A strong case for investing in BlackRock (BLK) can be made when markets implode. It is the world’s largest asset manager with over $11.5 TRILLION of Assets Under Management (AUM).

In prior Brookfield (BN.to), Blackstone (BX), and BlackRock (BLK) posts, I stated that the asset management industry is saturated and that a ‘shake-out’ is imminent. Many smaller asset managers have struggled of late for a variety of reasons (eg. unable to exit investments as originally intended, poor results, and inability to raise ‘new’ money).

Brookfield Corporation (BN.to) predicted in May 2023 that the challenging economic environment will force asset managers to consolidate to ‘up to 10 leading industry players’. A similar trend is playing out in wealth management.

In 2023, PwC surveyed 500 asset managers and institutional investors. The survey findings suggested that the asset management industry would consolidate dramatically in the next few years with ~1 in 6 likely to disappear because of a combination of market volatility, high interest rates, and cost/margin pressures. Several firms will likely fail or be bought up by bigger groups by 2027. Given the current market turmoil, I anticipate that more than ~1 in 6 will fail and that we will not need to wait until 2027 to witness an industry implosion.

In my January 18, 2025 post I concluded that BLK shares were overvalued; shares were trading at ~$1,006. I followed up that post with my February 15 post in which I disclosed the purchase of 20 shares @ $972.56 in a ‘Core’ account within the FFJ Portfolio bringing my exposure to 180 shares.

When I composed my February 15 post, I wrote that BLK was ‘not on sale’. I envisioned, however, that the Global Infrastructure Partners (‘GIP’), HPS Investment Partners (‘HPS’), and Preqin (‘PRQ’) acquisitions would greatly expand BLK’s ability to significantly increase future earnings. I stated America’s wealthiest financiers are in business to make money and we should ‘follow the money’.

Fast forward to April 12, 2025. The turmoil in the financial markets reinforces the importance of mastering our mindset.

In my recent The Real Art Of Investing post, I touch upon the need to tune out the noise. Unless we do so, compounding can be difficult. Although the impact time has on our long-term investment results resonates with many investors, not everyone will have the wherewithal to withstand the turmoil we are likely to continue to experience in the foreseeable future.

I envision marital breakdowns and suicide levels will surge. Even before the current market turmoil kicked in, many people were in a ‘world of hurt’.

- Credit card delinquency is increasing;

- Car repossessions and mortgage delinquencies are increasing;

- An increasing number of tenants are unable to meet their obligations. This, in turn, places a strain on real estate investors who rely on rental income; and

- Small businesses relying on imported products for subsequent resale will likely implode.

This, however, is not an all encompassing list of the likely impact of elevated tariffs.

Many businesses will undoubtedly need to reduce costs. This often leads to ‘right-sizing’ headcount. A rise in unemployment levels will have a ripple effect on the economies of several countries.

Given my outlook, I have limited recent purchases to the following:

- Brookfield Corporation (BN.to);

- Blackstone (BX);

- HEICO Corporation (HEI-a);

- Mastercard (MA); and

- S&P Global (SPGI)

In addition, I have acquired a few additional shares in other companies by way of the automatic reinvestment of dividend income.

I have several companies ‘on my radar’. BLK, however, is ‘front and center’.

With the release of Q1 2025 results on April 11, 2025, this is an opportune time to revisit this existing holding.

Overview

A comprehensive overview of BLK is found in Part 1 Item 1 in BLK’s FY2024 Form 10-K which is accessible through the SEC Filings section of the company’s website. I also strongly recommend reviewing the company’s website.

On April 7, Larry Fink (BLK’s Co-Founder, Chairman and CEO) spoke at the New York Economic Club at which time he stated that the US is very close to a recession (if not already in one). Despite this and the heightened level of uncertainty, he stressed the importance of facing uncertainty head on and trying to find solutions. Because BLK’s clients are facing a greater degree of uncertainty, BLK is spending more time conversing with clients in an effort to help, calm, and provide ideas.

The level of uncertainty creates an element of difficulty in terms of capital allocation. CAPEX at many companies, therefore, may be ‘dialed back’. The megatrends (AI, data centers, infrastructure and the reorientation of the US economy), however, are still intact. What may change is the execution of some of these trends with major projects being pushed out further into the future.

Financials

Q1 2025 Results

BLK’s quarterly financial results dating back to 2009 are accessible here.

In the April 11, 2025 Q1 2025 Earnings release, Mr. Fink states:

BlackRock is a global firm, but one that operates hyper-locally. Our nearly 23,000 employees work across over 30 countries to serve clients in more than 100. Today, we’re better prepared than ever to advise and deliver on each of our clients’ unique tactical and strategic objectives. The goal for us is to keep our clients focused on the long-term, and help them achieve any near-term allocation or liquidity changes they need within the BlackRock platform.

Uncertainty and anxiety about the future of markets and the economy are dominating client conversations. We’ve seen periods like this before when there were large, structural shifts in policy and markets – like the financial crisis, COVID, and surging inflation in 2022. We always stayed connected with clients, and some of BlackRock’s biggest leaps in growth followed.

We’ve intentionally shaped our platform to serve clients in all market environments, building a premier global public-private markets investment and technology firm. We have leading franchises in categories that we expect to benefit from capital flows and investment even against volatile public markets. These include our newly enriched private markets platform, ETFs, and Aladdin risk management and technology.

Capital Allocation

BLK’s capital allocation priorities are to:

- invest in the business to either scale strategic growth initiatives or drive operational efficiency;

- return excess cash to shareholders through a combination of dividends and share repurchases; and

- make inorganic investments where there is an opportunity to accelerate growth and support strategic initiatives.

Despite the current uncertain global business environment, BLK allocates its capital to maximize total long-term shareholder returns. I do not, therefore, anticipate management will change its capital allocation priorities.

FY2025 Outlook

BLK does not provide an outlook for the entire fiscal year. It does, however, state that it will either:

- continue to prioritize investments with differentiated organic growth potential; or

- that will expand operating leverage through enhanced scale.

Risk Assessment

Risk mitigation is an integral component of my investment strategy. Having said this, my risk tolerance may be greater/lesser than your risk tolerance. I, therefore, encourage you to consider this when making your investment decisions.

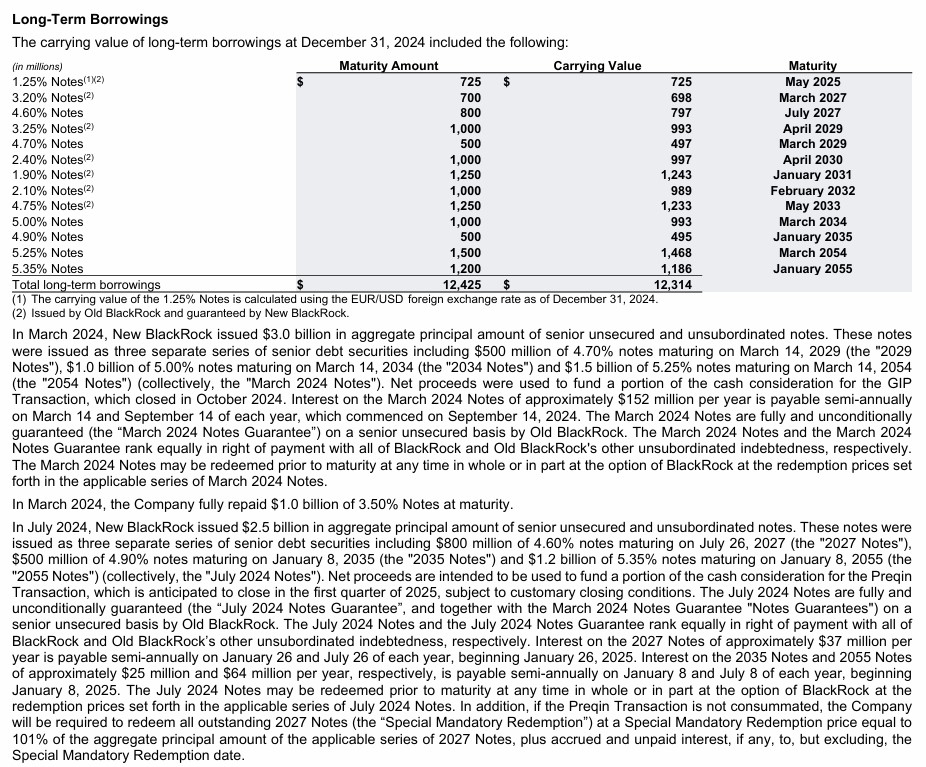

BLK’s 2024 Q1 2025 From 10-Q is currently unavailable, and therefore, I provide the following note from BLK’s FY2024 Form 10-K.

The credit rating agencies don’t always ‘get it right’ when assessing a company’s risk. I, however, consider the domestic senior unsecured credit ratings they assign. I then take into account that as an equity investor, my risk is higher than that of unsecured debt.

There are 6 credit rating tiers between BLK’s domestic senior unsecured credit ratings and the top tier of the ‘junk ratings’.

A deterioration in the global economic conditions is very likely. Even if the rating agencies lower BLK’s domestic senior unsecured credit ratings, I do not expect they will ever reach ‘junk levels’.

Since June 2018, Moody’s rates BLK’s domestic senior unsecured credit Aa3; this rating was affirmed in December 2024. The outlook is stable.

Since May 2014, S&P Global rates BLK’s domestic senior unsecured credit rating AA-; this rating was affirmed in June 2024. The outlook is stable.

Both ratings are the bottom tier in the high-grade investment-grade category. These ratings define BLK as having a very strong capacity to meet its financial commitments. The ratings differ from the highest-rated obligors only to a small degree.

Dividends and Share Repurchases

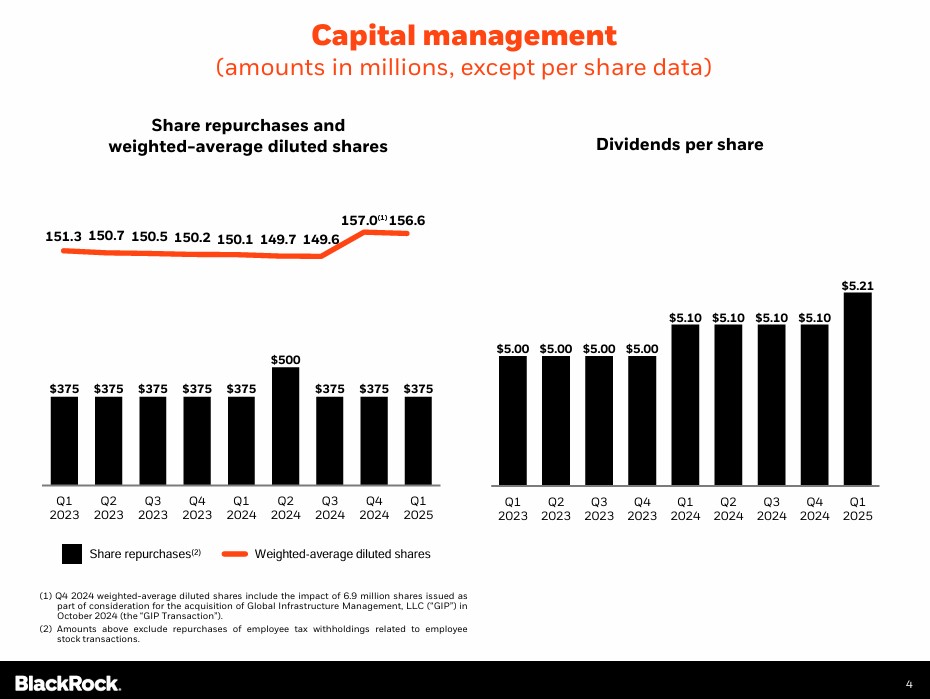

The following reflects the share repurchase and dividend distribution components of BLK’s quarterly capital allocation for the past 2 fiscal years.

Although BLK repurchases shares as part of its capital allocation strategy, the weighted-average diluted shares outstanding surged in Q4 2024. This is because the total consideration for the GIP acquisition consisted of $3B in cash and ~12 million shares of BLK common stock.

Dividend and Dividend Yield

BLK initiated a quarterly dividend in 2003 (see dividend history).

I anticipate that the majority of the total return from a BLK investment will continue to come from capital appreciation; the dividend component is likely to remain relatively insignificant.

Share Repurchases

BLK’s capital allocation priority is to invest either to scale strategic growth initiatives or drive operational efficiency. After these priorities, BLK returns excess cash to its shareholders through a combination of dividends and share repurchases.

Share repurchases have been a consistent element of BLK’s capital management strategy. In Q1 2025, it repurchased ~$0.375B of common shares. BLK still anticipates it will repurchase $0.375B of shares quarterly for the remainder of FY2025; this is consistent with its January 2025 guidance.

Valuation

In my recent Why I Do Not Perform Discounted Cash Flow Analyses post I explain why I deem this exercise to be a waste of time. The process might look impressive. The results, however, can be vastly different depending on the input data. How can input data going out 2+ years on the calendar be remotely reliable? DCF calculations performed in late 2024/early 2025, for example, are now likely irrelevant.

When I wrote my February 15, 2025 post, BLK’s share price was ~$974. Using current broker forward adjusted diluted EPS estimates, the forward adjusted diluted PE levels were:

- FY2025 – 15 brokers – mean of $47.46 and low/high of $46.08 – $50.17. Using the mean estimate: ~20.5.

- FY2026 – 14 brokers – mean of $54.05 and low/high of $51.25 – $59.28. Using the mean estimate: ~18.

- FY2027 – 7 brokers – mean of $61.59 and low/high of $55.52 – $67.40. Using the mean estimate: ~15.8.

I concluded that BLK was not currently be ‘on sale’. With the GIP, HPS, and PRQ acquisitions greatly expanding BLK’s ability to significantly increase future earnings, however, I acquired a few additional shares.

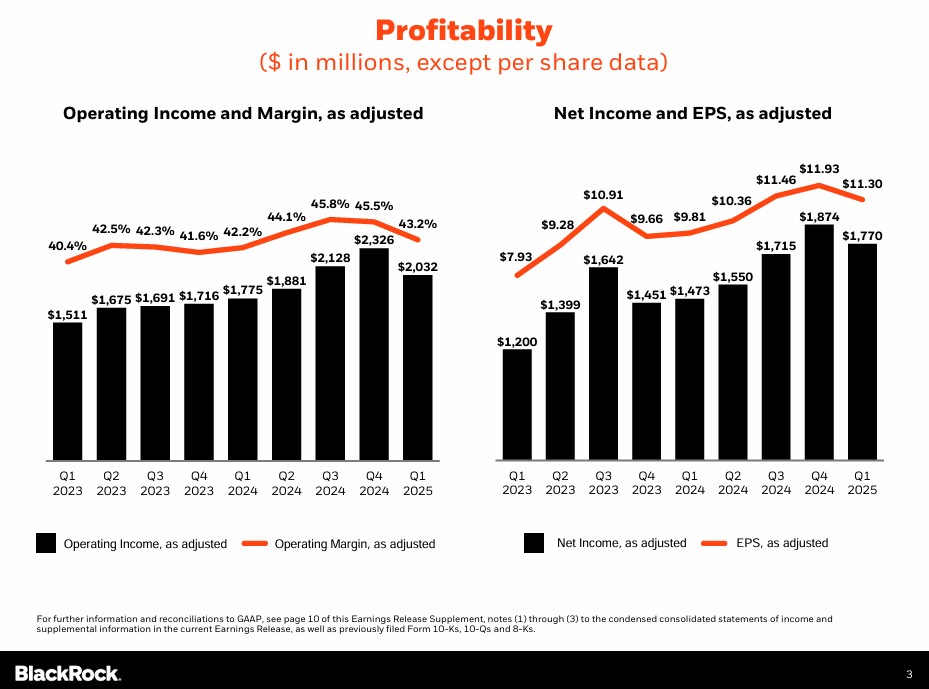

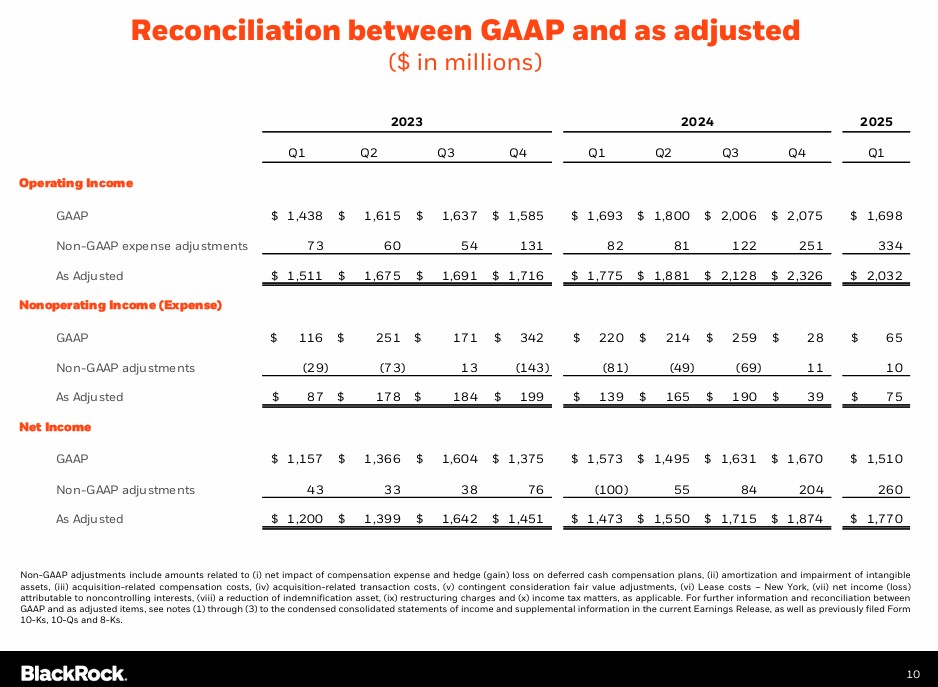

In Q1 2025, BLK generated $9.64 and $11.30 of diluted EPS and adjusted diluted EPS.

With shares currently trading at ~$879 as I compose this post, the following are the forward adjusted diluted PE levels using current broker estimates:

- FY2025 – 15 brokers – mean of $45.10 and low/high of $42.84 – $47.32. Using the mean estimate: ~19.5.

- FY2026 – 15 brokers – mean of $51.08 and low/high of $47.03 – $54.26. Using the mean estimate: ~17.2.

- FY2027 – 8 brokers – mean of $57.67 and low/high of $54.19 – $61.89. Using the mean estimate: ~15.2.

Within the past week, BLK’s share price briefly slipped below $800. At this share price and using the FY2025 mean of $45.10, the forward adjusted diluted PE is ~17.7. This gives us an indication of just how quickly BLK’s valuation can change.

BLK’s Q1 earnings were just released, however, and several brokers are likely revisiting their earnings estimates. Given current market conditions, I expect lower earnings estimates than those reflected above.

The extent to which the earnings estimates have been lowered subsequent to my February 15, 2025 post and the variance in the brokers’ earnings estimates implies there are multiple opinions as to how BLK is likely to perform in the short-term. Looking at BLK from a long-term investment perspective, however, I think it is strategically positioned to become far more valuable.

Final Thoughts

On March 9, 2023, I initiated a BLK position in a ‘Core’ account within the FFJ Portfolio at ~$664/share. I added to my exposure in April and May 2023 @ ~$656 and ~$635 and again in April 2024 @ ~$770. I failed to exhibit sufficient discipline and ‘paid up’ to acquire 20 shares @ $972.56 in February 2025 which raised my average cost to ~$706.98.

When I completed my 2024 Mid Year FFJ Portfolio Review, BLK was my 21st largest holding. At the time of my 2024 Year End FFJ Portfolio Review, however, it was my 18th largest holding.

In prior posts, I suggest we ‘follow the money’.

Given BLK’s scale and competitive advantages, I am of the opinion that it is one of the asset managers to which we should have exposure if we want exposure to the highly fragmented asset management industry that is undergoing industry consolidation.

Not many asset managers have the wherewithal to compete with BLK. The sheer magnitude of some of its transactions rules out a huge percentage of asset managers!

In March 2025, for example, the BLK-led consortium that includes Mediterranean Shipping Company, one of the world’s leaders in shipping and logistics and Terminal Investment Limited, one of the world’s largest global container terminal operators, announced a massive infrastructure investment with an agreement in principle to acquire a portfolio of 43 ports in more than 20 countries from CK Hutchinson Holdings; the proposed acquisition includes two Panama ports.

While someone in Washington has touted BLK’s acquisition of the Panama Canal, this may have been premature. Panama’s top auditor has accused the operator of wrongdoings and owing millions in dues. This component of the acquisition, therefore, has been thrown into doubt.

Even if the Panamanian component of the acquisition falls through, the consortium will have a portfolio of ~100 ports around the world!

I intend to increase my BLK exposure. Its share price behavior is volatile, however, with recent intra-day share price fluctuations exceeding ~$50/share. I am, therefore, waiting for the broad market to capitulate further at which time I intend to acquire shares. The young investors I am helping on their journey to financial freedom are also patiently waiting before acquiring BLK shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BLK.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.