I last reviewed Copart (CPRT) in this February 21, 2025 post where I disclose the purchase of an additional 400 shares @ ~$56.29 in a ‘Side’ account within the FFJ Portfolio.

On May 22, 2025, CPRT released its Q3 and YTD2025 results. Despite reporting strong results, the company’s share price has fallen from ~$64 in mid-May to ~$52.30. Based on my analysis and long-term prognosis for this company, I acquired another 100 shares @ ~$52.13 on May 28 on behalf of a young investor I am helping on their journey to financial freedom.

Much like Zoom Communications (ZM) (see my May 27, 2025 post), CPRT is ‘swimming’ in liquidity.

- the held to maturity securities are primarily U.S. Treasury Bills.

- less than 10% of the cash, cash equivalents, and restricted cash is held by CPRT’s foreign subsidiaries. Should these funds be needed for CPRT’s US operations, the repatriation of these funds could be subject to the foreign withholding tax. Management’s intent, however, is to permanently reinvest these funds outside of the US and the current plans do not require repatriation to fund the US operations.

Some investors may argue that CPRT holds far too much ‘cash’. My support for CPRT’s level of liquidity, however, is the same as that for ZM.

Business Overview

Section 1 of CPRT’s Form 10-K provides a good overview of the company (refer SEC Filings).

I encourage you to watch some ‘live’ CPRT auctions.

CPRT, the largest online salvage vehicle auction operator in the US, was founded in 1982. Since 2003, however, all auctions are been online. By holding all auctions online, CPRT is able to connect buyers and sellers around the world.

In hindsight, I wish I had known about the company a couple of decades ago because CPRT has grown its top line nearly five-fold since 2009. Fortunately, the probability of CPRT’s growth stagnating is unlikely. It continues to receive the majority of its vehicle volume through contracts with large auto insurers and then sells these vehicles on consignment for high margins often to

dismantlers.

There are several reasons why insurers like to use CPRT, one of which is CPRT having adequate storage capacity and providing flexible service. Imagine being an insurance company whose customer base gets hit hard by a hurricane. Insurance companies are not in a position to recover and store damaged vehicles nor are they set up to try and recover some of their insurance payouts.

While some damaged vehicles may have little appeal to North American buyers, CPRT’s online platform allows parties in other parts of the world to access damaged vehicles which they can restore to meet local demand.

The industry is highly fragmented but CPRT is the industry leader. There may be many auto salvage yards but most can only cater to their local market.

RB Global (RBA) (formerly Ritchie Bros.) is one of CPRT’s primary competitors. Its global marketplace provides value-added insights, services, transaction solutions for buyers and sellers of commercial assets and vehicles worldwide. Through its auction sites in 14 countries and digital platforms, it serves customers and partners in ~170 countries across a variety of asset classes,

including automotive, commercial transportation, construction, government surplus, lifting and material handling, energy, mining and agriculture.

While seemingly impressive, Moody’s and S&P Global assign a Ba1 and BB+ Corporate Family Rating. These ratings have recently been upgraded one tier but these ratings are still non-investment grade. Furthermore, equity investors face a greater risk than debt holders. Anybody considering a RBA equity investment needs to be fully aware of their risk exposure.

Why anybody would invest in a junk rated company versus a company that is ‘swimming in liquidity’ is beyond me. In the current environment, however, many investors appear to be tossing caution to the wind.

Financials

Q3 and YTD2025 Results

CPRT’s financial results are available through the SEC Filings section of the company’s website; the Q3 Form 10-Q is unavailable as I compose this post.

The company’s cash, cash equivalents, and restricted cash and investment in held to maturity securities increased to ~$4.384B versus ~$3.422B at FYE2024 (July 31). This increase is despite YTD2025 net CAPEX of ~$0.482B!

In addition to its cash, CPRT has an unused revolving credit facility of over $1.2B.

YTD2025, net cash provided by operating activities is ~$1.361B versus ~$1.033B during the same period in the prior fiscal year.

Few companies have 100% ZERO exposure to tariffs. Having said this, CPRT has much less exposure than just about every other US auto-related company.

YTD revenue and gross profit has risen by 11.2% and 9.4%, respectively. YTD total operating expenses, however, have risen ~14.4%. On the Q3 2025 earnings call, management stated the following about the increase in General and Administrative expenses:

The main driver of the increase was attributable to our continued investment in the sales force within Purple Wave. The rest was really just some minor investments across our platform services to support our global organization. We don’t necessarily look to that or provide guidance in terms of whether or not that is a steady-state number. We make investments from time to time in projects and solutions that we think and believe will drive greater operating leverage for the business in the future.

And so I wouldn’t point you to that as being a run rate, but each individual investment that we do make into G&A, we do take an investment mindset approach to it and ensure that there are tangible returns that we will achieve, whether it’s through cost reduction efficiency or other opportunities for the business more generally.

NOTE: I touch upon CPRT’s Purple Wave investment in my November 17, 2023 post.

Land Acquisition

In prior posts I touch upon the number of facilities CPRT has in various regions (see locations). CPRT, however, is continually expanding its presence. In early 2025, it acquired 835 acres in Charlotte County, Florida. In Q3, CPRT expanded its South Florida operations through a $65 million acquisition of nearly 40 acres of prime industrial land in Palm Beach County. These purchases are included in the YTD2025 ‘Purchases of property and equipment’ totaling ~$0.481B reflected on the Consolidated Statements of Cash Flows.

Once CPRT acquires land, however, it does not serve much purpose unless there is the appropriate infrastructure to operate a yard. This is another significant component of the property and equipment expenditures.

Given the number of CPRT locations, it is impressive that CPRT is able to fund its property and equipment (for maintenance and growth purposes) needs without availing itself of debt.

Note 5 – Leases in the FY2024 Form 10-K provides details about CPRT operating and finance lease liabilities. In the grand scheme of things, the current and long-term portion are not that significant coming in at ~$0.1B at the end of Q3 2025.

Q3 2025 Earnings Call Transcript

The following is CPRT’s CEO commentary from the Q3 2025 earnings call which addresses key topics that impact CPRT’s performance and outlook.

Starting with our insurance business, our global insurance volume remained relatively flat year-over-year with a nominal decline of 0.3% globally in unit sales and 0.9% in the United States. Accounting for the extra business day of leap year 2024, global insurance and U.S. insurance units sold grew by 1.3% and 0.6%, respectively.

At the same time, total loss frequency continues to rise as it has throughout the vast majority of the history of our industry. In the United States, total loss frequency reached 22.8% in the first calendar quarter of 2025, up 100 basis points or thereabouts in comparison to last year. And while individual quarters can fluctuate and from time to time, we observed even seasonal effects, the underlying drivers of total loss frequency remain quite consistent over time.

First, the economics of vehicle repairs become less economically attractive to our client base, the insurance industry, with increasing vehicle complexity, rising parts prices, rising labor rates, storage fees, rental car expenses as well. At the same time, on the other side of the ledger, the economics of total loss become more attractive over time.

For emerging economies around the world, our salvaged vehicles are an essential source of mobility for them. Copart’s auction technology and our ecosystem of sellers and members is uniquely well suited to finding the highest and best use for every vehicle we touch.

In anticipating a question about why nominal insurance volumes haven’t kept pace with what appears to be rising total loss frequency, we’d offer a couple of notes.

First, the precision of total loss frequency measures do vary or does vary. The varying nature of the calculation is to assess what portion of the claims in any individual quarter are ultimately resolved to be a total loss in the end, meaning some figures are even revised after the fact for historical periods. And notably, we observe that there are cyclical forces at work as well, including an increase in the rate of uninsured and underinsured drivers. According to the Insurance Research Council, they observed meaningful increases in both over the course of the past 4 years. And we would note cyclical trends over the decades in terms of the rate of uninsured and underinsured drivers. What that means in practical — in practice is that drivers with coverage of that type may never bring their vehicles into the traditional insurance claim settlement pathway in the first place. We would expect, over time, as has been proven over the decades, that these cyclical forces will reverse — will revert at some point as well.

I wanted to turn my attention to the 2025 storm season. Meteorologists and experts have released a number of forecasts for how they expect 2025 storm season to unfold, noting that 2024 was an active season itself. Most would expect based on above-average oceanic temperatures that this form season could well be an active one as well, perhaps as active as 2024. In anticipation of these types of events, we continue to invest in real estate, infrastructure, technology, our people and other aspects of operational readiness.

Our preparation is not an ad hoc spring event, but in fact, a year-round exercise for us as a company. One tangible example is our acquisition of Hall Ranch, a property located in South Florida, which offers nearly 400 usable acres of vehicle storage for a storm. With this addition, we now have the physical footprint to handle a storm more than 3x the size of the largest Florida storms on record in Copart history.

Capital Allocation Strategy

CPRT does not repurchase shares nor does it issue a dividend. Reinvesting in the business is CPRT’s capital allocation priority.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

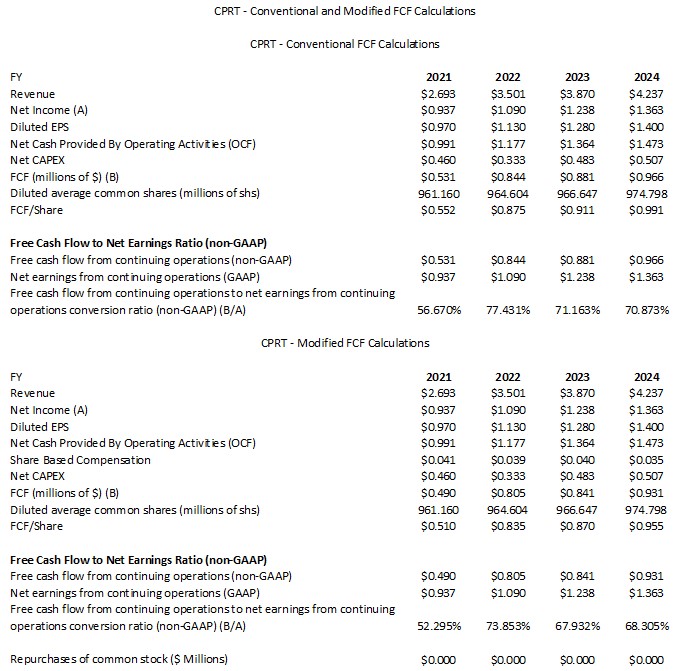

In various prior posts, I deduct stock-based compensation (SBC) when determining a company’s net cash provided by operating activities. This is particularly important when a significant component of a company’s employee compensation is in the form of SBC.

Let’s suppose a company grants a significant number of company shares to employees as part of its various compensation packages. This form of remuneration is not reflected on the Income Statement to determine Net Earnings. If the company did not grant this SBC, however, you would think it would need to boost salaries/wages in order to retain its employees. These higher wages/salaries WOULD be reflected within the Income Statement thus having an impact on earnings.

Some investors may resort to the argument that a company is issuing shares to its employees but is often offsetting these new shares by repurchasing an equal or greater number of shares.

Having looked at countless Form 10-Ks over the years, I see companies granting stock options at prices that are often far below current share prices. So….you have a company repurchasing a boatload of shares at $X but it is issuing shares to employees (with a significant component to senior management) at a small fraction of $X. As a retail investor with an insufficient number of shares to sway the decision making at the Board level, I have no choice but to watch my investment in a company being eroded while insiders and employees are being enriched.

CPRT is unlike companies in the technology sector that have a substantial component of its employee remuneration in the form of share-based compensation. It issues shares to its employees but the annual SBC is negligible. This explains the reason for the moderate FCF variance using the conventional and modified calculation methods.

In the first 3 quarters of FY2025, net cash provided by operating activities is ~$1.361B. Purchases of property and equipment (~$0.481B) and Assets and liabilities acquired in connection with acquisition (~$0.001B) amounts to ~$0.482B giving us YTD FCF of ~$0.879B.

The YTD diluted weighted average common shares outstanding are 977,485 million and will likely be ~980 million shares for the year.

If CPRT generates a similar amount of FCF in Q4 as in prior quarters ($0.879B/3 = ~$0.293B) FY2025’s FCF should be ~$1.172B (~$0.879B + ~$0.293B). Divide ~$1.172B by 980 million shares and we get FCF/share of ~$1.20.

YTD share based compensation (SBC) is ~29 million versus ~20 million in the first half of the year. If FY2025 SBC increases to ~38 million and we subtract this from the FY2025 FCF estimate of ~$1.172B, CPRT should generate ~$1.134B of FCF for the year. Divide ~$1.134B by 980 million shares and we get FCF/share of ~$1.16.

FY2025 Outlook

CPRT does not provide any outlook.

Risk Assessment

CPRT has no debt to rate.

Dividend and Dividend Yield

CPRT has not paid a cash dividend since becoming a public company in 1994.

Stock Splits

Since becoming a shareholder on January 18, 2022, CPRT has had two 2 for 1 stock splits (November 3, 2022 and August 21, 2023).

In FY2013 – FY2024, CPRT’s weighted average number of outstanding shares (in millions of shares rounded) was 1,038, 1,050, 1,051, 977, 948, 968, 962, 955, 961, 965, 967, and 975. This has increased to ~977.5 for the first 9 months of the year and ~978.1 in Q3 2025.

On September 22, 2011, CPRT’s Board authorized a 320 million share increase in the stock repurchase program, bringing the total current authorization to 784 million shares.

The following are previous share repurchases:

- 2013: $572 thousand

- 2014: $15,009 million

- 2015: $233,484 million

- 2016: $442,855 million

- 2018: $364,997 million

There were no repurchases in FY2017, FY2018, FY2020 – FY2024, and YTD2025.

CPRT could easily repurchase shares so as to offset the dilution that has occurred over the last few years. Whether management decides to allocate capital accordingly has not been discussed on recent quarterly earnings calls.

Valuation

My February 21, 2025 post reflects previous valuation estimates.

In the first 3 quarters of FY2025, CPRT generated $1.18 EPS versus $1.07 in the same period in FY2024.

Using the current broker estimates and my May 28 ~$52.13 purchase price, the forward-adjusted diluted PE levels are:

- FY2025 – 11 brokers – ~33.4 based on the mean of $1.56 and low/high of $1.52 – $1.64.

- FY2026 – 11 brokers – ~29.9 based on the mean of $1.75 and low/high of $1.65 – $1.91.

- FY2027 – 6 brokers – ~26.3 based on the mean of $1.98 and low/high of $1.80 – $2.23.

As noted earlier, I estimate CPRT will generate ~$1.20 and ~$1.16 of FCF in FY2025 calculated under the conventional and modified methods. Using my recent ~$52.13 purchase price, CPRT’s P/FCF is ~43.4 and ~45.

CPRT’s valuation appears rich until we consider its dominant industry position, fortress balance sheet, and growth opportunities. Many investors, however, may have no interest in CPRT because:

- the industry is unappealing;

- it issues no dividend; and/or

- it is not a technology company.

While CPRT is not a technology company, it has revolutionized the salvage industry by employing technology.

Final Thoughts

I initiated a CPRT position on February 17, 2022 in one of the ‘Core’ accounts within the FFJ Portfolio and have made various additional purchases since then. CPRT was my 10th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review and 12th largest holding when I completed my 2024 Year End Review. I do not know its current ranking unless I perform another review.

In my February 21, 2025 post, I state that a couple of young investors I am helping on their journey to financial freedom have CPRT exposure. I do not, however, disclose details of their investments. Furthermore, I exclude their holdings when I complete my Mid Year and Year End FFJ Portfolio Reviews.

CPRT is ‘swimming in cash’. This places it in an enviable position of being able to repurchase shares without having to rely on the use of debt. Whether CPRT decides to repurchase shares or not is unknown. I am, however, confident management will allocate capital appropriately so as to generate attractive long-term total investor returns.

Based on the currently available information, I think a fair valuation translates into a ~$60 share price. Based on a $52.13 purchase price, we arrive at a ~15% return if CPRT’s share price retraces to ~$60. This share price is not an unrealistic expectation considering environmental changes are increasing the frequency and intensity of natural disasters; hurricane season in the US is but a few months away!

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CPRT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.