In my February 8, 2024 and May 2 2024 Paycom (PAYC) posts, I noted that shares were considerably undervalued and disclosed additional share purchases. When I last reviewed PAYC in my November 4, 2024 post following the release of Q3 and YTD2024 results, I felt shares were almost fairly valued.

With the surge in PAYC’s share price the day following the May 7, 2025 release of Q1 2025 results and FY2025 outlook, PAYC is now overvalued.

Business Overview

I provide a brief business overview in prior posts. The best sources of information to learn about the company, however, are PAYC’s website and the FY2024 Annual Report/Form 10-K.

Financials

Q1 2025 Results

Details of PAYC’s Q1 2025 results are accessible here. The Q1 Form 10-Q is currently unavailable as I compose this post but will be accessible here upon release.

In FY2022 – FY2024, PAYC’s research and development (R&D) expenses amounted to $0.1483B, $0.199B, and $0.2426B. In Q1 2025, the R&D expense was $62.3 million.

An example of the effectiveness of PAYC’s R&D investments is GONE, the company’s industry leading automated solutions launched in December 2023. This is a fully automated time-off solution that decisions all time-off requests based on customizable guidelines set by the company’s time-off rules. Before GONE, 10% of an organization’s labor cost went substantially unmanaged. This led to scheduling errors, increased cost from overpayments, staffing shortages, and employee uncertainty over pending time-off requests.

A Forrester Consulting study conducted in 2024 reveals that GONE’s automation can potentially deliver a return on investment of up to 821% over three years.

On the Q1 2025 earnings call, management states:

Our award-winning payroll solution continues to be a major selling point. Organizations looking to reduce the labor needed to process payroll by up to 90% and also cut the time spent correcting payroll errors by up to 85%.

Beti allows clients to focus resources on profit-driving initiatives as it eliminates human involvement in non-revenue-generating tasks like post payroll adjustments, check reversals, voids, ledger corrections and more.

Thanks to Beti and the importance of perfect payrolls, we are also successfully getting former clients back onto the Paycom platform. We recently brought back a 500-employee health care company, who quickly realized the pain they brought on themselves by switching to another provider.

With this other provider, this client lost the transparency and ability to fix errors before they became problems.

In fact, their employees were some of the biggest advocates and encouraged this client to return to Paycom because they missed having control over the accuracy of their pay.

Once employees experience Beti, they don’t want to go backwards in technology. The client returned to us within 9 months and went from processing payroll in 4 days with their previous vendor to 4 hours with Beti.

Sales continues to break records, including the first quarter, where we saw a meaningful increase in book sales.

We also saw an increase in the number of units sold for the quarter as compared to the same period last year.

One of the new clients we onboarded was a 2,500-employee restaurant group who wanted a single easy-to-use software solution. Working across nearly 80 locations, this group is now utilizing Beti and the rest of the Paycom suite to automate tasks that were previously performed across numerous systems, which created data inconsistencies.

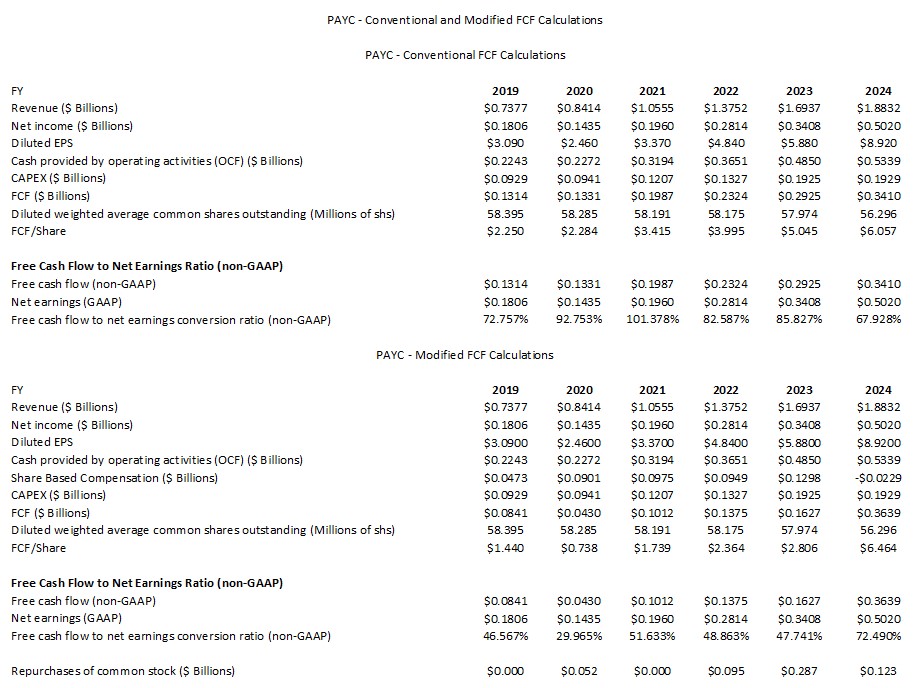

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

PAYC deducts CAPEX from its net cash provided by continuing operating activities to determine its FCF. I address my rationale for also deducting share based compensation (SBC) when determining FCF in my How Stock Based Compensation Distorts Free Cash Flow post.

NOTE: In my November 4, 2024 post I explain why FY2024 SBC is negative.

PAYC’s FCF to net earnings ratio is less than impressive. We, however, need to look more closely at the numbers.

At FYE2019, PAYC had ~$31 million of long-term debt and the current portion of its long-term debt was ~$2 million. At FYE2024 there was no debt.

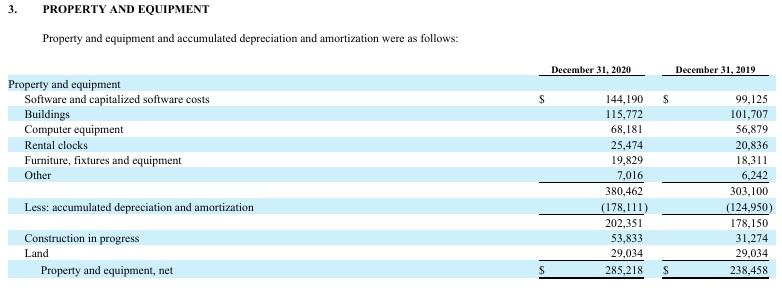

Fixed assets have grown from FYE2019 to FYE2024 (see tables below) with PAYC having spent ~$0.8258B on CAPEX. All this CAPEX has been fully funded using cash generated from normal business operations.

Cumulative FCF in FYE2019 to FYE2024 totals ~$1.3291B and ~$0.8924B calculated under the conventional and modified methods. If PAYC had borrowed, for example, ~30% – ~45% of its ~$0.8258B CAPEX, FCF during this 6 year period would be ~$0.25B – ~$0.372B higher thus improving FCF.

At the end of Q1 2025, net property and equipment had increased to ~$0.5671B and PAYC still had no debt.

FY2025 Outlook

PAYC’s FY2025 outlook is:

- Total revenue of $2.023B – $2.038B, representing YoY growth of ~8% at the midpoint.

- Recurring and other revenue growth of ~9% YoY. Management expects the highest growth to occur in Q4.

- Interest on funds held for clients of ~$0.110B.

- Adjusted EBITDA of $0.843B – $0.858B, representing a margin of ~42% at the midpoint.

- Full year GAAP and non-GAAP tax rates of 28% and 27%, respectively.

- Stock compensation of ~8% of revenues.

PAYC’s prior FY2025 outlook released on February 12, 2025 was:

- Total revenue of $2.015B – $2.035B, representing YoY growth of ~8% at the midpoint.

- Recurring and other revenue growth of ~9% YoY.

- Interest on funds held for clients of ~$0.110B.

- Adjusted EBITDA of $0.820B – $0.840B, representing a margin of ~41% at the midpoint.

Risk Assessment

PAYC has no debt.

At FYE2024, it had ~$0.402B of cash and cash equivalents. Current liabilities before client funds obligation (excluding deferred revenue of ~$30 million) was ~$0.2111B. The difference is $0.1909B.

At the end of Q1, PAYC had ~$0.5208B in cash and cash equivalents. Current liabilities before client funds obligation (excluding deferred revenue of ~$30.2 million) was ~$0.2123B. The difference is $0.3085B.

This is a $0.1176B improvement in just 1 quarter!

PAYC does not need to rely on external financing. It benefits from the receipt of funds from clients in advance of providing services (short-term and long-term deferred revenue).

Dividends and Share Repurchases

Dividend and Dividend Yield

PAYC has a brief dividend history having distributed its first quarterly dividend on June 12, 2023.

On May 5, PAYC announced that its Board declared a $0.375/share cash dividend to be paid on June 9, 2025 to all stockholders of record as of the close of business on May 27, 2025.

Dividend metrics are of little relevance in my investment decision making process. I would much rather a company retain funds to grow the business if this is the most efficient form of capital allocation.

Share Repurchases

The weighted average diluted shares outstanding in FY2019 – FY2024 is reflected in the table found within the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post.

Pursuant to a stock repurchase plan announced on November 20, 2018, PAYC was authorized to purchase (in the aggregate) up to $0.150B of its common stock in open market purchases,

privately negotiated transactions or by other means.

- On May 13, 2021, PAYC announced that its Board increased the availability under the existing stock repurchase plan to $0.3B and extended the expiration date to May 13, 2023.

- On June 7, 2022, PAYC announced that its Board increased the availability under the existing stock repurchase plan to $0.55B and extended the expiration date to June 7, 2024.

- On August 15, 2022, PAYC announced that its Board increased the availability under the existing stock repurchase plan to $1.1B and extended the expiration date to August 15, 2024.

- On July 31, 2024, PAYC announced that its Board increased the availability under the existing stock repurchase plan to $1.5B and extended the expiration date to August 15, 2026.

In Q1 2025, repurchased 24,987 shares of common stock for $5.2 million. The weighted average diluted shares outstanding in the quarter was 56.3 million.

At the end of Q1, PAYC had $1.47B remaining under its existing stock repurchase plan.

Valuation

PAYC’s valuation at the time of my previous two posts are in my November 4, 2024 post.

Following the release of Q1 2025 earnings, PAYC’s share price has surged and is ~$246.60 as I compose this post on May 8. Broker estimates are currently under revision with several estimates already having been raised considerably. The current forward-adjusted diluted EPS broker estimates and forward adjusted diluted PE levels are:

- FY2025 – 18 brokers – ~27.9 using the mean of $8.85 and low/high of $8.51 – $9.16.

- FY2026 – 17 brokers – ~25 using the mean of $9.88 and low/high of $9.34 – $10.62.

- FY2027 – 6 brokers – ~22.2 using the mean of $11.12 and low/high of $10.80 – $11.45.

In Q1 alone, PAYC generated ~$144.8 million and ~$122.6 million of FCF calculated using the conventional and modified calculation methods. I estimate that PAYC will generate ~$550 million and ~$490 million of FCF in FY2025 using the conventional and modified calculation methods.

The diluted weighted average shares outstanding in Q1 was 56.3 million. I anticipate the diluted weighted average shares outstanding in FY2025 will be ~56.2 million.

My expectation is for PAYC to generate ~$9.80 and ~$8.72 of FCF/share in FY2025 using ~$550 million and ~$490 million of FCF for FY2025 using the conventional and modified calculation methods ($0.55B/56.2 million and $0.49B/56.2 million).

With shares currently trading at ~$246.60, my forward P/FCF estimates are ~25.2 and ~28.3.

Final Thoughts

My most recent PAYC share purchases are:

- 100 shares on February 8, 2024 @ $192.8999

- 50 shares on February 9, 2024 @ $188.60

- 100 shares on March 4, 2024 @ $178.185

- 100 shares on May 2, 2024 @ $163.03

bringing my total exposure to 700 shares in a ‘Core’ account within the FFJ Portfolio.

When I completed my 2024 year-end review, PAYC was my 23rd largest holding. I do not know its current ranking. It is likely still a top 30 holding.

I like PAYC’s long-term prospects and want to increase my exposure. The time to acquire shares in great companies, however, is when they experience temporary challenges and the investment community sours on the company.

What were once undervalued shares are now overvalued. The ~$15/share or ~6.73% surge in PAYC’s share price the day following the earnings release is an indication that PAYC has regained investor confidence. This, in my opinion, is not the time to add to my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long PAYC.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.