![]()

When I last reviewed Merck & Co. (MRK) in this August 4, 2023 post, the most current results were for Q2 and YTD2023. We now have MRK’s Q2 and YTD2025 results released on October 30, 2025 thus prompting me to revisit this existing holding.

On October 28 I increased my exposure with the purchase of 200 shares @ $87.02 in a ‘Core’ account within the FFJ Portfolio and disclosed this purchase in my FFJ Portfolio – October 2025 post.

When I completed my 2025 Mid-Year Portfolio Review I held 429 shares and it was not a top 30 holding. Following my recent purchase of 200 shares, my exposure is 635 shares. This is still insufficient to make it a top 30 holding.

Business Overview

MRK has transformed over the last couple of years. I, therefore, recommend reviewing the following SEC Filings:

- FY2024 10-K; and

- Q3 2025 Form 10-Q.

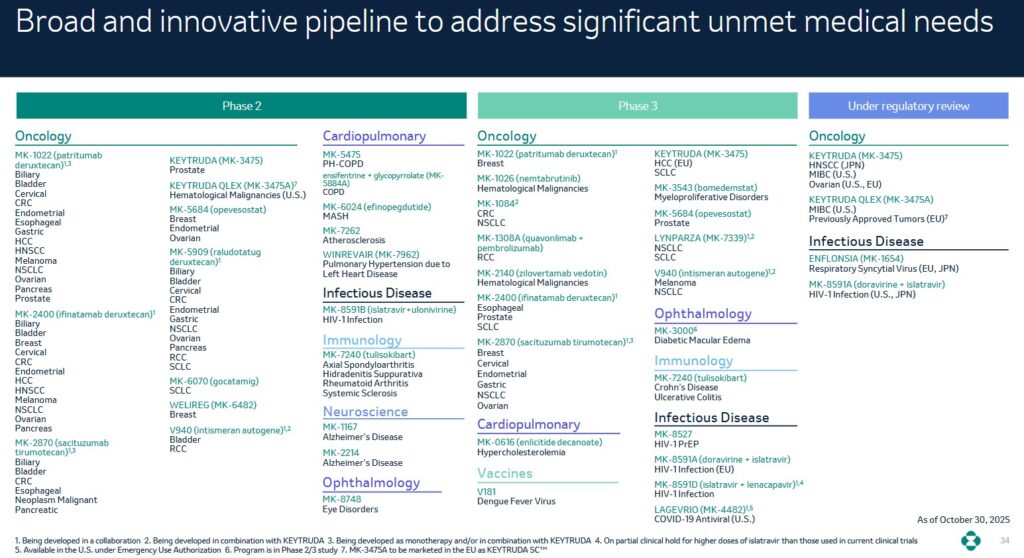

Pipeline

A critical factor in determining whether to invest in a pharmaceutical company is the robustness of a company’s pipeline; MRK’s pipeline is accessible here.

Drug development is a rigorous time-consuming and costly undertaking and most programs do not make it beyond Phases 2 or 3. MRK’s current pipeline includes 50+ programs in Phase 2, 30+ programs in Phase 3, and 5+ programs under review.

Pharmaceutical companies MUST prioritize reinvesting in the business to remain competitive over the long-term. On the Q3 earnings call, management states:

Strategic business development remains a top priority. We’re assessing potential targets with urgency given our desire to make additional compelling investments when both science and value align. The investments we’re making to advance and expand our pipeline are increasingly translating into positive clinical results and successful new product launches. This is giving us improved line of sight toward the transformation of our portfolio to one with a far more diversified set of growth drivers.

The time and costs to develop a drug explains why major pharmaceutical companies acquire smaller industry participants that have a pipeline of promising drugs.

Drug Development Phases

The US Food and Drug Administration has a multi-step process before a drug receives FDA approval.

Preclinical Research

In this phase, selected lead compounds undergo laboratory and animal studies to assess safety, toxicity, pharmacodynamics, and pharmacokinetics. The key goal is to ensure the drug is not harmful before testing in humans. Successful completion is required to file an Investigational New Drug (IND) application with regulators to start clinical trials.

Clinical Research (Clinical Trials)

Clinical trials are conducted in humans and take place in several sub-phases.

- Phase I: Tests safety and dosage in a small number of healthy volunteers or patients. These trials can take from six months to one year to complete.

- Phase II: Evaluates efficacy and side effects in a larger patient group. These trials can take from six months to one year or more to complete.

- Phase III: Confirms effectiveness, monitors adverse reactions, and compares the new drug to standard treatments in large populations. These trials can take from one to four years to complete, depending on the disease, length of study and number of volunteers.

- Some frameworks include a Phase IV for ongoing monitoring after approval.

Regulatory Review and Approval

After successful clinical trials, data are submitted to regulatory agencies (e.g., FDA, EMA) for a thorough review. If approved, the drug can be marketed. This phase focuses on confirming the risk/benefit ratio and ensuring product quality.

Post-Market Safety Monitoring

Following approval, there is continuous monitoring for long-term safety and effectiveness in the general population. This phase aims to detect any rare or long-term side effects that may not have been seen in earlier trials and to ensure quality control continues.

Just because a pharmaceutical company develops a drug and receives regulatory approval is no indication the drug will be a commercial success. A competitor, for example, could develop a superior drug.

Acquisitions

In July 2025, MRK completed the acquisition of SpringWorks Therapeutics for ~$3.9B, in a move that established MRK’s rare tumor business.

In October 2025, MRK completed the acquisition of Verona Pharma for ~$10B. This added the FDA-approved COPD maintenance treatment, OHTUVAYRE, to MRK’s cardiopulmonary portfolio.

MRK is focused on growth through strategic M&A, particularly in the life sciences sector and rare disease area within the healthcare business. Its senior management has indicated a strategy of using a string of targeted acquisitions of companies delivering breakthrough solutions to drive growth, with a focus on smaller, pipeline-driven deals (typically of ~$1B – ~$15B value).

Blackstone Life Sciences Provides Financing To MRK

In my recent Blackstone (BX) post is a section titled Private Credit Market – Misunderstandings and Misinformation in which I provide the following statement from Stephen Schwarzman, (:

For Blackstone, our $150B+ direct lending platform is comprised of over 95% senior secured debt, with low loan-to-value ratios of less than 50% on average, meaning there is significant borrower capital subordinate to our positions in nearly all cases from companies backed by financial sponsors or public companies.

And in the private investment-grade area, we’ve concentrated our activities in multitrillion-dollar markets where Blackstone is often a leading player, including data centers, energy infrastructure and real estate, with our loans secured by underlying assets of excellent quality.

In MRK’s November 4, 2025 Press Release, we see that BX through Blackstone Life Sciences, is providing $0.7B to MRK for the development of sacituzumab tirumotecan (sac-TMT), an investigational antibody-drug conjugate (ADC) targeting trophoblast cell-surface antigen 2 (TROP2), a protein found on the surface of various cancer cells. MRK is currently evaluating sac-TMT in 15 global Phase 3 clinical trials spanning six tumor types, including breast, endometrial and lung cancers.

Under the terms of the agreement, BX will pay MRK $0.7B (which is non-refundable, subject to termination provisions provided for in the agreement) to fund a portion of the development costs for sac-TMT expected to be incurred throughout 2026. In return, BX is eligible to receive low-to-mid single-digit royalties on net sales of sac-TMT across all approved indications in MRK’s marketing territories contingent upon receipt of regulatory approval in the U.S. for first-line treatment of triple-negative-breast cancer based on findings of the TroFuse-011 clinical trial.

As noted earlier, Phase 3 trials can take from one to four years to complete. Terms of the financing arrangement, however, are only to fund a portion of the development costs for sac-TMT expected to be incurred throughout 2026. I do not envision FDA approval will be granted in 2026, and therefore, I suspect BX and MRK have already had extensive discussions about what happens toward the end of 2026.

Financials

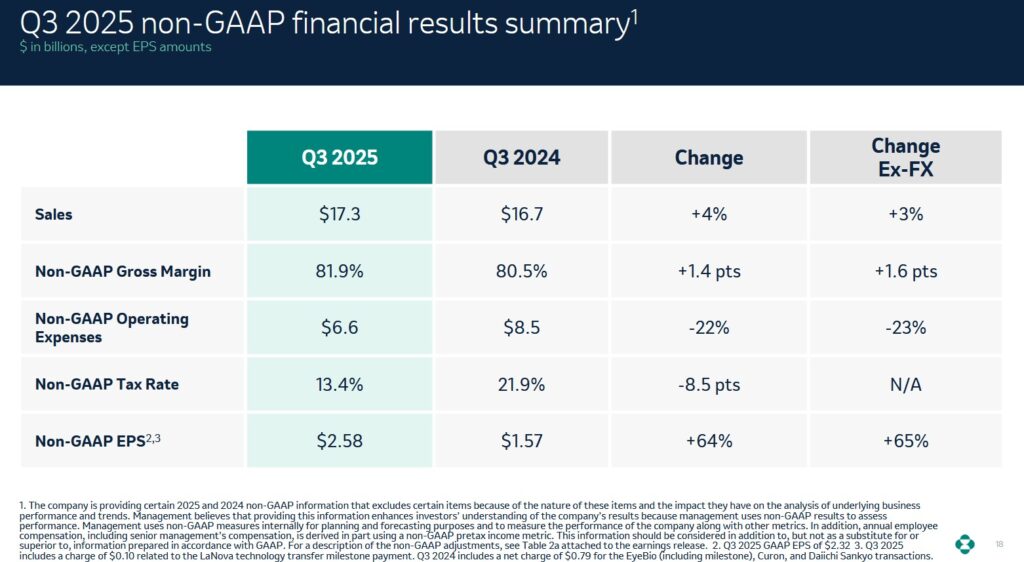

Q3 and YTD2025 Results

Details of MRK’s Q3 and YTD2025 results are accessible here.

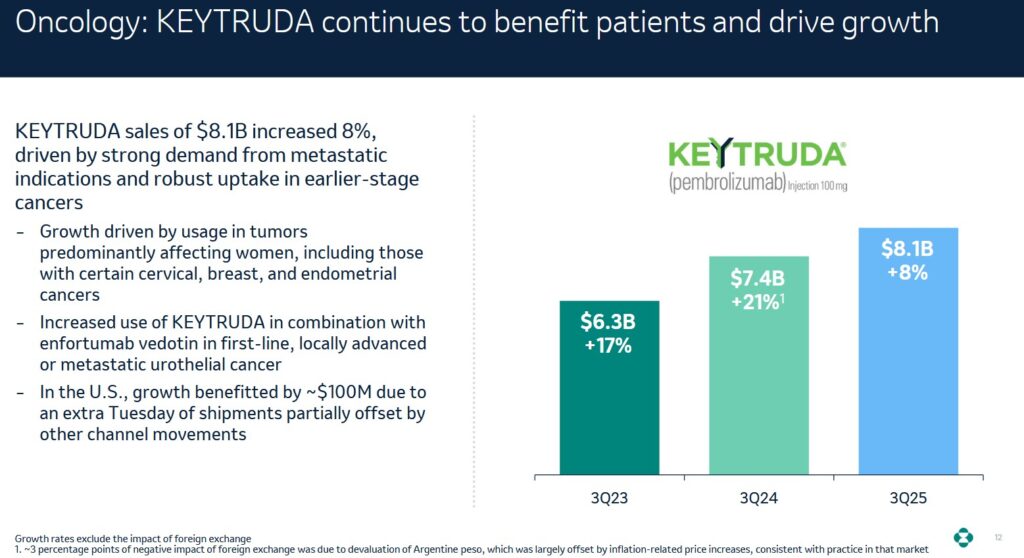

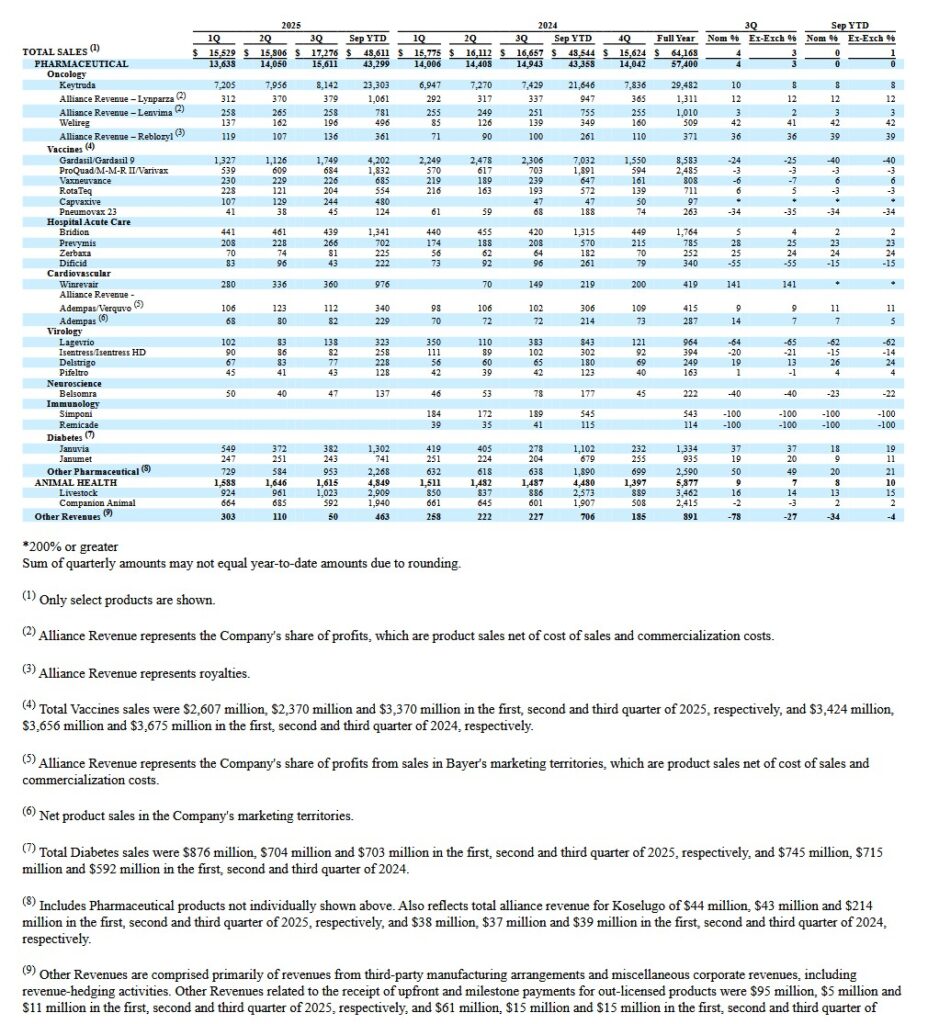

In Q3 2025, MRK generated ~$17.276B of revenue. Keytruda, however, represented ~$8.1B of this revenue!

Keytruda, MRK’s blockbuster drug is an immunotherapy cancer medication approved to treat many different types of cancer, including lung cancer, skin cancer, bladder cancer, and more. It is given as an intravenous (IV) injection by itself or in combination with other cancer treatments.

Gardasil and Gardasil 9 are HPV vaccines that protect against infection with human papillomaviruses (HPV). HPV is a group of more than 200 related viruses, of which more than 40 are spread through direct sexual contact. Gardasil 9 has, since 2016, been the only HPV vaccine used in the United States.

Gardasil and Gardasil 9 are the 2nd highest revenue-generating drug within MRK’s drug portfolio. This drug begins to lose patent protection in 2028 and the significant decrease in revenue from this product is primarily attributed to the drop in sales in China.

As noted earlier, it takes considerable time and money to develop a drug that ultimately receives regulatory approval. MRK, therefore, is heavily focusing on its efforts to bolster its pipeline of drugs and to create drugs that receive regulatory approval. In the first 9 months of FY2025, it incurred research and development costs of ~$11.903B.

In order to reduce its heavy reliance on Keytruda, MRK is advancing its early- and late-phase pipeline. It has tripled its late-phase pipeline since 2021. It is also launching new growth drivers and estimates that recent launches and late-phase pipeline drugs present a $50B+ commercial opportunity by mid-2030s.

The following is a snapshot of MRK’s Q3 2024 and Q3 2025 performance.

We see from the FY2020 – FY2022 and the first half of FY2023 sales results that Keytruda is MRK’s blockbuster drug.

Keytruda’s U.S. loss of exclusivity for the original intravenous formulation is expected in 2028 which opens the opportunity for biosimilar competition then. In Europe, market exclusivity is expected to end around 2031, with Japan following in 2032–2033.

While MRK has several promising drugs in its pipeline, it is aggressively working to extend Keytruda’s exclusivity by expanding its benefits, including for earlier-stage patients.

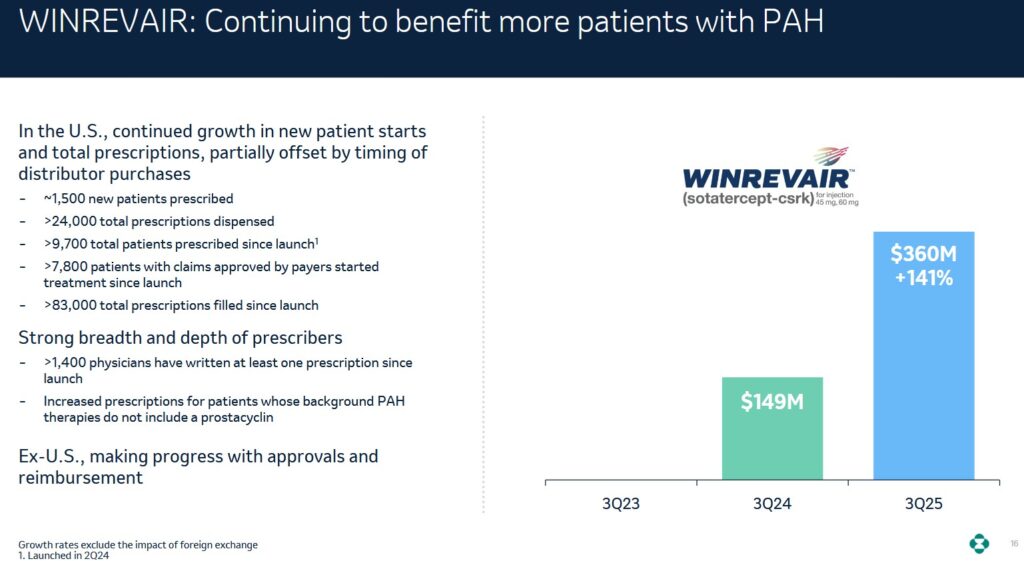

NOTE: The Q3 2025 earnings release includes additional informative tables. MRK’s soon-to-be-blockbuster Winrevair has arisen from its ~$11.5B buyout of Acceleron in 2021. The Federal drug Administration (FDA) has very recently signed off on a label update for the first-in-class activin signaling inhibitor, which was the key piece of the Acceleron acquisition. The new approval adds language to the medicine’s label about its ability to reduce patients’ risk of hospitalization for pulmonary arterial hypertension (PAH), lung transplantation and death.

MRK’s soon-to-be-blockbuster Winrevair has arisen from its ~$11.5B buyout of Acceleron in 2021. The Federal drug Administration (FDA) has very recently signed off on a label update for the first-in-class activin signaling inhibitor, which was the key piece of the Acceleron acquisition. The new approval adds language to the medicine’s label about its ability to reduce patients’ risk of hospitalization for pulmonary arterial hypertension (PAH), lung transplantation and death.

In PAH, the blood vessels narrow in the lungs, which causes blood pressure to increase, leading to heart failure. Roughly 40,000 people in the U.S. have the disorder, which often leads to death and strikes more women than men.

Winrevair reduced the risk of mortality by 76% versus placebo. Patients in the trial’s treatment cohort received a subcutaneous dose of Winrevair every three weeks, and the median follow-up with patients was 10.6 months.

The results were so conclusive that the trial was halted at an interim stage in November 2024 at the urging of an independent data monitoring committee, which also advised MRK to offer Winrevair to all patients in the study.

On the Vaccines & Infectious Disease front, MRK reported CAPVAXIVE 1 sales of $244M driven by demand from retail pharmacies and non-retail customers, as well as expected seasonal inventory build. This is up from $47 million in Q3 2024.

In Animal Health, Q3 2025 sales increased ~7% to ~$1.6B from ~$1.4B and ~$1.5B in Q3 2023 and Q3 2024.

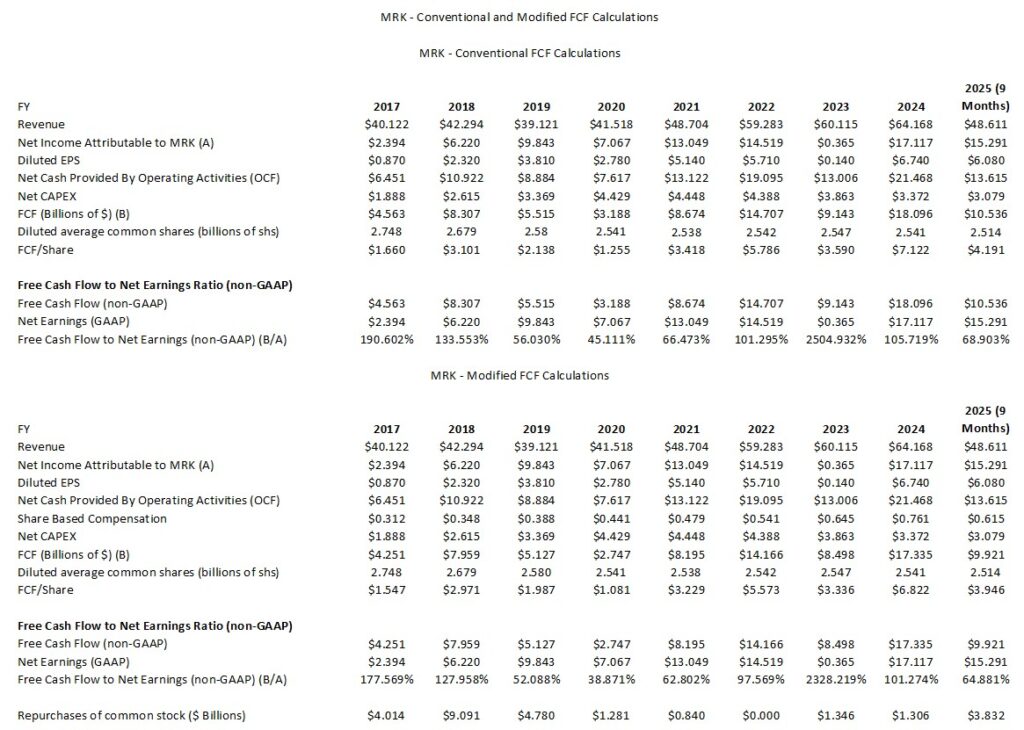

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2017 – YTD2025 (9 Months))

In several posts I express my thoughts about how many companies calculate Free Cash Flow (FCF). Since FCF is a non-GAAP metric, there is no standardization in its calculation.

In most cases, companies merely deduct net CAPEX from net cash flows from operating activities. I choose to also deduct share based compensation (SBC) to arrive at a modified FCF.

MRK remains focused on pursuing opportunities that have the potential to drive both near- and long-term growth. This entails heavy investments in Acquisitions, Research Collaborations and Licensing Agreements. These heavy investments can vary considerably YoY. It is not, therefore, surprising diluted earnings and FCF experience large YoY swings.

MRK’s annual CAPEX is ‘relatively’ modest having been ~$3.3B – ~$4.5B for the past few years. MRK, however, prioritizes its research and development efforts and at FYE2024 it employed ~23,500 people in its research activities. In FY2022 – FY2024 it incurred R&D expenses of ~$13.5B, ~$30.5B, and ~$17.9B. In the first 9 months of FY2025 it incurred ~$11.9B in R&D expenses.

Having said this, on October 20 MRK announced the start of construction for a $3B, 400,000-square-foot pharmaceutical manufacturing facility at its Elkton, Virginia, site. This investment in the Center of Excellence for Pharmaceutical Manufacturing is part of a more than $70B investment beginning in 2025 to expand domestic manufacturing and research and development.

Capital Allocation

The following reflects MRK’s capital allocation over the past 12 months.

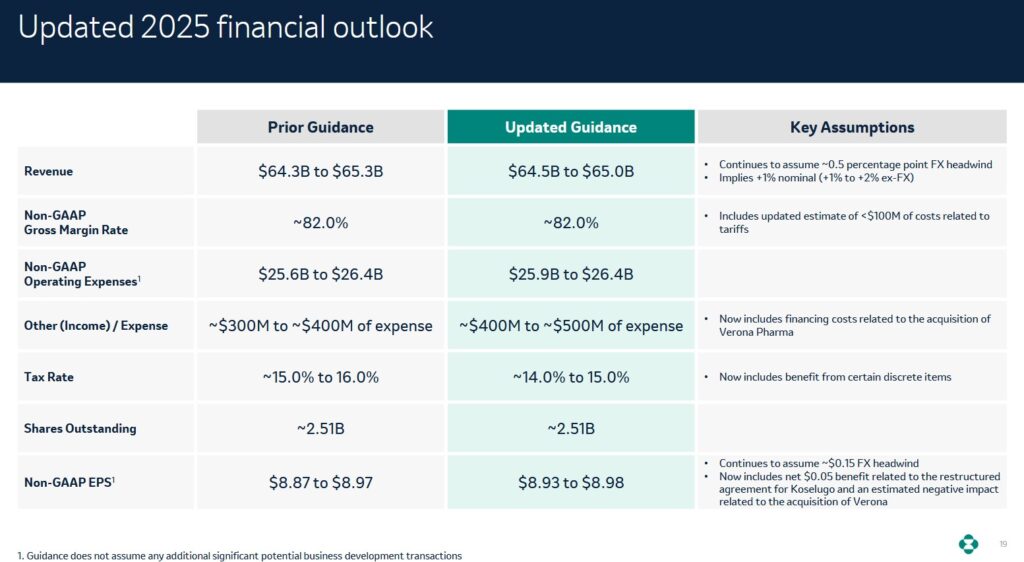

FY2025 Financial Outlook

MRK’s revised FY2025 financial outlook reflects minor changes from the prior outlook.

Risk Assessment

Credit Risk

MRK’s senior domestic unsecured long-term debt is investment grade.

- Moody’s: Aa3 upgraded from A1 on March 24 2025

- S&P Global: A+ (stable outlook) last reviewed on May 15 2025

Moody’s rating is the bottom tier within the high grade investment grade category. It defines MRK as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

S&P’s rating is the top tier within the upper-medium grade category. It defines MRK as having a STRONG capacity to meet its financial commitments. MRK, however, is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

As a relatively conservative investor, MRK’s satisfy my risk tolerance.

The following ratings for a few of MRK’s major competitors are provided for comparison:

Eli Lilly’s (LLY) ratings are the same as MRK’s.

- Moody’s: Aa3 upgraded from A1 on February 7 2025

- S&P Global: A+ (positive outlook) last reviewed on August 18, 2025

Johnson & Johnson’s (JNJ) senior domestic unsecured long-term debt ratings are:

- Moody’s: AAA affirmed on January 14 2025

- S&P Global: AAA affirmed on April 25 2025

These ratings define JNJ as having an extremely strong capacity to meet its financial commitments.

Novo Nordisk’s (NVO) long-term issuer (foreign currency) ratings are:

- Moody’s: Aa3 upgraded from A1 on January 22, 2025

- S&P Global: AA upgraded from AA- on May 19 2025

Moody’s rating defines NVO as having an extremely strong capacity to meet its financial commitments.

S&P’s rating is the middle top tier within the high grade investment grade category. It defines NVO as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

AstraZeneca’s (AZN) senior domestic unsecured long-term debt ratings are:

- Moody’s: A1 with a stable outlook upgraded from A2 on February 21 2025

- S&P Global: A+ with a stable outlook upgraded from A on July 26 2024

Both ratings are the top tier within the upper medium grade category. They define AZN as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Bristol-Myers Squibb’s (BMY) senior domestic unsecured long-term debt ratings are:

- Moody’s: A2 with a stable outlook affirmed on December 2 2024

- S&P Global: A with a stable outlook affirmed on January 10 2025

Both ratings are the middle tier within the upper medium grade category. They define BMY as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Pfizer’s (PFE) senior domestic unsecured long-term debt ratings are:

- Moody’s: A2 with a stable outlook downgraded from A1 on December 13 2023

- S&P Global: A with a stable outlook downgraded from A+ on December 13 2023

Both ratings are the middle tier within the upper medium grade category. They define BMY as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Abbvie (ABBV)

- Moody’s: A3 with a stable outlook affirmed on August 1 2024

- S&P Global: A- with a stable outlook affirmed on April 1 2025

Both ratings are the bottom tier within the upper medium grade category. They define BMY as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Reputational Risk

Reputational risk refers to the potential for damage to an organization’s reputation, brand, or public standing, which can result from negative publicity, ethical lapses, operational failures, or any incident that diminishes stakeholder trust and confidence. This type of risk can arise directly from a company’s own actions, indirectly from employee conduct, or tangentially through business partners, suppliers, or customer interactions.

This type of risk encompasses any event or behavior that can result in negative perceptions and loss of trust, thereby threatening an organization’s financial performance and ongoing viability.

It is highly relevant in the pharmaceutical manufacturing industry due to the sector’s critical role in public health and its history of intense public scrutiny.

Valeant Pharmaceuticals readily comes to mind when I think of pharmaceutical companies that imploded because of malfeasance. This company’s share price touched ~$260 in July 2015; the current share price is ~$7.00.

Following revelations of price inflation and fraudulent accounting practices, the company rebranded (Bausch Health Companies Inc. (BHC)) and settled numerous legal actions related to its past misconduct. The company is now saddled with significant debt.

Fitch currently assigns a CCC+ Issuer Default Rating. This non-investment grade rating defines BHC as being currently vulnerable and dependent upon favourable business, financial, and economic conditions to meet its financial commitments. A quick look at this company’s Q3 2025 Form 10-Q confirms this company is in a heap of trouble.

More recently, Ascend Laboratories and its parent company (Alkem Laboratories in India) has been in the news…and not in a good way.

As one of the world’s leading major drug manufacturers, MRK can’t afford the risk of becoming another Valeant or Alkem. It, therefore, invests heavily to protect its reputation. This gives me confidence that the probability is low that my MRK investment will implode overnight because its reputation has been tarnished.

Dividend and Dividend Yield

MRK’s dividend history reflects October 7 as being the distribution date of the 4th consecutive $0.81 quarterly dividend. MRK will likely declare its next quarterly dividend shortly. I envision a ~$0.04/share increase in the quarterly dividend.

As noted in several prior posts, fixating on dividend metrics is not recommended. The focus should be on total potential investment return.

Depending on your investor profile, however, you may want/need dividend income. If such is the case, MRK generates ample Cash Flow from Operations and Free Cash Flow. This is extremely important because dividend distributions are typically MRK’s 2nd largest form of capital allocation.

In FY2011, MRK’s average shares outstanding (in billions) was 3.094. In Q3 2025, the average outstanding diluted shares is 2.498 but management’s FY2025 outlook assumes ~2.51 outstanding.

On the Q3 2025 earnings call, management states:

We are maintaining our increased pace of share repurchases and expect approximately $5B for the full year.

Management seeks to provide a competitive return to shareholders through a growing dividend and share repurchases. This is balanced with the need to invest in the business to drive growth and business development. The desire is not to create excess cash on the balance sheet. MRK, therefore, looks opportunistically at share buybacks based on the assessment of the business development pipeline.

In October 2018, the Board authorized purchases of up to $10B of MRK’s common stock for its treasury. The treasury stock purchase authorization has no time limit.

In January 2025, it authorized purchases of up to an additional $10B of the company’s common stock for its treasury. The treasury stock purchase authorizations have no time limit and will be made over time in open-market transactions, block transactions on or off an exchange, or in privately negotiated transactions.

During the first nine months of 2025, MRK purchased ~$3.832B (46 million shares) of its common stock for its treasury under these programs. MRK expects the pace of share repurchases to continue at this level for the remainder of 2025.

As of September 30, 2025, the remaining share repurchase authorization was ~$8.6B.

Valuation

My prior assessment of MRK’s valuation is accessible in my August 4, 2023 post.

In the first 9 months of FY2025, MRK generated $6.08 and $6.93 of diluted EPS and adjusted diluted EPS. The company’s revised FY2025 adjusted diluted EPS outlook is $8.93 – $8.98.

On October 28 I increased my exposure with the purchase of 200 shares @ $87.02. Using this purchase price and the ~$8.96 mid-point of the revised FY2025 adjusted diluted EPS outlook, the forward adjusted diluted PE is ~9.71. As I complete this post after the November 5 market close, however, the share price is ~$84.40. At this share price, the forward adjusted diluted PE is ~9.42.

Using the adjusted diluted EPS estimates from the brokers who cover MRK and a ~$84.40 share price, the forward adjusted diluted PE levels are:

- FY2025: 14 brokers – mean of $8.97 and a low/high range of $8.94 – $9.07. The forward adjusted diluted PE using the mean estimate is ~9.41.

- FY2026: 14 brokers – mean of $9.25 and a low/high range of $8.71 – $9.80. The forward adjusted diluted PE using the mean estimate is ~9.12.

- FY2027: 11 brokers – mean of $10.19 and a low/high range of $9.39 – $10.95. The forward adjusted diluted PE using the mean estimate is ~8.28.

In the first 9 months of FY2025, MRK’s FCF/share is ~$4.191 and $3.946 calculated using my conventional and modified methods. If it generates a comparable level of FCF in Q4 as in each of the first 3 quarters, the FY2025 should be ~$5.59 ($4.191 + (33.33% of $4.191)) and ~$5.26 ($3.946 + (33.33% of $3.946)). With shares trading at ~$84.40, the forward P/FCF is ~15.1 and ~16.

Final Thoughts

MRK’s annual diluted EPS and FCF over the past several years has experienced wide YoY swings. Given the October 20, 2025 announcement to expand domestic manufacturing and research and development to the tune of $70B over the coming years, MRK investors should expect further wild YoY earnings and FCF variances.

The success of a pharmaceutical company is heavily dependent on obtaining FDA approval for new drugs. Pharmaceutical companies invest a considerable amount in R&D only to have most drugs under development failing to receive FDA approval. Given that the patents on its Keytruda blockbuster drug begin to expire in 2028 and the Gardasil patents expire in 2028 in the US, MRK is actively pursuing M&A opportunities to bolster its pipeline.

Growth through M&A, however, is not without risk.

Earlier in this post I present two acquisitions totaling ~$13.9B that were completed in recent months. MRK also completed the ~$11.5B Acceleron Pharma acquisition in November 2021 and the $10.8B acquisition of Prometheus Biosciences, Inc. in June 2023. These acquisitions alone total ~$36.2B!

My exposure to the major drug manufacturers is limited to JNJ and MRK. I do, however, have exposure to Thermo Fisher (TMO), Intuitive Surgical (ISRG), Agilent (A), Danaher (DHR), Veeva Systems (VEEV), and West Pharmaceutical (WST) that all fall within the Healthcare sector.

At this point, I intend to just gradually increase my exposure through the automatic reinvestment of the quarterly dividends.

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long MRK.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.