I last reviewed CME Group Inc. (CME) in this April 26, 2025 post at which time the Q1 2025 results were the most current. With the release of the Q2 2025 financial results on July 23, 2025, I revisit this existing holding.

I last reviewed CME Group Inc. (CME) in this April 26, 2025 post at which time the Q1 2025 results were the most current. With the release of the Q2 2025 financial results on July 23, 2025, I revisit this existing holding.

Business Overview

CME operates a derivatives marketplace which offers a range of futures and options products for risk management. It is where market participants turn to manage risk across the most diverse set of benchmark products.

Please review the company’s website and Part 1 of the FY2024 Form 10-K.

Financials

Q2 and YTD2025 Results

The Q2 and YTD2025 earnings release is accessible through the SEC Filing section of the company’s website. In this earnings release we see that CME reported all-time record revenue, adjusted operating income, adjusted net income, and adjusted EPS surpassing records set in Q1 2025.

This earnings release reflects the following:

Demand for CME Group benchmark futures and options reached an all-time high in Q2 as clients around the globe turned to our markets to manage their business risks across asset classes,” said Terry Duffy, CME Group Chairman and Chief Executive Officer. “During the quarter, our average daily volume (ADV) rose 16% to a record 30.2 million contracts, driving double-digit growth and setting new records for revenue, adjusted operating income, adjusted net income and adjusted earnings per share. Notably, the number of new retail traders at CME Group increased 57% year over year, contributing to record Micros ADV of 4.1 million contracts in Q2 and demonstrating the appeal of our products to a broader base of users.

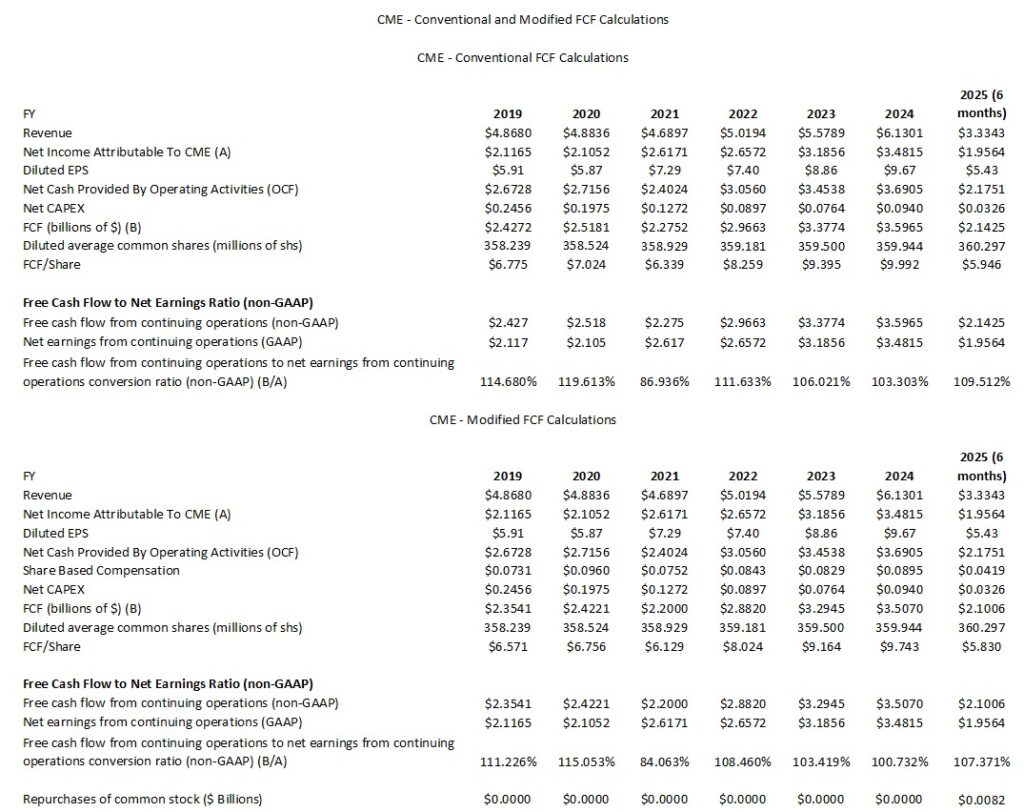

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2024 and YTD2025)

FCF is a non-GAAP measure, and therefore, its calculation is inconsistent. Many investors deduct CAPEX from OCF to arrive at FCF. In my How Stock Based Compensation Distorts Free Cash Flow post, I explain why I now also deduct stock based compensation (SBC) that is found in the Consolidated Statements of Cash Flows to determine FCF.

The conventional method only deducts CAPEX from OCF while the more conservative modified method also deducts SBC.

FY2025 Guidance

CME does not issue guidance.

Risk Assessment

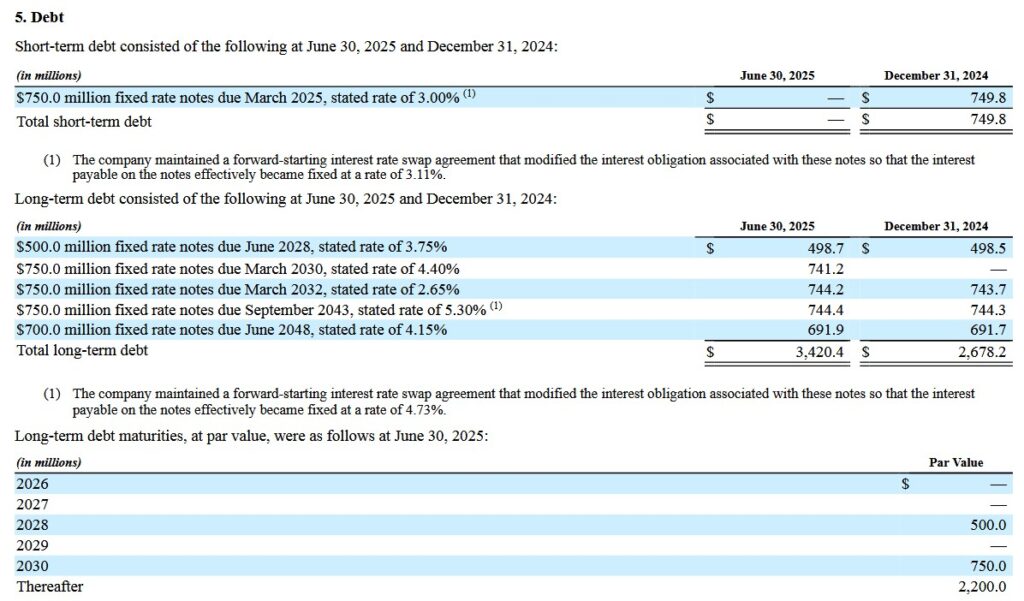

In March 2025, CME completed an offering of $750.0 million of its 4.4% fixed rate notes due March 2030 and also repaid the $750.0 million of 3% fixed rate notes due March 2025.

CME’s senior unsecured long-term debt ratings are the lowest tier of the high-grade category and are investment grade. These ratings define CME as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

- Moody’s: Aa3 with a stable outlook (affirmed May 19, 2025)

- S&P Global: AA- with a stable outlook (affirmed July 18, 2025)

- Fitch: AA- with a stable outlook (affirmed February 6, 2025)

These strong ratings are acceptable for my risk tolerance.

Dividend and Dividend Yield

The following is reflected in CME’s FY2024 Form 10-K.

We intend to continue to pay a regular quarterly dividend to our shareholders, with a target of between 50% to 60% of the prior year’s cash earnings. The decision to pay a dividend and the amount of the dividend, however, remains within the discretion of our board of directors and may be affected by various factors, including our earnings, financial condition, capital requirements, levels of indebtedness and other considerations our board of directors deems relevant. We are also required to comply with restrictions contained in the general corporation laws of our state of incorporation, which could limit our ability to declare and pay dividends.

CME’s dividend history is accessible here.

NOTE: In conjunction with the December 5, 2024 declaration of the ‘special’ dividend, CME indicated that it intends to continue its variable dividend structure. Beginning in 2026, however, the declaration and payment of the annual variable dividend will align with the first quarter regular dividend paid in March 2026 rather than at the end of the calendar year.

In FY2014 and FY2024, the weighted average outstanding diluted shares outstanding (in millions of shares rounded) was 336.063 and 359.944. In the 6 months ending June 30, 2025, it was ~360.297.

Shares are issued as part of the company’s employee compensation programs. CME, however, has not repurchased shares in recent years thus leading to the steady increase in the weighted average diluted shares outstanding.

In December 2024, CME’s Board approved a share repurchase program which authorizes the repurchase of up to $3.0B of the company’s Class A common stock at prevailing market prices.

CME has yet to make any meaningful share repurchase which is just as well since shares are overvalued.

Valuation

The following valuation calculations use the July 25, 2025 closing share price of $279.55.

Management does not provide earnings guidance, and therefore, I extrapolate YTD2025 results. In the first half of FY2025, CME generated diluted EPS and adjusted diluted EPS of $5.43 and $5.75. If the second half of the year is relatively similar to the first half, FY2025 diluted EPS and adjusted diluted EPS should be ~$10.86 and ~$11.50. Erring on the side of caution, I use the ~$11.18 mid-point thus suggesting the current adjusted diluted PE is ~25.

Using the current forward adjusted diluted EPS broker estimates, CME’s forward adjusted diluted PE levels are:

- FY2025 – 17 brokers – mean of $11.15 and low/high of $10.75 – $11.53. Using the mean estimate, the forward-adjusted diluted PE is ~25.1.

- FY2026 – 17 brokers – mean of $11.59 and low/high of $10.94 – $12.11. Using the mean estimate, the forward-adjusted diluted PE is ~24.1.

- FY2027 – 11 brokers – mean of $12.39 and low/high of $11.55 – $13.06. Using the mean estimate, the forward-adjusted diluted PE is ~22.6.

CME’s YTD2025 FCF/share is ~$5.946 and ~$5.830 using the conventional and modified calculated methods. I do not anticipate any share repurchases the remainder of the year. Fortunately, additional SBC in the second half of the year is unlikely to be meaningful. Given this, the weighted average diluted shares outstanding in FY2025 should be just marginally higher than the YTD weighted average. On this basis, I estimate CME’s FY2025 FCF will be ~$11.90 and ~$11.67. Divide the current $279.55 share price and CME’s P/FCF is likely close to ~23.5 and ~24. CME’s FCF conversion ratio is typically above 100% so it seems reasonable to expect CME’s valuation based on FCF to be slightly superior to that based on adjusted diluted EPS.

Final Thoughts

I currently hold 477 shares in in a ‘Core’ account and 412 shares in a ‘Side’ account within the FFJ Portfolio.

Although I only added to my CME exposure by way of the automatic reinvestment of dividend income, it was my 11th largest holding when I completed my 2025 Mid-Year Portfolio Review versus being the 13th largest holding when I completed my 2024 Year-End Portfolio Review.

Despite the comments in my Dividends Have Drawbacks post, I am a CME shareholder because I like the business and long-term prospects.

In my prior post I note that share repurchases have historically not been a capital allocation priority. I remain of the opinion that this is about to change since CME’s Board approved in December 2024 the repurchase of up to $3B of Class A common stock at prevailing market prices.

Furthermore, on April 23 CME entered into a new multi-currency revolving credit facility maturing on April 23, 2030. This Senior Credit Facility is for a line of credit of $2.25B with the option to increase the facility from time to time from $2.25B to $3.25B. The proceeds of the Senior Credit Facility can be used for ongoing working capital and other general corporate purposes and is voluntarily pre-payable from time to time without premium or penalty.

Interestingly, this new facility coincided with the announcement that CME and S&P Global (SPGI) signed a definitive agreement to sell OSTTRA, a leading provider of post-trade solutions for the global OTC market, to investment funds managed by KKR, a leading global investment firm. The terms of the deal equals a total enterprise value of $3.1B, subject to customary purchase price adjustments. Proceeds will be divided evenly between SPGI and CME pursuant to their 50/50 joint venture. The transaction is expected to close in the second half of 2025.

Management states that it can grow its business without having to resort to strategic acquisitions. On several recent quarterly earnings calls, management speaks about the importance of new client acquisition (NCA). In Q1 2025, NCA surged 44% to over 83,000 new traders making it the 4th consecutive quarter of double-digit NCA growth. In Q2 2025, over 90,000 new retail traders participated in CME’s markets for the first time. This is a 56% increase versus same period last year.

Given this, I anticipate that the increase in its credit facility and the OSTTRA sale proceeds will be used to repurchase shares (if/when shares become undervalued).

I am of the opinion that CME is slightly overvalued with a fair price being closer to ~$245. At this price, CME’s forward adjusted diluted PE is ~22 if we use the brokers’ FY2025 mean adjusted diluted EPS of $11.15. The P/FCF is ~20.6 and ~21 using my FY2025 FCF estimates of ~$11.90 and ~$11.67.

Until such time as CME’s valuation improves, I will merely continue to increase my exposure through the automatic reinvestment of dividend income.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CME.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.