I last reviewed Agilent (A) in this November 27, 2024 post at which time the most current financial information was for Q4 and FY2024. With the recent release of Q1 2025 results and an update to the FY2025 outlook, I revisit this existing holding.

In my prior review, I state that if A’s share price retraces to the upper $120s, I might add to my exposure. As luck would have it, this has materialized.

Following my February 27, 2025 100 share purchase, my A exposure now consists of 600 shares in a ‘Core’ account the FFJ Portfolio at an average cost of ~$121.79; A was not a top 30 holding when I completed my 2024 Year End Portfolio Review.

Business Overview

When I wrote my November 27, 2024 post, A had recently announced a change in its operating segments. It moved its cell analysis business from the life sciences and applied markets segment to the diagnostics and genomics operating segment. The purpose of this transition was to further strengthen growth opportunities for both organizations. It now has 3 reportable business segments:

- life sciences and applied markets;

- diagnostics and genomics; and

- Agilent CrossLab.

A comprehensive overview of the business and each segment plus the risk factors is found in Item 1 within the FY2024 Form 10-K, (see SEC Filings). The company’s website also includes a wealth of information.

Growth Potential

The company’s website currently reflects that A serves large, attractive markets with a $65B opportunity, growing 4-6%. With FY2024 revenue of ~$6.5B, A has ample growth opportunity.

Financials

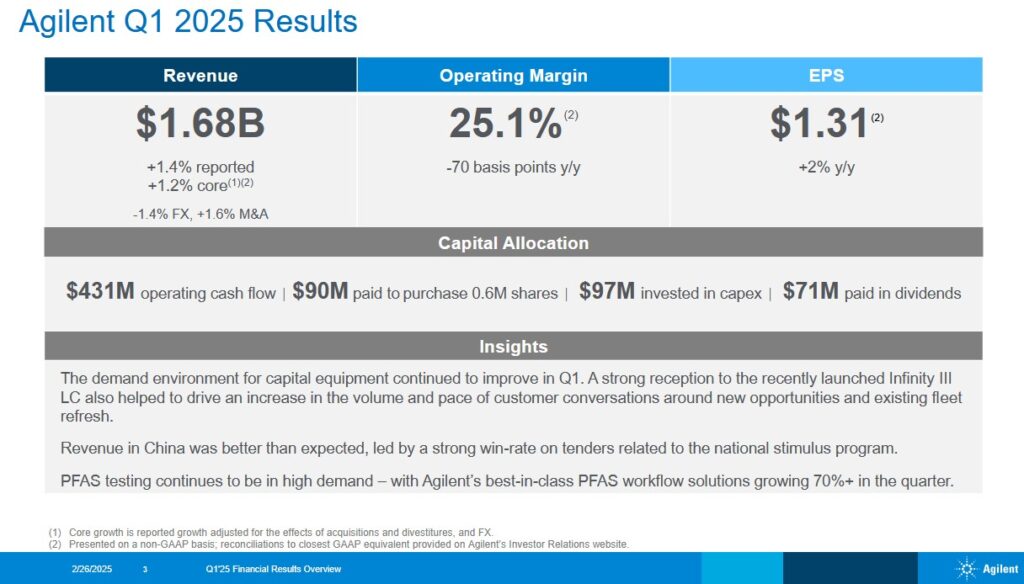

Q1 2025 Results

Material related to the Q1 2025 earnings release is accessible here. The investor presentation reflects the results by by geography, product type, end market, and segment.

Looking at the ‘reconciliations of revenue by region excluding acquisitions, divestitures, and the impact of currency adjustments (core)’ schedules reflected within the Financial Information report, we see the following:

- A’s FY2024 revenue by business segment suffered a ~5% YoY decline. The Q4 results, however, were 1% better than in Q4 2023.

- A’s FY2024 revenue by region suffered a ~5% YoY decline. The Q4 results, however, were 1% better than in Q4 2023.

- China and Hong Kong, a key growth market, suffered a 12% YoY reduction in revenue. The Q4 results, however, were only 2% lower than in Q4 2023.

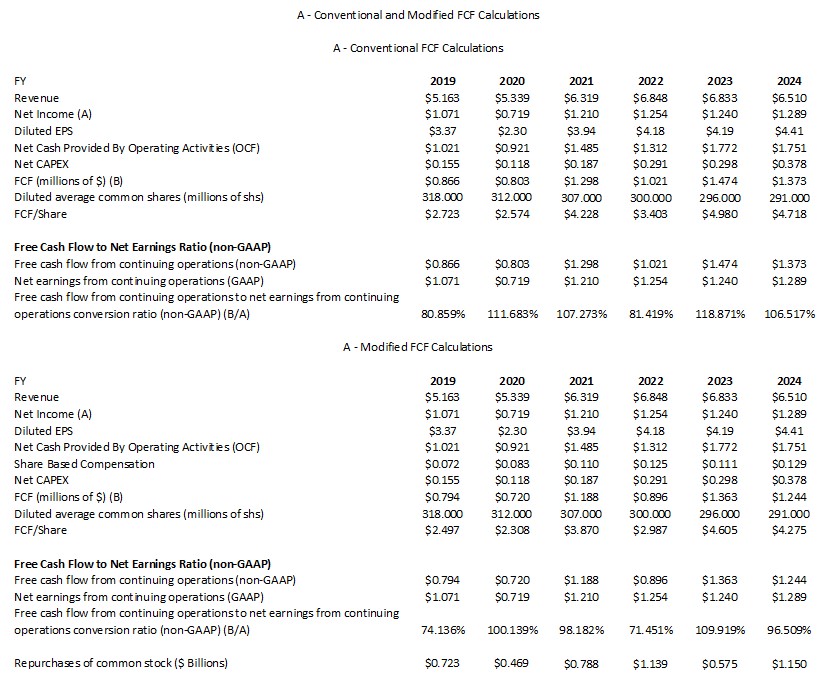

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In recent posts I explain my rationale for deducting share-based compensation (SBC) from a company’s OCF to determine FCF. The following reflects A’s FCF using the conventional and modified methods. Fortunately, A’s SBC is nothing remotely close to that of many technology companies!

Capital Allocation

A’s capital allocation priority is to reinvest in the business. Share repurchases and dividend distributions are also a component of A’s capital allocation.

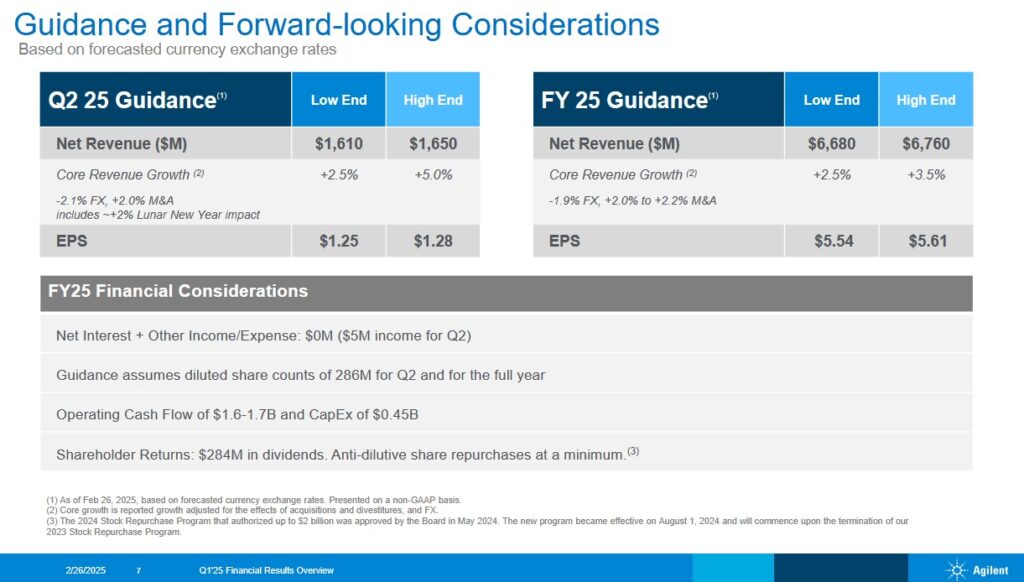

Q2 and FY2025 Guidance

The following reflects A’s Q2 and FY2025 guidance.

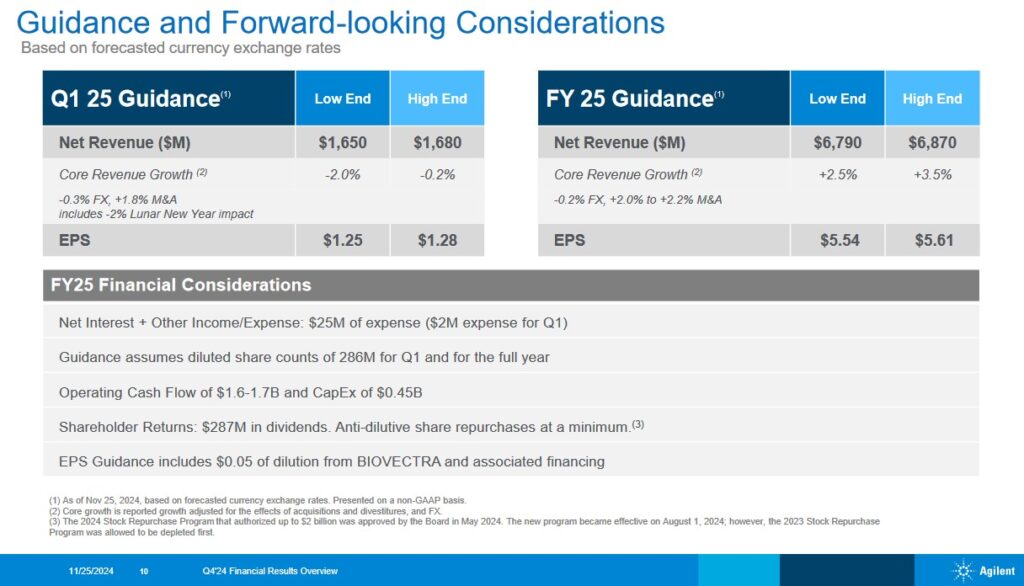

Prior guidance was as follows.

The adjustment to A’s full year reported revenue reflects the strengthening of the U.S. dollar. Prior revenue guidance provided in November incorporated only a very modest FX headwind. Since then, the U.S. dollar has appreciated. Based on current exchange rates, A now projects an incremental $0.11B in currency headwinds. Currency is now expected to represent a 1.9% headwind for the year versus a prior 20 bps headwind.

A’s management is typically conservative with guidance and the FY2025 guidance is no exception. On the earnings call, management indicated there remains considerable uncertainty as to the extent industry conditions will improve. This cautionary outlook is despite Chinese government stimulus and the aging fleet of instruments which its biopharma clients should be updating.

Risk Assessment

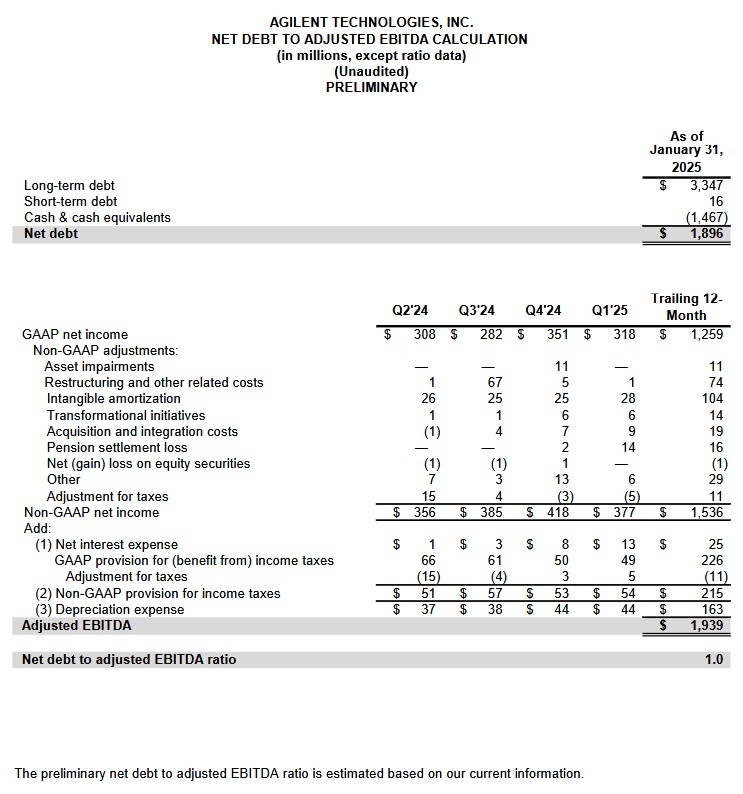

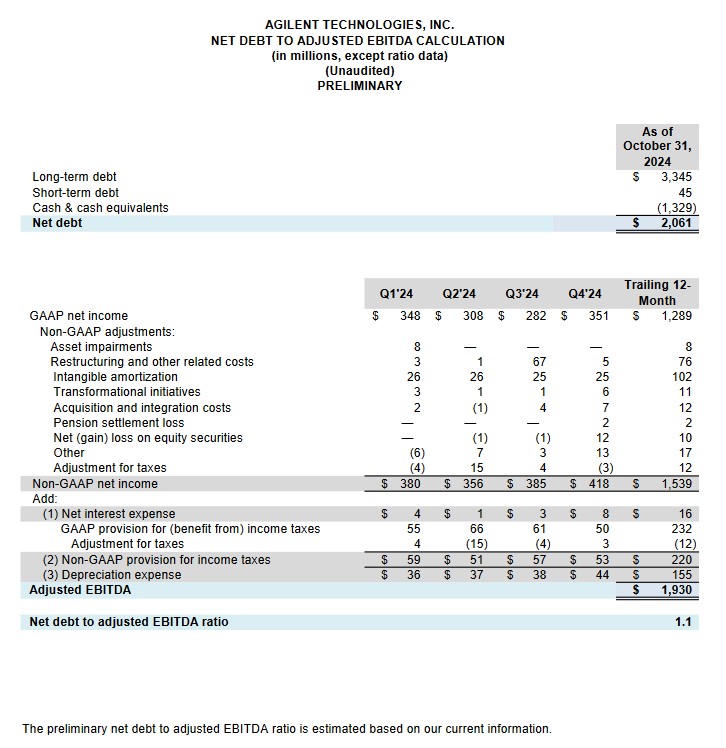

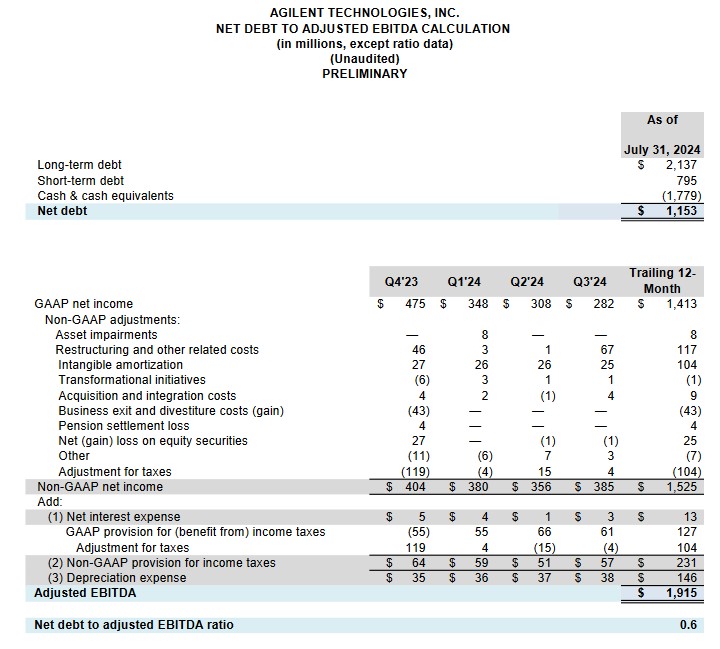

A’s net debt to adjusted EBITDA ratio is 1.0 at the end of Q1 2025 versus 1.1 at FYE2024 and 0.6 at the end of Q3 2024.

- At the end of Q1 2025, A had $0.016B of short-term debt and $3.347B of long-term debt.

- It had $0.045B of short-term debt and $3.345B of long-term debt at FYE2024.

- At the end of Q3 2024, A had ~$0.795B of short-term debt and ~$2.137B of long-term debt.

Investors need to remember that A completed a couple of acquisitions which I touched upon in prior posts (Sigsense Technologies and BIOVECTRA). In FY2024, A disbursed ~$0.862B to acquire businesses and intangible assets, net of cash acquired. These acquired businesses, however, contributed little to A’s earnings.

While A’s net debt to adjusted EBITDA ratio is higher than at the end of Q3 2024, investors should not be alarmed; A’s credit ratings remain unchanged from the time of my prior posts.

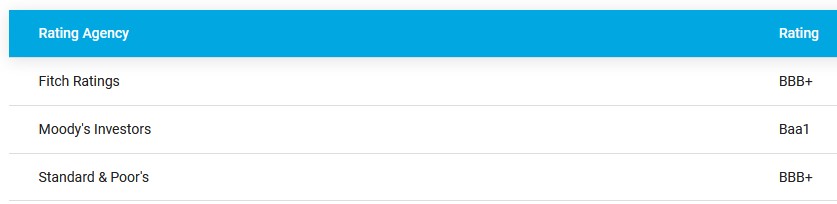

A’s website currently reflects the following credit ratings.

- Moody’s completed its most recent review on May 3, 2023 at which time A’s rating was upgraded from Baa2 to Baa1.

- S&P Global completed its most recent review on April 16, 2024 and affirmed A’s BBB+ rating with a Positive outlook.

- Fitch completed its most recent review on October 31, 2024 and affirmed A’s BBB+ rating with a Stable outlook.

All three rating agencies define A as having an adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of A to meet its financial commitments.

Dividend and Dividend Yield

On February 19, 2025, A announced a quarterly dividend of 24.8 cents/share. The quarterly dividend will be paid on April 23, 2025, to all shareholders of record as of the close of business on April 1, 2025. The company’s dividend history has yet to reflect this recently announced dividend.

The dividend yield is typically below 1% and should have little bearing on whether to invest in the company or not. Investors should expect the bulk of A’s future total investment return to continue to be predominantly in the form of capital appreciation.

The Inflation Reduction Act of 2022, which was enacted into law on August 16, 2022, imposes a nondeductible 1% excise tax on the net value of certain stock repurchases made after December 31, 2022. During FY2024, A recorded the applicable excise taxes payable of ~$10 million as an incremental cost of the shares repurchased and a corresponding liability for the excise tax payable in other accrued liabilities on its consolidated balance sheet. In comparison, in FY2023, A recorded excise taxes payable of ~$3 million related to shares repurchased in 2023 and paid the tax in 2024.

Despite this nondeductible 1% excise tax, I much prefer that a company repurchase undervalued shares versus distributing dividends.

As a Canadian resident, I incur a 15% dividend withholding tax on any dividends received in a taxable account. Furthermore, I have to report dividend income on my annual tax return. I am not seeking additional annual income and much prefer deferring any tax liability for as long as possible.

The weighted average shares outstanding (in millions of shares) in FY2013 was ~345. In FY2024, Q4 2024, and Q1 2025, it was ~291, ~287, and ~287.

Repurchases in FY2018 – FY2024 (in $B) were 0.422, 0.723, 0.469, 0.788, 1.139, 0.575, and 1.15. Unfortunately, A’s shares were generally overvalued with the exception of the last couple of years.

Management’s FY2025 guidance includes anti-dilutive share repurchases at a minimum.

The 2024 Stock Repurchase Program that authorizes the repurchase of up to $2B was approved by the Board in May 2024 and became effective on August 1, 2024.

In Q1 2025, A repurchased ~$90 million of its shares but this amount was partially offset by ~$40 million of SBC.

Valuation

The link to my November 27, 2024 post in which I provide my prior valuation estimate is found at the beginning of this post.

A’s FY2025 guidance still calls for an adjusted diluted PE range of ~$5.54 – ~$5.61.

On February 27, I acquired an additional 100 shares @ ~$127.30 resulting in a forward adjusted diluted PE range of ~22.7 – ~23; the share price at the time of my prior review was ~$134.

A’s forward-adjusted diluted PE levels using my ~$127.30 purchase price and the current broker estimates are:

- FY2025 – 20 brokers – ~22.9 using a mean of $5.57 and low/high of $5.54 – $5.63.

- FY2026 – 20 brokers – ~20.8 using a mean of $6.11 and low/high of $6.00 – $6.22.

- FY2027 – 15 brokers – ~19 using a mean of $6.71 and low/high of $6.51 – $6.95.

Management’s FY2025 guidance calls for OCF of $1.6B – 1.7B and CAPEX of $0.45B.

SBC in Q1 2025 was $40 million. If A’s quarterly SBC continues at this pace for the remaining quarters in FY2025, FY2025 SBC will be $0.16B. This is substantially higher than in recent prior years so I envision a scale back over the remaining 3 quarters and use $0.14B to calculate A’s FY2025 FCF.

Subtracting CAPEX of $0.45B and $0.14B of SBC from the $1.65B OCF mid-point guidance, we get ~$1.06B of FCF. The FY2025 diluted share count outlook is 286 million shares so $1.06B/286 million shares equals ~$3.71 of FCF/share.

NOTE: A’s guidance calls for anti-dilutive share repurchases at a minimum. If shares remain undervalued, I anticipate the company may repurchase more than the minimum number of shares.

Divide my ~$127.30 purchase price by ~$3.71 and we get a P/FCF of ~34.3.

The consensus average price target from analysts is ~$154. I, however, continue to deem ~$140 to be a fair value. The difference between my fair value estimate and my February 27 purchase price suggests a ~10% upside before reaching fair value (($140 – $127.30)/$127.30).

Final Thoughts

The Bank of Canada’s January 2025 Monetary Policy Report states:

Economic growth has ticked up in Canada, boosted by past cuts in interest rates. In the absence of new tariffs, growth is forecast to strengthen, and inflation remains close to 2%. But the threat of new tariffs is causing major uncertainty.

The Royal Bank of Canada January 7, 2025 Economics Report is equally optimistic with a forecast that Canada’s annual inflation is expected to remain below 2% for 2025.

I think The Bank of Canada and The Royal Bank of Canada inflation estimates are outdated!

I very seriously question whether Canada’s rate of inflation will remain at the ~2% level given the impending implementation of tariffs by the US. Whether the rate of inflation rises to 3% or more is currently an unknown. Anyone in Canada, however, who is satisfied with a sub-6% pre-tax investment return will find that they are merely treading water versus building wealth.

While A’s share price could slip further in the short-term, I focus on an investment’s total return potential over the very long-term. Based on my assessment of Agilent, I think near-term headwinds present a buying opportunity.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long A.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.