This post is written from the perspective of a Canadian resident/taxpayer. I also have no knowledge of your circumstances, risk tolerance, goal, and objectives. You should, therefore, not rely on my recommendations without advice from legal and financial professionals who understand your specific circumstances.

My examples reflected below are based on a family with 1 young adult. If you have 2 or more young adults, the data I use may be unrealistic. I, therefore, encourage the use of input data in this calculator that is appropriate for you.

In addition, this post does not address how to help young adults who have yet to complete their education. Given this, I do not address the funding of education costs and the use of Registered Education Savings Plans (RESPs).

Let’s dive in.

Tax Free Savings Account (TFSA)

The Tax Free Savings Account (TFSA) was established in 2009. If you were 18 or older in 2009 and have never contributed to a TFSA, your cumulative contribution room is currently $102,000.

For a young adult to immediately raise $102,000 is somewhat daunting. Depending on your circumstances, however, you may be in a position to help young adults by making TFSA contributions to an account held in their name.

Using this calculator we see the long-term impact of TFSA contributions over time.

In 2025, the annual TFSA contribution limit is $7000. In this example, however, I assume:

- the young adult has never opened a TFSA;

- lending a $50,000 lump-sum for the young adult’s initial TFSA contribution;

- a $5000 annual contribution at the beginning of every year for the next 40 years; and

- a 6% average annual rate of return.

The parent or young adult can make the annual TFSA contribution. I prefer that the young adult make the annual contribution so they ‘have skin in the game’.

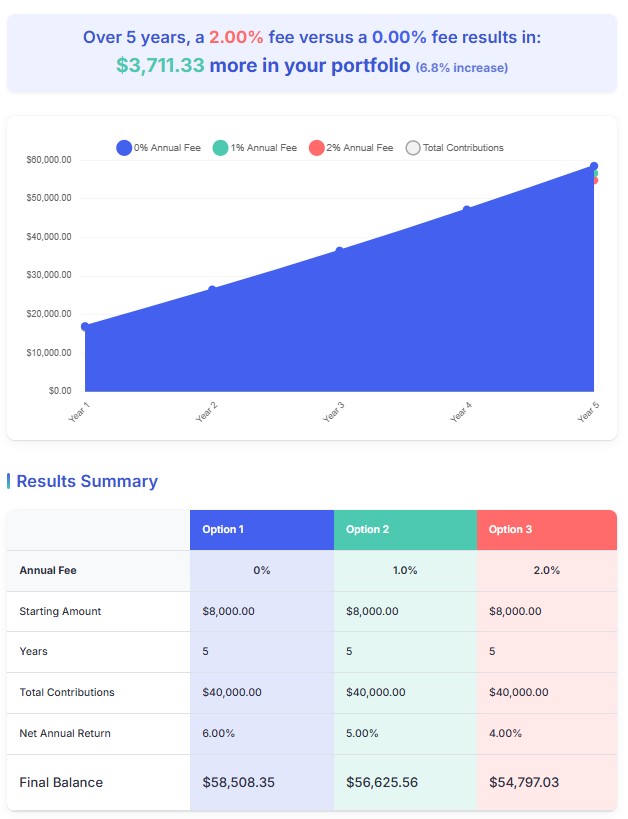

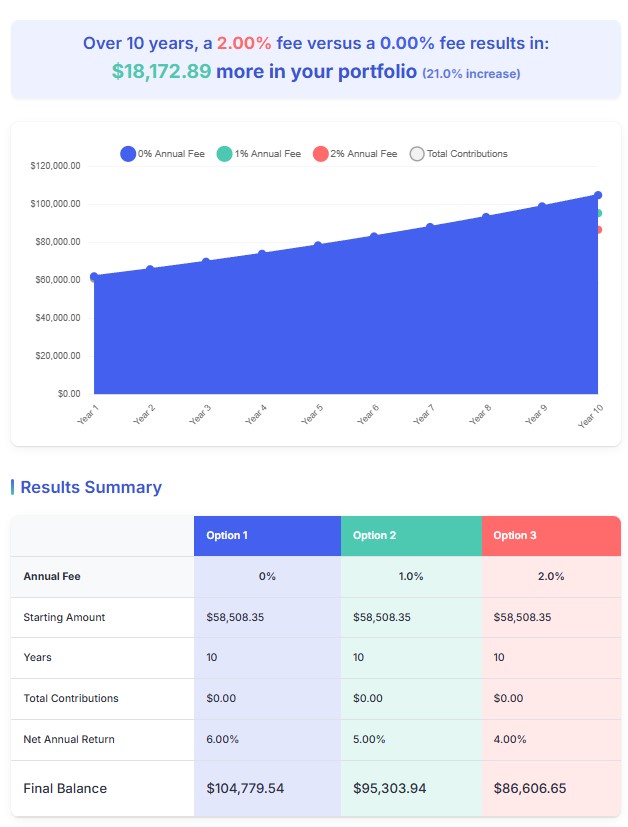

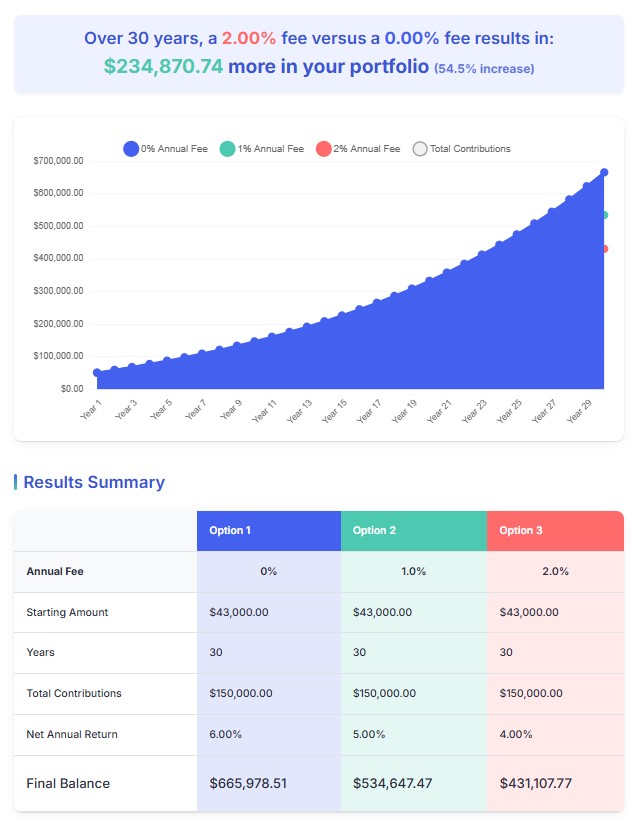

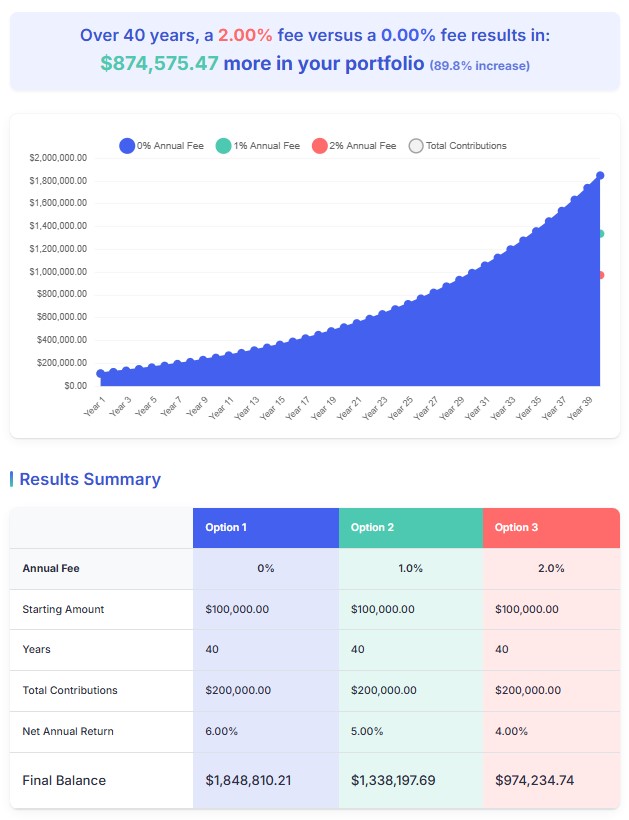

The TFSA should have a value in excess of $1.3 million in the 40th year. The caveat is the use of a self-directed plan to limit the fees to a nominal fee per trade. If you resort to investing through a mutual funds, we see how fees erode the value of the TFSA.

First Home Owner Savings Account (FHSA)

A First Home Owner Savings Account (FHSA) is a registered plan which allows a first-time home buyer to save to buy or build a qualifying first home tax-free (up to certain limits); these accounts became available on April 1, 2023.

The FHSA participation room in the first year of owning a FHSA is $8,000. Contributions to a FHSA are generally tax deductible. Transfers from your RRSPs to your FHSAs, however, are not tax deductible. Additional details are accessible here.

Under the existing guidelines, the maximum total contribution is $40,000. This means a FHSA account holder can contribute up to $8000/year for 5 years.

Suppose we help a young adult by making $8000 annual contributions for 5 years. At the end of 5 years, we make no further contributions. The value of the FHSA investments, however, continue to grow for another 10 years at 6% annually.

The following reflects the value of the investments in the FHSA using $8000 annual contributions in each of the first 5 years.

The FHSA remains open for another 10 years.

At the end of 15 years, the value of the holdings in the FHSA should be ~$105,000. If a young couple contribute a similar amount to their respective FHSA, they could potentially have ~$210,000 to purchase their first home.

Registered Retirement Savings Plan (RRSP)

A Registered Retirement Savings Plan (RRSP) is a retirement savings plan that you establish, that the CRA registers, and to which you or your spouse or common-law partner contribute. Deductible RRSP contributions can be used to reduce your tax.

Any income you earn in the RRSP is usually exempt from tax as long as the funds remain in the plan. You generally, however, pay tax when you receive payments from the plan.

In theory, RRSPs are a wonderful method to invest for your retirement years. In practicality, however, RRSPs can be a tax nightmare if not used wisely.

Imagine making annual RRSP contributions for decades for which you receive an annual tax deduction. The investments within the RRSP grow tax free. Eventually, however, RRSP withdrawals will have tax implications.

In most cases, RRSP account holders end up transferring the RRSP assets to a Registered Retirement Income Fund (RRIF).

Without proper tax planning, the annual RRIF withdrawals can place the account holder in the highest income tax bracket.

Given the tax implications associated with registered accounts, it is important to engage the services of professionals who can provide guidance regarding tax planning strategies.

In many cases, a RRSP meltdown strategy may be advisable. Depending on your circumstances, this meltdown may need to commence several years before the mandatory date by which RRSP assets must be transferred to a RRIF. If you have a sizable RRSP, you may need to commence your RRSP meltdown strategy several years before establishing a RRIF!

Having said this, it is far better to have saved too much in a RRSP versus not enough. It is, therefore, recommended that young adults take advantage of what the Canadian government has to offer.

The annual RRSP contribution limit is based on the maximum annual RRSP contribution room set by the Canadian government, the earned income you had during the previous tax year, and any unused contribution room from previous years.

The maximum contribution in 2025 is $32,490. Young adults typically do not have sufficient income and/or disposable income to meet the maximum annual contribution levels.

Suppose a young adult, however, is eligible to contribute $18,000 to a RRSP for the 2025 tax year. Furthermore, this young adult may have been unable to maximize their annual RRSP contributions in prior years. They may, for example, have $25,000 in contribution room carried over from prior years.

It might be unrealistic for a young adult to come up with a $43,000 ($18,000 + $25,000) RRSP contribution in 2025. Depending on your circumstances, however, you could lend/gift $43,000 to this young adult.

If this young adult invests $43,000 in their RRSP for 30 years, makes no additional annual RRSP contributions, and the investments in the RRSP generate a 6% annual rate of return, the value of the RRSP will be ~$247,000 in year 30.

If we modify the input data to include $5,000/year RRSP contributions for 30 years, the value of the RRSP should be ~$666,000. Once again, I prefer that the young adult make the annual contribution so they ‘have skin in the game’.

Taxable Account

The use of tax efficient accounts is wise. I, however, recommend young adults also hold taxable accounts. Taxable accounts offer greater flexibility and are not subject to the same restrictions imposed by the Canadian federal government on tax efficient accounts.

Young adults have time on their side and if used wisely, the value of investments held in taxable accounts can grow exponentially over decades. A young adult could hold shares in great companies with significant growth potential that appreciate considerably in value over time. The values of the investments grow tax free until such time as the investments are sold and a tax obligation on the capital gain is triggered.

Once again, a young adult may not be able to come up with the initial investment. This is when proper tax planning may lead to gifting/lending the young adult a significant sum to invest in a taxable account.

In this example, $100,000 is gifted/loaned to the young adult which is then invested in high quality growth companies for 40 years. Each year, an additional $5000 is contribution is made to this account. The expectation is that the value of the investments will grow by 6% annually. Furthermore, the annual fees are kept to a minimum. Using these parameters, this young adult could have just under $1.85 million in the investment account at the end of 40 years.

If we change the investment time frame to 50 years, the value of the investment portfolio jumps to just under $3.4 million!

Super Charge The Taxable Account

Before proceeding further, it is important to understand that employing debt to increase the potential return on investment has advantages/disadvantages. Leverage can amplify gains and can magnify losses. Borrowing to invest, therefore, is ill-suited for some investors.

Here are some of the advantages and disadvantages of employing leverage to invest in equities.

Leverage Advantages:

- Increased Buying Power: Leverage allows you to control a larger position than your available capital would otherwise permit. This means you can potentially profit from price movements on a larger scale.

- Amplified Returns: If your investments perform well, the percentage return on your initial capital can be significantly higher because you are working with a larger base. The returns on the borrowed funds enhance your overall gains.

- Access to More Opportunities: With increased capital, you might be able to access investment opportunities that would typically be out of reach due to higher initial costs.

- Potential for Quick Gains: In volatile markets, leveraged positions can generate substantial profits in a short period if the market moves in your favor.

- Capital Efficiency: Leverage can free up your capital for other investment opportunities, allowing for better diversification.

Leverage Disadvantages:

- Amplified Losses: Leverage can magnify losses if the value of your investments moves against your position – you could lose a significant portion or even more than your initial investment.

- Interest Costs: Borrowed funds usually come with interest charges which erode returns. If the investments do not perform well, these costs exacerbate your losses.

- Margin Calls: If the value of your leveraged investments falls below a certain level (the maintenance margin), you risk a margin call. This means you must quickly cover the margin shortfall or risk your investments being liquidated at a loss.

- Increased Risk of Ruin: Combining leverage with illiquid or concentrated positions can be particularly dangerous and lead to substantial financial losses.

- Limited Flexibility: High leverage can potentially restrict your ability to take on new investments or secure financing for other significant purchases.

- Market Volatility: Leveraged positions are more sensitive to market fluctuations. Even small adverse price movements can result in significant losses.

- Emotional Stress: Managing leveraged positions, especially in volatile markets, can be stressful and may lead to impulsive decision-making.

Charlie Munger was vice chairman of Berkshire Hathaway, the conglomerate controlled by Warren Buffett from 1978 until his death in 2023. His advice was to always invert. This is a mental model giving consideration to great outcomes AND terrible outcomes from investment decisions.

In my recent Wealth-Destroying Mistakes to Avoid post, I touch upon people borrowing for things that destroy wealth (eg. degrees for which student loan payments are required for several years, credit card debt, payday loans, vehicle financing, etc.). Under no uncertain terms am I suggesting debt be used for wealth destruction purposes.

In their Lifecycle Investing: A New, Safe, and Audacious Way to Improve the Performance of Your Retirement Portfolio published in 2010, authors Barry Nalebuff and Ian Ayres, two of the most innovative thinkers in business, law, and economics explain why building a well diversified portfolio and then increasing expected returns with the use of leverage actually leads to a better expected outcome than increasing concentration in risky assets.

Being ‘Real’ With Your Risk Tolerance

On a scale of 1 – 100, one investor might define their risk tolerance at a particular level. Another investor might define their risk tolerance equally. In reality, however, the second investor could be far less or far more risk tolerant the first investor. Risk tolerance, therefore, is somewhat ambiguous.

In early April 2025, we experienced a brief market implosion. I know investors who thought their risk tolerance was high who ended up liquidating a sizable component of their investment portfolio out of fear.

If you intend to employ leverage, you must be able to withstand significant market pullbacks. There is nothing wrong with a plunge in the value of your investments. You must, however, be able to ‘weather the storm’. If you are unable to do so, you run the risk of breaking Warren Buffett’s and Charlie Munger’s two rules of investing which are:

- Rule #1: Do not lose money.

- Rule #2: Do not forget rule #1.

Margin Calls

If the young adult employs leverage, they can:

- borrow against the value of their investment holdings; or

- establish credit arrangements that are separate and distinct from their investment accounts.

Naturally, they need to qualify for credit.

A risk of borrowing against the value of the investment holdings is a potential ‘margin call’.

A margin call occurs when the value of an investor’s margin account drops below the broker’s required maintenance margin. This situation typically arises when the securities held in the account decrease in value, leading to a decline in the investor’s equity. The broker issues a margin call to ensure there are sufficient funds to cover potential losses on trades made with borrowed money.

When employing the use of leverage through a margin account, investors must closely monitor it. This is essential to ensure sufficient equity above the maintenance margin requirement is maintained. This may require the retention of extra cash in the account.

At the very least, investors employing leverage should have readily accessible liquidity. This is because there is a very short ‘window’ in which to restore a margin account to a position where the risk of equities being sold without the account holder’s consent at the most inopportune time is eliminated.

It is important to note that brokers can alter the margin values assigned to specific equity investments. Some holdings may be assigned 70% margin while 50% margin or no margin may be assigned to other holdings. If a company’s financial position deteriorates, the broker may decide to lower the amount it is prepared to lend against the company’s security.

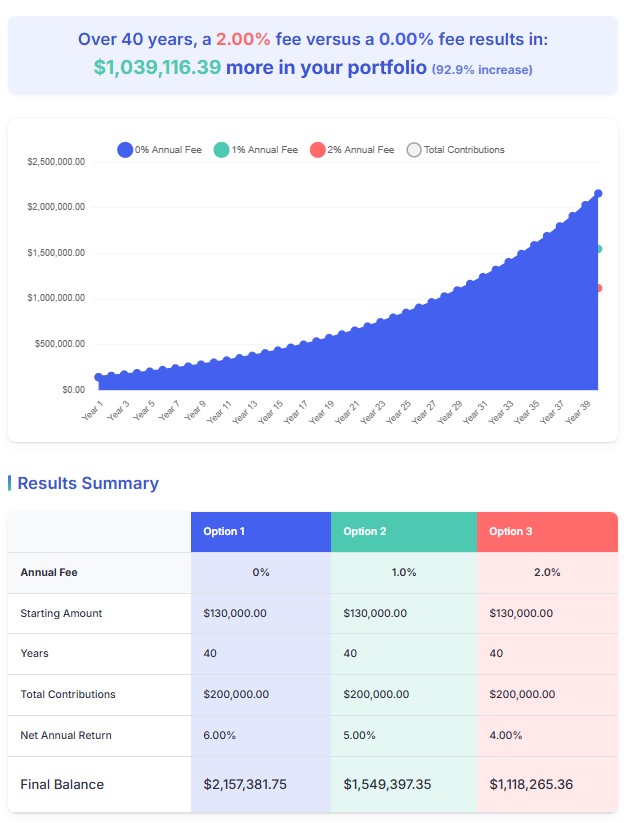

If the young adult plans to employ the use of leverage and qualifies for a margin account, the recommendation is to restrict the use of debt. To limit the potential for a margin call, a plan might be to borrow a maximum of $30,000 on a $100,000 portfolio of high quality stocks.

By increasing the amount invested to $130,000, we see the extent to which the portfolio appreciates in value leaving the other metrics constant. This scenario continues with the assumption of a $5000 annual contribution at the beginning of every year.

If we change the investment time frame to 50 years, the value of the investment portfolio jumps to just over $3.9 million!

Tax Deductible Interest

The Canada Revenue Agency (CRA) clearly outlines the terms and conditions under which interest is tax deductible. Their conditions must be met otherwise the CRA will deny this tax deduction. If the conditions for the deductibility of investment loan interest are satisfied, the young adult can deduct this expense on their personal tax return.

Another consideration is the cost of borrowing and the investments’ expected rate of return. Borrowing at 6%, for example, might make sense if the projected long-term total investment returns are likely to exceed 6%. Borrowing at 10% with the expectation for a 6% long-term total investment return, however, appears unwise.

Ownership/Control Of Assets

It may be prudent to engage the services of tax and legal professionals to limit potential problems that could arise.

If you decide to loan/gift money to the young adult, you may want to make it a condition that you can monitor all investment accounts. This may not be necessary if the amount in question is negligible but certainly seems justified if the amount is significant.

Time Is A Young Adult’s Ally

It is entirely possible that a young adult could lose their entire investment. Limiting their investments to very high quality companies that are likely to be far more valuable in the future, however, reduces the probability of this happening. I do not recommend highly speculative investments to a young adult. They do not need to ‘hit home runs’ within a short time frame. Time is their ally. The longer they maintain exposure to stocks, the more reliable the potential outcome.

Powers of Attorney (Health and Finances) and Wills

As noted at the outset of this post, seek legal and financial advice from professionals who understand your specific circumstances.

Although we expect young adults to outlive us, such is not always the case.

The time to start thinking about loan and/or gift recovery is not when the young adult accumulates a sizable investment portfolio and becomes incapacitated or passes away. It is, therefore, recommended that the appropriate legal documentation be in place before advancing money.

Final Thoughts

With a typically moderate level of income and the rising cost of living, some young adults may need financial assistance. Depending on your circumstances, you may wish to consider helping your children financially while you are able to witness the benefits of your financial assistance.

Using my metrics, it is not out of the realm of possibility that one young adult could have a mid-6 figure (at the very least) investment portfolio by the age of 30. As noted at the outset of this post, however, everyone’s circumstances differ. A family with 4 young adults may find it difficult to use the figures I have used in my calculations. It is, therefore, essential to use data based on your circumstances.

Furthermore, do not give all your assets to your children if this will lead you to becoming destitute.

Family dynamics also come into play, and therefore, engaging the services of legal and financial professionals is wise.

As noted at the outset of this post, I am a Canadian resident. The tax advantaged accounts reflected in this post are, therefore, irrelevant if you reside elsewhere. Your country of residence, however, may have tax advantaged accounts. If so, you may wish to explore the use of such accounts.

The use of leverage can increase the value of an investment portfolio. The wise use of leverage can enhance investment returns. It, however, increases exposure to potential losses and should only be considered by experienced investors with a high-risk tolerance and a solid risk management strategy. Employing the use of leverage, therefore, is not a blanket recommendation.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.