I last reviewed Zoom Communications in this November 26, 2024 post at which time I pointed out how stock-based compensation (SBC) distorts the company’s Free Cash Flow (FCF).

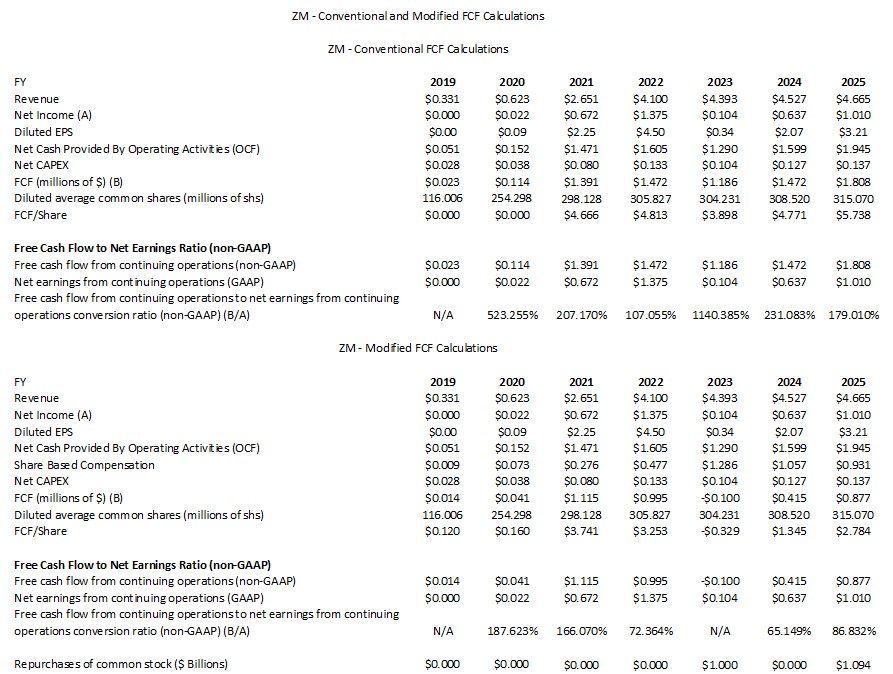

FCF is a non-GAAP metric. How companies calculate FCF is, therefore, inconsistent. ZM, for example, merely deducts capital expenditures (CAPEX) from its Net cash provided by operating activities. As explained in various prior posts, I think it is prudent to also deduct share-based compensation (SBC). ZM was issuing a TON of shares, and therefore, I compare ZM’s FCF with/without deducting SBC (see below).

At the time of my November 26, 2024 post, the most currently available financial information was for Q3 and YTD2025; ZM has a January 31 fiscal year-end. With the release of Q4 and FY2025 results and FY2026 guidance, I now revisit this existing holding.

Business Overview

Part 1, Item 1 in ZM’s FY2024 Form 10-K (see SEC Filings) provides a comprehensive overview of the business, competition, and risks.

On October 9, 2024, ZM held its Zoomtopia Investor Session. I highly recommend reviewing this information to get a better idea of this company’s future potential.

ZM has Class A (publicly traded shares) and Class B shares. The Class A and B shares have 1 and 10 votes per share, respectively.

The Class B shareholders have significant influence over the management and over all matters requiring stockholder approval, including the election of directors and significant corporate transactions, such as a merger or other sale of ZM or its assets, for the foreseeable future. Within the Risk Factors section of ZM’s Form 10-Q and Form 10-K, there is commentary regarding this dual-class structure.

Financials

Q4 and FY2025 Results

ZM’s Q4 and FY2025 earnings material (including the transcript of management’s commentary of the earnings call) is accessible here.

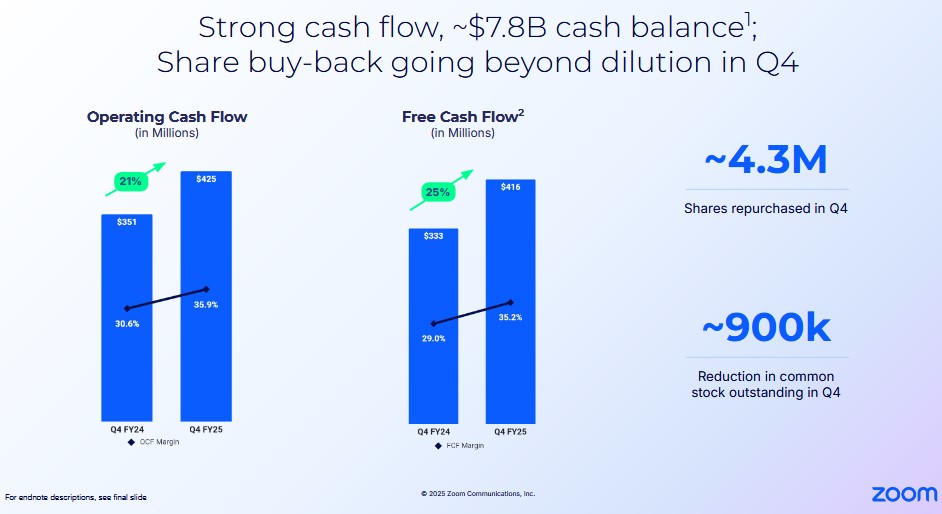

At the time of my prior post, ZM’s cash and cash equivalents and marketable securities at the end of Q3 2025 was ~$7.7B. This was an increase from ~$7.5B at the end of Q2 2025 and ~$7B at FYE2024. At FYE2025, this has risen to ~$7.79B.

The company’s total liabilities at the end of Q3 2025 were ~$2B but ~$1.379B was current and non-current deferred revenue – money received from clients in advance of services having been provided. At FYE2025, total liabilities were ~$2.053B but ~$1.354B was current and non-current deferred revenue. Keep in mind, that ZM still has all this liquidity AFTER ~$1.094B of share repurchases in FY2025!

ZM is a great example of how investor sentiment can have an immediate impact on a company’s share price. Despite posting solid results in Q4 and FY2025, ZM’s share price has retraced from ~$89 at the time of my November 29, 2024 post to ~$74 following the February 24 after-market earnings release.

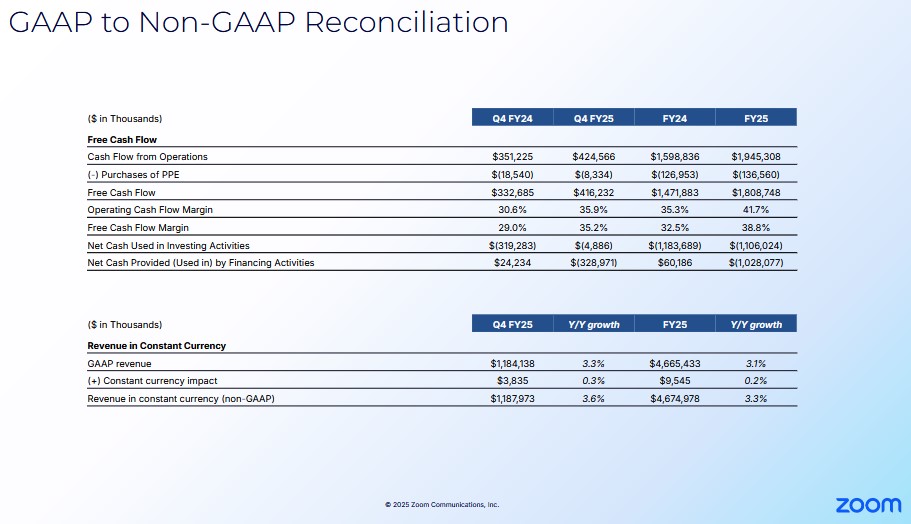

Revenue in Q4 2025 came in at $1.18B, up 3.3% YoY, operating cash flow jumped 21.7% to ~$1.95B, and margins continued to expand. Investors, however, are underwhelmed with ZM’s FY2026 outlook with projected revenue growth of just 3.1% in constant currency. Furthermore, heavy SBC continues to weigh heavily on the company’s earnings outlook.

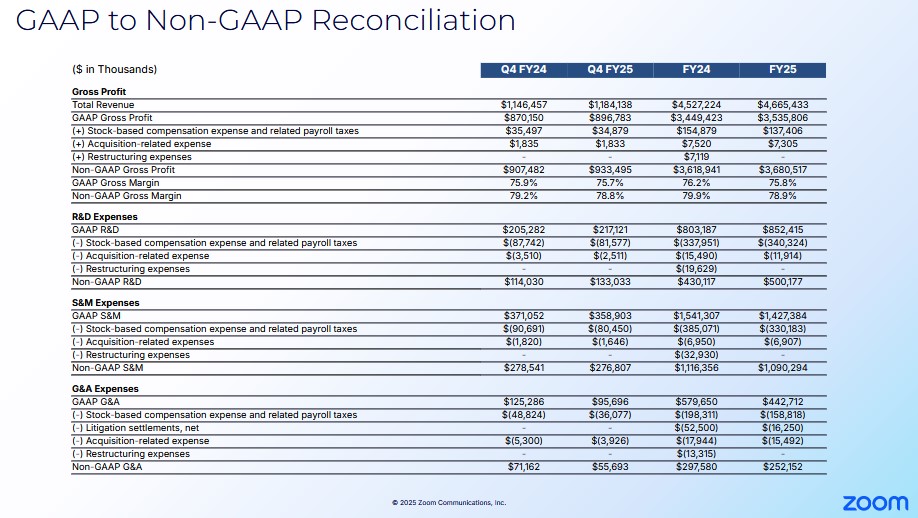

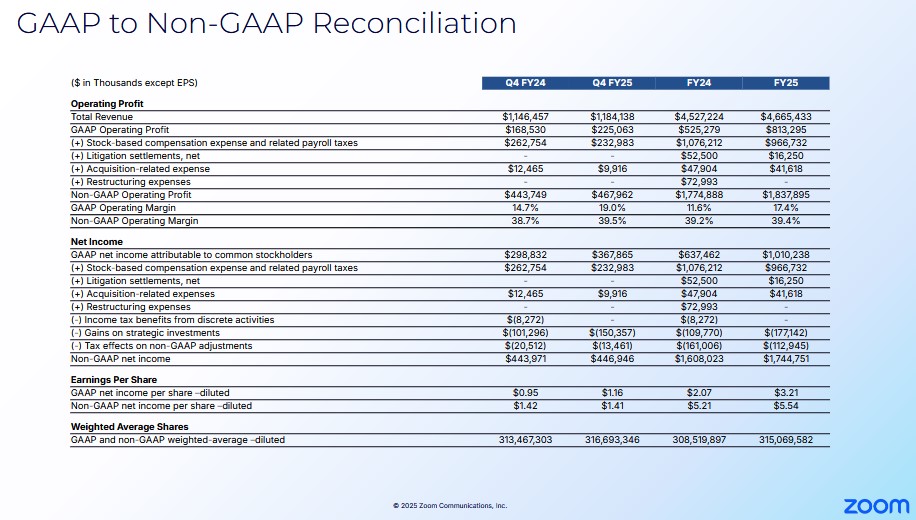

I provide the Q4 and FY2024 and Q4 and FY2025 results below for ease of reference.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

The following reflects the manner in which ZM calculates FCF. Although CAPEX is relatively low, keep in mind that ZM spends a considerable amount on R&D; R&D in FY2024 and FY2025 was $0.803B and ~$0.853B!

I think investors should exclude the stock-based compensation (SBC) line item on the Consolidated Statements of Cash Flows to arrive at a company’s net cash provided by operating activities; common forms of SBC are shares, stock options, restricted share units (RSUs), phantom shares, and employee stock ownership plans (ESOP).

Let’s use an extreme example where Company A remunerates its employees solely by way of SBC thereby requiring no use of cash. The income statement will treat the SBC as an expense but the SBC will be added back to determine the net cash provided by operating activities on the Consolidated Statements of Cash Flows.

On the other hand, Company B compensates its employees 100% by way of wages/salaries; the income statement will reflect this expense. On the Consolidated Statements of Cash Flows, however, nothing will be added back to determine the net cash provided by operating activities.

Both companies could perhaps compensate their respective employees the same amount. Because Company A disburses no cash, however, its FCF would be greater than that of Company B by the exact amount of the SBC (assuming all other line items are the same).

Why should how a company compensates its employees lead to different Price/FCF valuations?

Given my rationale for deducting SBC, I provide a comparison of ZM’s FCF using the ‘conventional’ and ‘modified’ methods.

We see that ZM’s diluted average common shares outstanding has ballooned in recent years. In FY2025, for example, it repurchased ~$1.094B of shares BUT its SBC was ~$0.931B. Management has previously stated that it intends to bring its SBC under control and/or repurchase sufficient shares to offset SBC. FY2025 is a start but it remains to be seen whether this continues.

Capital Allocation

The capital allocation priority is to reinvest in the company. The opportunistic repurchase of Class A shares comes next with dividend distributions being non-existent.

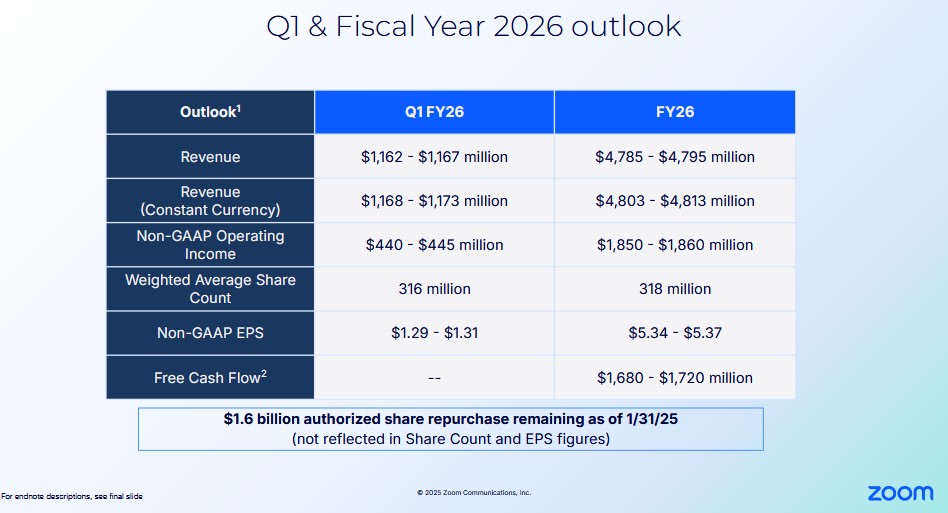

Q1 and FY2026 Outlook

The following reflects ZM’s Q1 and FY2026 outlook.

Risk Assessment

ZM has no debt to rate.

Dividends and Share Repurchases

Dividend and Dividend Yield

ZM does not distribute a dividend.

Share Repurchases

Under ZM’s $2.7B share buy-back authorization, it repurchased 4.3 million shares for $0.355B in Q4, increasing its repurchases quarter over quarter by $53 million dollars and contributing to the reduction of common stock outstanding in Q4.

The FY2026 outlook calls for an increase in the weighted average number of outstanding shares (~318 million from ~315 million in FY2025). This, however, does not account for any share repurchases the company might make with the remaining $1.6B authorized share repurchase as of FYE2025.

Management likely knows when ZM’s shares are undervalued, and therefore, I hope repurchases FY2026 will be at attractive valuations.

Suppose it uses the entire $1.6B to repurchase shares at an average cost of $82. This works out to ~19.5 million shares. If it repurchases shares at ~$78, this works out to ~20.5 million shares. The FY2026 outlook excluding any share repurchases calls for only a 3 million share increase from FY2025.

Valuation

When I wrote my November 26, 2024 post, ZM’s share price was ~$89. I concluded that post with:

ZM’s share price can be volatile, however, so retracing to the high $70s is entirely possible. Should this happen, I intend to increase my exposure.

As luck would have it, ZM’s share price has pulled back. On February 25, 2025, I acquired an additional 100 shares @ ~$73.60 in one of the ‘Core’ accounts in the FFJ Portfolio.

ZM’s FY2026 outlook calls for adjusted diluted EPS of $5.34 – $5.37. Using my purchase price, the forward adjusted diluted PE is ~14.3.

Using my purchase price and the currently available adjusted diluted EPS broker estimates, ZM’s forward adjusted diluted PE levels are:

- FY2026 – 31 brokers – ~13.7 using a mean of $5.39 and low/high of $4.84 – $5.99.

- FY2027 – 29 brokers – ~ 13.4 using a mean of $5.51 and low/high of $5.00 – $6.62.

- FY2028 – 13 brokers – ~ 13 using a mean of $5.70 and low/high of $4.70 – $6.75.

These estimates will likely change over the coming days. Furthermore, I place little reliance on estimates beyond FY2026 since much can change beyond the current fiscal year.

Conventional FCF Calculation

ZM’s FY2026 FCF guidance is $1.68B – $1.72B. Management’s weighted average diluted shares outstanding estimate for FY2026 is 318 million shares. This, however, excludes any share repurchases that may occur.

Using management’s outlook, we get FCF/share of ~$5.28 – ~$5.41. Based on my ~$73.60 purchase price, the forward P/FCF is ~13.6 – ~14.

Modified FCF Calculation

If FY2026 SBC increases from the FY2025 level of ~$0.931B to ~$1B, the FY2026 FCF range drops to ~$0.68B – ~$0.72B. I calculate this range by subtracting ~$1.0B from management’s FY2026 FCF outlook. Taking the ~$0.7B mid-point and dividing it by 318 million shares, I arrive at a FY2026 FCF/share estimate of ~$2.20. Divide my ~$73.60 purchase price by ~$2.20 and the P/FCF is ~33.5.

Should ZM repurchase ~$1.6B of its shares at attractive valuations throughout FY2026, the weighted average number of outstanding shares should be less than 318 million. The FCF/share should be somewhat greater than ~$2.20 meaning that the P/FCF should be better than ~33.5.

Final Thoughts

Despite negative investor sentiment, I have increased my Zoom Communications exposure.

I like ZM’s long-term outlook and appreciate that its Balance Sheet is a fortress. Although I dislike the extent of ZM’s SBC, I remain hopeful it will continue to repurchase shares (at attractive valuations) that exceed the number of shares issued as part of its employee compensation. Furthermore, the SBC component of employee compensation is something management can alter if required. If employees do not like changes to their compensation structure, they can leave and go elsewhere. The challenge they will face, however, is that the job market is not what it was a few years ago. Other tech firms are laying off people AND some are also coming to the realization they need to scale back on SBC.

Based on my analysis, I have acquired an additional 100 shares in a ‘Core’ account within the FFJ Portfolio. ZM, however, is still not a top 30 holding.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ZM.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.