its FCF. My preference, however, is to look at ACN’s FCF conversion ratio when we deduct SBC because ACN’s annual SBC is significant (~$2B annually in recent years). When we deduct SBC, ACN’s FCF conversion ratio is much closer to 100%. It, therefore, stands to reason that ACN’s current forward P/modified FCF is ~14.50.

These valuation estimates are far superior than at the time of my prior reviews.

Final Thoughts

My current exposure is 800 shares in a ‘Core’ account in the FFJ Portfolio at a ~$267.8545 average cost.

On the Q2 2026 earnings call with analysts, management states the intent is continue to use a significant portion of cash generated from operations for share repurchases during the remainder of FY2026.

The weighted average diluted shares outstanding in Q2 2026 was 622,640,891. In the first half of FY2026, ACN repurchased ~16.3 million shares. If the share price remains depressed and ACN continues to generate strong earnings and FCF, it is not out of the realm of possibility that the weighted average diluted shares outstanding could conservatively be reduced by at least 8 – 10 million shares annually. If this materializes, ACN’s diluted weighted average shares outstanding could be below 600 million shares within a few years.

I am of the opinion that a number of consulting firms will experience challenges when enterprises are ready to deploy agentic AI solutions at scale. ACN should, however, benefit from its dominant position and envision firms will continue to seek ACN’s services because of its strong AI credentials and comprehensive AI portfolio.

A fair value appears to be ~$250 – $260 suggesting that ACN is undervalued thus presenting long-term investors with a wonderful opportunity to acquire shares in what is arguably an industry leader.

My final thoughts are the same as in my prior post. I continue to welcome opportunities when great companies temporarily fall out of favor and hope ACN’s share price continues to experience weakness.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ACN.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.