With ~$11.6T in assets under management (AUM) following a record $641B of full year net inflows, including $281B in Q4 2024, I view BlackRock (BLK) as a great long-term investment. What I need to determine is whether BLK’s valuation is sufficiently attractive to increase my exposure.

I last reviewed BLK in my October 17, 2024 post at which time the Q3 and YTD2024 results were the most current. In that post, I touch upon the acquisition of Global Infrastructure Partners (GIP); GIP owns and operates energy, transportation, and water and waste companies, including a stake in London’s Gatwick Airport. This acquisition closed on October 1, 2024.

At the end of June 2024, BLK also announced its intent to acquire UK data provider Preqin in an effort to expand its private-market operations. The plan was to close this acquisition by the end of 2024. In early December, however, British antitrust officials said they were opening a formal investigation into BLK’s acquisition of Preqin. The Competition and Markets Authority in the UK launched its first phase of a formal investigation. A decision is due by February 12 on whether to escalate the case for a more in-depth probe.

In that post I also touch upon BLK’s discussions with Jio Financial Services Ltd. in India in its effort to tap the expanding direct lending opportunities in India. In late October, BLK and Jio announced the incorporation of two joint venture companies (Jio BlackRock Asset Management Private Limited and Jio BlackRock Trustee Private Limited) to undertake the mutual fund business.

Additionally, at the time of my prior post BLK and HPS Investment Partners (HPS) were in discussions about a potential acquisition by BLK.

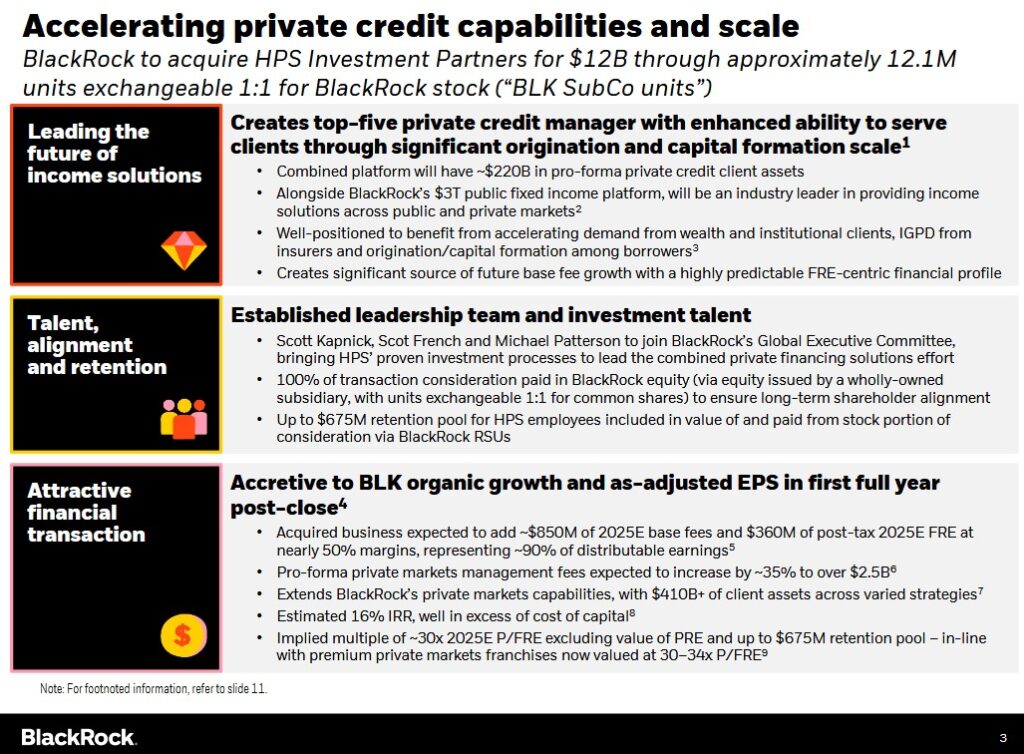

On December 3, 2024, BLK announced its intent to acquire HPS for ~$12B with a target closing in mid-2025. Founded in 2007, HPS is a global credit investment manager with capabilities across the capital structure.

BLK is a leading provider of solutions for insurers, which represent 100 Aladdin technology clients and ~$700B in assets under management (AUM).

HPS’s client base consists of sovereign, pension, insurance, and wealthy retail clients. The addition of HPS will position BLK to be a full-service, fiduciary provider of public-private asset management and technology solutions for a broad base of clients; the acquisition will deepen BLK’s capabilities.

BLK has grown its fixed income capabilities and now serves clients through a $3T platform across:

- Fundamental Fixed Income;

- Financial Institutions;

- Municipals;

- Systematic Fixed Income;

- Index Fixed Income; and

- iShares bond ETFs.

Should this acquisition receive the appropriate regulatory approvals, it will likely increase private markets fee-paying AUM and management fees by ~40% and ~35%, respectively, and be modestly accretive to BLK’s adjusted EPS in the first full year post-close.

Details of the acquisition and payment structure are in the Press Release and accompanying presentation.

The acquisition is to be funded 100% with BLK equity; the equity is to be issued by a wholly-owned subsidiary of BLK and is exchangeable on a one-for-one basis into BLK common stock.

Overview

A comprehensive overview of BLK is in Part 1 Item 1 in BLK’s FY2023 Form 10-K which is accessible through the SEC Filings section of the company’s website. I also strongly recommend reviewing the company’s website.

Financials

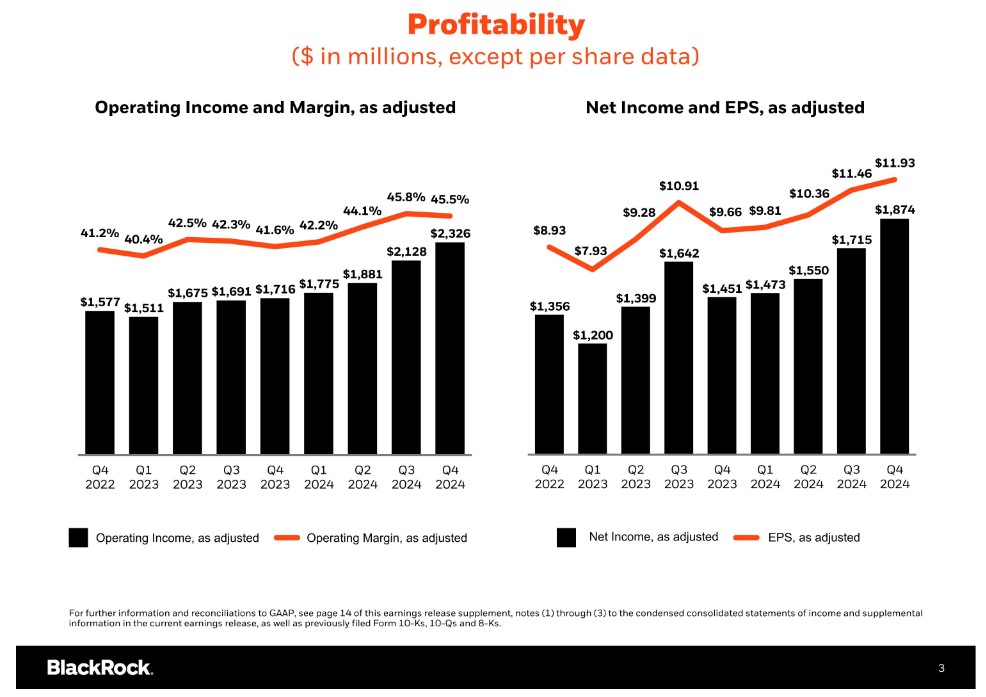

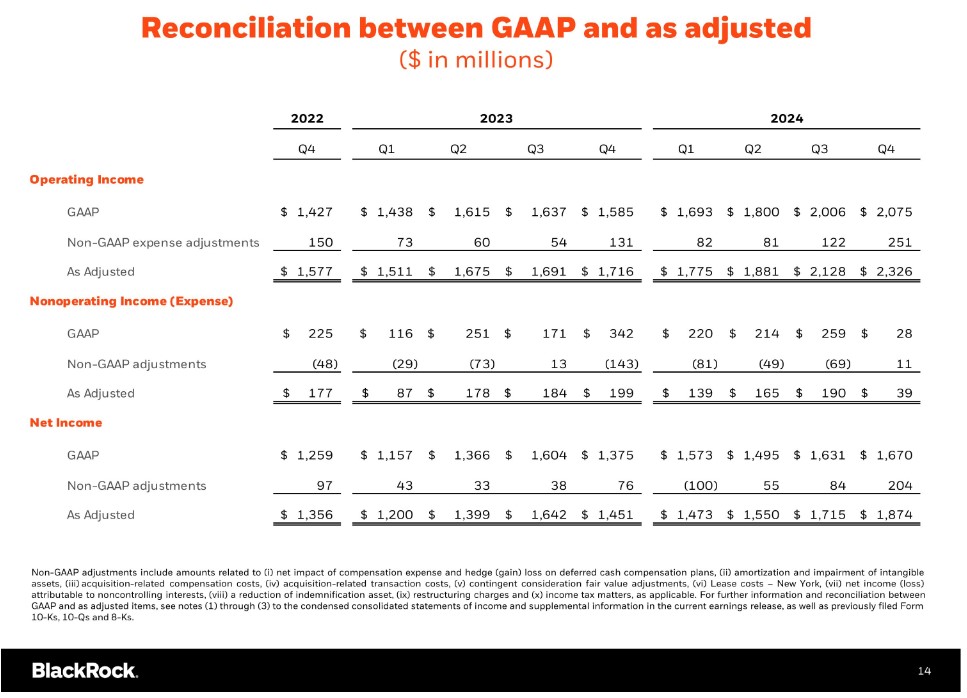

Q4 and FY2024 Results

BLK’s quarterly financial results dating back to 2009 are accessible here.

Capital Allocation

BLK’s capital management priorities are to:

- invest in the business to either scale strategic growth initiatives or drive operational efficiency;

- return excess cash to shareholders through a combination of dividends and share repurchases; and

- make inorganic investments where there is an opportunity to accelerate growth and support strategic initiatives.

FY2025 Outlook

BLK does not provide an outlook for the entire fiscal year. It does, however, state that it will either:

- continue to prioritize investments with differentiated organic growth potential; or

- that will expand operating leverage through enhanced scale.

Risk Assessment

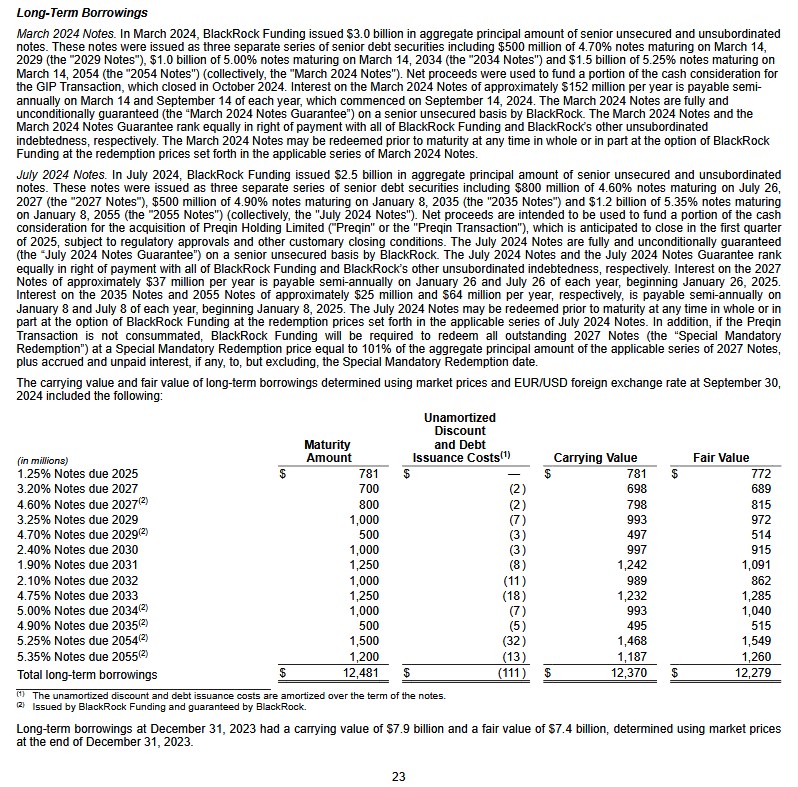

BLK’s 2024 Form 10-K is currently unavailable, and therefore, I provide the following note from BLK’s Q3 2024 Form 10-Q.

Since June 2018, Moody’s rates BLK’s domestic senior unsecured credit Aa3; this rating was affirmed in December 2024. The outlook is stable.

Since May 2014, S&P Global rates BLK’s domestic senior unsecured credit rating AA-; this rating was affirmed in June 2024. The outlook is stable.

Both ratings are the bottom tier in the high-grade investment-grade category. These ratings define BLK as having a very strong capacity to meet its financial commitments. The ratings differ from the highest-rated obligors only to a small degree.

These investment-grade ratings are acceptable for my purposes.

Dividends and Share Repurchases

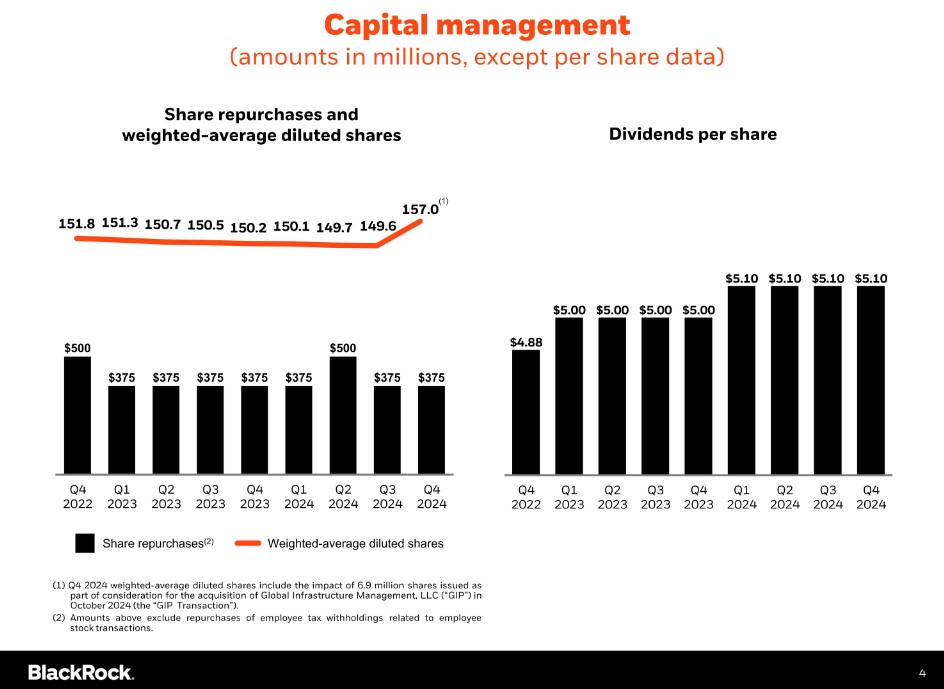

The following reflects the share repurchase and dividend distribution components of BLK’s quarterly capital allocation for the past 2 fiscal years.

Although BLK repurchases shares as part of its capital allocation strategy, the weighted-average diluted shares outstanding surged in Q4 2024. This is because the total consideration for the GIP acquisition consisted of $3B in cash and ~12 million shares of BLK common stock.

If BLK receives regulatory approval to acquire Preqin, the purchase will be made with ~$3.2B in cash. The ~$12B HPS acquisition, however, will be through ~12.1M units exchangeable 1:1 for BLK stock.

The SubCo Units will be exchangeable on a one-for-one basis into BLK common stock at the election of the holder. They will also have equivalent dividend rights to BLK common stock.

The structure of the transaction consideration is as follows:

- ~9.2 million SubCo Units payable at closing; and

- ~25% of the consideration, or 2.9 million SubCo Units, is payable in ~5 years subject to achievement of certain post-closing conditions.

There is also potential for additional consideration to be earned of up to 1.6 million SubCo Units that is based on financial performance milestones measured and paid in ~5 years. Of the total deal consideration, up to $0.675B will fund an equity retention pool for HPS employees.

In aggregate, inclusive of all SubCo Units paid at closing, eligible to be paid in ~5 years, and potentially earned through achievement of financial performance milestones, the maximum amount of BLK common stock issuable upon exchange for SubCo Units would be ~13.7 million shares.

Dividend and Dividend Yield

BLK initiated a quarterly dividend in 2003 (see dividend history).

On the Q4 2024 earnings call, management states its intention to seek Board approval before the end of January 2025 for an increase to the Q1 2025 dividend.

I envision the bulk of the total return from a BLK investment will continue to come from capital appreciation; the dividend component is likely to remain relatively insignificant.

Share Repurchases

BLK’s capital allocation priority is to invest either to scale strategic growth initiatives or drive operational efficiency. After these priorities, BLK returns excess cash to its shareholders through a combination of dividends and share repurchases.

Open market share repurchases were ~$0.375B and ~$1.6B in Q4 and FY2024.

Share repurchases have been a consistent element of BLK’s capital management strategy. Repurchases in the last 10 years amount to 28 million shares at an average price of $510/share.

On the Q4 earnings call, management states:

For both the GIP and HPS transactions, BLK equity proved a valuable currency in consummating these transactions and structuring them for alignment with our shareholders. At present, based on capital spending plans for the year and subject to market and other conditions, we’re targeting the purchase of 1.5 billion of shares during 2025.

Valuation

BLK clearly states that its equity is proving to be a valuable currency. Essentially, BLK would be foolish not to use its richly valued shares for acquisition purposes. If BLK shares were undervalued, I think it would be looking to other means by which to finance its acquisitions.

My October 17, 2024 post reflects BLK’s estimated valuation at prior points in time. For ease of comparison, I include my estimate of BLK’s valuation at the time of my last review.

The share price at the time of my most recent previous post was ~$1015.75. Using this and the broker forward adjusted diluted EPS estimates at the time, I arrived at the following forward adjusted diluted PE levels:

- FY2024 – 13 brokers – mean of $43.28 and low/high of $42.70 – $44.90. Using the mean estimate: ~23.5.

- FY2025 – 15 brokers – mean of $49.19 and low/high of $43.85 – $54.97. Using the mean estimate: ~20.7.

- FY2026 – 11 brokers – mean of $54.76 and low/high of $47.20 – $59.87. Using the mean estimate: ~18.6.

We now know that BLK’s FY2024 diluted EPS and adjusted diluted EPS were $42.01 and $43.61, respectively. Using the January 17, 2025 ~$1006 closing share price, the trailing diluted PE is ~24 and the trailing adjusted diluted PE is ~23.1.

Using the ~$1006 share price and the current broker forward adjusted diluted EPS estimates, the following are the forward adjusted diluted PE levels:

- FY2025 – 17 brokers – mean of $48.21 and low/high of $46.08 – $54.97. Using the mean estimate: ~20.9.

- FY2026 – 15 brokers – mean of $54.09 and low/high of $51.25 – $59.28. Using the mean estimate: ~18.6.

- FY2027 – 8 brokers – mean of $60.37 and low/high of $51.84 – $67.40. Using the mean estimate: ~16.7.

- FY2028 – 1 broker – mean of $59.97 and low/high of $47.20 – $59.87. Using the mean estimate: ~16.8.

I am reluctant to place much reliance on broker estimates beyond FY2025.

The range of estimates are currently quite wide. I envision the variances will shrink over the coming days/weeks once all the brokers have had a chance to complete their analysis.

Final Thoughts

On March 9, 2023, I initiated a BLK position in a ‘Core’ account within the FFJ Portfolio at ~$664/share. I added to my exposure in April and May 2023 @ ~$656 and ~$635 and again in April 2024 @ ~$770. In hindsight, I should have loaded up on BLK shares in early 2023. Instead, I now find myself only holding 160 BLK shares in the FFJ Portfolio.

When I completed my 2024 Mid Year FFJ Portfolio Review, BLK was my 21st largest holding. At the time of my 2024 Year End FFJ Portfolio Review, however, BLK was my 18th largest holding.

My reluctance to immediately add to my exposure lies in what I consider a rich valuation; BLK’s shares offer an insufficient margin of safety and general market conditions are not conducive to being an aggressive acquirer.

Consider BLK’s share price volatility. The historical difference between the annual low/high share price is often significant. As recently as early September 2024, the share price was in the mid $800 range. Has BLK’s business changed so dramatically in 3 – 4 months to warrant a ~$150 increase in its share price? I think not. The acquisitions and joint venture referenced earlier were either close to be being completed or negotiations were public knowledge. This information, therefore, should have been reflected in BLK’s share price a few months ago. I think the share price increase witnessed in recent weeks is because investors are being irrational.

The weighted average diluted shares outstanding increased by 7.4 million shares from Q3 2024 to Q4 2024. If the HPS acquisition closes in the next few months, we can expect the issuance of an additional significant number of BLK shares.

In the first 3 quarters of FY2024, BLK’s stock based compensation (SBC) amounted to ~$0.511B. If it plans to ‘only’ repurchase ~$0.375B of shares quarterly, just under half a year of share repurchases (~$0.75B) will be offset by SBC over a 12 month period (~$0.68B). At this repurchase rate, it will take years of share repurchases to equal the number of newly issued/soon to be issued shares.

If BLK thought its shares were undervalued I suspect the acquisitions would likely have been structured with the issuance of far fewer BLK shares. In essence, given BLK’s view about its shares being valuable currency, it strikes me as an inopportune time to increase my exposure. I think it would be prudent to be patient.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BLK.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.