I initiated a CME Group Inc. (CME) position on June 29, 2020 and have increased my exposure over the years. Several aspects of this business appeal to me one of which is that CME is the world’s leading derivatives marketplace. In essence, CME is a key provider of products for the purpose of increasing or reducing risk.

Since initiating my exposure, CME’s average daily volume (ADV) has been steadily increasing. In November 2024 for instance, CME reported record November ADV of 30.2 million contracts, driven by growth across all 6 asset classes. This increase in activity bodes well for CME shareholders.

I last reviewed CME in this July 29 post at which time the most currently available financial information was for Q2 2024. Subsequently, CME released its Q3 and YTD2024 results on October 23.

In addition, CME announced on December 5 that its Board approved two initiatives to return capital to shareholders. It declared the company’s 2024 annual variable dividend, amounting to $5.80/share payable January 16, 2025, to shareholders of record on December 27, 2024; this totals ~$2.1B. It also authorized a share repurchase program of up to $3B of CME Group Class A common stock, subject to market conditions.

Business Overview

CME is where market participants turn to manage that risk across the most diverse set of benchmark products. It operates a derivatives marketplace which offers a range of futures and options products for risk management.

In prior posts I touch upon CME’s ongoing Google Cloud transformation project; CME announced this transformation project in November 2021. Part of this transformation project included Google making a $1B equity investment in a new series of non-voting convertible preferred stock of CME Group.

I encourage you to review the company’s website and Part 1 of the FY2023 Form 10-K.

Financials

Q3 and YTD2024 Results

The Q3 and YTD2024 earnings release on October 23 and the Q3 Form 10-Q are accessible through the SEC Filing section of the company’s website.

I dispense with a review of these results since the end of Q4 and FY2024 is at the end of December 2024.

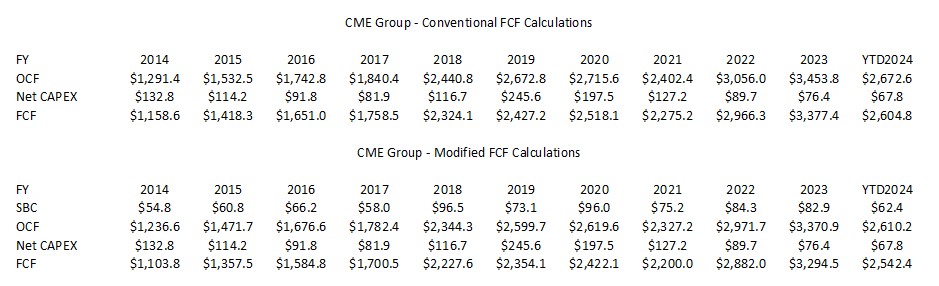

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

In my November 26 Zoom Communications (ZM) post, I provide my rationale for adjusting a company’s OCF and FCF to account for stock-based compensation (SBC).

The following reflects CME’s FCF using the conventional and modified methods. Fortunately, its SBC is nothing remotely close to that of many technology companies!

FY2024 Guidance

CME does not issue any guidance.

Credit Ratings

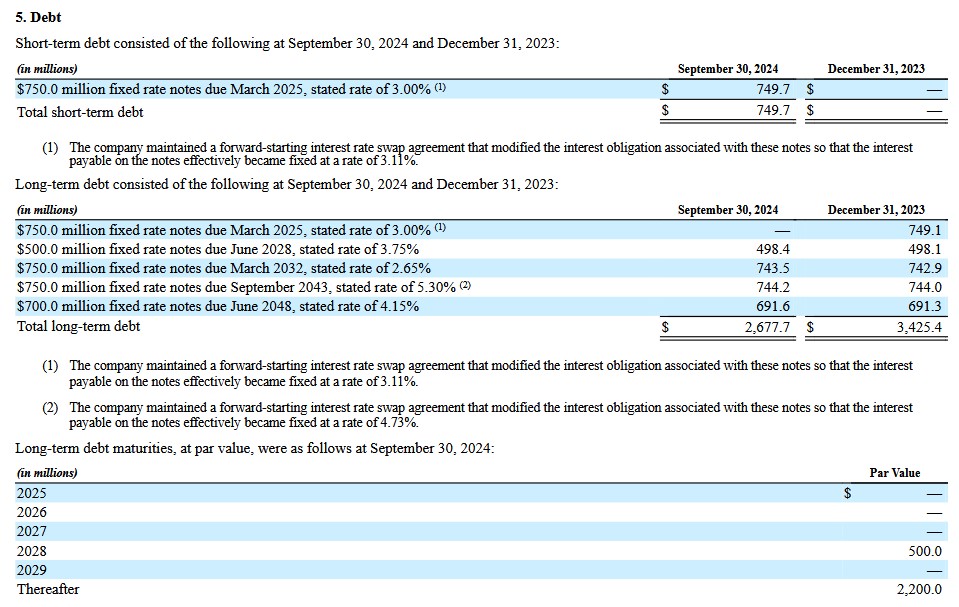

The Q3 2024 Form 10-Q provides an overview of CME’s current portion of long-term debt and long-term debt.

CME’s senior unsecured long-term debt ratings are the lowest tier of the high-grade category and are investment grade. These ratings define CME as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

- Moody’s: Aa3 with a stable outlook (affirmed November 13, 2023)

- S&P Global: AA- with a stable outlook (affirmed January 22, 2024)

- Fitch: AA- with a stable outlook (affirmed February 13, 2024)

These ratings are acceptable for my risk tolerance and I foresee no difficulty in CME being able to repay its obligations on a timely basis.

Dividend and Dividend Yield

CME’s dividend history is accessible here.

As noted earlier, CME will distribute a $5.80 annual variable dividend on January 16, 2025 to shareholders of record on December 27, 2024. This will be in addition to the $1.15 quarterly dividend to be distributed on December 27 to shareholders of record on December 9.

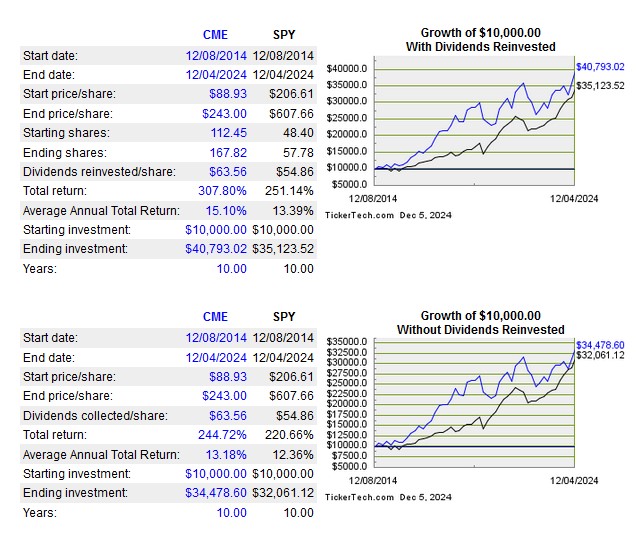

I typically dislike the distribution of dividends and touch upon this in my recent Dividends Have Drawbacks post. The annual variable dividend, however, ‘juices’ CME’s average annual total return to the extent where the average annual total return exceeds that of the broad S&P500.

As a Canadian resident who holds CME shares in taxable accounts, however, I incur a 15% dividend withholding tax. My average annual total return, therefore, is slightly lower than the 15.10% reflected above; I automatically reinvest the dividend income.

If we apply the Rule of 72 (divide 72 by ~15%), a CME investment is likely to double in value in just under 5 years.

CME intends to continue its variable dividend structure. Beginning in 2026, however, the declaration and payment of the annual variable dividend will align with the Q1 regular dividend paid in March 2026 rather than at the end of the calendar year; the Q1 dividend is generally declared in early February for distribution in late March.

Following the recent dividend declaration, CME will have paid a total of more than $28B in quarterly and variable dividends since adopting the annual variable dividend structure in the beginning of 2012.

I anticipate CME will declare an increase its quarterly $1.15 dividend to $1.20 in early February.

In FY2014 and FY2023, the weighted average outstanding diluted shares outstanding (in millions of shares rounded) was 336.063 and 359.550. In Q3 2024, it was ~359.989. At no point within this time frame (nor YTD2024) has CME repurchase any shares. This explains why the number of outstanding shares has risen so much.

CME is unlikely to repurchase $3B of its shares all at once. Hopefully, repurchases will be made when shares are undervalued.

Valuation

CME’s valuation at the time I wrote prior posts is found in my July 29 post.

CME’s current valuation using the ~$244.30 share price as I compose this post on December 5 and the current adjusted diluted broker estimates are:

- FY2024 – 17 brokers – mean of $10.22 and low/high of $10.11 – $10.35. Using the mean estimate, the forward adjusted diluted PE is ~24.

- FY2025 – 17 brokers – mean of $10.38 and low/high of $9.87 – $10.72. Using the mean estimate, the forward adjusted diluted PE is ~23.5.

- FY2026 – 14 brokers – mean of $10.83 and low/high of $10.12 – $11.41. Using the mean estimate, the forward adjusted diluted PE is ~22.6.

The ~$51 surge in CME’s share price subsequent to my July 29 post has resulted in CME now being overvalued.

I am optimistic CME’s FY2024 FCF will exceed ~$3.3B of FCF. I, therefore, use this estimate to gauge CME’s valuation on a FCF basis.

Using ~360 million as a weighted average diluted shares outstanding in FY2024, I estimate CME will generate ~$9.17 of FCF/share (~$3.3B/360 million shares). With a ~$244.30 share price, the forward diluted P/FCF is ~26.6.

I consider CME to be fairly valued at ~$225 meaning shares appear to be overvalued by just shy of $20.

Final Thoughts

Despite the comments in my recent Dividends Have Drawbacks post, I have invested in CME because I like the business and long-term prospects.

One negative aspect of the company is the steady increase in the weighted average diluted shares outstanding. Over at least the past decade, shares were being issued as part of the company’s employee compensation programs. No shares, however, were ever repurchased meaning my share of the company (however small) was being gradually diluted. Fortunately, CME’s Board has approved a $3B share repurchase program. Now, we just have to hope that shares will be aggressively repurchased when they are undervalued.

I currently hold 461 shares in a ‘Core’ account and 401 shares in a ‘Side’ account within the FFJ Portfolio. CME was my 14th largest holding when I completed my 2024 Mid Year FFJ Portfolio Review. I will be performing a similar review at the end of 2024 at which time I will be able to better determine CME’s ranking.

The automatic reinvestment of the dividends (after the 15% dividend withholding tax) will increase my CME exposure. I do not, however, intend to make outright CME purchases while shares are overvalued.

I wish you much success on your journey to financial freedom!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CME.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.