Invest in a business any fool can run, because someday a fool will.

Charlie Munger and Warren Buffett – Berkshire Hathaway

Nike (NKE) is a good example of how poor leadership can harm even great companies!

When John Donahoe was appointed as NKE’s 4th CEO in January 2020, NKE called out his ‘expertise in digital commerce, technology, global strategy and leadership’ as the reason behind his appointment. At the time, NKE was leaning into its Consumer Direct Offense plan that it first announced in 2017. Donahoe’s ‘expertise’ was expected to support the firm’s digital transformation. Under his watch, NKE cut back on several wholesale relationships in favor of direct channels.

In essence, NKE selected a CEO with a complete lack of knowledge about sneakers and sneaker culture and no retail experience. He underestimated the importance of major retail partners in selling NKE products. As a former Bain management consultant with no industry experience, his go-to tactic was to cut costs. This, however, exacerbated NKE’s problems.

These missteps enabled NKE’s competitors to steal market share. Smaller brands such as Hoka, Brooks, and Saucony, for example, are more nimble and offer trendy designs at lower price points. This has permitted them to gain sales in the athletic sneaker industry after spending millions of dollars on branding deals with running clubs and community events.

Recognizing that urgent and drastic changes were required, Donahoe was punted to the curb within 4 years of becoming CEO. Effective October 14, 2024, Elliott Hill, rejoined NKE as its 5th CEO; this move was met with praise from employees and analysts.

Hill, a company veteran of 32 years, joined NKE in 1988 as an apparel sales representative intern. He held several leadership positions over 32 years before retiring from NKE in 2020 from his role as president of consumer and marketplace.

Shortly after his appointment as CEO, Hill commenced the process of reversing NKE’s efforts to cut back on several wholesale relationships in favor of direct channels.

The March 20, 2025 release of Q3 and YTD2025 results represents the first full quarter under Hill’s helm. While NKE has embarked on the path to recovery, the return to its ‘glory days’ is a monumental undertaking. A dramatic improvement in its results, therefore, will likely take several quarters.

The current business environment certainly complicates NKE’s turnaround. On the Q3 earnings call with analysts, management states the turmoil created by Vladimir Putin’s Employee of the Month is forcing NKE to:

navigate through several external factors that create uncertainty in the current operating environment, including geopolitical dynamics, new tariffs, volatile for rates and tax regulations as well as the impact of this uncertainty and other macro factors on consumer confidence.

NKE investors will need to be extremely patient!

I last reviewed NKE in this post following the release of FY2024 results. In my brief December 3, 2024 post, however, I disclose the purchase of additional shares. Now that we have NKE’s Q3 and YTD2025 results, this is a good time to revisit this existing holding.

Business Overview

The best resource from which to learn about NKE is Part 1 Item 1 – Business in the FY2024 Form 10-K. This section provides a general overview of the company, its products, and markets amongst other pertinent information. I also strongly encourage a review of Item 1A – Risk Factors in the Form 10-K.

Pershing Square’s Rationale For Investing In NKE

I never invest in a company just because highly successful investors invest in a company. It is, however, encouraging when they invest in companies to which I have exposure. Two examples are:

- Berkshire Hathaway investing in HEICO; and

- Pershing Square Holdings Ltd. (Bill Ackman) investing in NKE.

Both companies are existing holdings in the FFJ Portfolio and/or retirement accounts for which I do not disclose details.

Pershing’s reasoning for investing in NKE (see below) provides another investor’s rationale for a NKE investment. Sometimes investing in a great company when it falls out of favor can potentially lead to attractive long-term total investment returns.

The following, extracted from Pershing’s 2024 Annual Report, is accessible through the Materials section of Pershing’s website.

At the end of Q4 2024, Pershing Square held ~18.5 million NKE shares. As noted in the NKE commentary, Pershing converted its common equity position to deep in-the-money call options in early 2025. I understand the logic for Pershing’s decision but I am choosing to retain my shares. My total NKE exposure is less than 1300 shares and it has never been a top 30 holding. Pershing, on the other hand held ~18.5 million shares. If it purchased shares @ $75/share, for example, that amounts to ~$1.387B. This is far in excess of my exposure!!!

Financials

Q3 and YTD2025 Results

The Q3 and YTD2025 results are accessible here.

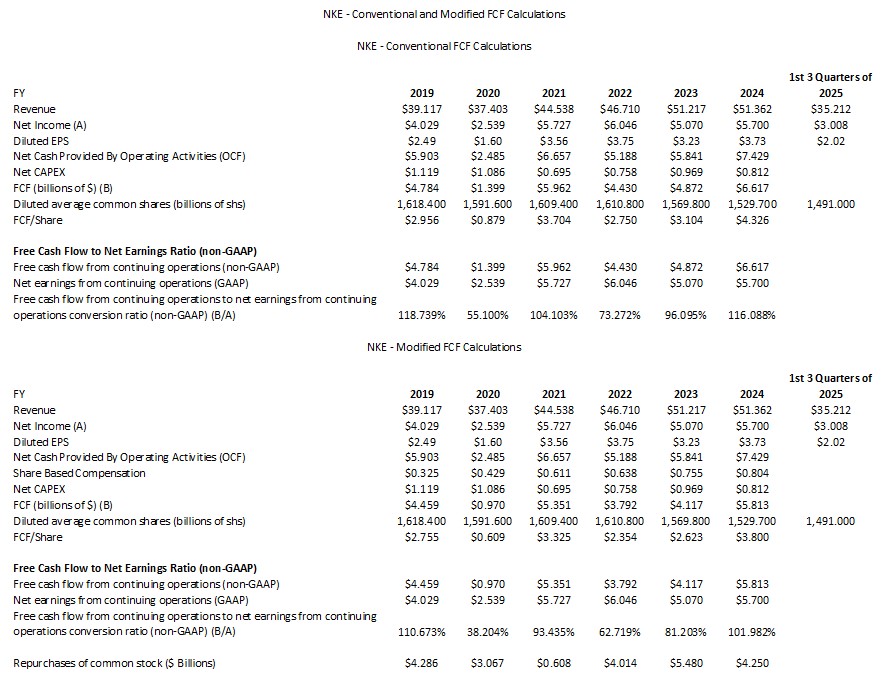

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

The following reflects NKE’s FCF using the conventional and modified methods. The modified method deducts share-based compensation (SBC) from a company’s OCF.

The results over the last few years reflect less than stellar FCF conversion.

The Form 10-Q for Q3 is currently unavailable and the March 20, 2025 earnings release reflects insufficient information to determine NKE’s YTD2025 FCF. This explains why some cells have not been populated with data.

Using the Q2 2025 Form 10-Q, we arrive at NKE’s conventional and modified FCF of $1.194B and $0.819B.

FY2025 Guidance

On the Q3 earnings call, management states:

We believe that the 4th quarter will reflect the largest impact from our Win Now actions and at the headwinds to revenue and gross margin will begin to moderate from there.

We are also navigating through several external factors that create uncertainty in the current operating environment, including geopolitical dynamics, new tariffs, volatile for rates and tax regulations as well as the impact of this uncertainty and other macro factors on consumer confidence. Our 4th quarter guidance includes our best assessment of these factors based on the data we have available to us today.

We expect Q4 revenues to be down in the mid-teens range, albeit at the low end. This includes several points of unfavorable shipment timing in North America as well as 2 points of negative impact from foreign exchange headwinds.

We expect Q4 gross margins to be down ~400 – ~500 bps, including restructuring charges during the same period last year.

We have included the estimated impact from newly implemented tariffs on imports from China and Mexico.

We expect Q4 SG&A dollars to be up low to mid-single digits, including restructuring charges in the prior year.

We will continue to tightly manage expenses while we increase investment to fuel our Win Now priorities, most notably demand creation.

We expect other income and expense, including net interest income to be $45 – $55 million for Q4, and we expect the tax rate for the full year to be in the mid-teens range.

Risk Assessment

NKE’s domestic senior unsecured long-term debt ratings are:

- Moody’s: A1

- S&P Global: AA-

The outlook from both is stable.

Moody’s rating is the top tier of the ‘upper-medium grade’ investment-grade category. S&P Global’s rating is one notch higher at the bottom tier of the high-grade investment-grade category.

Moody’s rating defines NKE as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

S&P’s rating defines NKE as having a VERY STRONG capacity to meet its financial commitments with its rating differing from the highest-rated obligors only to a small degree.

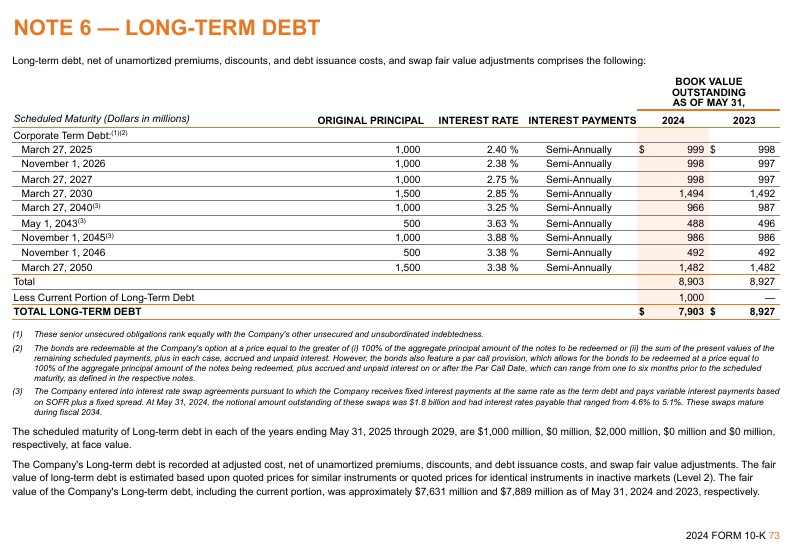

NKE’s long-term debt schedule extracted from the FY2024 Form 10-K reflects $1B of debt that matures on March 27, 2025. Within the next few days, this will be fully repaid thus reducing the company’s corporate term debt to ~$7.9B. I also anticipate NKE will fully repay the debt maturing on November 1, 2026 and March 27, 2027. Once these payments are made, the next maturity date is March 27, 2030. With no significant debt repayments in 2028 and 2029, NKE should be able to aggressively reinvest in the business and/or repurchase shares.

Dividend and Dividend Yield

NKE does not keep its dividend history current on its website. Its dividend history, however, is accessible here.

In May, we can expect NKE to declare its 3rd consecutive $0.40/share quarterly dividend for distribution in July. Following the July and October $0.40/share distributions, I anticipate NKE will increase the quarterly dividend to ~$0.43/share commencing with the January 2026 dividend. Should this materialize, the next 4 quarterly dividend distributions will total $1.66 (($0.40 x 2) + ($0.43 x 2)). With shares trading at ~$68 as I compose this post, the forward dividend yield is ~2.44%.

Dividend metrics are of little relevance in my investment decision making process. My interest lies in the efficient allocation of capital so as to maximize shareholder value; dividend distributions are not always the most optimal means by which to reward investors.

NKE’s capital allocation includes the prolific repurchase of its outstanding shares.

In FY2014 – FY2024 and Q3 2025, the weighted average diluted shares outstanding (in billions) was 1.812, 1.769, 1.743, 1.692, 1.659, 1,618, 1.592, 1.609, 1.611, 1.570, 1.530, and ~1.481B.

At FYE2024 (May 31, 2024), a total of 84.9 million shares at an average price of $106.65 per share had been repurchased under the current $18B program for a total of ~$9.1B.

In Q3 2025, NKE repurchased 6.5 million shares for total consideration of ~$0.499B.

At the end of Q3 2025, NKE had repurchased ~119.3 million shares for a total of ~$11.8B under its $18B June 2002 share repurchase authorization.

With ~$6.2B remaining under the existing share repurchase authorization, NKE could ramp up its share repurchases while shares are undervalued. In addition, the Board could authorize an increase in the share repurchase authorization.

Without jeopardizing its credit ratings, NKE could enter into an accelerated share repurchase (ASR). This is an investment strategy where a publicly-traded company expeditiously buys back large blocks of its outstanding shares from the market by relying on a go-between investment bank to facilitate the deal; NKE would need to furnish upfront cash to the investment bank and then enter into a forward contract to buy/sell NKE shares at a future date.

Valuation

NKE has generated $2.02 of diluted EPS in the first 3 quarters of FY2025. Given the current challenges, I anticipate FY2025 diluted EPS will be ~$2.50. If my estimate is correct, the forward diluted PE is ~27.2 using the current ~$68 share price.

Its valuation based on forward adjusted diluted earnings estimates from the brokers which cover NKE is:

- FY2025 – 38 brokers – ~32 using a mean of $2.13 and low/high of $1.95 – $2.90.

- FY2026 – 38 brokers – ~31.2 using a mean of $2.18 and low/high of $1.23 – $3.56.

- FY2027 – 27 brokers – ~23.6 using a mean of $2.88 and low/high of $1.97 – $3.63.

Looking at the brokers’ earning estimates, there is no consensus on NKE’s performance over the next 1 -2 years. I, therefore, recommend placing no reliance on the current estimates.

As noted earlier, NKE’s conventional and modified FCF amounted to $1.194B and $0.819B in the first half of FY2025. If the second half of FY2025 is similar to the first half, I envision the FY2025 conventional and modified FCF will be ~$2.4B and ~$1.6B.

The diluted weighted average shares outstanding in Q3 2025 and the first 3 quarters of FY2025 was 1.4806 and 1.491 billion shares. If NKE aggressively repurchases shares in Q4, the weighted average for all of FY2025 could be ~1.485B.

Divide ~$2.4B by ~1.485 billion shares and we get FCF/share of ~$1.62 and ~$1.08 calculated under the conventional and modified methods of determining FCF.

With shares trading at ~$68, the P/FCF is ~42 and ~63.

I am very hesitant to rely on these valuations and recommend waiting for the Q3 2025 Form 10-Q at which time the Condensed Consolidated Statement of Cash Flows will provide a better indication of NKE’s YTD cash flow. Furthermore, I anticipate the low end of the broker forward adjusted diluted EPS earnings estimates will be raised in the coming weeks.

Given the current environment, I am also hesitant to place any credence in the FY2026 earnings estimates.

Final Thoughts

Contrarian investing – buying when others are fearful and selling when they are greedy – can create opportunities for above-average returns.

NKE is a turnaround story that needs to play out over the next several quarters to determine the turnaround’s degree of success.

With a US President suffering from narcissistic and sociopathic psychological disorders who is just beginning his 4 year term, business/market conditions are likely to remain highly volatile. NKE’s turnaround is, therefore, highly unlikely to be easy.

The company, however, continues to be profitable. Using the FCF it generates, I see no reason why it should not be able to reduce its corporate term debt from ~$8.9B at FYE2024 to ~$5.9B by the end of March 2027.

Keep in mind that one of NKE’s priorities is to reduce its bloated inventory levels. If it achieves success in reducing its inventory levels, this should free up additional cash flow which can be deployed more efficiently.

If NKE’s valuation remains depressed, I envision a significant reduction in the diluted weighted average number of outstanding shares. From FY2019 to YTD2025, there has been a ~130 million reduction in the weighted average diluted shares; this includes FY2020 and FY2021 when shares were overvalued!

Howard Marks, renowned investor and co-founder of Oaktree Capital, emphasizes that becoming above average in stock investing requires a deep understanding of market behavior, risk, and psychology.

In his memos and books (Mastering the Market Cycle: Getting the Odds on Your Side and The Most Important Thing Illuminated: Uncommon Sense for the Thoughtful Investor), he explains the stock market is driven by emotions like fear and greed. In order to outperform the average investor, we must think independently, avoid following the herd, and consider the behavior of other investors. This requires ‘second-level thinking’ which goes beyond simple analysis.

Marks often highlights the role of risk management – superior returns come from effectively balancing risk and reward. Patience and discipline are crucial, as short-term market fluctuations often mislead investors.

It is imperative that we focus on a company’s intrinsic value rather than reacting to market noise. Markets are unpredictable, and therefore, it is key to remain humble and to maintain emotional control.

I am satisfied with my current exposure and will not be acquiring additional shares. I think, however, this is an opportune time to acquire NKE shares. You, however, need the right temperament.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long NKE.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.