Following my October 2, 2024 post at which time the most currently available financial information was for Q1 2025, Paychex (PAYX) disclosed its intent to acquire Paycor HCM (PYCR) for ~$4.1B on January 7, 2025. PAYX expects to close this acquisition in April 2025.

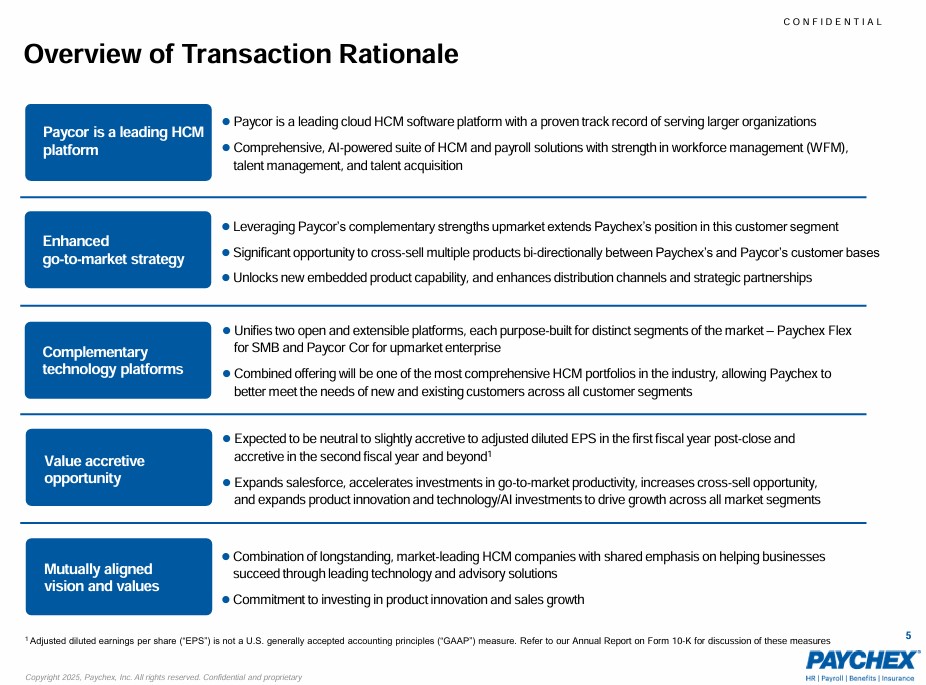

This impending acquisition makes strategic sense as it enables PAYX to expand its client scope. PYCR focuses more upmarket while PAYX focuses more small to medium-sized businesses. PYCR also has some HCM-focused products that are not part of PAYX’s current product offering.

Conceptually, the acquisition should allow PAYX to expand into a more enterprise-focused market. While PYCR will operate as a stand-alone business unit, I anticipate cross-selling opportunities.

Initially, PAYX expected synergies in excess of $80 million. This, however, has been revised higher. While encouraging, success will be highly dependent on a smooth integration and an ongoing collaboration between business units.

With the release of PAYX’s Q3 2025 results and amended FY2025 guidance, I revisit this existing holding.

Business Overview

Please review the company’s website and Part 1 in the company’s Form 10-K.

Paycor Acquisition

Information about PYCR is available in Part 1 Item 1 in the FY2024 Form 10-K that is accessible through the SEC Filings section of its website.

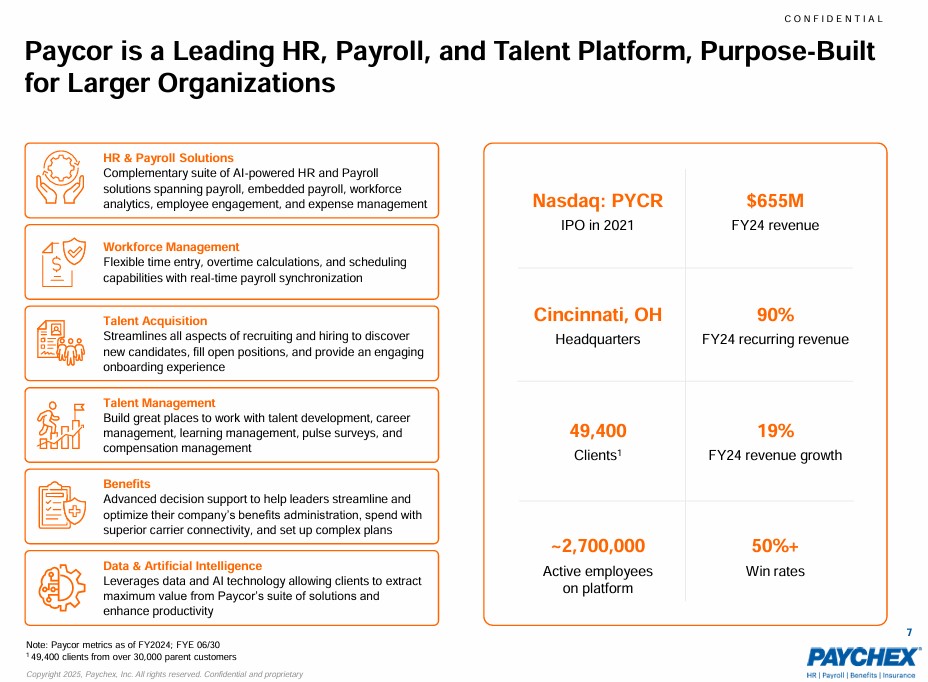

The company was founded in 1990 to provide payroll services to the Cincinnati market; it completed its Initial Public Offering (IPO) in 2021.

PYCR targets small and medium-sized businesses with tens to thousands of employees through its direct sales team and broker partnerships. It focuses on the 50 most populous metropolitan statistical areas in the United States, which encompasses ~66% of the U.S. population. In addition, its Human Capital Management (HCM) Solution partnerships extend its distribution.

The following is from PYCR’s FY2024 Form 10-K:

We estimate our current annual recurring market opportunity is $40 billion in the U.S. and we expect the opportunity to grow as the number of SMBs increase and we continue to expand our product portfolio. To estimate our market opportunity, we identified the number of companies in the U.S. with an employee count between 10 and 1,000. Based on the most recent available data from the U.S. Census Bureau and the U.S. Bureau of Labor Statistics, there were approximately 1.3 million businesses with between 10 to 1,000 employees, totaling approximately 62.3 million employees within our target demographic. We then applied our $53 total list PEPM rate as of June 30, 2024 for our full suite of products to derive our current total addressable market opportunity of $40 billion.

As of June 30, 2024 (FYE2024), PYCR had just over 49,000 clients from over 30,000 parent customers representing a small percentage of the U.S. market for HCM and payroll solutions.

Roughly 90% of PYCR’s FY2024 revenue was recurring with ~2.7 million active employees on its platform.

Since going public, the company’s annual revenue has grown from ~$0.353B in FY2021 to ~$0.348B in the first half of FY2025. The company, however, remains unprofitable and if we deduct share based compensation and capital expenditures (CAPEX) from net cash provided by operating activities, it generates negative Free Cash Flow (FCF).

In essence, PYCR is a company I would eliminate as a potential investment within minutes of reviewing its financial statements. PAYX, however, views PYCR differently and an overview of the transaction rationale is reflected below.

Combined, PAYX deems its total addressable market has risen from ~$90B+ to ~$100B+.

Once the PYCR acquisition is complete, PAYX expects to have ~800,000 customers combined.

Although PYCR is unprofitable and generates negative FCF, the acquisition means PAYX can immediately add ~$0.7B annually to its top line as opposed to working ~2 – ~3 years to organically increase its top line by this amount. (PAYX’s annual revenue in FY2022 and FY2024 was ~$4.612B and ~$5.278B – an increase of ~$0.666B).

Furthermore, PAYX has identified a significant amount of expenses that can be eliminated. For example, in the first half of PYCR’s FY2025, SBC was $28.806 million. I envision the elimination of a good portion of this SBC.

The plan is for:

- PYCR to operate as a stand-alone business unit; and

- PYCR and PAYX customers to remain on the platforms they currently use and to continue to receive support through their existing service team relationships.

Since announcing the PYCR acquisition, PAYX has made considerable progress on integration planning. It now expect synergies over the $80 million it originally forecast and this acquisition is expected to be accretive to PAYX’s adjusted EPS in FY2026.

Financial Review

Q3 and YTD2025 Results

PAYX’s Q3 and YTD2025 results and FY2025 outlook are accessible here.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

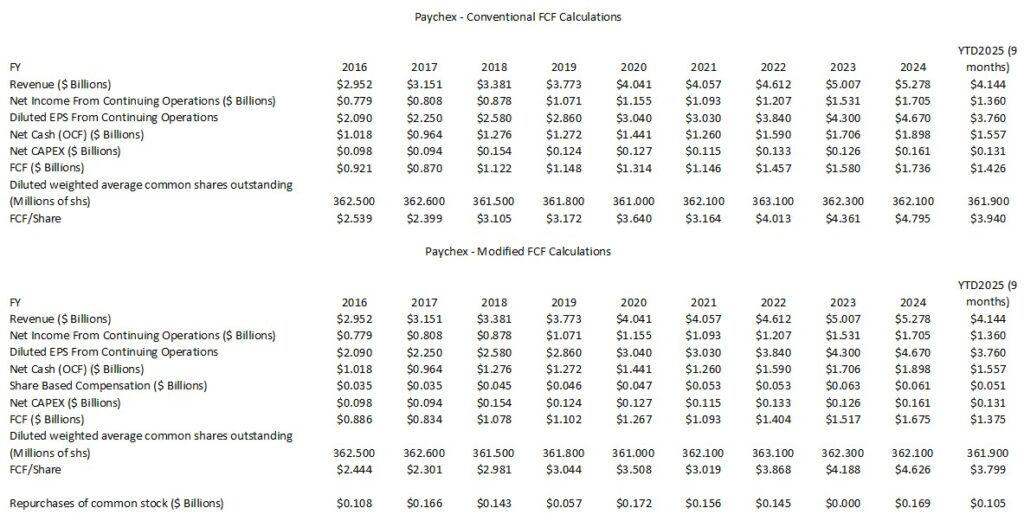

The following reflects PAYX’s FCF using the conventional and modified methods. The modified method deducts share-based compensation (SBC) from OCF.

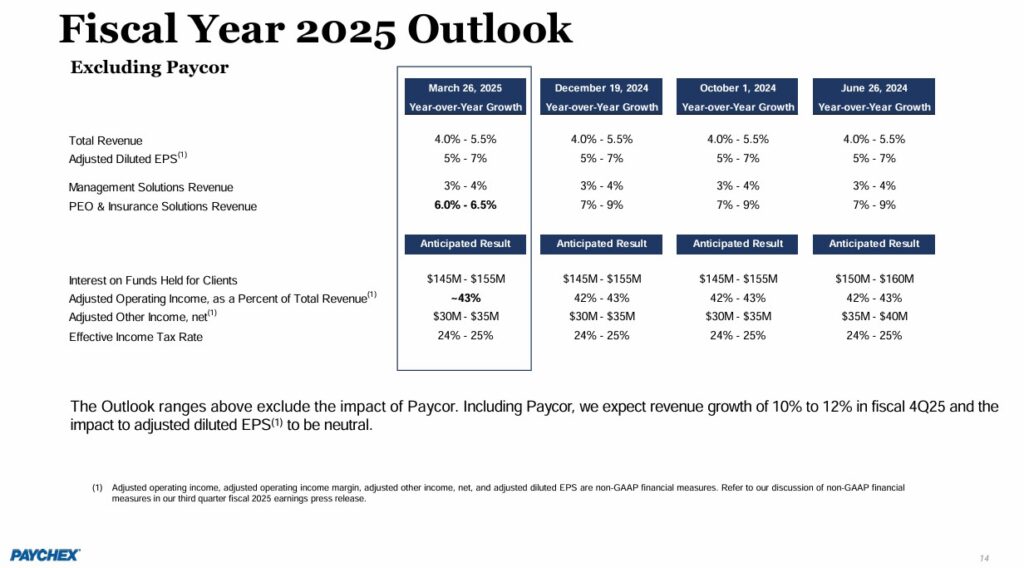

FY2025 Outlook

The following reflects PAYX’s prior and current FY2025 outlook. Including PYCR, management now expects ~10% – ~12% revenue growth in Q4 2025 and a neutral impact from the acquisition to adjusted EPS.

Risk Assessment

No rating agency currently rates PAYX’s debt.

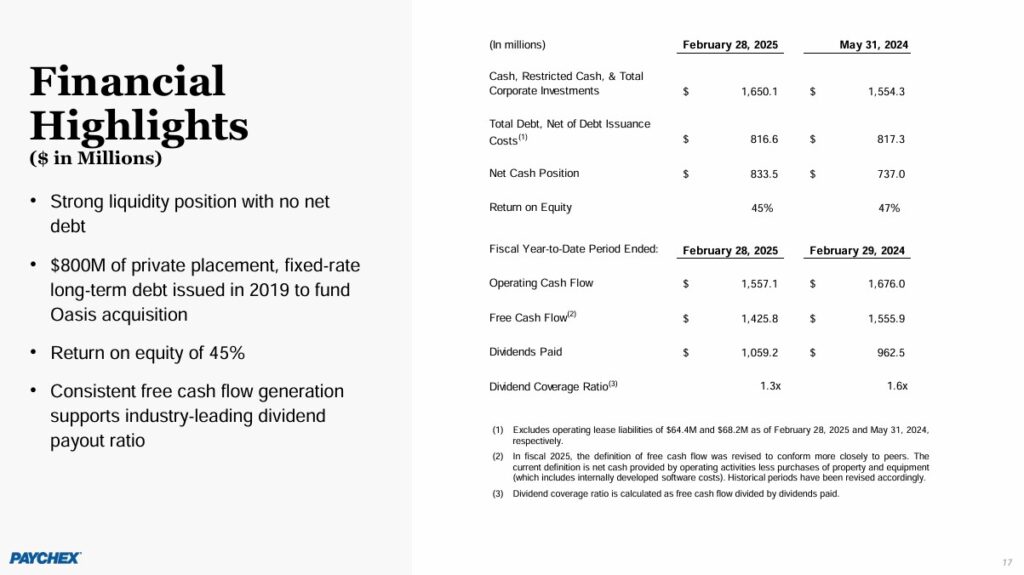

At the end of Q3 2025, PAYX had current assets before funds held for clients of ~$3.893B. Of this total, ~$1.601B was cash, cash equivalents, and corporate investments and ~$1.843B was Accounts Receivable, net of allowance for credit losses and professional employer organization (PEO) unbilled receivables, net of advance collections.

At the end of Q3 2025, PAYX’s Current Assets before funds held for clients were ~2.5x more than Current Liabilities before client fund obligations.

Total short-term and long-term borrowings of ~$0.818B are similar to prior recent quarters.

The following reflects the details of PAYX’s long-term debt. On March 13, 2019, PAYX completed the private placement of Senior Notes, Series A in an aggregate principal amount of $0.4B due on March 13, 2026, and Senior Notes, Series B in an aggregate principal amount of $0.4B due on March 13, 2029.

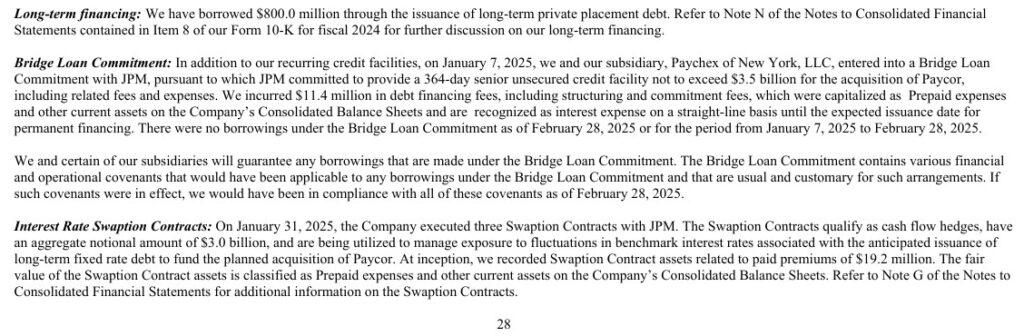

Financing arrangements for the PYCR acquisition are:

In FY2026, I expect PAYX to arrange long-term financing to retire the financing provided under the $3.5B Bridge Loan Commitment. With a $0.5B variance between the maximum borrowing permissible under the Bridge Loan facility and the Interest Rate Swaption, I suspect PAYX might be planning to arrange only $3B of long-term financing. The remaining $0.5B might be classified as short-term debt with repayment to be made in FY2027. This seems logical since PAYX is scheduled to repay the $0.4B Series A Senior Notes maturing in March 2026. I do not envision PAYX disbursing ~$0.9B toward debt repayment in 1 fiscal year.

PAYX is a conservatively managed company. I envision management will structure its Balance Sheet to retain a relative low risk profile.

Dividends and Dividend Yield

PAYX currently does not reflect its dividend history on its website; the dividend history is accessible here.

Looking at PAYX’s historical capital allocation priorities, we see that steadily increasing the dividend ranks ahead of share repurchases. Given this, I expect PAYX will declare a dividend increase in early May that will take effect with the end of May dividend payment.

With an increase in PAYX’s leverage resulting from the PYCR acquisition, I expect the next dividend increase will be less than the last couple of dividend increases which were ~$0.09 – ~$0.10.

In the first 3 quarters of FY2025, PAYX repurchased $104.5 million of its shares; $104 million in Q1, $5 million in Q2, and $0 in Q3.

Looking at the weighted average diluted shares outstanding in FY2016 – YTD2025 (see table above), share repurchases appear to be primarily for ‘anti-dilutive’ purposes.

Valuation

In the Valuation section of my October 2, 2024 post I wrote:

Management’s FY2025 outlook calls for a ~5% – ~7% increase from the FY2024 adjusted diluted EPS meaning a range of ~$4.96 – ~$5.05; in Q1 2025 it generated $1.16.

With the current share price being ~$140.80 and management’s ~$4.96 – ~$5.05 FY2025 adjusted diluted EPS outlook, we get a forward adjusted diluted PE range of ~27.9 – ~28.4.

Revisions to broker adjusted diluted earnings estimates are likely over the coming days but at the moment, we get the following using current estimates:

- FY2025 – 17 brokers – mean of $4.98 and low/high of $4.90 – $5.03. Using the mean estimate, the forward adjusted diluted PE was ~28.3.

- FY2026 – 17 brokers – mean of $5.29 and low/high of $5.18 – $5.37. Using the mean estimate, the forward adjusted diluted PE was ~26.6.

- FY2027 – 9 brokers – mean of $5.61 and low/high of $5.45 – $5.77. Using the mean estimate, the forward adjusted diluted PE was ~25.1.

PAYX typically generates FCF that slightly exceeds net earnings and I expect the same in FY2025.

In Q1 2015, it generated ~$0.510B of FCF. We can expect ~$2.042B of FCF in FY2025 if PAYX generates a similar amount of FCF in each of the next 4 quarters.

Erring on the side of caution, I estimate PAYX will generate ~$1.95B of FCF in FY2025 and the weighted average diluted shares outstanding should be ~361.9 million. Using these estimates, PAYX’s estimated FCF/share is ~$5.39. Divide the current ~$140.80 share price by ~$5.39 and the forward P/FCF is ~26.1. This is slightly higher than most levels during FY2014 – FY2024.

We now know that in the first 3 quarters of FY2025, PAYX generated $3.76 of diluted EPS and $3.79 of adjusted diluted EPS. The acquisition of PYCR in April 2025 is expected to have minimal impact on PAYX’s adjusted diluted earnings in FY2025.

If PAYX generates a comparable level of earnings in Q4 as in the prior 3 quarters, we can expect diluted EPS and adjusted diluted EPS in FY2025 to be ~$5.00 and ~$5.05. Using the ~$150.20 March 26 closing share price, the forward diluted PE and forward adjusted diluted PE are ~30 and ~29.7.

PAYX’s valuation based on adjusted diluted earnings broker estimates and the current share price is:

- FY2025 – 17 brokers – mean of $4.98 and low/high of $4.73 – $5.06. Using the mean estimate, the forward adjusted diluted PE is ~30.2.

- FY2026 – 17 brokers – mean of $5.30 and low/high of $5.00 – $5.61. Using the mean estimate, the forward adjusted diluted PE is ~28.3.

- FY2027 – 12 brokers – mean of $5.62 and low/high of $5.38 – $5.86. Using the mean estimate, the forward adjusted diluted PE is ~26.7.

I anticipate changes to the broker estimates over the coming days.

In the first 9 months of FY2025, PAYX’s FCF was ~$3.94 and ~$3.80 calculated under the conventional and modified methods. If it generates a comparable amount of FCF in Q4 as in the first 3 quarters of FY2025, I anticipate FY2025 FCF of ~$5.25 and ~$5.07. Using the ~$150.20 March 26 closing share price, PAYX P/FCF is ~28.6 and ~30 .

Final Thoughts

I am a PAYX shareholder since July 2, 2009.

My PAYX exposure currently consists of 847 shares (394 and 453 shares in a ‘Core’ and a ‘Side’ account, respectively). It was my 26th largest holding when I completed 2024 Year End Review and my 27th largest holding when I completed my 2024 Mid Year Review.

PAYX makes periodic bolt-on acquisitions with its largest being the Oasis acquisition for $1.2B in December 2018…UNTIL…the impending $4.1B PYCR acquisition.

When I last wrote about PAYX in my October 2, 2024 post, I stated:

It is also quite possible it will eliminate half its long-term debt in March 2026 and fully eliminate it in March 2029. Eliminating this debt would reduce annual interest costs by ~$33.74 million. In addition, PAYX’s capital allocation could change with the elimination of this $0.8B of debt. Hopefully, the valuation of PAYX’s shares might be sufficiently compelling to prompt the Board to ramp up share repurchases.

There are other investment opportunities that have the potential to generate superior long-term total annual investment returns. PAYX’s business, however, is predictable. Furthermore, it has the potential to become another holding in the FFJ Portfolio with billions of cash, cash equivalents, and corporate investments and NO long-term debt.

This is now no longer the case as PAYX requires financing to acquire PYCR.

At the time of my prior post, I thought PAYX was too richly valued. Now, I think PAYX is even less attractively valued. Based on management’s current outlook, I think a fair price is closer to the low – mid $130s. I am, therefore, in no rush to increase my PAYX exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long PAYX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.